Slouching Toward Phase One

On current trends, goods exports to China will struggle to reach their 2017 level—there won’t be any big gains from the Phase One deal.

By experts and staff

- Published

Brad W. SetserCFR ExpertWhitney Shepardson Senior Fellow

Brad W. SetserCFR ExpertWhitney Shepardson Senior Fellow- Dylan YalbirResearch Associate, International Economics

This is a joint blog post by Brad W. Setser and Dylan Yalbir, a research associate at the Council on Foreign Relations

Once an administration strikes a deal with China, it often ends up finding itself playing the role of China’s defense attorney. Admitting that China isn’t living up to the deal would cast doubt on the wisdom of the initial deal. And right now, it would also raise a second awkward question for President Trump, namely what if anything is he willing to do ahead of the election if China isn’t living up to its end of the bargain. Going back to tariff threats might trigger a stock market sell-off (and it obviously wouldn’t do anything to help contain the virus).

Assigning motive of course is hard. But the Trump Administration’s vigorous defense of the existing deal is still notable, as it is quite clear that China isn’t in fact on track to meet the most visible component of the deal—the purchase requirements.

Now you can argue that the purchase commitments themselves were a mistake—why does the United States care if China is buying U.S. oil (typically from Alaska) rather than Japan or Korea?

And you can argue that COVID-19 changed everything—though the force of that argument has waned a bit as it seems like China has pulled off a V shaped recovery (output in the second quarter should be close to its level in the second quarter of 2019, and the IMF is forecasting that China’s q4 output will be up by 4.4 percent over q4 2019).

But it is very hard to argue that China is on track to live up to its purchase commitments. The business community seems—unusually—more worried here than the Trump Administration.

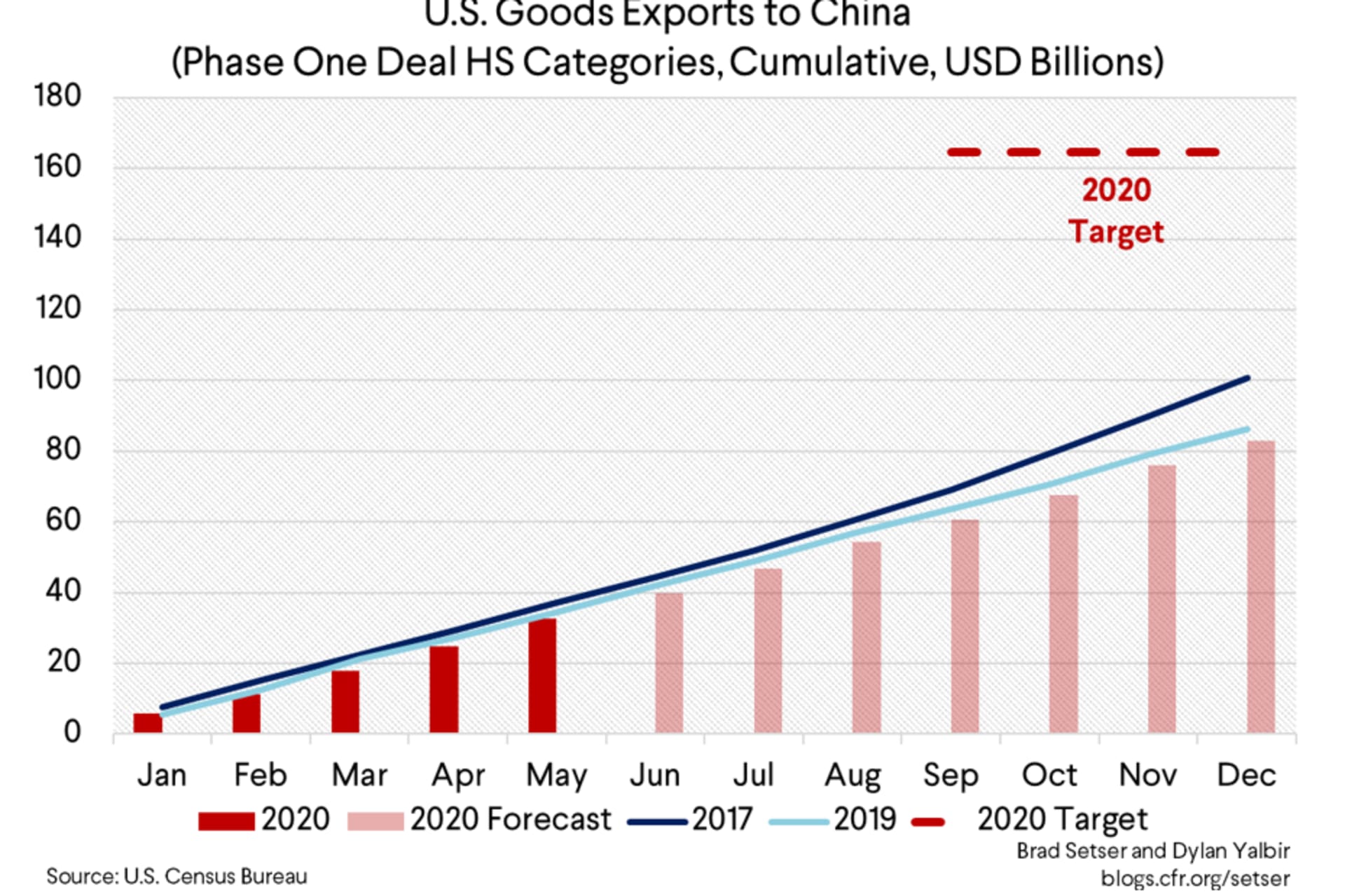

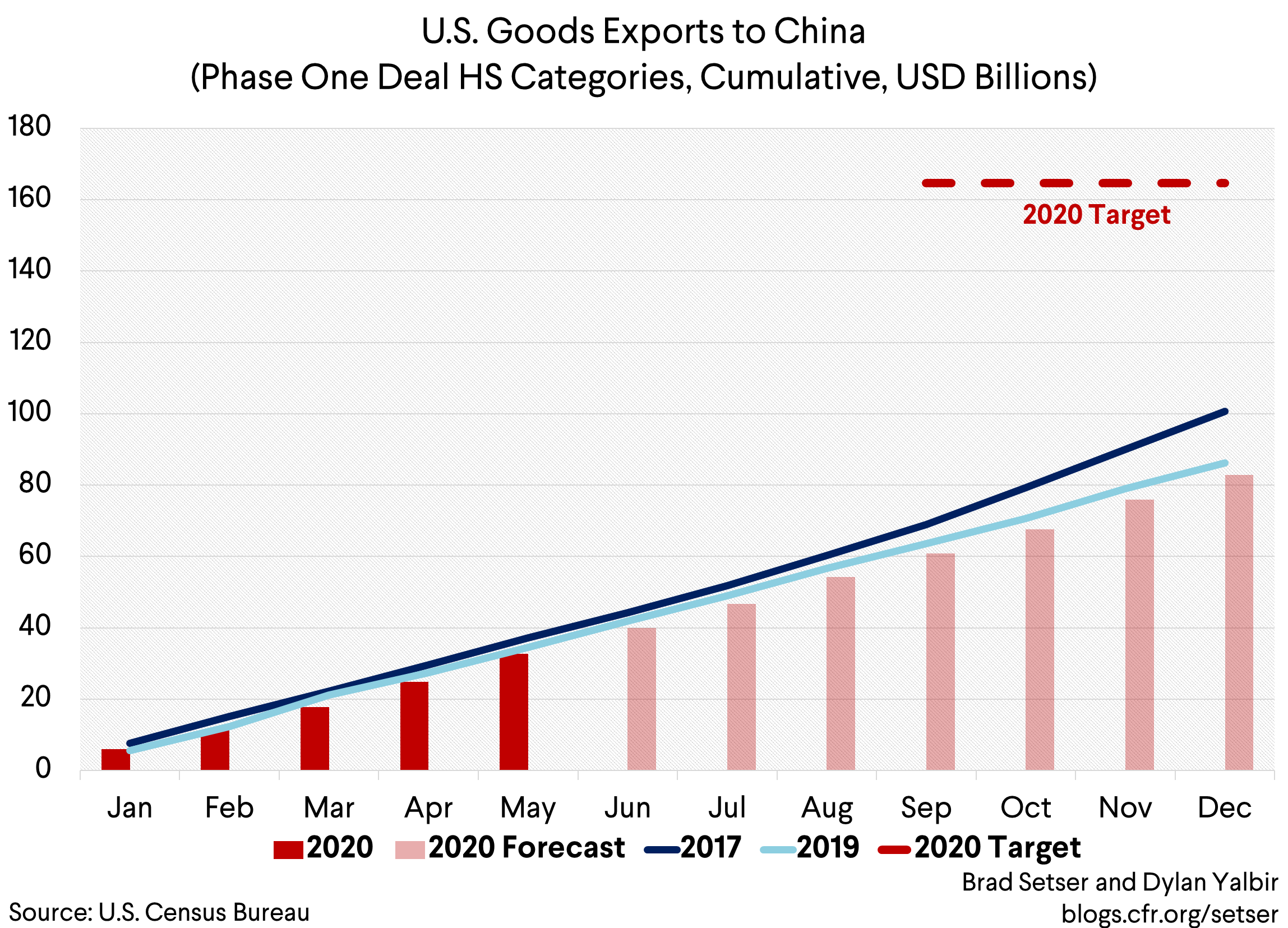

In the Phase One deal, China committed to raise its purchases of U.S. goods and services above its pre-trade war levels—the baseline is 2017, not 2018 or 2019. So in 2020 China needs, more or less, to purchase $60 billion more in U.S. goods than it did in 2017.

To simplify, the target for U.S. goods exports in the categories specified in the Phase One deal with China is $164.65 billion in 2020—a huge increase over the $100 billion exported in 2017 across the HS categories detailed in the text of the Phase One text (PDF, Chapter 6, annex 6.1). Total U.S. goods exports to China clocked in at a bit more in 2017 at $130 billion, so this implies something like $180 billion in total goods exports after adjusting for the (excluded) fall in actual aircraft exports.*

But if the current pattern of export growth from the first half (minus a month for the United States) continues, China would only import ~$83 billion in 2020 across the HS codes listed in the deal text. That would put it below the 2017 baseline of ~$101 billion in these categories—and even below 2019’s annual total of ~$86 billion. Of course, q1 was an exceptional quarter, so it isn’t surprising that China dipped below its targets then. But there isn’t much evidence of a catch up in the data for q2 either.

As a result, targets that seemed ambitious in January now seems close to impossible.

A closer look at the data by each category outlined in Phase One—manufacturing, agriculture, and energy—shows that in addition to not addressing the larger structural issues that have long generated conflict in the U.S.-China relationship, the trade deal may struggle to deliver the much heralded increase in headline purchases.

Manufacturing

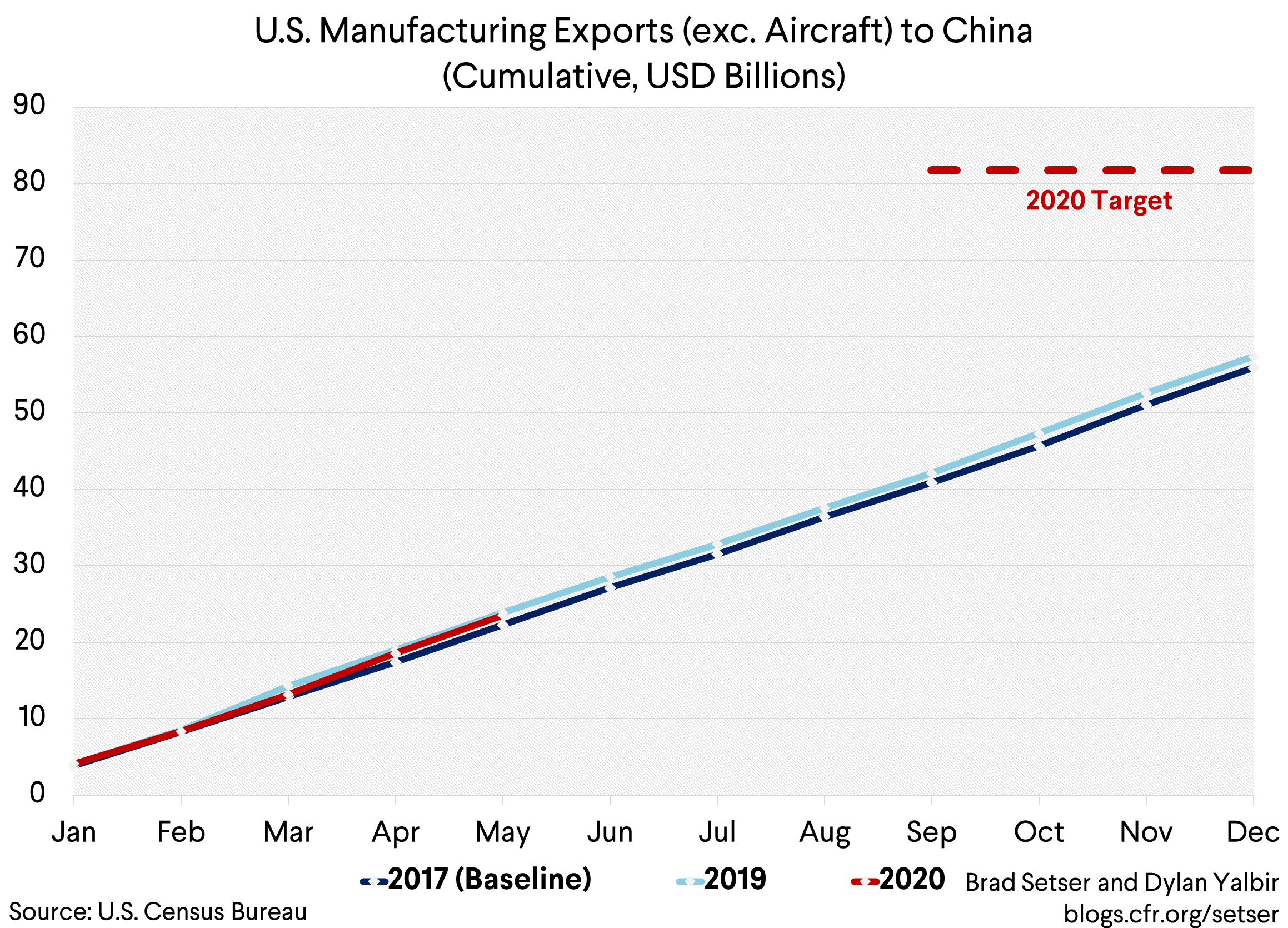

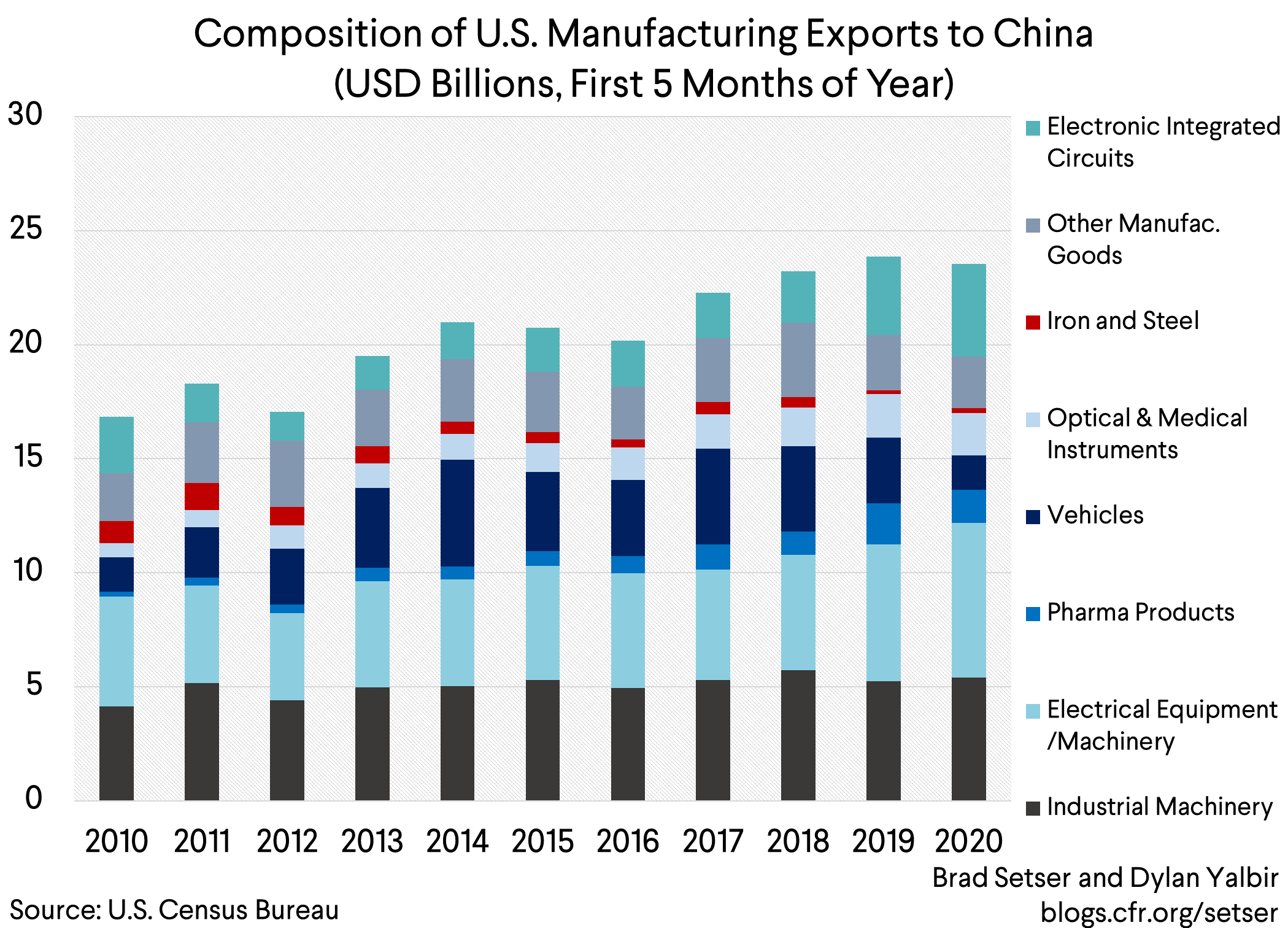

Manufacturing is a difficult category. China doesn’t import many manufactures for its own internal use, and the United States isn’t a particularly big exporter of manufactures. As a share of China’s GDP, U.S. exports of manufactures have been declining for a long time (i.e. the pace of growth has failed to keep with the growth in China’s economy).

And, well, the largest single category of manufacturing exports—aircraft—has been in free fall since the 737 MAX was grounded last year.

The U.S. auto sector —an important source of U.S. manufactured exports to China —also had a difficult May.

But manufactures were also the category of U.S. exports (somewhat strangely) least affected by the trade war. The best way to understand this is that China still needs to (or wants to) import the bulk of what it still imports from the United States—think of the equipment needed to manufacture cutting edge chips, and some actual chips.

So if you set aside aircraft, U.S. manufacturing exports to China so far this year have largely been in line with exports during the same period last year and in 2017.

But a breakdown of the specific categories that make up manufacturing also suggests it would be difficult for China to rapidly increase purchases over the remainder of the year in order to exceed the 2017 baseline by roughly $26 billion. Imports are in fact a bit down compared to the first five months of 2019… and since China hasn’t exactly given up on its strategy of import substitution, it is a little hard to see what policies China would implement to raise its imports here. Manufacturing isn’t like agriculture or energy, where the bulk of trade flows through a few big state-owned firms.

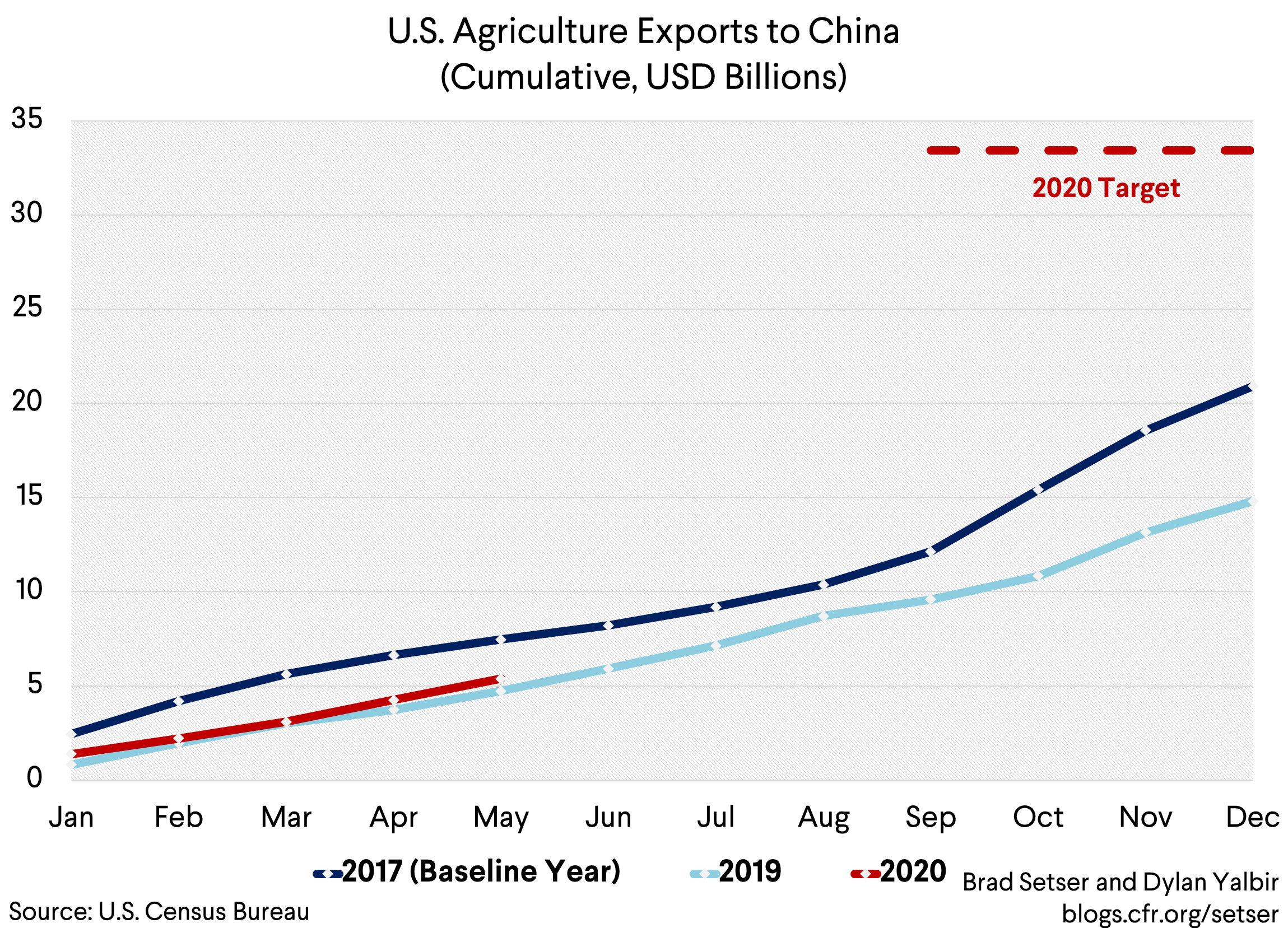

Agriculture

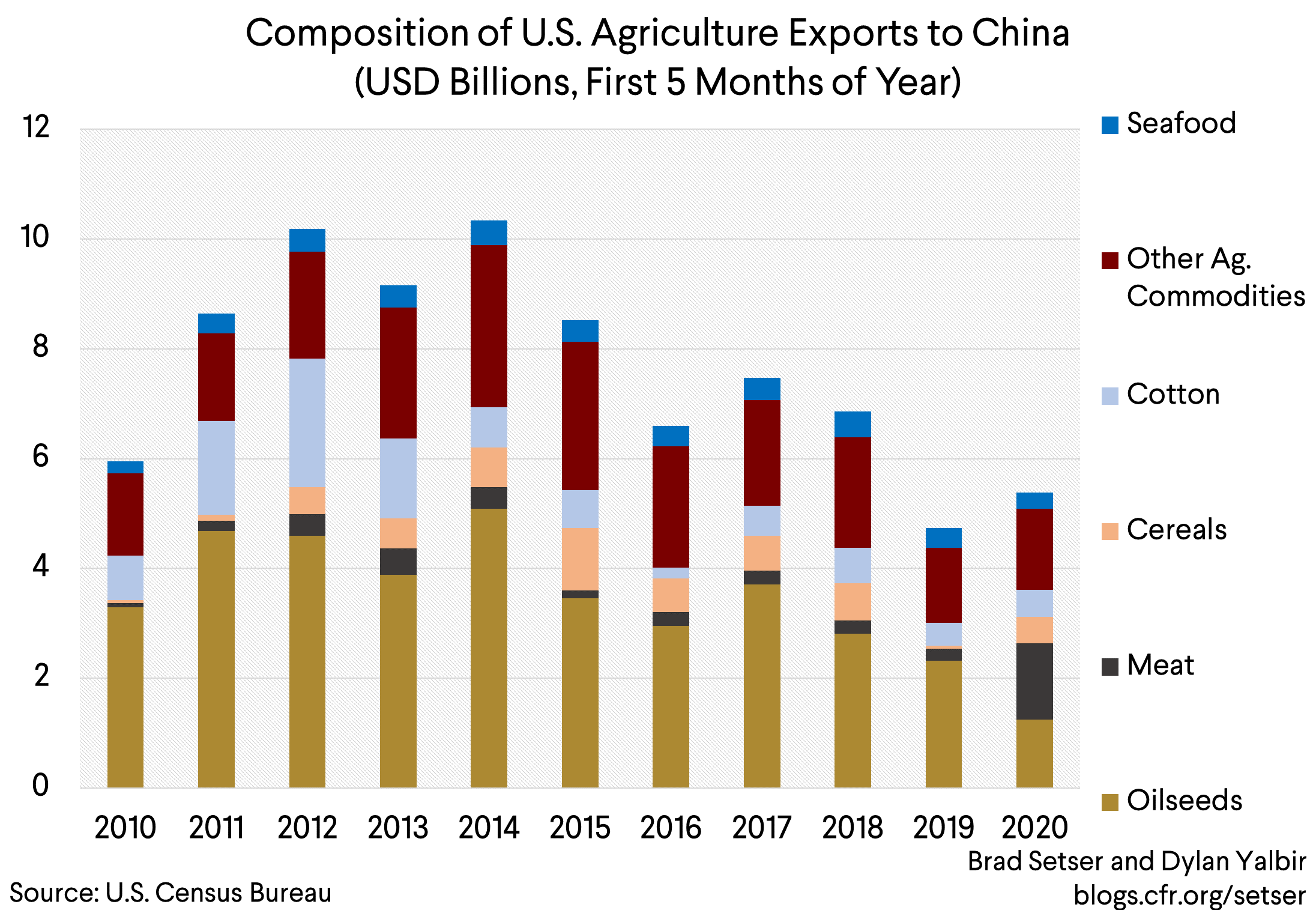

Agriculture is an important category for the United States, and not simply because of the outsized political impact of Iowa’s soybean farmers. Soybeans are the first or second largest category of U.S. exports to China, depending on the price of ‘beans and the number of aircraft delivered in a given year. And some agricultural export categories, notably pork, offered obvious scope for growth.

It is thus a bit surprising how weak overall U.S. agricultural exports to China have been this year. Exports are tracking their (depressed) 2019 levels, not their 2017 levels. They certainly aren’t showing the kind of growth promised.

The product by product breakdown is especially important here—

Meat exports are up significantly (that’s mostly poultry parts and pork), but exports of the almighty bean have lagged. They actually picked up a bit in May, but it is hard to make up for a weak q1 in the off season for U.S. agricultural exports. And with Brazilian exports of beans to China surging in the first half of 2020 (the Brazilian real is also very weak, so American farmers face some real competition), it isn’t entirely clear that China can make up for a weak start of the year after the harvest.

This though could be put differently. China hasn’t delivered upfront—but it in theory still could deliver on its agricultural commitment in q4, which means that there is an obvious cost to breaking off the broader deal now. With a deal, there is some change soybean exports might jump in the fall. With a failed deal, they would almost certainly falter. That’s the price paid by any President who has staked so much political capital on a deal whose implementation depends on the purchasing decisions of China’s state.

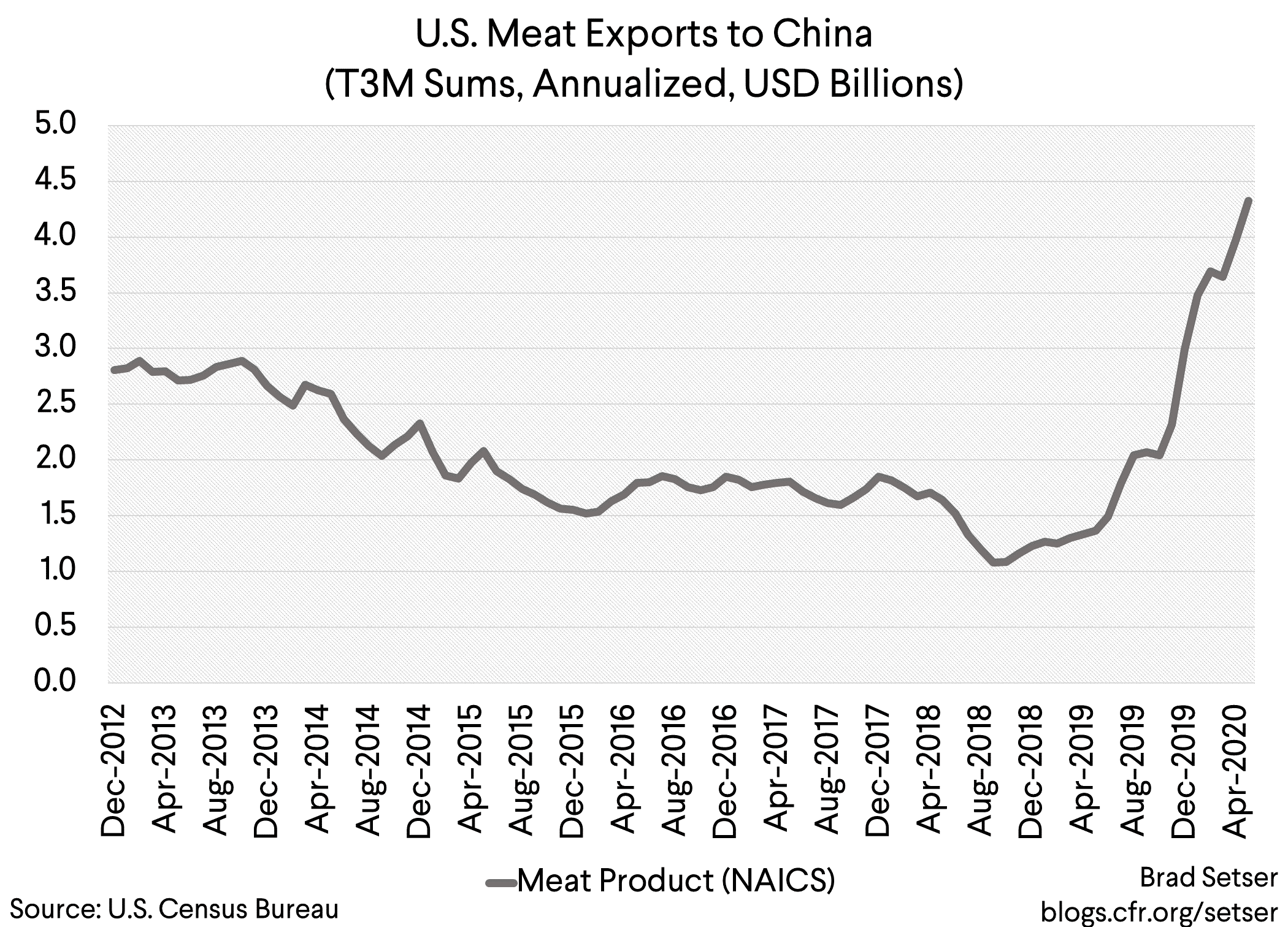

U.S. meat exports to China by contrast have surged in the first five months of the year—partially on the back of pork exports brought on by the African Swine Flu that has decimated China’s domestic pig stock, and partially off the renewal of the chicken parts trade (or chicken paws). Meat exports are on track to triple (versus 2017, using the NAICS code for meat product exports) .

As for seafood, despite the recent coronation of Peter Navarro as a lobster king, U.S. exports of the crustacean are still pretty limited. The lobster harvest last year was poor, air links have been severed reducing the scope for the “live” trade and the traditional export season to China won’t come again till after the election (though China could take up any frozen supplies). Ultimately though the numbers here are modest relative to the scale of the soybean trade—$250 million in a good year vs. over $12 billion of beans.

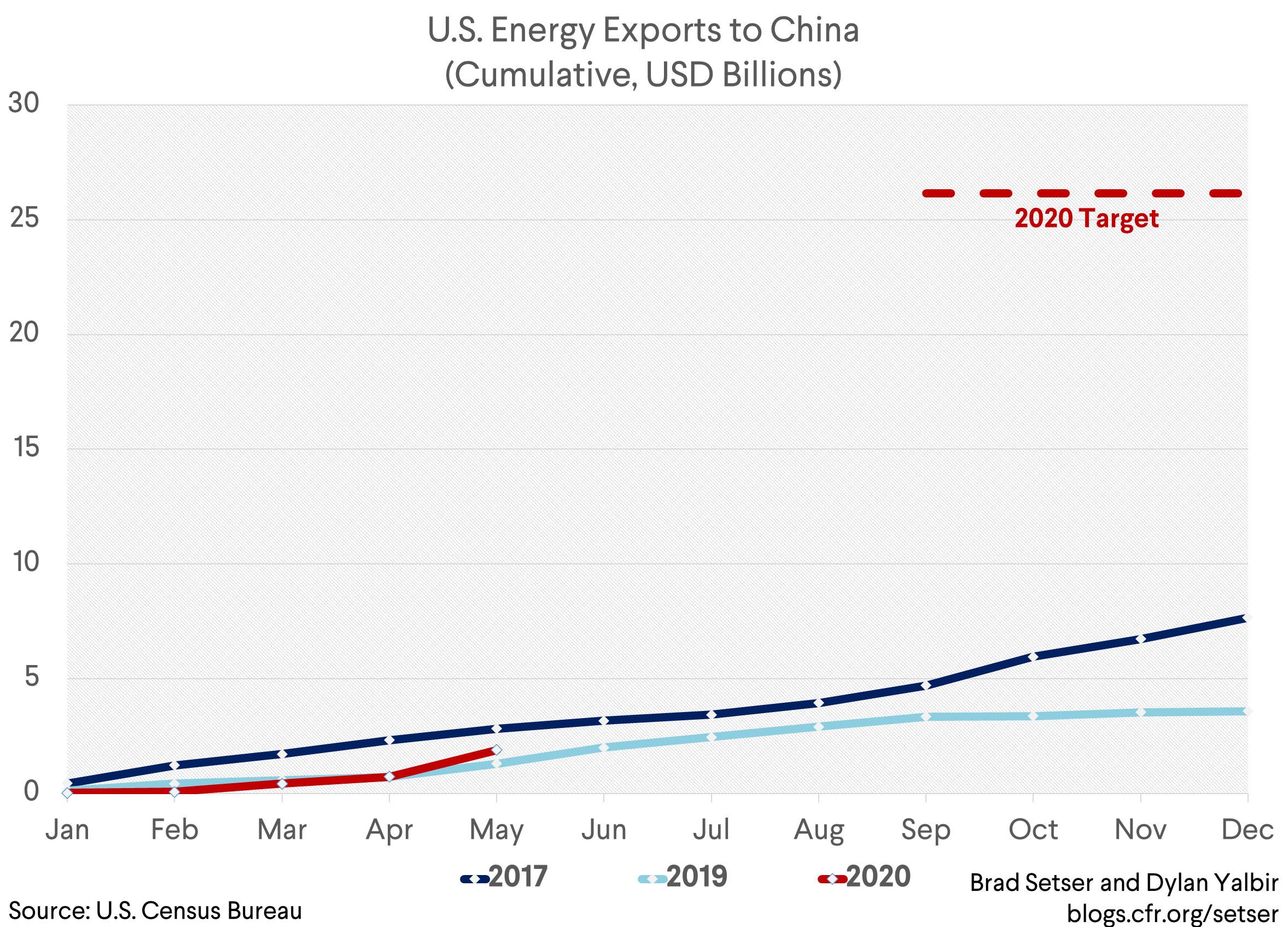

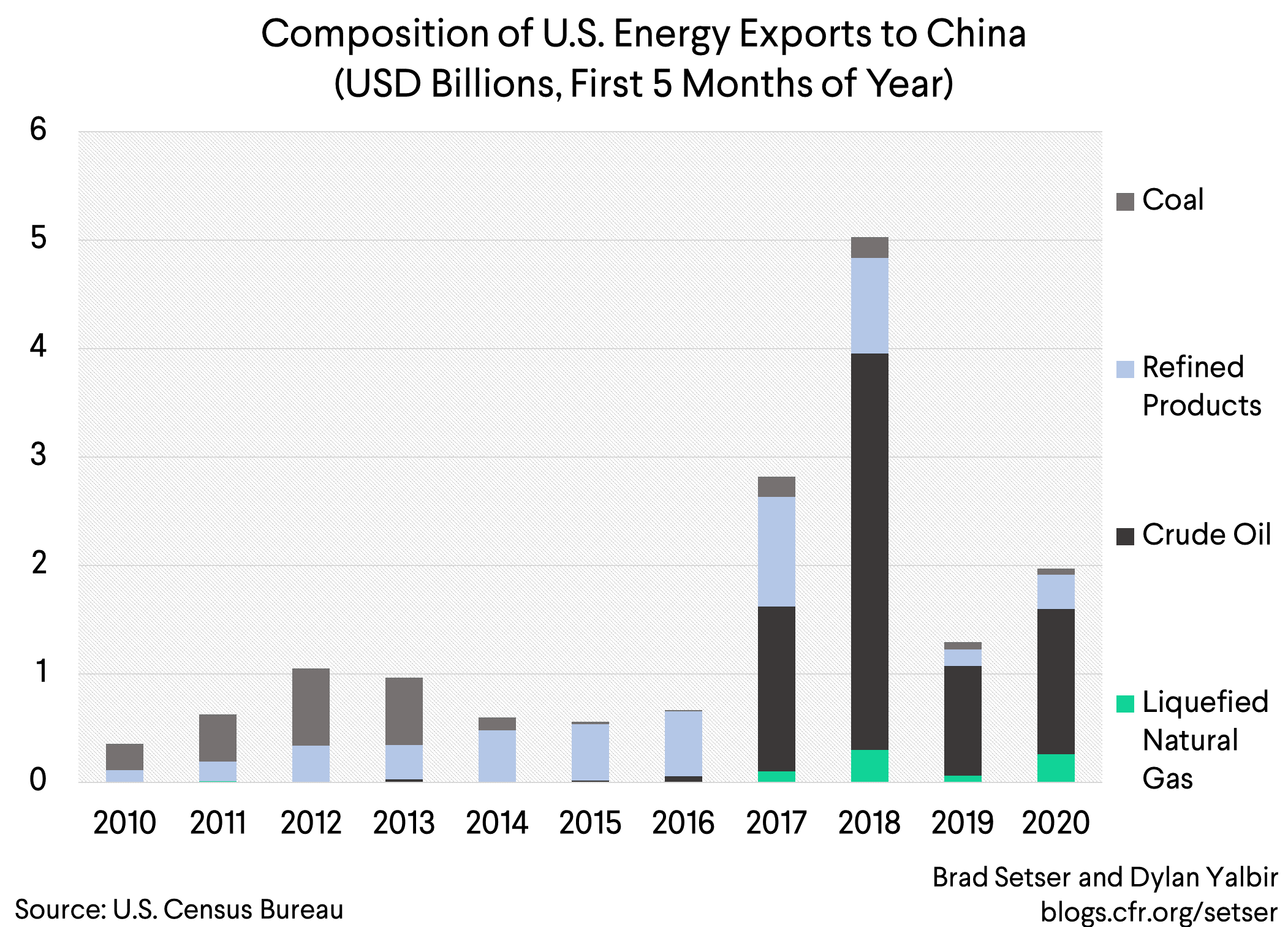

Energy

Energy exports have enormously lagged the ambitious Phase One target—through the first five months, total exporters were only 7 percent of the $26.14 billion target. U.S. energy exports to China largely track 2019—which won’t cut it. Energy exports did jump to $1 billion a month in May—but the target implies an annual average of $2 billion a month or so, which is basically impossible to meet at this stage.

China’s energy imports from the United States are LNG, crude oil, coal, and various refined products with crude accounting for the majority of those imports over the past few years. Now in theory that does allow China some scope to catch up—but only if it really tilts its purchases away from other suppliers.

Reuters notes that after a dismal first six months of imports, China is slated to import just over 31 million barrels of crude from the United States in July or about 1 million barrels per day. If by some miracle, China were to keep the 1 million bpd pace for the rest of the year (August forward purchases are currently below that) and the price of WTI remains steady at the ~$40 level, the article further notes that U.S. exports to China for the year would only amount to $7.36 billion. That still would fall short of matching the 2017 baseline amount of $7.64 billion. Price matters here, given the that the target was laid out in nominal terms.

Can refined products or LNG pick up the slack? Unlikely.

At their peak over the past decade, refined product exports reached $1.95 billion in 2017. Even if Chinese state purchasers do encourage an increase in purchases over the 2017 peak, products that fall under this category like pet coke are plagued by the same COVID-19 related price drop that crude has suffered from during the H1 2020.

LNG? With a 2010s peaks of ~$365 million in 2017 and U.S. natural gas prices above that of competition in Europe and East Asia, LNG seems unlikely to help cover the gap. Over 40 U.S. LNG cargoes for August were canceled by buyers according to S&P Global.

Conclusion

The Phase One deal’s clear numerical targets provide a simple and transparent way of assessing the deal’s success—and by insisting on targets that sound impressive, Trump ironically made it easier to show that this particular deal is failing on its own terms.

A different deal—one focused less on headline purchases and more on removing specific barriers (the tariffs and health rules that limited trade in chicken parts and the like) might have delivered sector specific gains without so obviously falling short of the overall target. But it wouldn’t have tried to mobilize the undeniable purchasing power of China’s state to raise U.S. exports—and for better or worse, that became a clear goal of the Trump administration. And it wouldn’t have lent itself to Trump’s showmanship, as a barrier-by-barrier calculation of likely gains wouldn’t have produced a big number.

Yet defending this deal when China is falling so obviously falling short of the numerical targets will make the Trump administration’s recent shift toward being China’s (trade) defense lawyers all the more striking.

Right now though the question isn’t whether or not China will deliver on its full Phase One purchase commitment. Rather it is whether U.S. exports in 2020 will significantly exceed their 2019 levels—getting back to 2017 levels of trade would, based on the data from the first five months, be a reach.

* Services have been excluded for two reasons: one, the Administration has been using fuzzy math here from the start as it counts in-China sales of financial services (not an export by any definition) toward meeting the targets; and two, for services exports, COVID-19 really did change everything. Travel services (tourism) accounts for a very large share of U.S. services exports. IP exports tend to be booked in firms global tax headquarters, and thus don’t register strongly in the actual trade data.