Singapore’s “Shadow” Intervention

Singapore looks to have resumed intervention in the foreign exchange market

Singapore gets a free pass in the U.S. Treasury’s foreign exchange report because of its small size, and because the U.S. exports more to Singapore than it imports. But the U.S. bilateral surplus with Singapore is deceptive. Singapore imports to re-export, not to consume. It has a 20 percent of GDP current account surplus for a reason.*

And, well, Singapore has a long history of managing its currency heavily—and not always showing its intervention in the most transparent way.

I can understand Singapore’s desire to manage its currency. Its small size makes it hard to conduct monetary policy using domestic assets alone. And Singapore has made it even harder through its history of running a tight fiscal policy, limiting the available supply of public debt: according to the IMF, Singapore has run a general government surplus every year since 1990 (though the surplus was tiny in 2009).

But even if Singapore is a country that should manage its currency against an external target, it is fair to ask if it has always targeted an appropriate level for the Singapore dollar. Especially given the size and persistence of Singapore’s external surplus.**

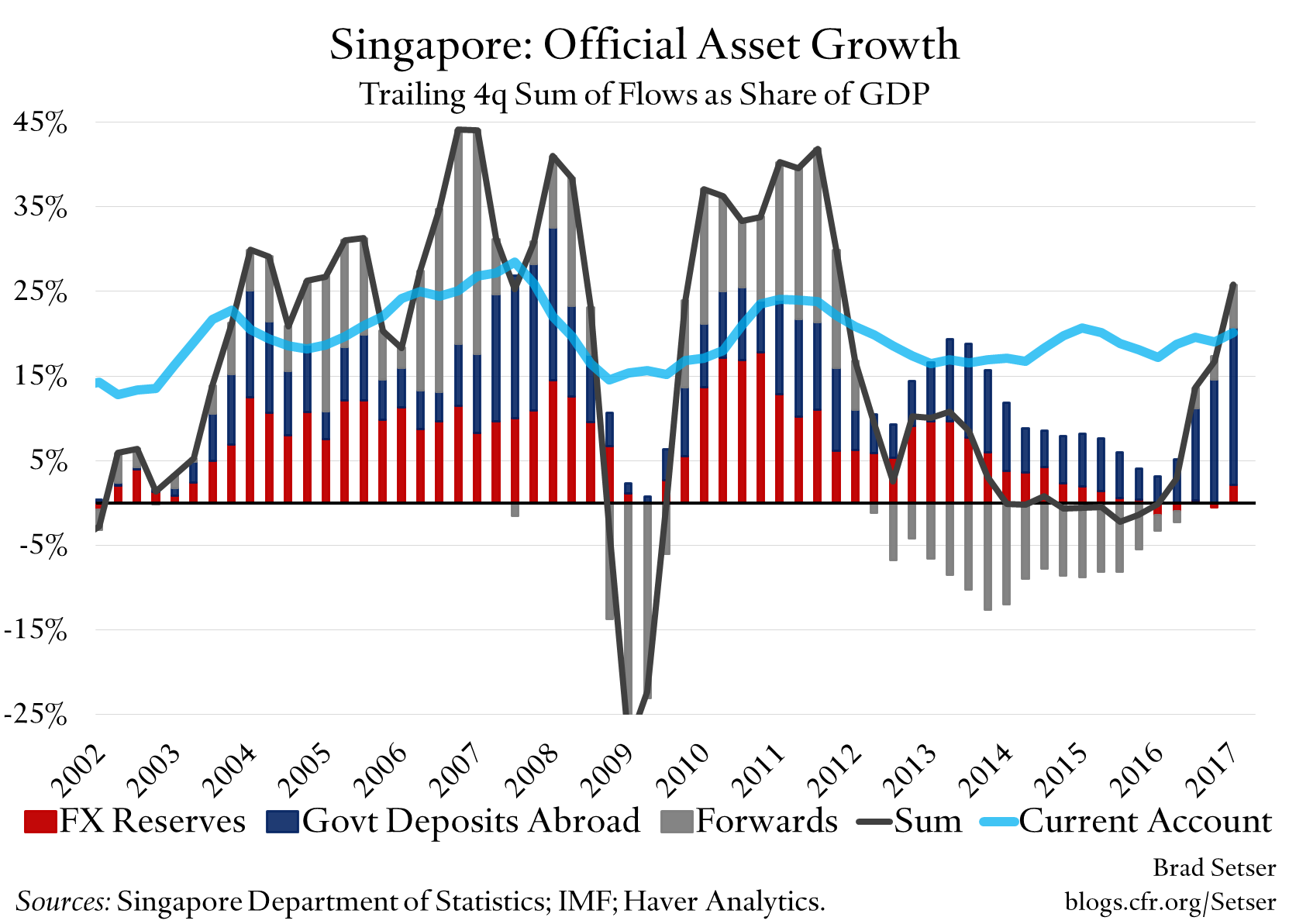

I think intervention—properly measured—generally exceeded Singapore’s current account surplus from 2003 to 2012 (apart from the period around the global crisis). That is the period Joe Gagnon and Fred Bergsten call the decade of intervention.

Intervention then fell to about zero during the Chinese growth and currency scare, which depressed the exchange rate of most emerging Asian economies. The dollar’s broad strength mattered here too.

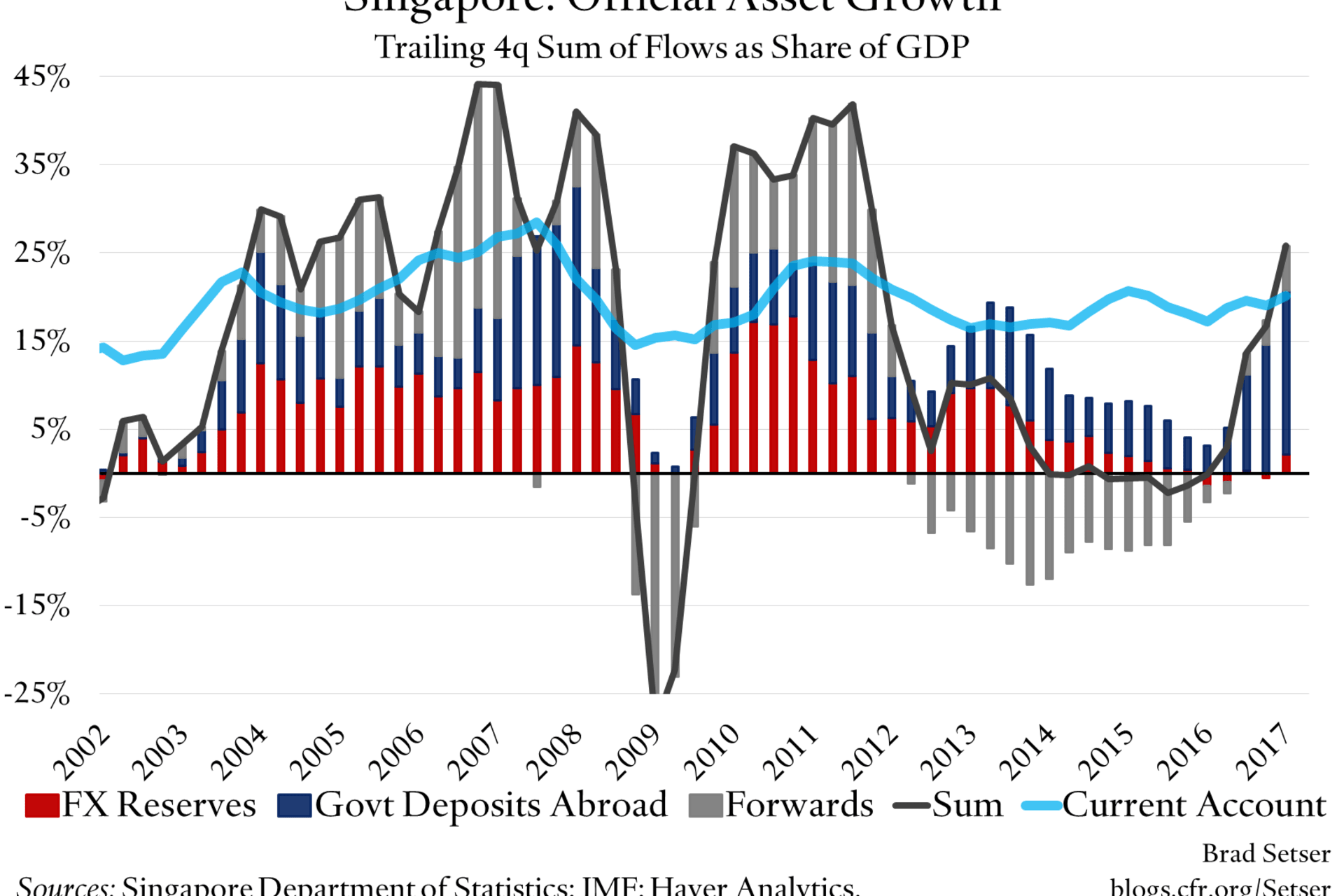

But something appears to have changed in the last four quarters. Singapore’s government is once again accumulating foreign assets at a rapid clip.

No one would know though only by looking at headline foreign exchange reserves, or by looking at the corresponding line item in the balance of payments (reserve outflows).

Headline reserves leaves out Singapore’s forward book—which has increased $11.5 billion over the last four quarters.

And the forward book isn’t the only source of action. Government deposits abroad have soared.

Combine the growth in reserves, the increase in the forward book, and the growth in deposits, and my estimate for total intervention over the last four quarters has risen to close to 25 percent of Singapore’s GDP.

This isn’t the first time that looking at government deposits has been important. In 2013 and 2014 Singapore’s forward book fell at a rapid clip. Singapore looked to be, in effect, selling off reserves to prop up its currency (technically, Singapore would have needed to take delivery of the foreign exchange it had previously bought forward and then sell spot). But it turned out the fall in the forward book was matched almost dollar for dollar by a rise in government non-reserve deposits abroad. The government likely took delivery of dollars the Monetary Authority had bought forward and then put the dollars on deposit as a non-reserve asset at Singapore’s sovereign wealth fund. Or some such.

I assume something similar is going on now. The sharp rise in government deposits abroad looks and feels like backdoor intervention—just in a way that doesn’t register on the central bank’s balance sheet.

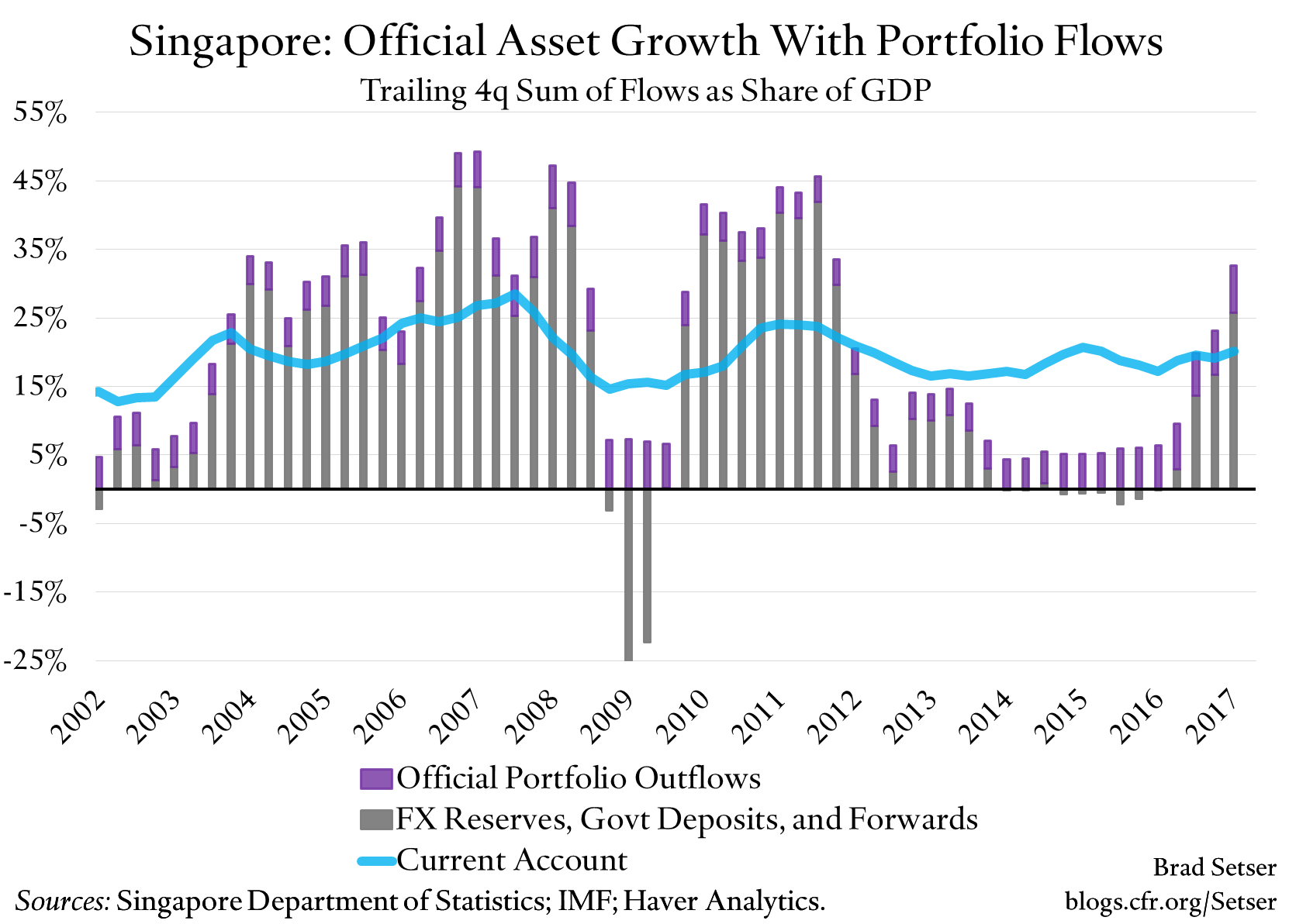

I haven’t added Singapore’s portfolio outflows—the purchase of foreign securities by government accounts—to my estimate of Singapore’s intervention. Some of those purchases likely come from Singapore’s state run retirement funds.

Singapore on its own doesn’t have a huge impact on the global balance of payments. But its reliance on hidden ways of intervening does point to a broader issue, one that I would encourage the U.S. Treasury to look at closely: less and less of the global growth in government assets abroad is showing up directly on central banks’ balance sheets. Singapore’s wealth fund. Korea’s government pension fund. China’s state banks.

* A couple of examples. Singapore is a petroleum refining hub. One of the biggest U.S. exports to Singapore is fuel oil. Another sizeable export is petroleum drilling equipment. That certainly isn’t used in Singapore (is there a big leasing business?). Another is semiconductors, which are likely reexported. Another is organic chemicals, which likely are inputs in Singapore’s pharmaceutical businesses. Another is aircraft, probably a reflection of both Singapore Airlines and some leasing companies. One of the reasons why I like the bilateral data is that can provide clues to tax-related distortions—like Australia’s large exports of iron to “marketing” hubs based in Singapore.

** To be sure Singapore’s surplus reflects a range of domestic policy settings—not just its currency policies. The current account surplus clearly is in part a reflection of its tight fiscal policy and the large required contributions to the provident funds, who clearly have been conduits for moving Singapore’s savings abroad.