Thailand: Currency Manipulator?

The Trump Administration seems to think of currency manipulation primarily as an issue with China.

But “currency” actually is a much broader issue.

Korea, Taiwan, and Singapore all have bigger current account surpluses, relative to their GDP, than China does. All have intervened to limit the appreciation of their currency within the past year. And all three have a long history of intervention, even if they intervened somewhat less when the dollar was exceptionally strong between the middle of 2014 and the middle of 2017.

But the country that comes closest to meeting all three of the numerical criteria the Treasury now uses, following the Bennet amendment, to determine whether or not a country qualifies for “enhanced bilateral engagement” (what used to be called manipulation) is Thailand.

Yep, Thailand.

The three criteria are:

- Intervention (purchases, I assume) in the foreign exchange market in excess of two percent of GDP.

- A current account surplus in excess of 3 percent of GDP.

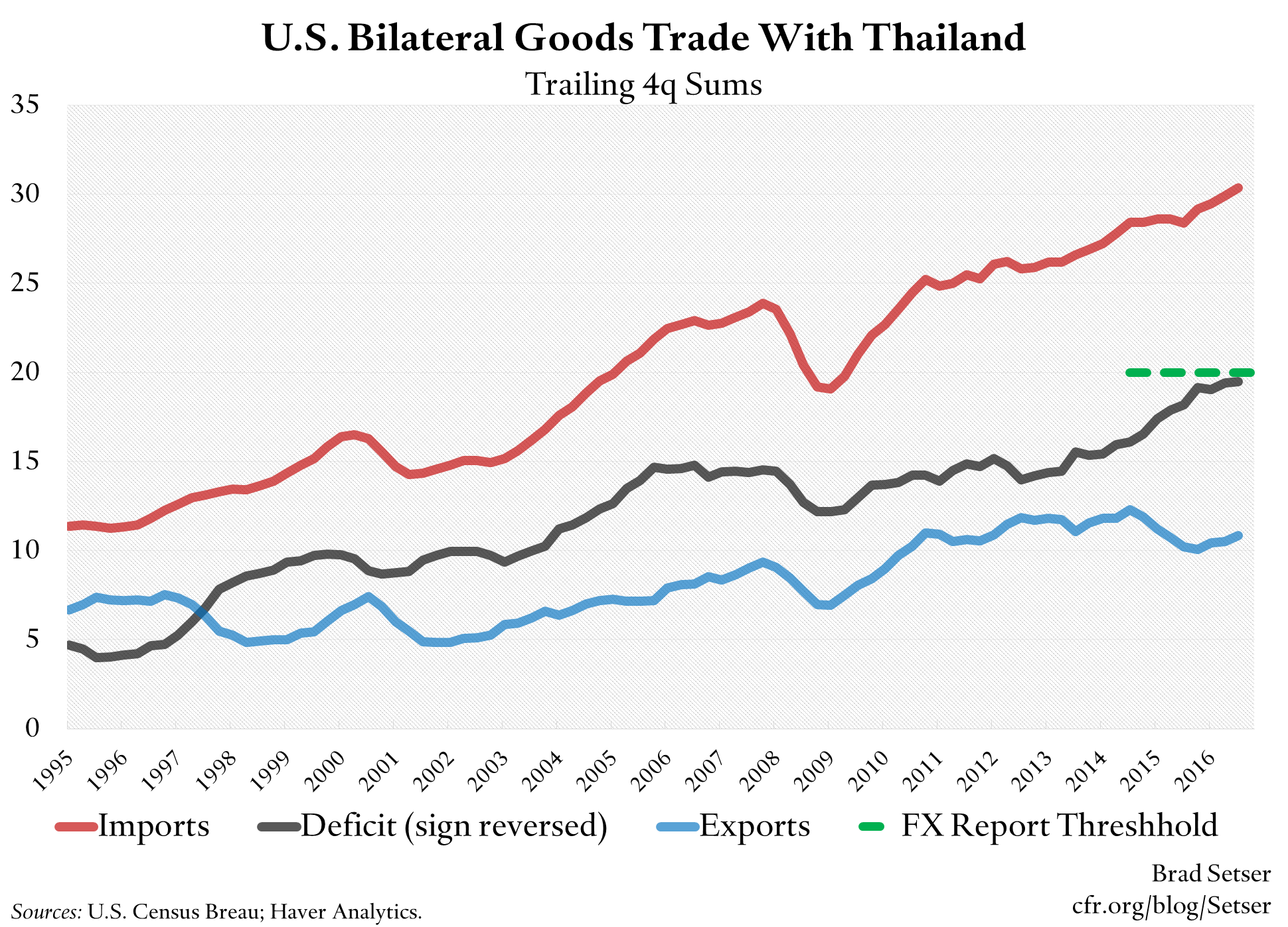

- A bilateral goods surplus with the U.S. of more than $20 billion dollars.*

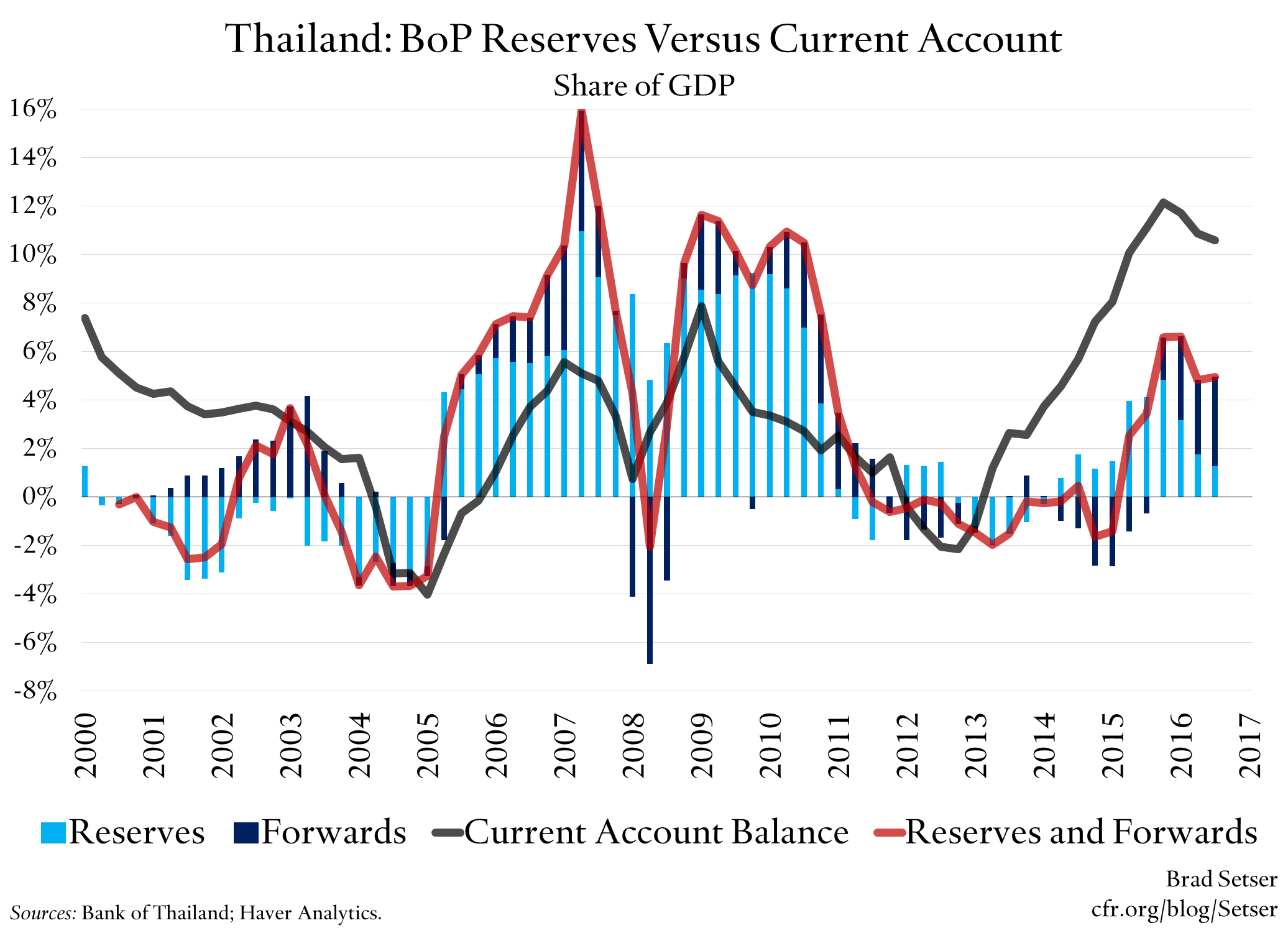

Thailand easily meets the first two criteria. Its current account surplus has soared after the baht’s depreciation in 2015, and now is close to 10 percent of Thailand’s GDP. 10 percent of GDP is a big number—it is higher than Germany or Korea right now. And roughly equal to China’s pre-crisis surplus at its peak.

Thailand’s intervention in the foreign exchange market—including its intervention in the forward market—topped five percent of its GDP in the last twelve months of balance of payments data. Thailand’s reserves rose strongly in July and August, so there is no doubt Thailand continued to intervene throughout the third quarter.

So it all comes down to the third criteria: a bilateral goods surplus with the U.S. in excess of $20 billion.

And Thailand comes close. Very close.

Its bilateral goods surplus in the last four quarters of U.S. data is above $19 billion…

Changing the criteria to include services wouldn’t let Thailand off the hook. In 2015 Thailand ran a small bilateral services surplus with the U.S. (see table 2.2 or table 2.3 in the services trade data interactive tables; 2016 data isn’t yet available, the services data comes with a long lag and the bilateral data isn’t especially reliable). Remember the U.S. services surplus is mostly tourism—not anything more highfalutin (most services are still hard to deliver across borders and across time zones, and, well, our IPR giants tend to understate their intellectual property exports for tax reasons). And Thailand is also strong in tourism: the United States (like China) runs a bilateral tourism deficit with Thailand.

Thailand historically hasn’t been covered in any detail in the foreign exchange report. It isn’t on the monitoring list in the last foreign exchange report.

It hasn’t been “put on notice” so to speak.

It should be. Based on current trends, Thailand’s bilateral surplus is likely to exceed the $20 billion threshold soon.

Of course, there is an elephant in the room: Thailand’s 1997 crisis, and Thailand’s belief that the U.S. didn’t provide it with as much assistance back then as say it provided to Mexico.**

But a crisis in the 1990s shouldn’t be a free pass twenty years later. Neither Thailand nor for that matter Korea should get “a get out of jail free” card now because of events twenty years ago.

Thailand got into trouble in 1997 for a host of reasons: a credit-fueled real estate boom produced a large current account deficit, a lot of real estate companies took out a lot of foreign currency denominated debt even though they lacked foreign currency revenues, and the Thai banks and finance companies funded their domestic foreign currency lending with risky short-term borrowing.

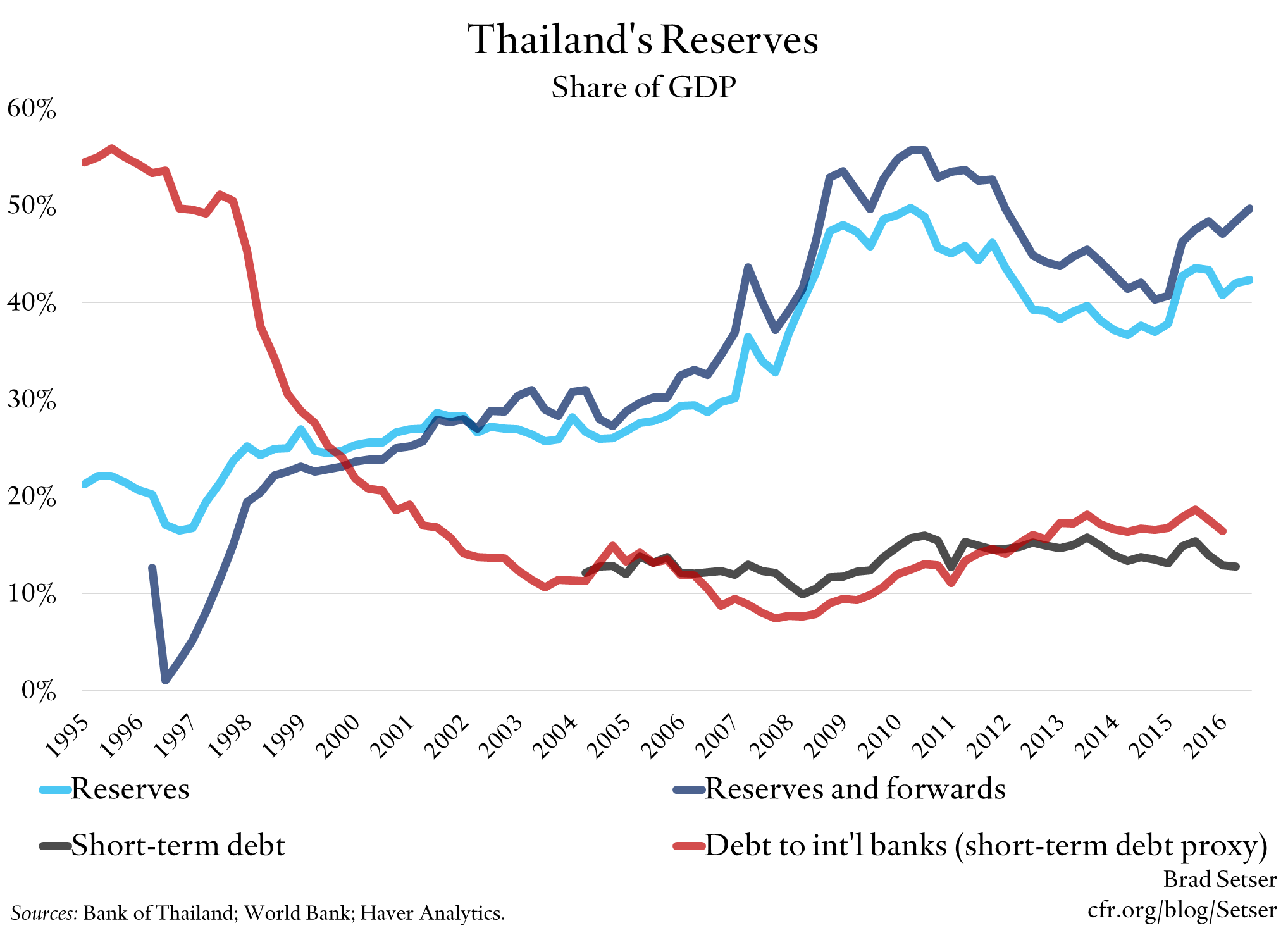

But it also fundamentally lacked enough reserves back then. Overall reserves weren’t high absolutely, and it turns out that Thailand had sold off a large fraction of its reserves in the forward market trying to defend the baht, so it really had almost zero in the bank. At the end of the second quarter of 1997, Thailand had about $30 billion in headline reserves, and had sold almost $30 billion forward. It literally had nothing in the bank.

Thailand’s reserves, though, are way bigger now—absolutely, and relative to short-term external debt.

Thailand has $180 billion plus in reserves, and has bought $30 billion in the forward market—so its reserves are higher than the headline number. Total reserves, counting forwards are about 50 percent of Thailand’s GDP—and its short-term debt is only a bit over 10 percent of its GDP.

So while Thailand absolutely needed to rebuild its reserves and bring down its debt after its 1997 crisis, it subsequently has gone overboard—and is pretty clearly now intervening to hold its currency down, not because it needs more reserves to protect itself from another crisis.

A current account surplus of 10 percent of GDP and reserves of close to 50 percent of GDP makes Thailand a small-scale version, numerically, of China back in 2007 or so.***

And, well, Thailand’s intervention does have an impact on the U.S. economy.

Thailand is a big producer of auto parts and other manufactures these days, it isn’t primarily a commodity exporter.**** Perhaps some of the over $3 billion in imports of telecommunications equipment, the $3 billion in imports of auto parts (including tires) from Thailand and $0.75 billion in imports of household appliances just squeezes out other imports—but competition from places like Thailand also adds pressure on other countries to keep their exchange rates artificially depressed. It all adds up.

One last point: designating a country for “enhanced bilateral engagement” doesn’t lead automatically to meaningful sanctions, let alone a trade war. The sanctions outlined in the Bennet amendment are quite mild. But it would force a dialogue. And, well, if the Bennet sanctions are too mild for the Trump Administration’s taste, they could always experiment with counter-intervention.

* I am not a huge fan of the bilateral balance criteria. For one, I think it lets the NIEs (Hong Kong, South Korea, Singapore, and Taiwan) off the hook a bit too easily, as they export parts to China and thus account for a portion of China’s surplus! But more generally, there is no particular reason to think a bilateral surplus with the U.S. on its own signals an unhealthy overall pattern of trade. But in Thailand’s current case, its bilateral surplus with the U.S. is a component of its overall surplus, and the overall surplus is clearly quite large.

** Thailand did not get a bilateral credit line from the Treasury’s Exchange Stabilization Fund back in 1997, in part because of the restrictions that Congress placed on its use after Mexico. But I think the reality is that the use of the Exchange Stabilization Fund is the exception not the rule–Mexico was treated a bit differently because it is on the U.S. border, but also because it really did primarily have a short-term liquidity problem and thus was in a position to repay the Treasury quite rapidly.

*** The combined current account surplus of the NIEs, Malaysia, and Thailand in 2016 was around $300 billion– substantially larger than China’s $200 billion surplus in 2016. Malaysia is the only one of these six that hasn’t been intervening this year to limit appreciation.

**** Thailand’s commodity exports are actually down a bit: the U.S. is importing less Thai seafood these days, and the U.S. is no longer importing oil from Thailand (a few years back the U.S. was importing half a billion in oil from Thailand–there are often surprises hidden in the bilateral numbers).