China’s August Reserves

For the past fifteen or more years, if not longer, the flow of foreign exchange in and out of China has never quite seemed to balance. Either the yuan was a one way bet up, and the PBOC had to buy foreign exchange to keep the currency from appreciating, or the yuan was (thought) to be a one way bet down, and the PBOC had to sell a lot of foreign currency to keep the yuan from depreciating. Neither was an especially comfortable position for the central bank.

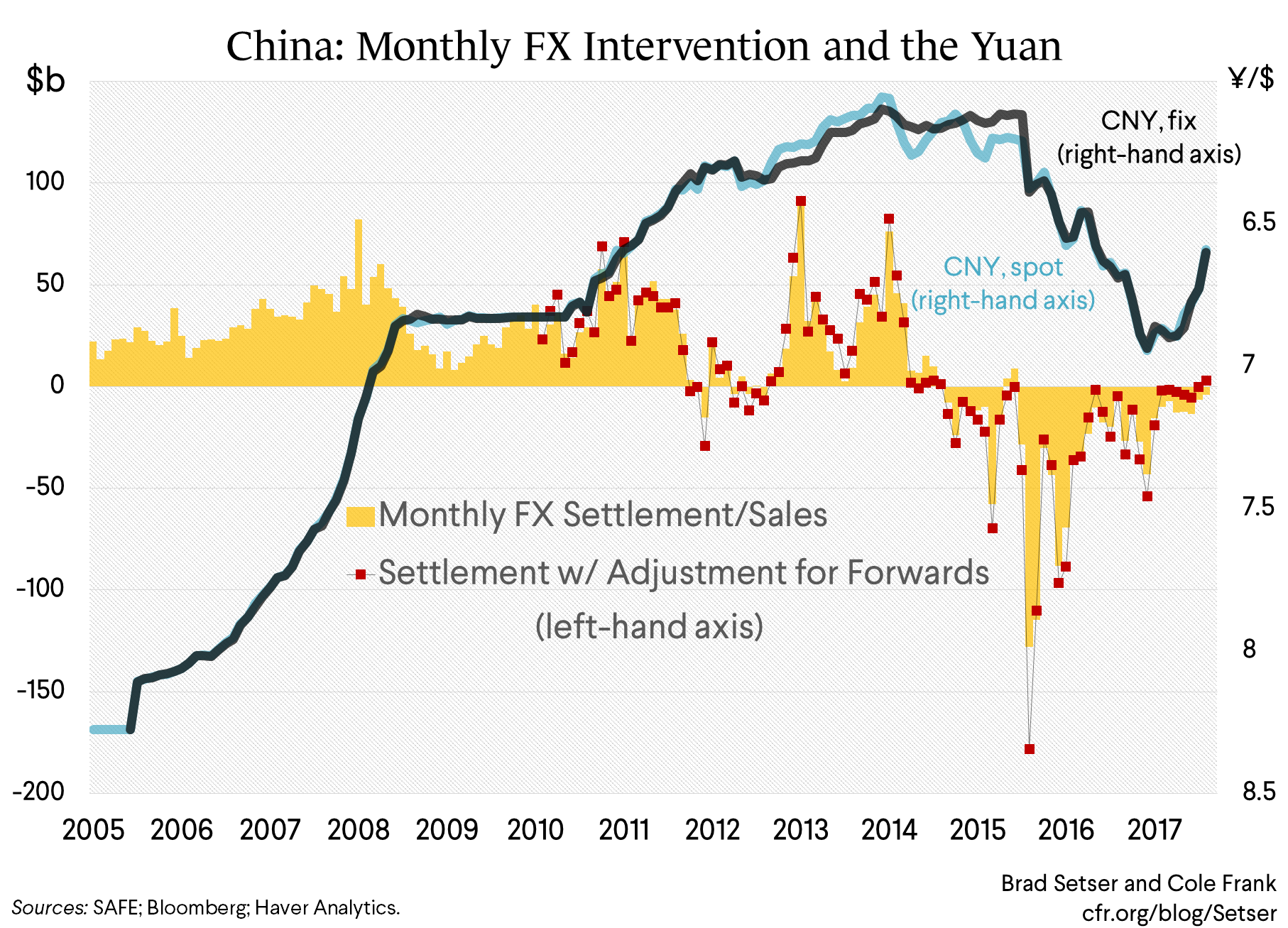

In August, though—and frankly through most of the summer—the available evidence suggests that inflows and outflows almost perfectly matched.* The stock of foreign exchange reserves reported on the PBOC’s yuan balance sheet—which shows its stock of foreign exchange reserves at its historical purchase price—didn’t move. And the numbers on foreign exchange settlement, which technically shows the flow of foreign exchange through the banking system but in practice tends to be dominated by the PBOC, show very modest net sales if you don’t adjust for reported forwards, and small net purchases if you do.

It is pretty amazing if you think about it. The PBOC supposedly thought flows were close to balance when it reformed its foreign exchange regime way back in August of 2015, but quickly discovered that the apparent balance hinged on expectations that the PBOC would keep the exchange rate constant. Those expectations, obviously, were disrupted by the August 2015 depreciation. Two years and a trillion or so in reserves later,** and calm has been restored. To the chagrin of those who bet that the August 2015 depreciation augured a big future move down: some thought the depreciation signaled that China’s leaders wanted a much weaker currency (and I suspect China’s leaders did want a somewhat weaker currency; the yuan did depreciate against the CFETS basket from mid 2015 to mid-2016), others thought that the depreciation signaled that the PBOC was about to lose control over the exchange rate (not a view I shared).

Yet it seems that the August equilibrium was itself somewhat fragile. The yuan shot up in the first week of September. I suspect—without having hard evidence—that the PBOC had to intervene to keep it from rising more. And then the PBOC loosened some of the controls that it had put in place to limit depreciation pressures. That was—rightly I think—interpreted as sign that China’s government didn’t want the currency to appreciate too much. The investment banks all seem to think that China’s exporters started to think the yuan was a one way bet up and started to unload the dollars they had accumulated back in 2016.

Three more comments:

1) The PBOC could have used the reemergence of appreciation pressure to rebuild reserves, rather than to loosen controls. The fact that it didn’t suggests something about the PBOC’s policy goals. Among other things, it suggest the PBOC doesn’t think it needs more than $3 trillion in reserves. I agree. The three trillion number came from the heavy weight the IMF’s new reserve metric placed on local currency deposits if a country has a fixed exchange rate and an open capital account. The IMF’s China team, incidentally, also now recognizes—see paragraph 44 of its latest staff report—that the reserve metric doesn’t really fit China.***

2) John Authers of the Financial Times noted last Friday that in China “the market and the economy are state-controlled.”**** That’s still largely the case for the onshore foreign exchange market, even if there are some channels that are difficult for China to completely control. China has lots of tools—especially now that it reversed the August 2015 reforms and effectively reintroduced the “fix” as a market signal back in June. It can dial capital controls up or down. And I think it can also dial the amount of state bank lending—and borrowing—from the rest of the world up and down. One reason why flows stabilized after the first quarter is that Chinese banks seem to have slowed their breakneck foreign loan growth (they also started borrowing more from the world, so their net foreign asset position stopped growing and actually looks to have shrunk a bit—but that’s a very technical topic for another time).

In other words, balance in the market has come in part through managing the flows allowed to enter the foreign exchange market. I don’t really expect that to change—any coming liberalization is likely to be done in ways that are reversible.*****

3/ Exchange rate moves impact trade flows with a lag. The August appreciation of the yuan almost certainly had no impact on China’s August trade data (year-over-year volume growth was down a bit in August relative to July, but that is likely a result of standard volatility in the trade data—and the fact that the base from August 2016 was quite strong). A good rule of thumb is to look back a year to get a sense of the impulse the exchange rate is giving to current trade flows. And by that measure, China is still getting a boost from the exchange rate.

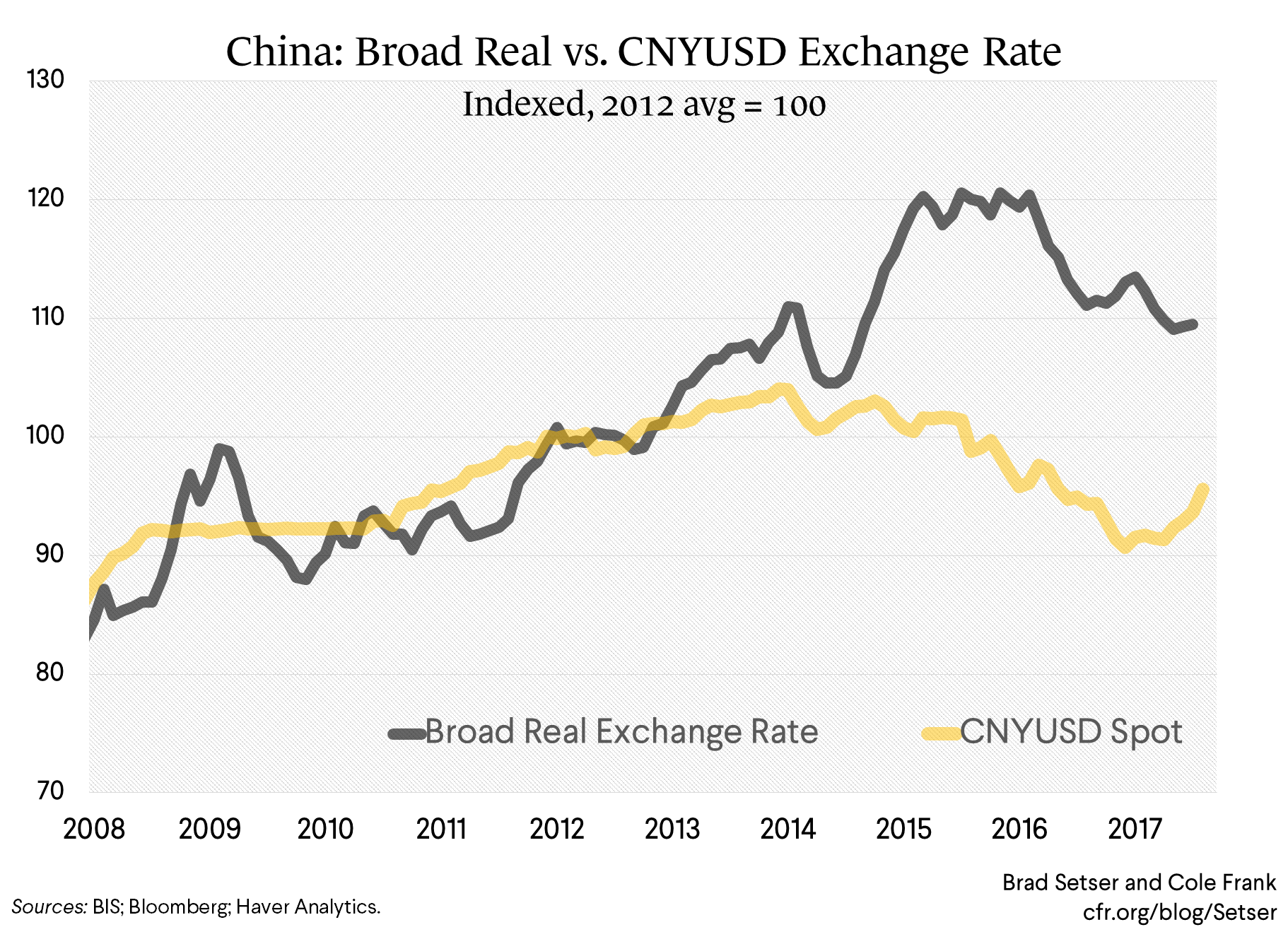

Plus, well, the yuan—against the dollar—really isn’t that far from where it was eight or nine years ago and ongoing productivity gains should be leading the yuan to appreciate over time. And even with the yuan’s appreciation in August and September, the broad yuan is down close to 10 percent from its peak (against the CFETS basket)—though to be fair, that depreciation came after a significant appreciation in late 2014.

I am not particularly impressed by the recent whinging of Chinese exporters (who probably should have hedged their future export orders earlier in the year but, well, probably didn’t when they expected the yuan to continue to depreciate). Chinese export growth in the first half of 2017 exceeded global trade growth, and exports to the U.S. have been doing just fine this year.

* There was a brief period in the summer and fall of 2012 when the PBOC doesn’t seem to have intervened much, as the euro crisis spilled over and triggered an emerging market sell-off. The foreign exchange reserves reported on the PBOC’s balance sheet (in yuan terms) were also relatively flat for a period in late 2014 (when the dollar was appreciating), though the settlement data suggests sales in September and q4.

** About half of the fall in reserves is balanced by a fall in short-term debt. And a significant fraction of the remaining half a trillion is explained, in a mechanical sense, by the ongoing rise in the foreign assets of the state banks.

*** I think it also doesn’t work that well for a lot of under-reserved emerging economies—largely because it gives equal weight to domestic and foreign currency deposits.

**** “The market and economy are state-controlled (even if the profit motive is put to much more use than it was in previous communist experiments)”; I enjoyed the entire column, though I also tend to think that the eventual credit “reckoning” could still play out with some very Chinese characteristics (e.g. through a rather opaque recapitalization similar to what happened after 2003, though made more difficult by a slower underlying pace of growth).

***** I am not sure that is a bad thing by the way. I agree with Martin Wolf’s argument that it safer for everyone if China’s domestic financial system is kept one step removed from global markets so long as the domestic financial system has so many undercapitalized institutions (backed by an implicit or explicit state guarantee).