Three Items of Note

Often one of the best ways to get noticed is to highlight something a bit surprising.

A data point that doesn’t match expectations for example. Puerto Rico’s large trade surplus for example, which, really is “fake” news: it is rather obviously a function of transfer pricing that helps pharmaceutical firms shift profits offshore, where they can be indefinitely tax-deferred.

But it also is important to remember that many things play out more or less as expected. Here are three that have caught my eye:

1. Capital flows to emerging market commodity exporters have been pro-cyclical.

Not exactly news, but important. Most emerging economies are commodity exporters, and most pay more to borrow when commodity prices are low. That makes it harder to smooth commodity price volatility by borrowing from abroad—and makes it more important for commodity exporters to have a buffer stock of assets (or a flexible currency). (A hat tip to Peterson’s Chad Bown for highlighting this VoxEU paper by Thomas Drechsel and Silvana Tenreyro).

Now perhaps this is changing. The IMF’s global financial stability report is worried that the global reach for yield may have gone a bit too far.* And I have certainly been struck by the large sums many Gulf countries have borrowed recently. But these countries may be the exception that prove the rules. The Emiratis, the Qataris, and the Saudis all have substantial assets stockpiled either in their central banks’ foreign exchange reserves or in their sovereign funds. They are in a sense borrowing to avoid selling their assets—rather than borrowing “naked” to finance the deficits created by the fall in oil prices.**

2. Tight fiscal policy often contributes to large current account surpluses.

The latest IMF revisions to Korea’s fiscal stance offer a case in point (the Korean article IV has been delayed it seems, but the WEO provides updated numbers). It turns out that Korea’s 2016 fiscal policy was tighter than that of Germany. Germany’s structural surplus was 1 percent of GDP, while Korea’s was 2 percent of GDP. The IMF also now believes there was significant structural tightening in 2016 as well (something I am not sure either the IMF or the Treasury noticed in real time; the Koreans have done a lot of “fake” stimulus). The IMF has taken note of the government of Korea’s substantial assets--Korea’s net debt is about 5 percent of GDP. I suspect the IMF added the social security funds’ assets to its calculations of net debt.

Korea’s 2016 fiscal tightening was thus globally unhelpful. It drained the world of demand when the world was short of demand. That put pressure on countries with weaker public balance sheets to do more to support demand. And it of course also contributed to the weaknesses in Korea’s economy that led the Bank of Korea to ease—and at times to intervene directly in the foreign exchange market to cap won strength.

The IMF’s fiscally driven current account model doesn’t always work well (China’s credit boom and large fiscal deficit for example sits oddly with its balance of payments surplus). But for Korea, it captures a large part of the story—especially because the social security fund’s accumulation of foreign assets provides a direct link between Korea’s structural surplus (a function of high contributions to the social security fund) and capital outflows.

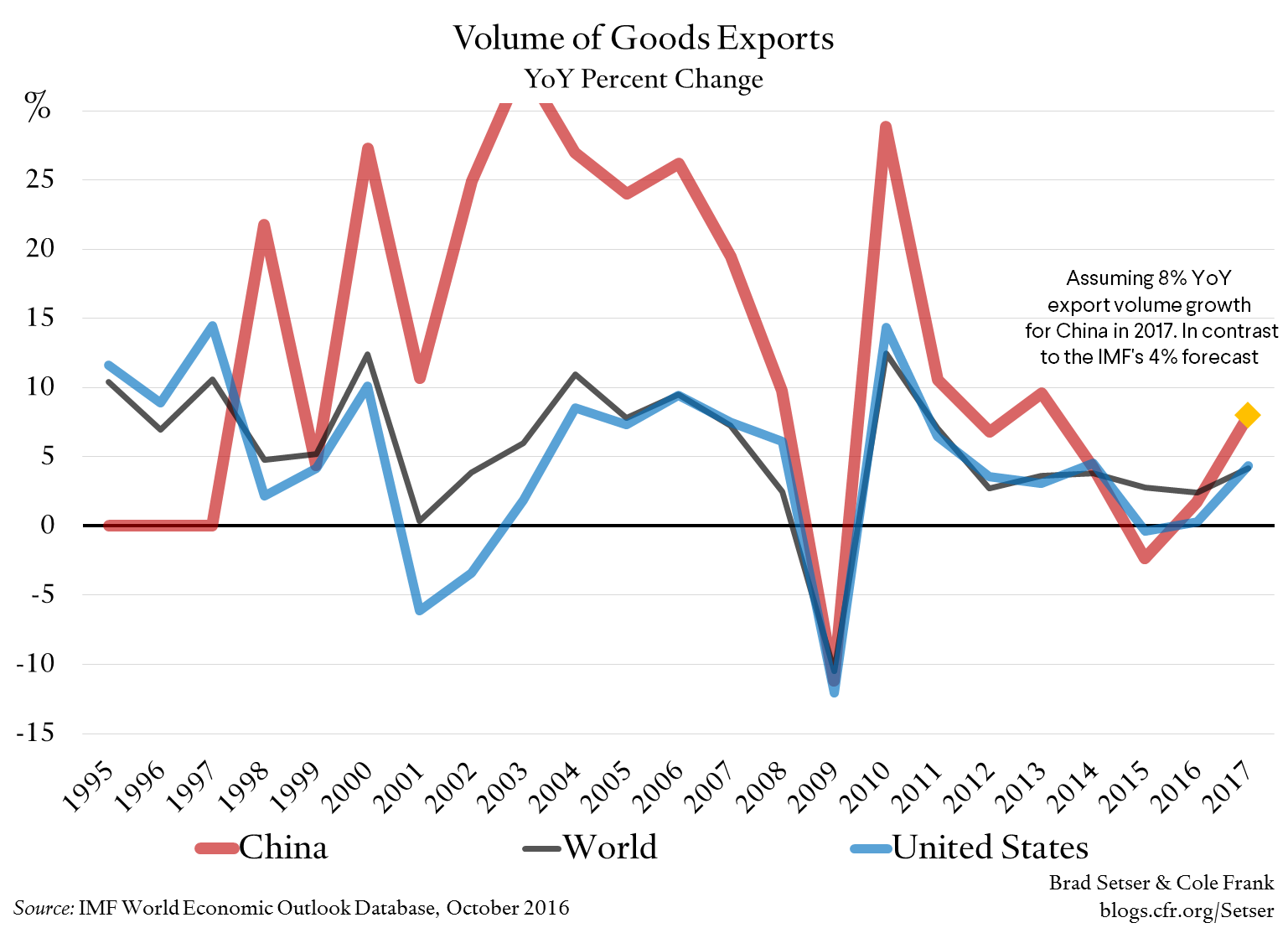

3. China’s export machine is still strong, and it still responds to changes in the real exchange rate

The IMF estimates that world import demand (and world exports) will grow by about 4 percent this year (for goods). China’s export volumes are, according to the (not ideal) Chinese data up about 8 percent.*** So Chinese export growth once again will exceed global export growth (Chinese import growth is more or less in line with China’s growth, or a bit faster than China’s growth, which is good news—and a bit of a change). That’s why I am generally skeptical about stories that suggest China is losing its competitive edge in manufacturing: it may be true in some narrow sectors, but it simply isn’t borne out in the global data.

And, well, a pick-up in Chinese export growth after a close to 10 percent real depreciation is more or less what a standard trade model would forecast. The yuan’s 2016 fall certainly seems to be having an impact on China’s 2017 export performance.

Basically, when the yuan rose strongly in 2014, Chinese export growth slowed to match global export growth (a change for China). And the 2016 depreciation seems to have helped push Chinese export growth above global export growth—which is more or less the “norm” for China. And that recovery in exports, along with tighter controls and a broader rebound in economic activity all have helped to stabilize China’s currency’s for the time being.

* The Fed’s balance sheet expansion since 2010, has, according to the IMF’s global financial stability report, explained a sizeable share of portfolio flows to emerging economies—about a half of the roughly $350-400 billion total in the data set, with fed policy expectations also contributing significantly to inflows (p. 21, and figure 1.15: model estimates indicate that about $260 billion in portfolio inflows since 2010 can be attributed to the push of unconventional policies by the Federal Reserve). I applaud the effort to quantify portfolio balance effects. But I also thought there was something a bit strange about the results of the IMF’s attempt to quantify the impact of balance sheet expansion on emerging market flows. The study focused entirely on the Fed, but—as Figure 1.13 on p. 19 shows—the Fed’s quantitative easing hasn’t been nearly as significant, relative to government bond issuance and thus to the available supply of bonds, as ECB and BoJ balance sheet expansion. Maybe there is a massive asymmetry here: ECB QE is bad for emerging markets flows because it induces inflows into the U.S., raises the value of the dollar and thus indirectly hurts emerging markets because they tend to borrow more in dollars than in euros or some such? But it isn’t obvious to me why the effect of ECB and BoJ QE should fundamentally differ from the effect of U.S. QE. At the end of the day, Europe and Japan are net savers and thus the ultimate supplier of funds—and QE in Europe and Japan has worked in part by reducing domestic yields and thus encouraging investors to reach for yield abroad (see Coure’s speech in July).

** Technically, their debts reduce their net asset position, rather than add to a net debt position.

*** China reports the y/y growth in its exports monthly, but doesn’t report an estimated level. I took the average of the available y/y changes. The y/y numbers can be volatile because of shifts in the timing of the lunar new year, but the monthly volatility tends to offset (a big fall in February means a big rise in March or vice versa).