Weak Won, Tight Fiscal: Korea’s Not-So Mysterious External Surplus

Korea’s macroeconomic policies have had a greater impact on its pattern of trade than any free trade agreement.

The Trump Administration seems to have decided—for now—not to withdraw from the U.S. Korea Free Trade Agreement (KORUS). The President’s threat to withdraw was spectacularly poorly timed. China’s efforts to squeeze Korea economically (see Hyundai’s trouble with its joint venture), especially after Korea decided it wanted high-tech U.S. missile defense (THAAD) deserve more coverage than they have gotten.

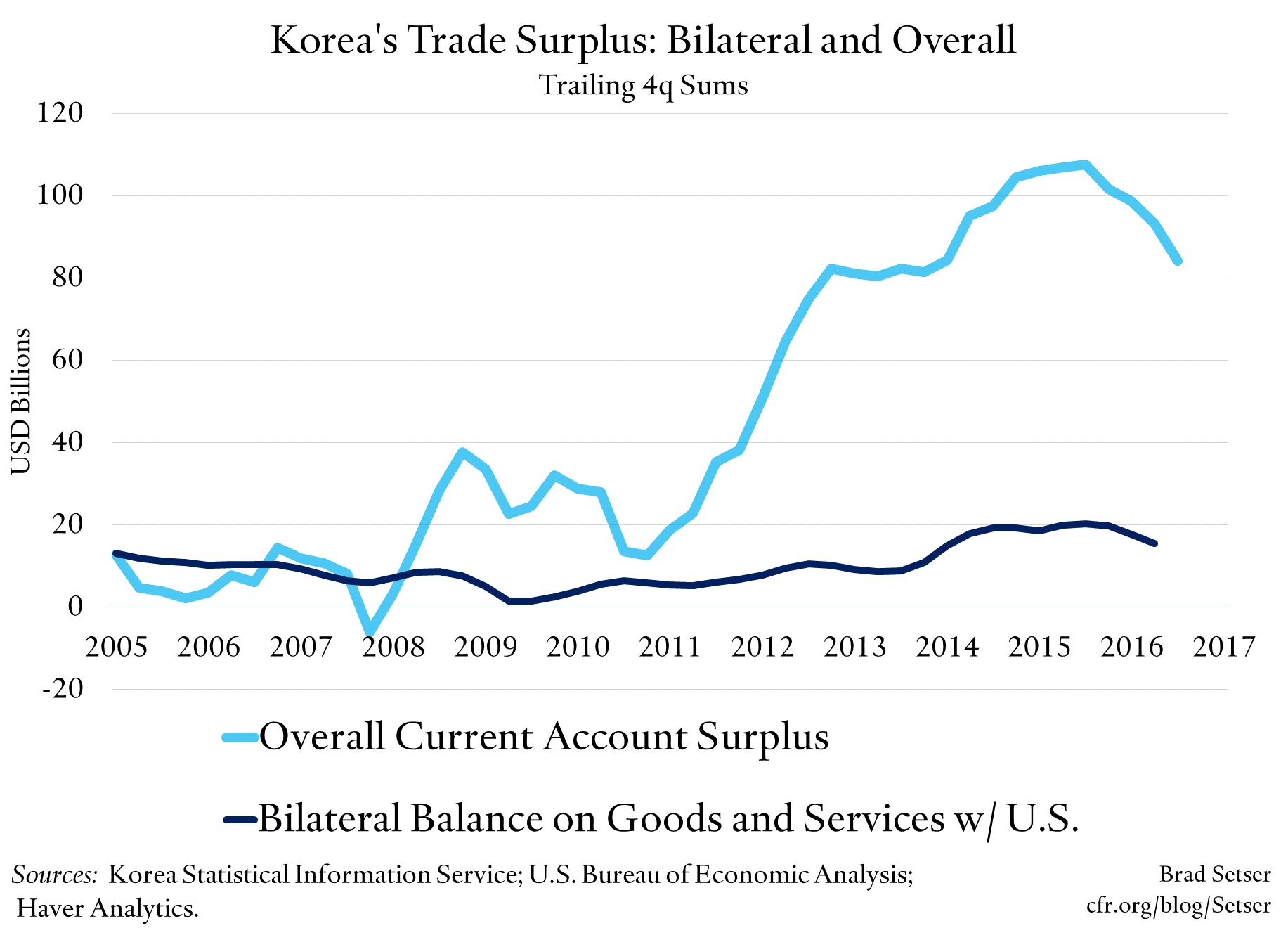

Korea though differs from Mexico or Canada in one critical way: Korea runs a quite sizeable overall trade surplus—while both Mexico and Canada run overall trade deficits. If you worry about trade and payments imbalances, Korea is a legitimate source of concern.

I consequently do think the bilateral surplus Korea runs with the U.S. should be viewed a bit differently than the bilateral surplus that say Mexico runs with the U.S. (counting services, Canada runs a deficit with the U.S).

Korea’s total external surplus was about $10 billion before the global crisis, and it is now around $100 billion (more when oil is low, less when oil is high). The surplus is down slightly from last year’s peak of over 7 percent of Korea’s GDP—but should still be around 6 percent GDP.

There is no reason to think KORUS (or Korea’s free trade agreement with the EU) contributed to the rise in Korea’s surplus. Tariffs don’t typically drive trade imbalances.* (See Gagnon).

The rise in Korea’s global surplus—and, for that matter, Korea’s bilateral surplus with the U.S.—started in 2009, well before KORUS entered into force in 2012.

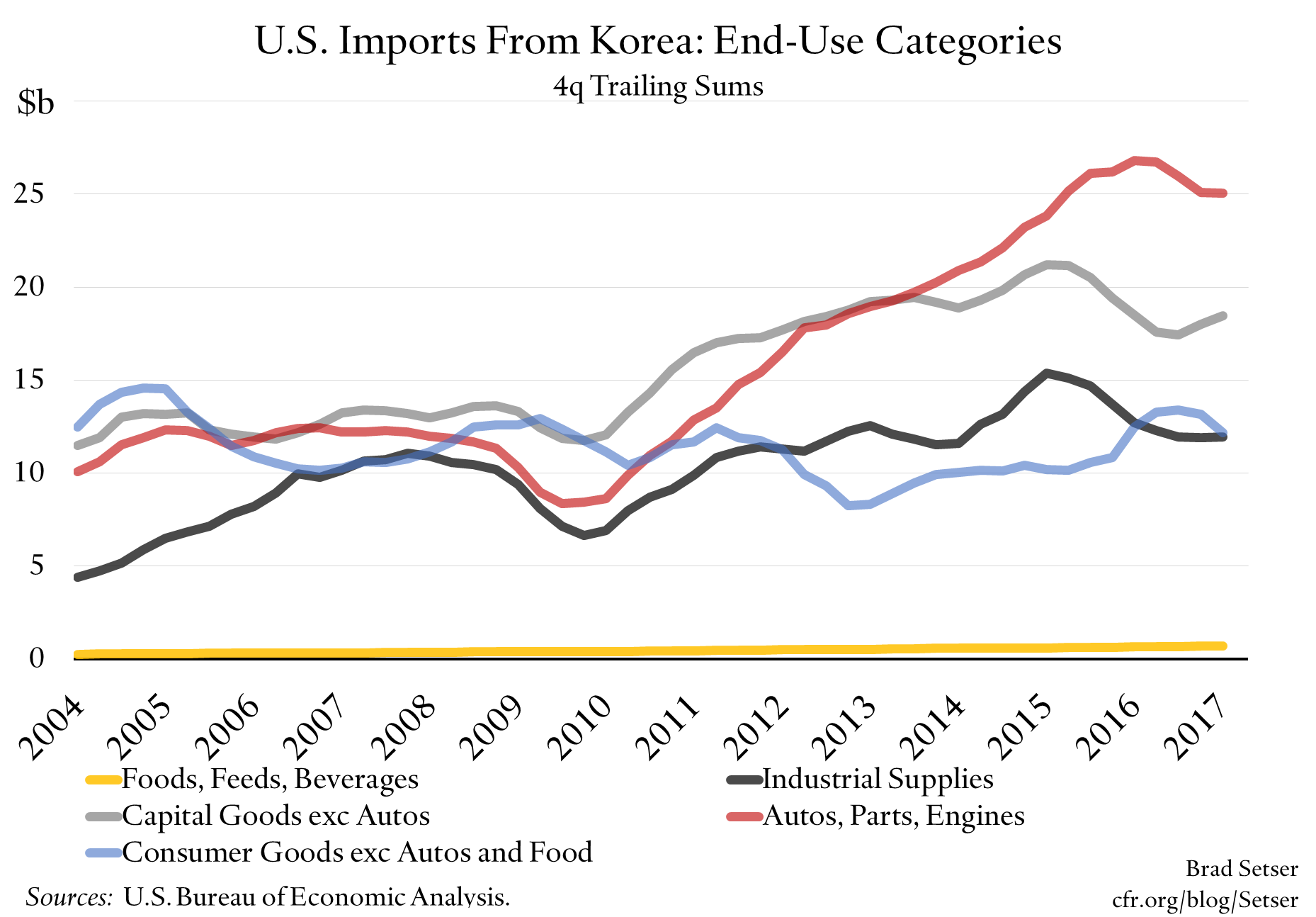

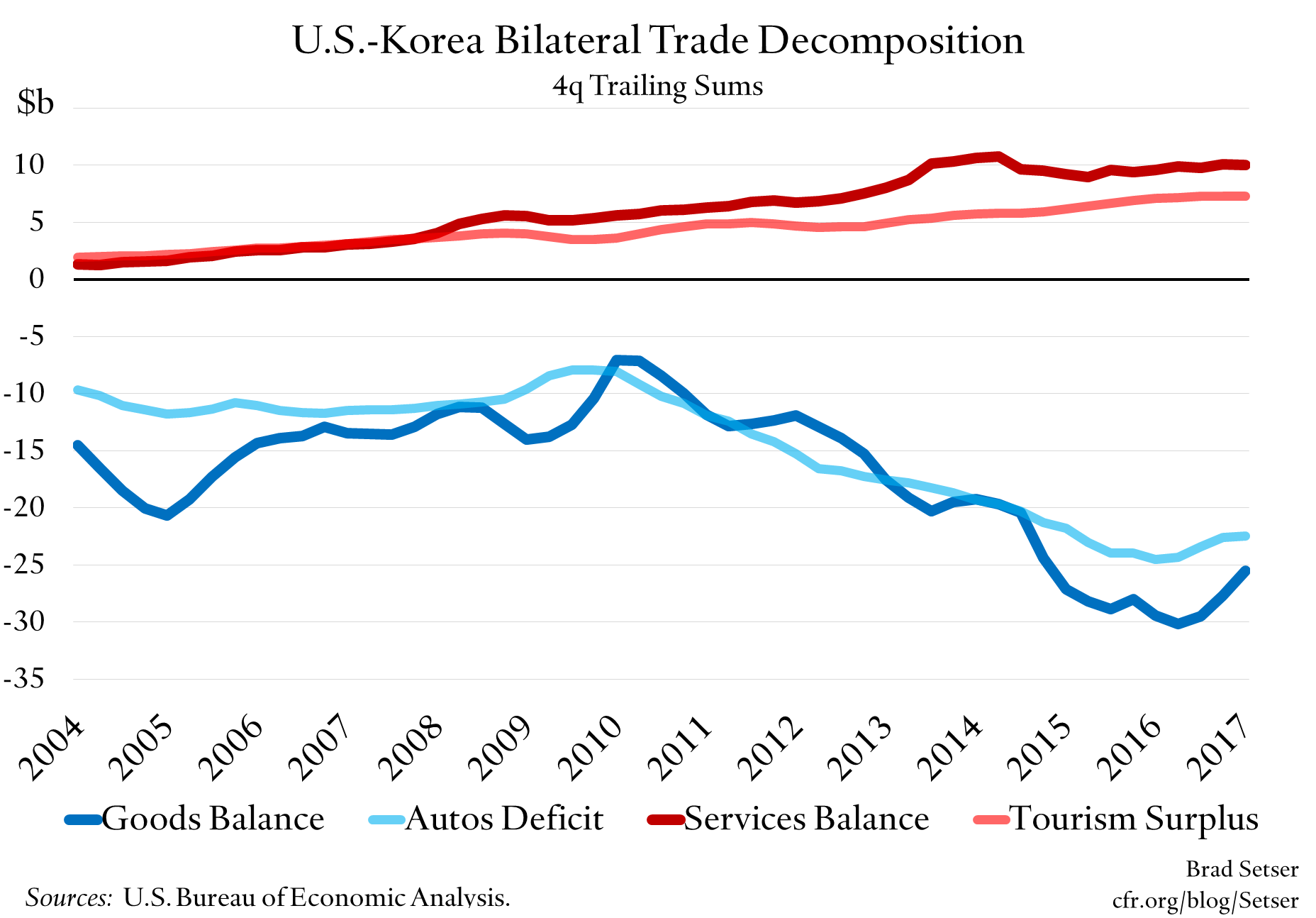

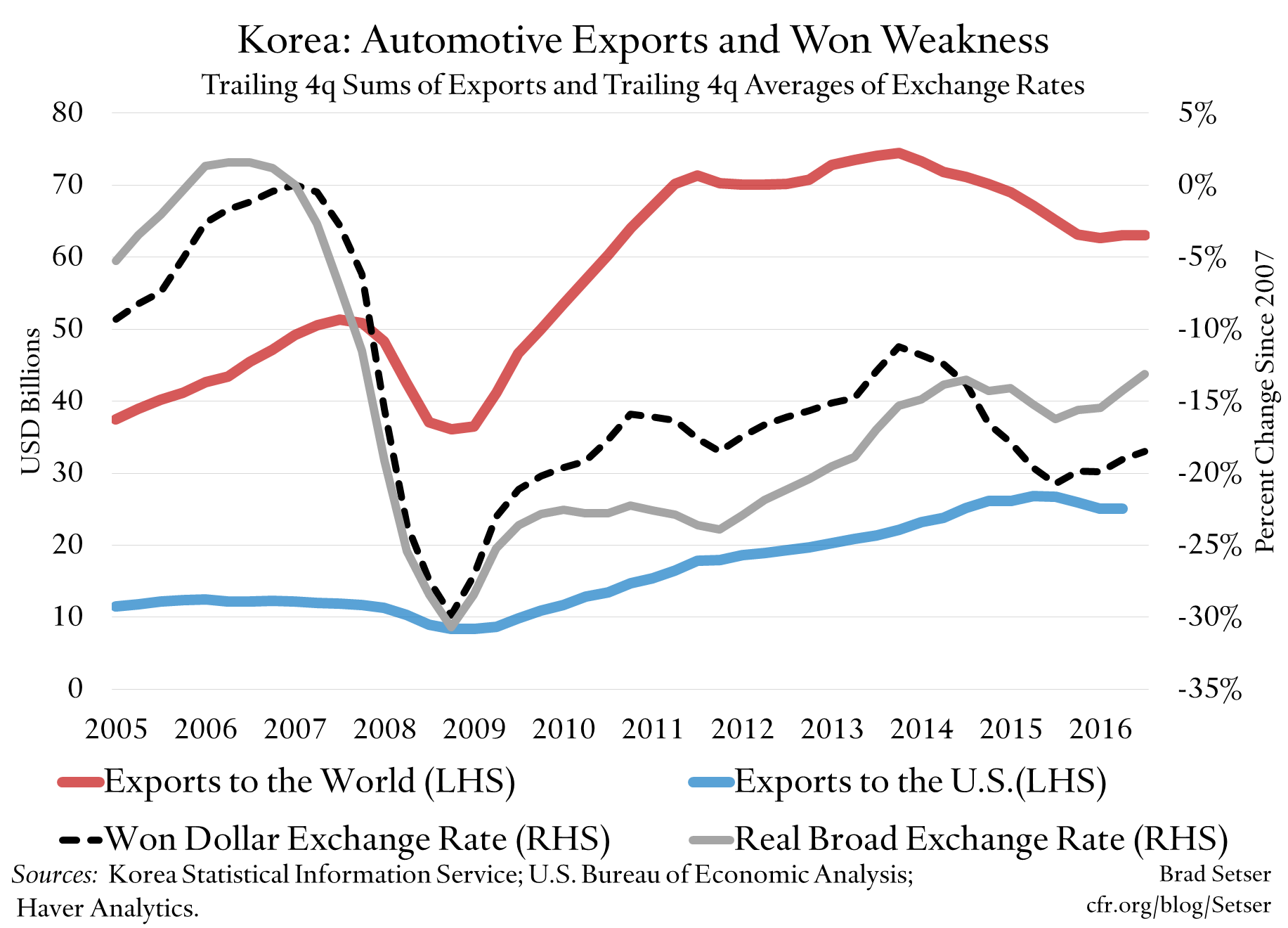

At the same time, KORUS didn’t do much to help offset the impact of Korea’s pro-surplus macroeconomic policies. The reduction in Korean tariffs no doubt helped certain agricultural exports (and, according to Chad Bown, some U.S. cars got into the Korean market despite not meeting Korean fuel economy and environmental standards).** But, well, the rise in U.S. imports of Korean autos was far larger than models at the time predicted.*** Largely because a weak won continued to provide incentives for Korean auto manufacturers (there are only two that really matter—Hyundai/Kia and GM Korea) to produce in Korea. The ongoing rise in Korean auto and auto parts exports to the U.S.—together with a fall in commodity prices that reduced the dollar value of U.S. exports to Korea—largely explain the evolution of the bilateral deficit with Korea.****

But I do think the U.S. should be pushing Korea to do make the kind of policy changes—more fiscal spending, less currency intervention—that would bring down its large current account surplus, and not simply fight for narrow trade concessions. There are no guarantees, but the policies that would reduce Korea’s overall surplus would also likely reduce Korea’s bilateral surplus with the U.S.

Korea’s surplus, in my view, surged because Korea basically opted out of the global fiscal stimulus after the financial crisis, and instead relied on a weak won—sustained when necessary through intervention in the foreign exchange market—to support its economy.

The IMF’s WEO data shows that Korea had a structural fiscal surplus (counting the surplus in its social security fund) of 1.3 percent of its GDP in 2008, 0.45 percent of GDP in 2009 and 1.5 percent of GDP in 2010—and Korea has retained a structural surplus in this data (estimated at 1 percent of GDP in 2017). Even Germany did more stimulus in the crisis.

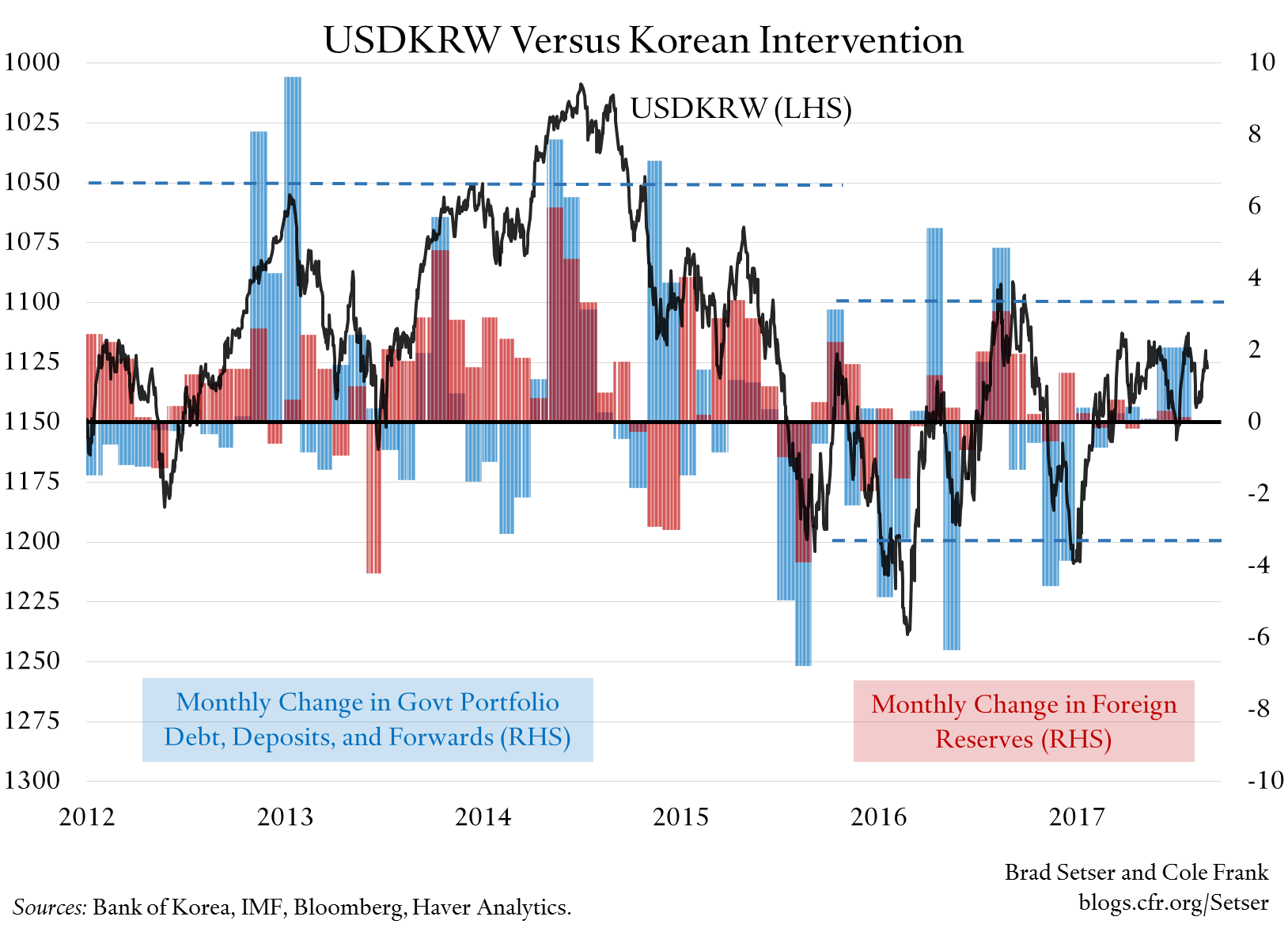

And after the won fell sharply in the crisis,***** Korea intervened heavily to keep the won weak. The won generally has been about 20 percent weaker (versus the dollar) after the crisis than during the 2006-07 period—and the impact of won weakness was augmented by the yen’s strength in the immediate aftermath of the crisis, and China’s appreciation in 2007-08 and again in 2010-11.

When I look at a chart of Korea’s automotive exports (using measures that count auto parts) I don’t see any connection to the entry into force of KORUS (March 2012), or the final phase out of the auto tariff (this year, I think, as it was phased out with a five year lag). The inflection point—both for exports to the U.S. and exports to the world—comes when the won depreciates. As one would expect: the won’s depreciation far exceeds the U.S. 2.5 percent tariff on autos. Through its intervention, I think Korea effectively signaled to its auto manufacturers that the depreciation would persist long after the global crisis.

And, well, Korea continues to intervene to block won appreciation even now.

Not all the time: when the market gets jittery after a North Korean missile launch or nuclear test, the won sells off and Korea has no need to intervene.***** But when the won approaches 1100, Korea does still seem to step into the market. The Bank of Korea’s forward book jumped by $1.5 billion in July.

Korea’s surplus—globally, and vis a vis the United States—thus reflects ongoing Korean macroeconomic and currency policy choices.

Korea’s new President does seem keen on raising social spending. That’s an important step in the right direction: Korea’s social insurance spending is well below that of other advanced economies. But if you look at the small print, the rise in Korean government spending next year matches the projected increase in revenue. The fiscal balance won’t change: the general government, which includes the national pension fund, should remain in surplus.

And it is hard to think of a more perfect connection between fiscal policy and the external balance of payments than Korea’s policy of using the national pension fund system’s surplus to buy foreign assets. The pension system runs a 2.5 percent of GDP surplus—and channels a large share of that surplus (around 1 percent of GDP) directly into foreign assets.

Korea thus has real scope to change its domestic macroeconomic policies in ways that would strengthen its own demand. And if a fiscal loosening was paired with an end to Korea’s visible and more hidden intervention, it almost certainly would have an impact on the size of its external balance.

* Brazil has very high tariffs on industrial goods, much higher than U.S. tariffs on average. And it has used state financed procurement to discriminate against imports—its broader industrial policy has had a strong whiff of protectionism. Brazil also runs a global trade deficit, and a bilateral deficit with the U.S.

** A hat tip to Chad Bown for noting that one of the main U.S. asks of Korea during the KORUS renegotiation was to let heavier and more polluting U.S. cars into the Korean market even if they didn’t meet Korean environmental standards. A more general point applies here: U.S. vehicle production is increasingly tilted towards light trucks and SUVs. Light car production is either in Mexico—or now China—as no one makes money in the U.S. on small cars. The composition of U.S. output limits the ability of the U.S. to export to markets where fuel economy plays a bigger role (and it helps the U.S. export to say the Middle East, which also likes big cars).

*** Back in 2007 the U.S. International Trade Commission (ITC) estimated that eliminating U.S. auto tariffs on imports from Korea would raise Korean exports to the U.S. by roughly $1.5 billion a year (see page 3-82), with about half that rise displacing imports from other auto-exporting economies (Japan, Mexico) rather than U.S. production. That kind of impact would be relatively easily matched by a rise (off a low base) in U.S. exports, as Korean tariffs on autos and machinery generally exceeded those of the United States. It is hard for me to argue that the model was wrong per se, as I clearly think other factors are far more important than the tariff (and one would reasonably expect only a modest rise in imports from eliminating a modest tariff). But the ITC report also didn’t exactly state that the impact of a weak won would overwhelm the impact of trade liberalization either—and it did suggest that the impact on textiles and apparel would be larger than the impact on autos (see table 2-2).

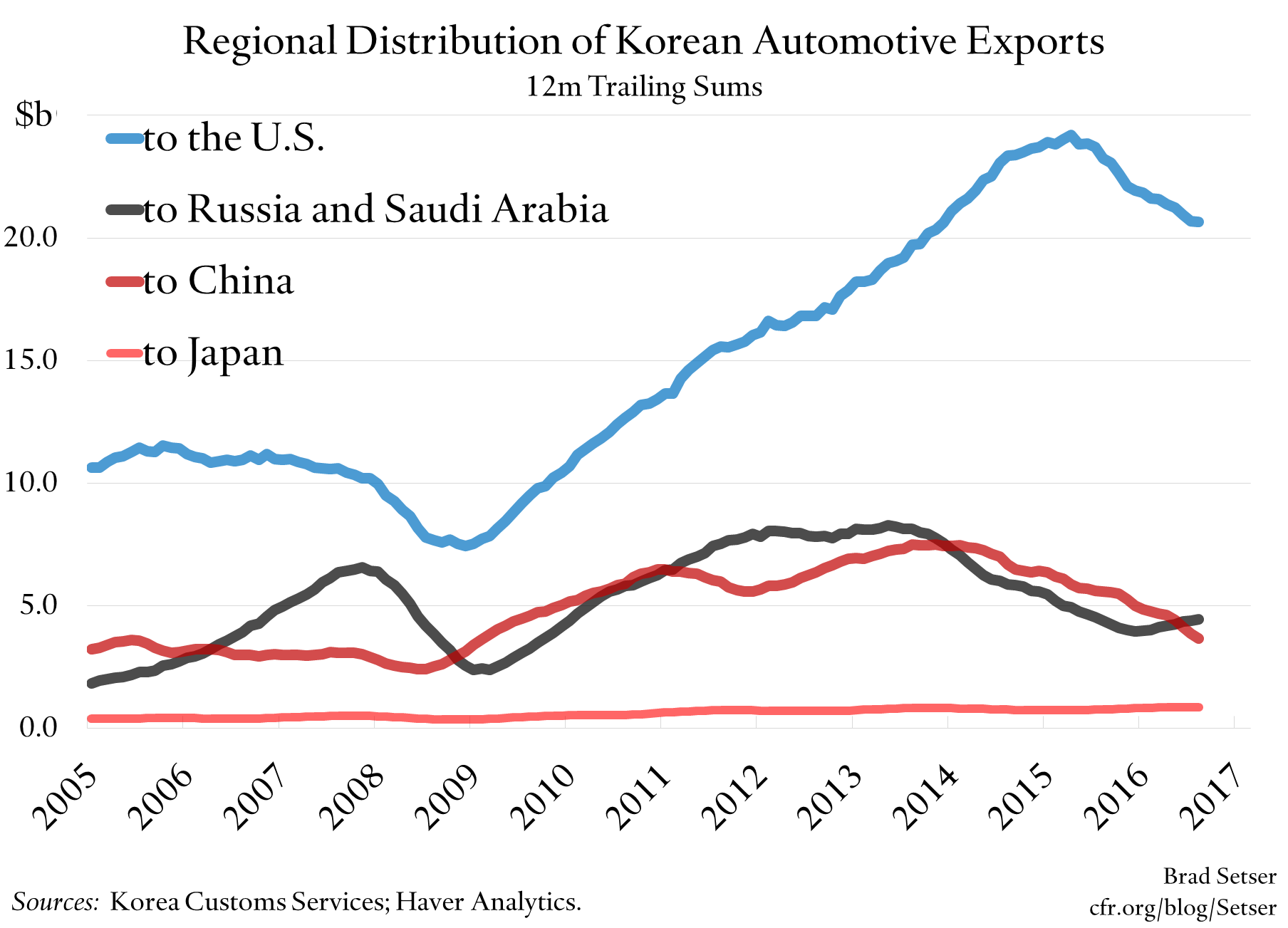

*** So, a bit more background on Korea’s auto sector. Korea produces a more than 4 million cars and trucks a year, and it exports close to 2.5 million of them. The U.S. market is very important to Korea—Korea exports about 1 million finished cars to the U.S. (and even after KORUS, Korea only imports 60,000 or so cars from the U.S.). In fact the U.S. market has gained in importance recently, as Korean exports of autos to Africa and the oil-exporting economies have fallen sharply after the 2014 commodity price shock. The U.S. is a bit less important if you add in parts, but it still is about 40 percent of total Korean auto exports. The pattern of Korean auto trade is also striking in one respect: there is very little trade in finished autos with Korea’s immediate neighbors. The lack of two way trade with Japan is well known, and stems from their complicated history. And, well, China’s 25 percent auto tariff has an impact: Hyundai produces in China—not in Korea—for the Chinese market, while it produces both in Korea and in the U.S. for the U.S market. And when Hyundai set up shop in China it also encouraged its Korean parts suppliers to set up shop in China too. Back in 2008 a Stanford Business School case study indicated that only 10 percent of Hyundai-Beijing’s parts were imported from Korea. This though hasn’t insulated Hyundai from political pressure: it now is being pushed by its Chinese JV partner to buy more parts from Chinese suppliers, not its “Korean” network in China. Because Hyundai’s Chinese sales are supported by Chinese production, the big drop in Hyundai’s sales in China hasn’t really cut in Korea’s overall exports this year as much as one might expect. Hyundai is also under a bit of pressure in the U.S. now: overall auto sales are falling this year, and vehicle demand is shifting towards heavier pickups and SUVs and thus away from Hyundai. One last thing—Korea’s overall auto exports to the U.S. were flat from 2005 to 2008 for a host of reasons, including the won’s strength at the time. But no doubt the opening of Hyundai’s first U.S. factory in 2005 also played a role.

**** Korea also intervened to limit the won’s weakness during a couple of China scares. But its last large sales were in early 2016, so the “two-way” intervention that the IMF and Treasury have noted in their recent reports is increasingly in the past. Thanks to the structural outflows from the pension funds and the U.S. Treasury’s practice of giving countries a free pass on the interest income on past intervention, Korea won’t cross the 2 percent of GDP intervention threshold that the U.S. Treasury now uses as a criterion for manipulation.

***** Korea had a short-term debt problem prior to the crisis, for complex reasons. The IMF has done good work on this. And the short-term funding need of Korea’s banks meant that Korea was caught up in the global crisis. Korea also got access to a swap line with the Fed in the crisis—which, in the end, didn’t change its decision to build up its reserves after the crisis.

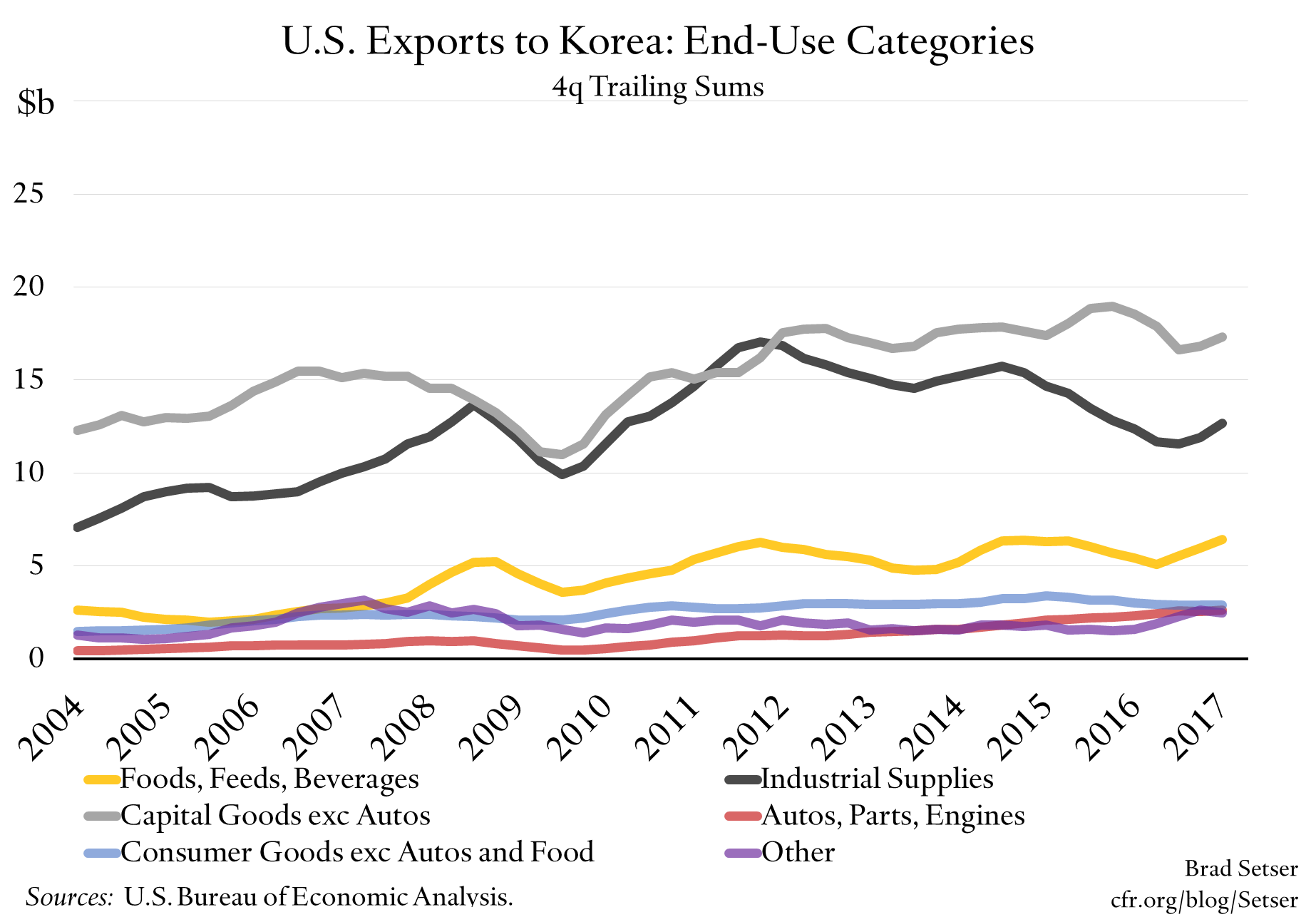

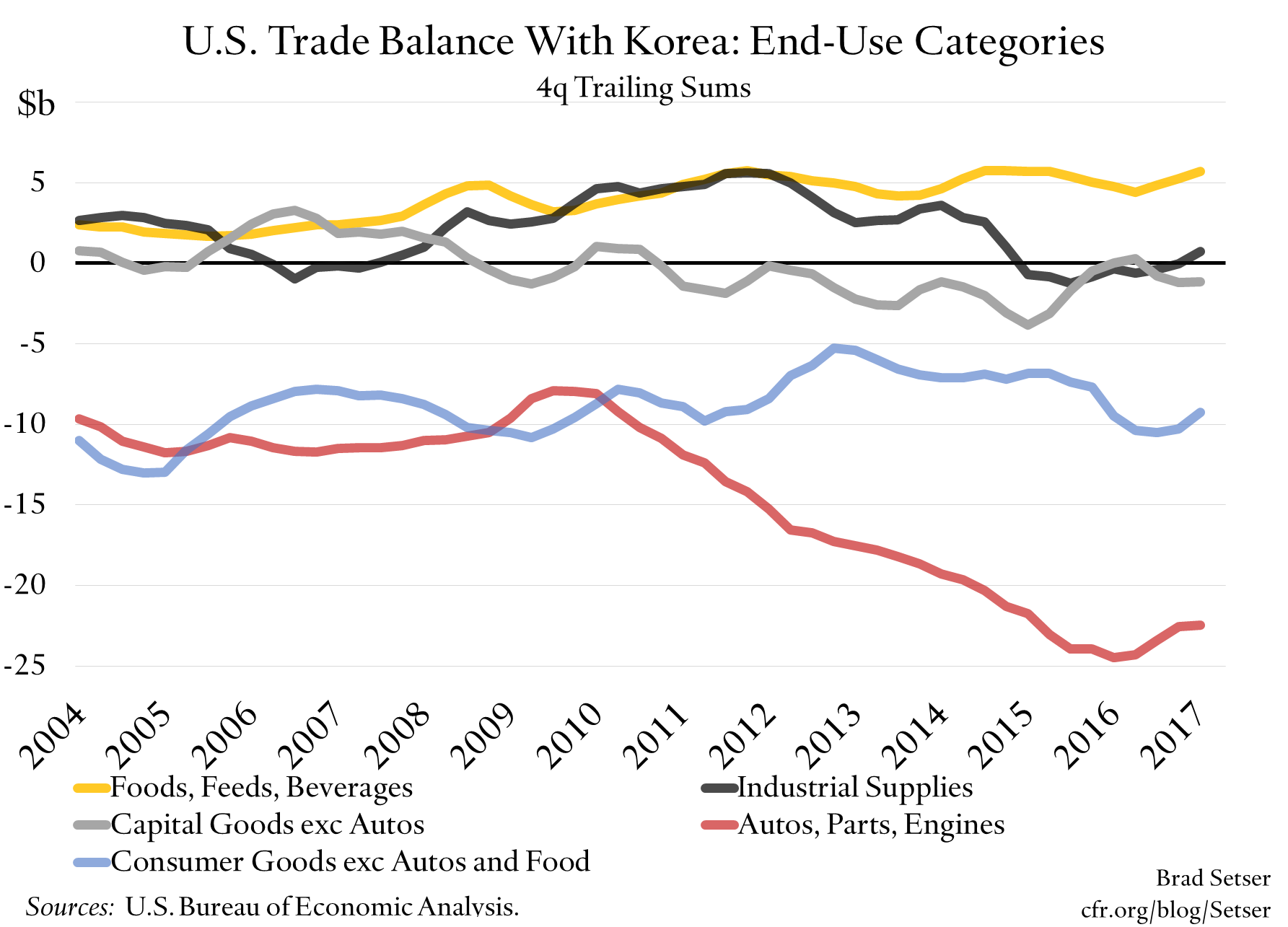

****** Bonus charts on exports and imports by the main-end use categories. Further disaggregation is possible but there are limits on what can be made to fit into a single graph. The relative stability of U.S. food exports reflects competing trends. Exports of grains and soybeans are down in dollar terms—as they are a function of price. Exports of specialized agricultural products are up, as proponents of KORUS predicted. Korea does have high tariffs on many specialized foods, so there is a real advantage to preferential market access. The pattern of trade “industrial” supplies reflects competing trends as well—U.S. exports of ores, coal, and wood products (lumber, paper) are down since KORUS was signed, but that reflects global price swings not Korean protectionism. Exports of LNG are now growing quickly. KORUS helps there, but attributing the rise entirely to KORUS goes too far. The U.S. increasingly licenses LNG facilities to export to everyone, not just to FTA partners (e.g. U.S. LNG trains can sell to China and Japan, not just Korea). And exports of “other petroleum products” are way down (price?). In capital goods, exports of civil aircraft has been strong (civil aircraft weren’t affected by KORUS) while other exports have gone down. One thing that surprised me in the end-use data is the two-way trade in oil and gas drilling equipment. I guess U.S. firms supply some of the technology that goes into the drilling platforms made by Korean shipbuilders (Korea itself doesn’t have oil or gas to drill). Ultimately though the key category is autos—nothing else evolved in a really unexpected way.