Three Sudden Stops and a Surge

Reflections on the Global Financial Crisis, through the lens of the U.S. balance of payments.

There is one point of agreement among most ten-year retrospectives that have been published on the global financial crisis: it wasn’t quite the crisis many had expected. It wasn’t marked by a loss of confidence in the safest of U.S. assets, a fall in the dollar and a rise in U.S. interest rates.

Rather the dollar—briefly I would argue—rallied at the height of the crisis. And demand for Treasuries soared. The crisis ushered in an extended era of low nominal and real U.S. interest rates.

All true.

Fundamentally, the crisis was a crisis of confidence in the health of the balance sheets of the great financial houses of the United States and Europe. At least in the absence of a government backstop for their capital—and a government backstop of their ability to raise the wholesale financing they needed to operate such large balance sheets. The line between banks and shadow banks was thin, it turned out.*

But a narrative of the crisis that writes the balance of payments out is still, in my view, misleading.

Contrary to a now popular opinion, demand for U.S. financial assets didn’t soar in the crisis.

The dollar rallied in large part because American funds that had moved abroad in search of higher returns came home, not because foreign investors wanted to hold more U.S. financial assets. The core financial inflow into the United States after the crisis—as before the crisis—came from foreign central banks that had to buy dollars and ultimately U.S. bonds so long as they resisted letting their currencies appreciate against the dollar, not private investors.

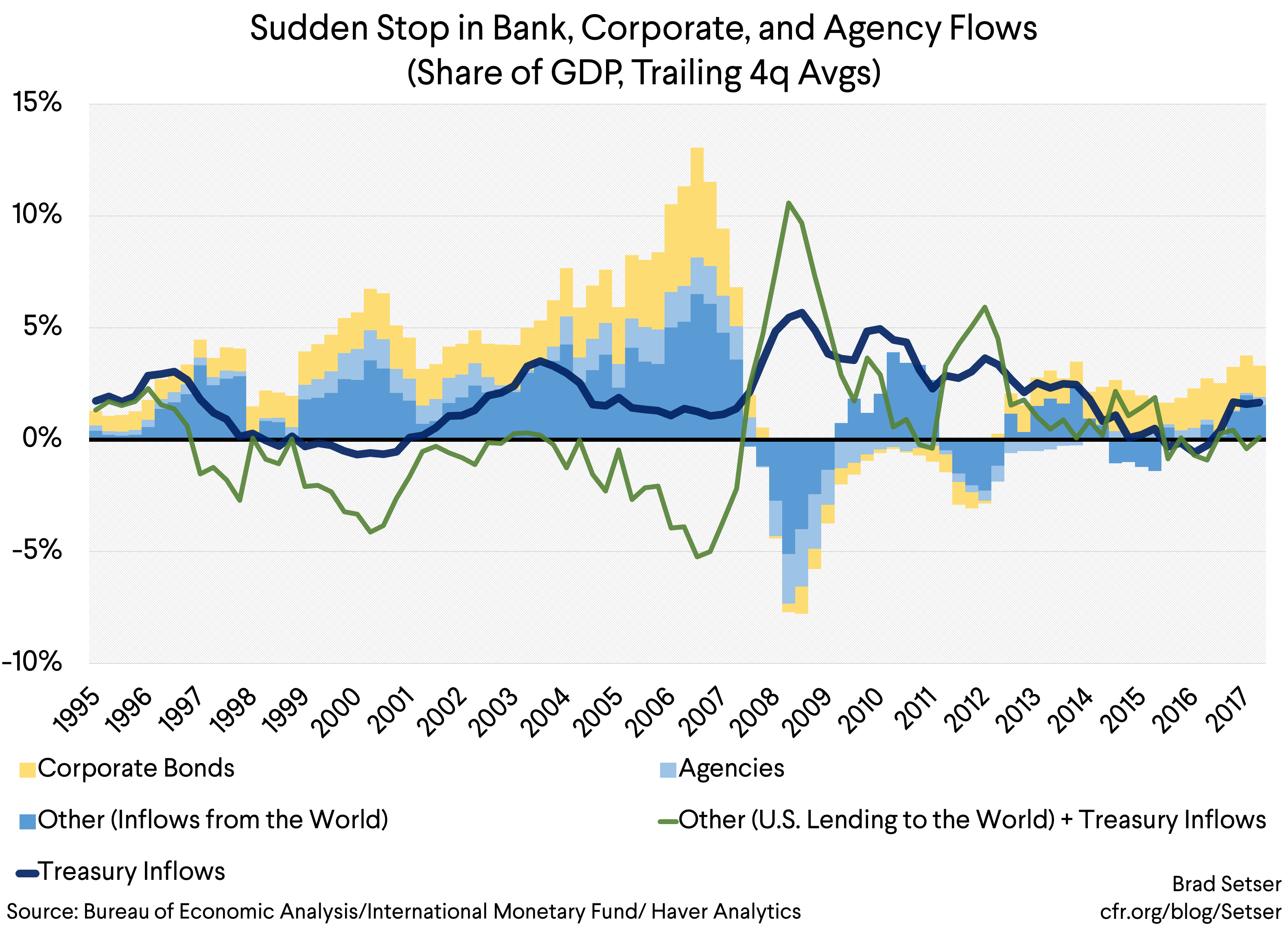

And—if you set aside the relatively stable net inflow from official investors that allowed the U.S. to keep running (for better or worse) current account deficits after the crisis—the U.S. balance of payments did show the kind of instability that is more often associated with emerging markets.

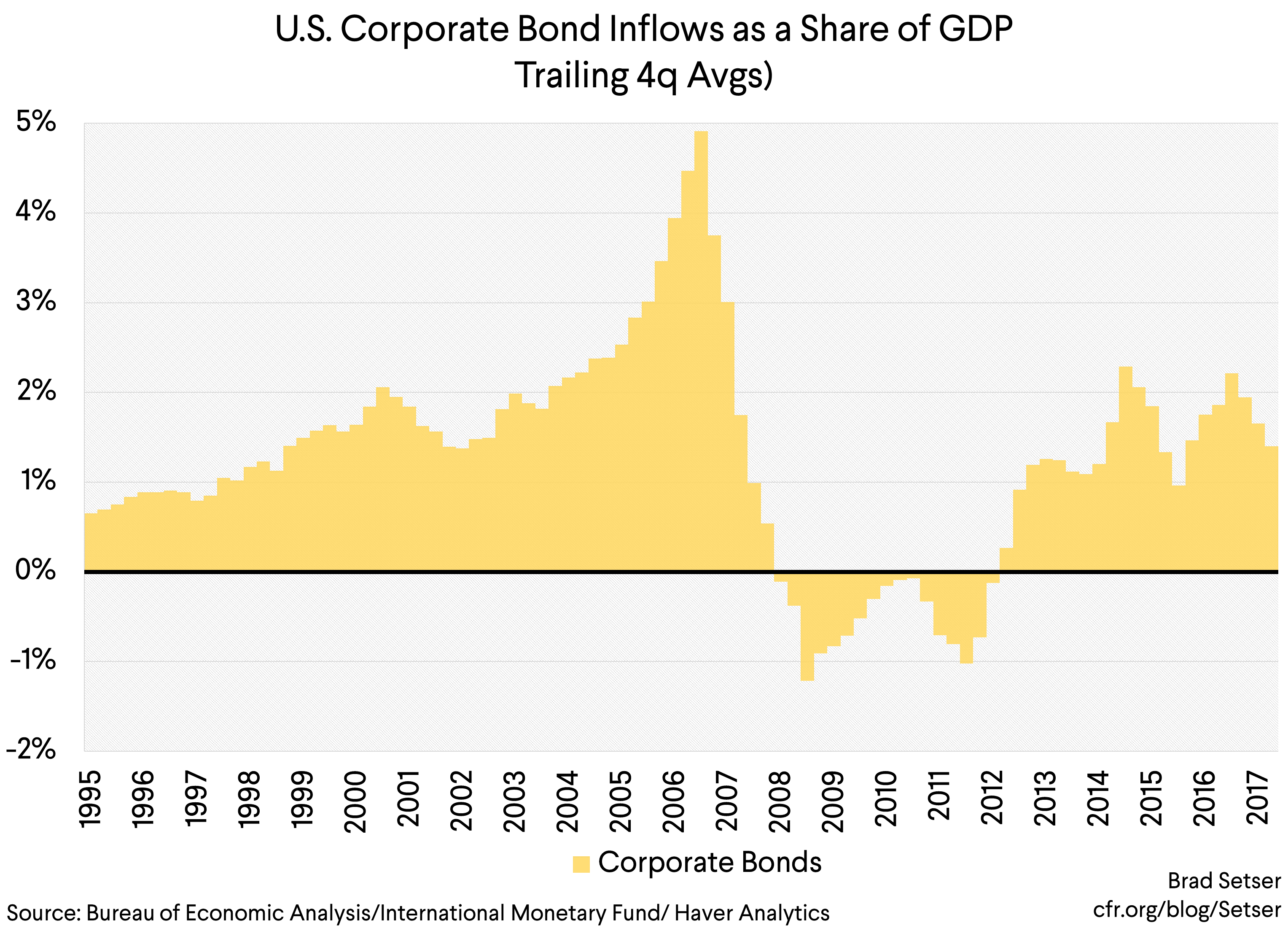

The first sudden stop, of course, came in the summer of 2007. Foreign demand for U.S. corporate bonds had absolutely soared in 2005, 2006, and the first part of 2007. It reached 5 percent of U.S. GDP in early 2007. And it then fell off a cliff.

At the time, unlike now, the typical corporate bond was a “private label” asset backed security. Private label means that it wasn’t issued by one of the federal agencies. And the assets backing these securities were mostly mortgages—part of the famous mortgage money machine that many have written about.

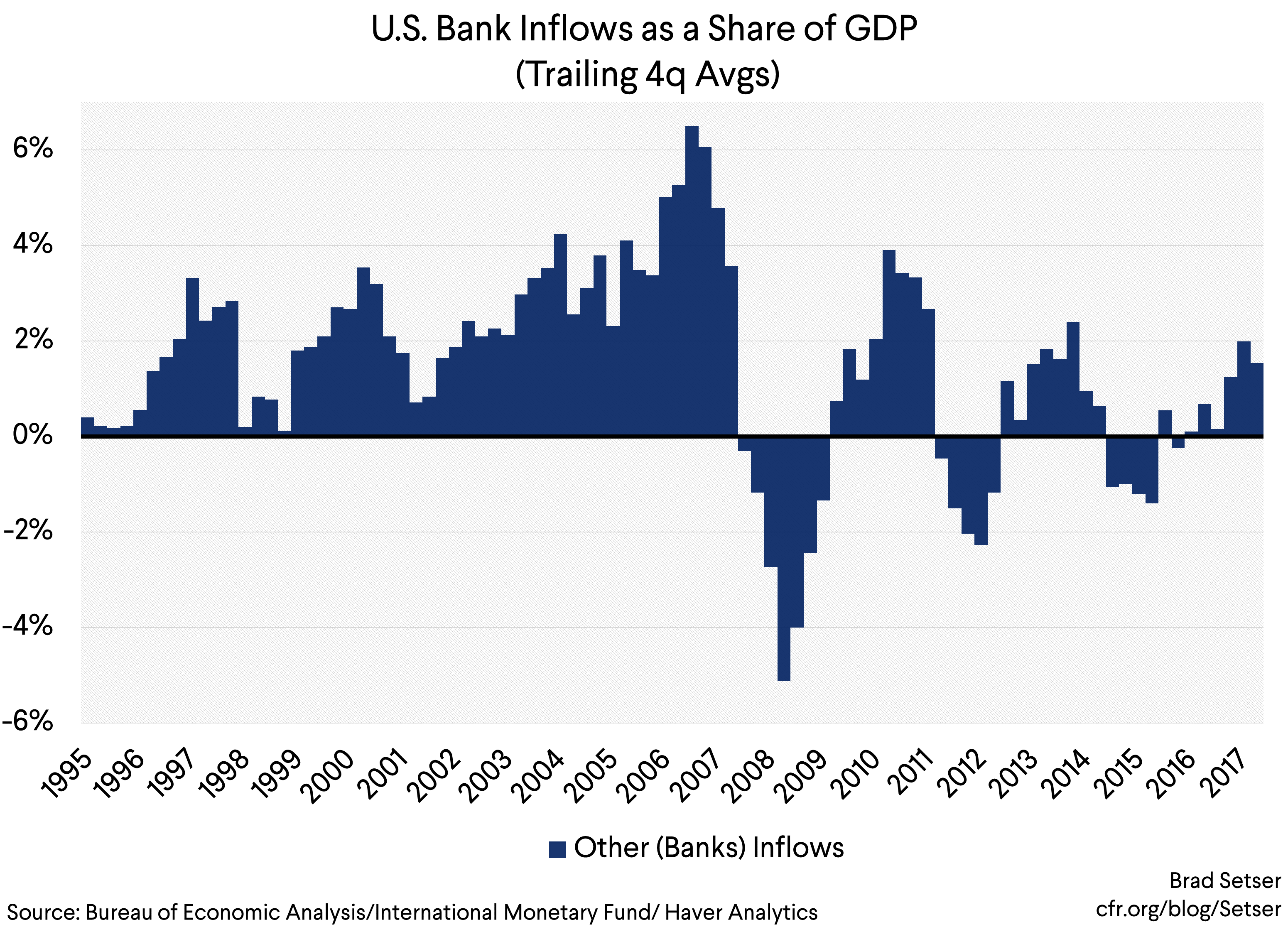

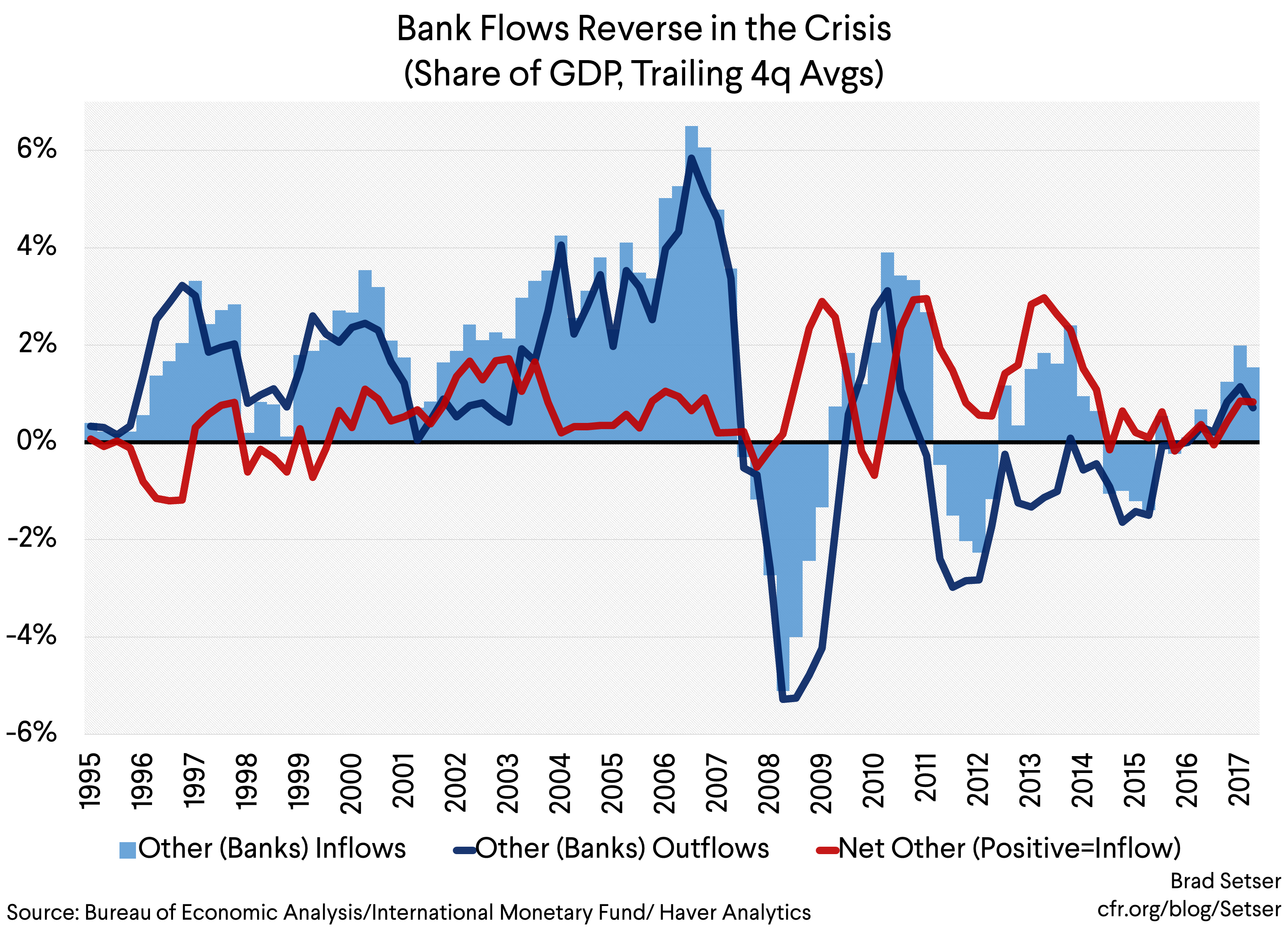

That flow wasn’t the only flow that disappeared during the crisis. “Other” inflows in the United States—basically bank flows—also tanked.

The fall in bank flows came a bit later than the fall in corporate bond flows. But it was equally brutal. The swing from mid-2007 to early 2009 was almost, gulp, ten points of GDP.

Take a four quarter average to smooth out some of the lumps and I think private inflows into U.S. debt swung from a peak inflow of 10 percent of GDP to an outflow of 5 percent of GDP (one note: I assume that all Treasury and Agency purchases are official).

That’s the kind of swing that you see in the most brutal emerging market crises. Or in the euro area back when it was on the edge of breaking apart.

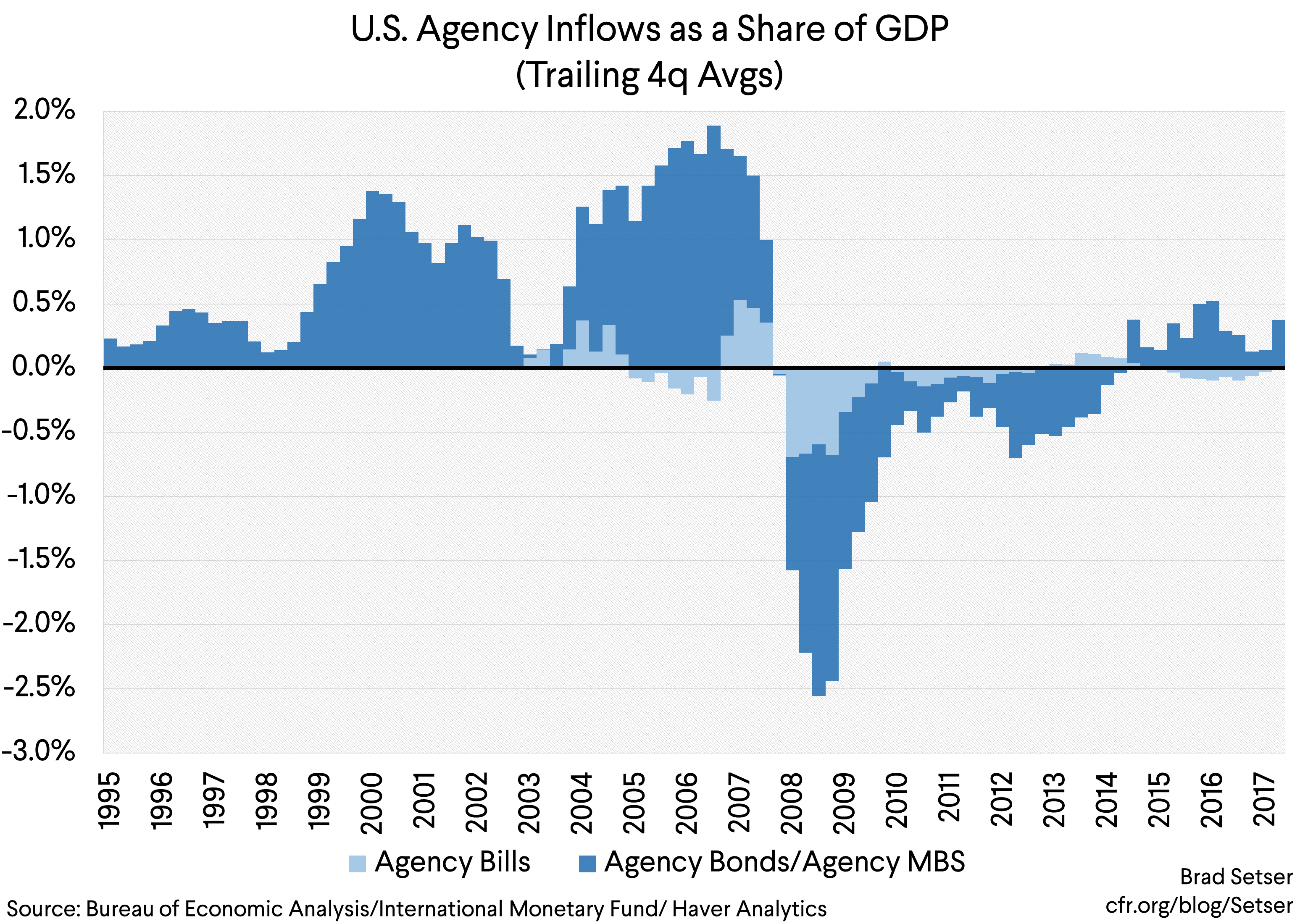

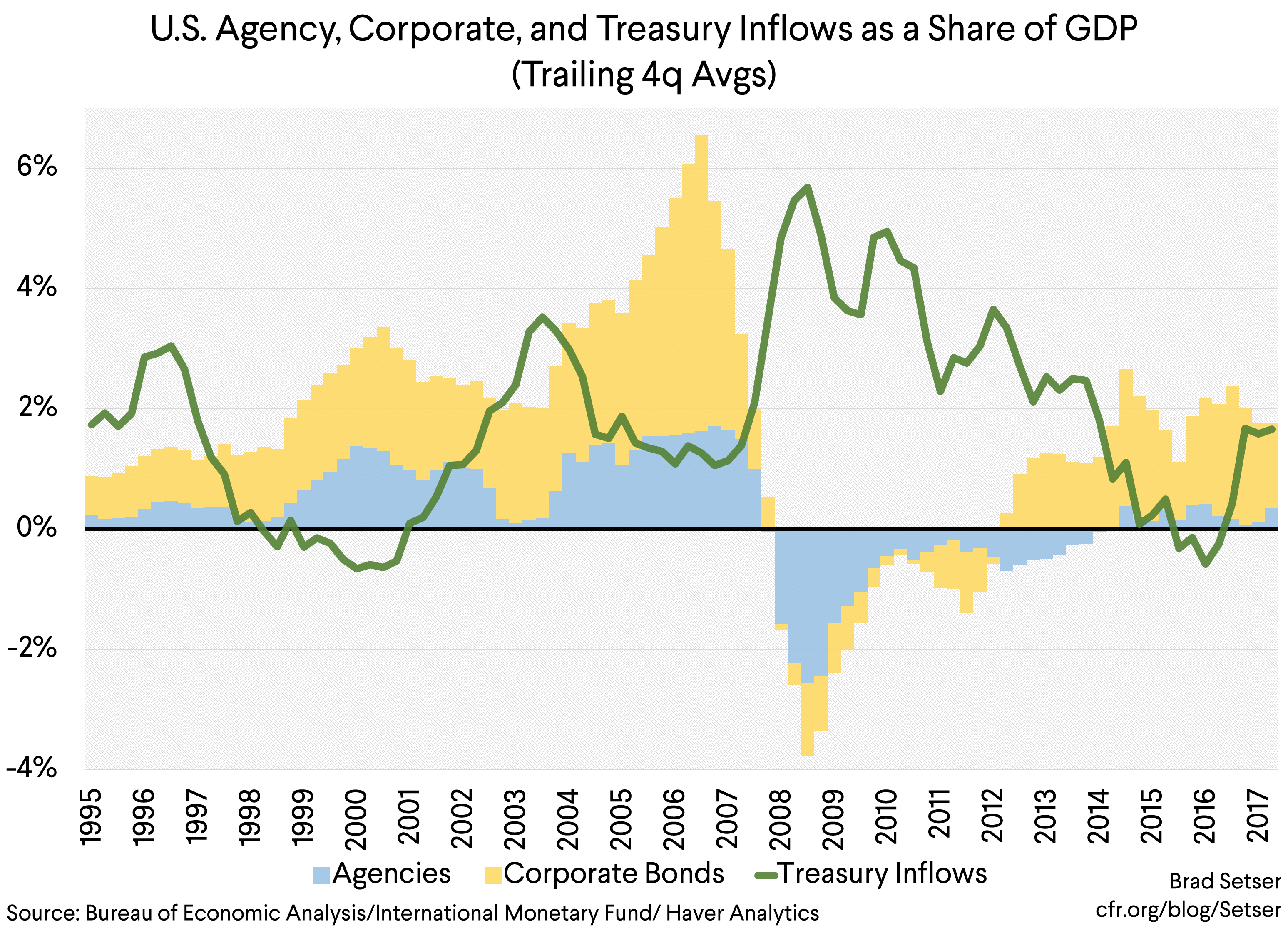

There was a third sudden stop: demand for Agencies dried up in the summer of 2008. Foreign central banks stopped buying Agencies about a year after private demand for private label mortgage backed securities dried up. And the swing was brutal. Ask Hank Paulson.

If you want an alternative crisis history, one option would have been to put the agencies into bankruptcy—and then essentially force the Agencies’ foreign bond holders to absorb the cost of a major restructuring. Read try to shift the cost of mortgage relief onto China.

It probably wouldn’t have worked that well—most Agency bonds were actually held domestically, so restructuring the Agencies would have created domestic financial problems (to put it mildly). And restructuring the mortgages held by the agencies wouldn’t have been enough to address the housing debt overhang either: the most toxic mortgages were in the hands of the banks and others that that had bought private label mortgage-backed securities. Finally, winding down the Agencies would have taken away one of the Fed’s more powerful stimulative tools—purchases of Agency MBS did a lot to help the U.S. economy manage through the most intense post-crisis fiscal consolidation.

But it—conceptually—provides an option. Iceland’s example here is interesting (for another time).

The United States of course went in the other direction—backstopping the Agencies‘ capital, which in turn allowed the Fed to buy large quantities of Agencies at the peak of the crisis and quickly bring down the Agency spread.

That’s the three sudden stops over the course of a little over a year. First in corporate bonds (asset backed securities), then in bank flows, and finally in Agencies.

The first two sudden stops did—contrary to the current narrative—put pressure on the dollar. Remember, the dollar was extremely weak in late 2007 and early 2008. And it would have been even weaker but for massive central bank intervention to bolster the dollar. Asia—and the oil exporting emerging economies—didn’t want their currencies to soar versus the dollar, so they bought dollars in unprecedented quantities. A standard exchange market pressure index that incorporates estimated foreign central bank purchases of the dollar (inferred from the COFER data) shows “peak” weakness in late 2007 and early 2008.

Of course, the dollar did rally in late 2008. That is unquestionably an important part of the story too.

And overall demand for all U.S. assets didn’t fall. The overall U.S. balance of payments was stabilized by two large inflows. Treasury purchases, obviously. And U.S. bank (and money market) lending coming home (The green line in the graph is the sum of reverse bank flows and Treasury inflows).

The reversal of bank outflows doesn’t get much attention because it was to a large degree the mirror image of the reversal of bank inflows. Most of this occurred in dollars—so its foreign exchange impact wasn’t so big. Even so the net inflow from the reversal of “other” (bank) flows in the balance of payments was over 2 percent of GDP in 2009.

This fall is a clear sign of the overall “deleveraging” that took place throughout the global financial system during the crisis—foreign banks reduced their short-term lending to the United States, and U.S. banks reduced their short-term lending to the world.

But I still think it is important to note that a large part of the inflow into the United States during the crisis was U.S. money coming home not foreigners wanting U.S. financial assets at the peak of the crisis. Foreign money was generally going home. At least private money.

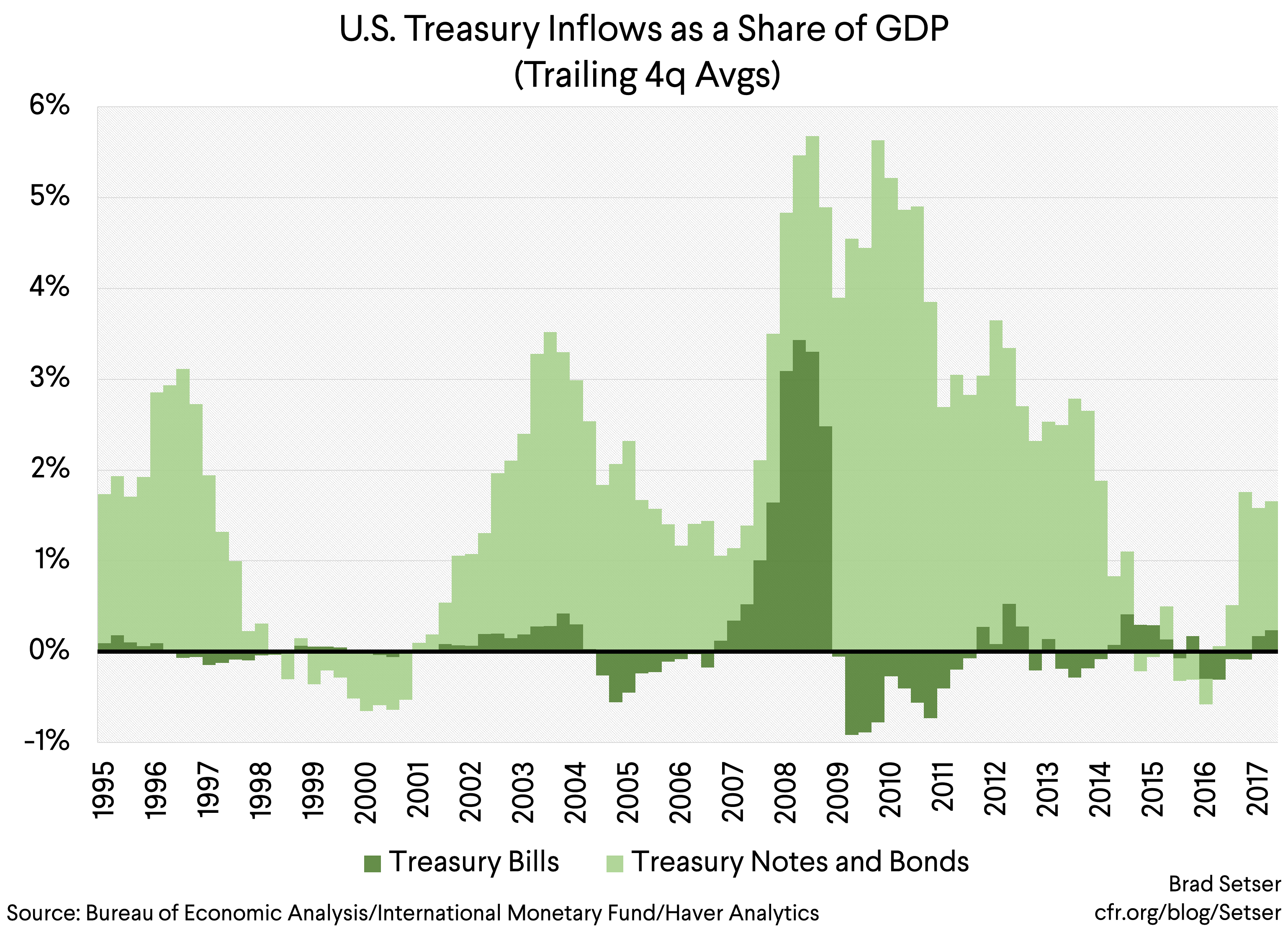

The initial surge in demand for Treasuries during the crisis largely was directed at bills. China’s bill holdings went from $15 billion in June 2008 to a peak of over $200 billion; total central bank holdings rose from $200 billion to around $600 billion. The flow into notes and bonds came later.

I have long wondered exactly where all the central bank funds that moved into bills came from—inflows into Treasuries then topped what I would have expected based on my work tracking reserve growth.

And on the other hand, I couldn’t find a lot of global reserves in the U.S. balance of payments data in 2007 and 2008.** Inflows into U.S. Treasury and Agency bonds usually track global reserve growth relatively well, but there was a clear gap then.

Some of that was central banks trying to be sovereign wealth funds and taking on equity risk.

Some of that—perhaps—was a shift into euros. China isn’t in the data for global reserve composition in this period, so there is a large “known unknown.”

And I increasingly suspect, with a flat yield curve, a number of central banks got into the business of funding banks’ balance sheets. Through dollar deposits offshore. And likely through the unwinding of cross currency swaps. Just a hunch on the last point—it is something I want to investigate further.

The implication is that the run on European banks‘ dollar funding was, in part, a run by the world’s dollar heavy central banks…one that in the end was solved by swaps funding from the Fed.

There is a bigger story here too—in the run up to the U.S. crisis, gross flows into the United States soared, running far above the (considerable) sums needed to maintain the United States 5-6 percent of GDP current account deficit.

I think I now understand this—though I didn’t at the time.

In the run up to the global crisis, the U.S. fiscal deficit was far smaller than the current account deficit. Fully funding the external deficit took more than foreign reserve managers buying U.S. Treasury bonds. The surge in gross flows reflected the need for more complex chains of financial intermediation (to use the terminology and concepts of Brender and Pisani’s amazing monograph).

Think of it this way.

The marginal borrower who needed financing was a U.S. household taking out a home equity line of credit. And the global creditor willing to buy dollar assets and finance the U.S. external deficit was an Asian (or Gulf) central bank resisting the appreciation of their own currency. But central banks, by and large, didn’t want to take the risk of lending to U.S. households. They would buy an Agency—and let the U.S. government (implicitly) take the risk. Or they would put their funds on deposit in a bank (the yield curve was flat, it didn’t mean losing money) or swap dollars for euros (providing a European bank dollar funding, while the central bank could take the euros and buy “safe” European government bonds) and then the bank would buy a package of securitized finance.

The huge gross flows—the big bank inflows and outflows in others, the large corporate bond purchases—in the run up to the U.S. crisis were the visible traces that these complex chains of financial intermediation left in the balance of payments data.

There was a signal there. And that signal was, by and large, missed.***

The conventional wisdom at the time was that these large flows indicated that a global financial system was dispersing the risk associated with funding the U.S. housing bubble globally, reducing the risk any correction posed to the U.S. financial system.

We learned the hard way that wasn’t really true. The complicated chains of financial intermediation needed to use in some deep sense central bank money to fund subprime mortgages were actually quite fragile.

And the weakest link in the chain was the ability and willingness of private investors to take credit risk, not the ability and willingness of foreign central banks to add to their dollar holdings.

That at least is what I think I learned from the crisis.

Note: This initially started in part as a review of Adam Tooze’s Crashed. But I quickly realized it wasn’t much of a review. Probably because I lack the necessary distance from the events (and or at least the flows) described in his book. Crashed is by far the best account of the “transatlantic” angle of the 2008 banking and credit crisis that I have read: it fully deserves all the accolades it has received.

*A lot of European banks were effectively running U.S. shadow banks. They ran wholesale funded credit portfolios. Most of the big U.S. broker-dealers weren’t much different. And some U.S. banks sponsored “shadow banks” of their own. Think of Citi’s SIVs.

**I assume that the “unallocated” portion of global reserves in the IMF’s data has a currency composition equal to allocated reserves. I assume, based in part on the correlation in the graph, that all foreign purchases of long-term Treasuries and Agencies come from “official” accounts (true official purchases could be smaller, but they couldn’t be larger). And, just to show off a bit, I included an estimate of the growth in sovereign wealth fund assets based on the flow data in the balance of payments from key countries (China, Korea, Singapore, and the main Gulf countries), and assumed 50 percent of that flow went into dollars.

***Hyun Shin is an important exception here.