The Trump Tax Reform, As Seen in the U.S. Balance of Payments Data

The international side of the Tax Cuts and Jobs Act was a real reform, not just a straight-forward cut in the rate. It ended deferral, and shifted to a (mostly) territorial tax system. Yet, judging from the balance of payments data, it didn’t get rid of the incentive for firms to offshore profits to low-tax jurisdictions. The global minimum is too low—and there are too many incentives to shift tangible assets abroad.

“Trillions of dollars in trapped profits will return to the United States”*

“With a lower tax rate, U.S. firms will no longer have an incentive to offshore.”**

“The tax cuts will make America a more competitive location for manufacturing.”***

I have heard all three arguments, in various forms.

All three claims can now be evaluated against the numbers—we now have five quarters of post-tax cut data.

All three arguments, in my view, come up short.

Those trillions of profits held offshore? That was always both true and untrue.

It was certainly the case that the old tax code created an incentive for firms to “reinvest” their offshore profits offshore, and by so doing, defer paying U.S. corporate income tax while waiting for (and lobbying for) a tax holiday to “free” all of those “trapped” profits.

But it is also true that funds “reinvested” offshore weren’t really held offshore—the bulk of the reinvested profits was held in dollars, and the bulk of those dollars were lent back to the United States. Firms that had large “cash” positions in Ireland invested the bulk of those profits in U.S. Treasury**** and U.S. corporate bonds, along with bank deposits and money market funds.

And it turns out that the firms were much keener on settling their deferred tax liability at a low rate than in legally moving the funds back to the United States.

With the tax reform, there is no longer a tax incentive to maintain the whole “offshore” profit charade. Under the new law, there is no tax difference between funds earned in Ireland and sent back to the United States and funds earned in Ireland and held (notionally) in the bank account of the fund’s Irish subsidiary. And the deferred tax liability on legacy profits has been settled (by what is called “deemed repatriation”). A firm that wants to bring its previously “offshore” funds home can, with no additional tax (the global minimum tax on intangible income is the only tax the United States imposes on offshore income, and that tax cannot be deferred by holding funds “offshore”).

What has happened?

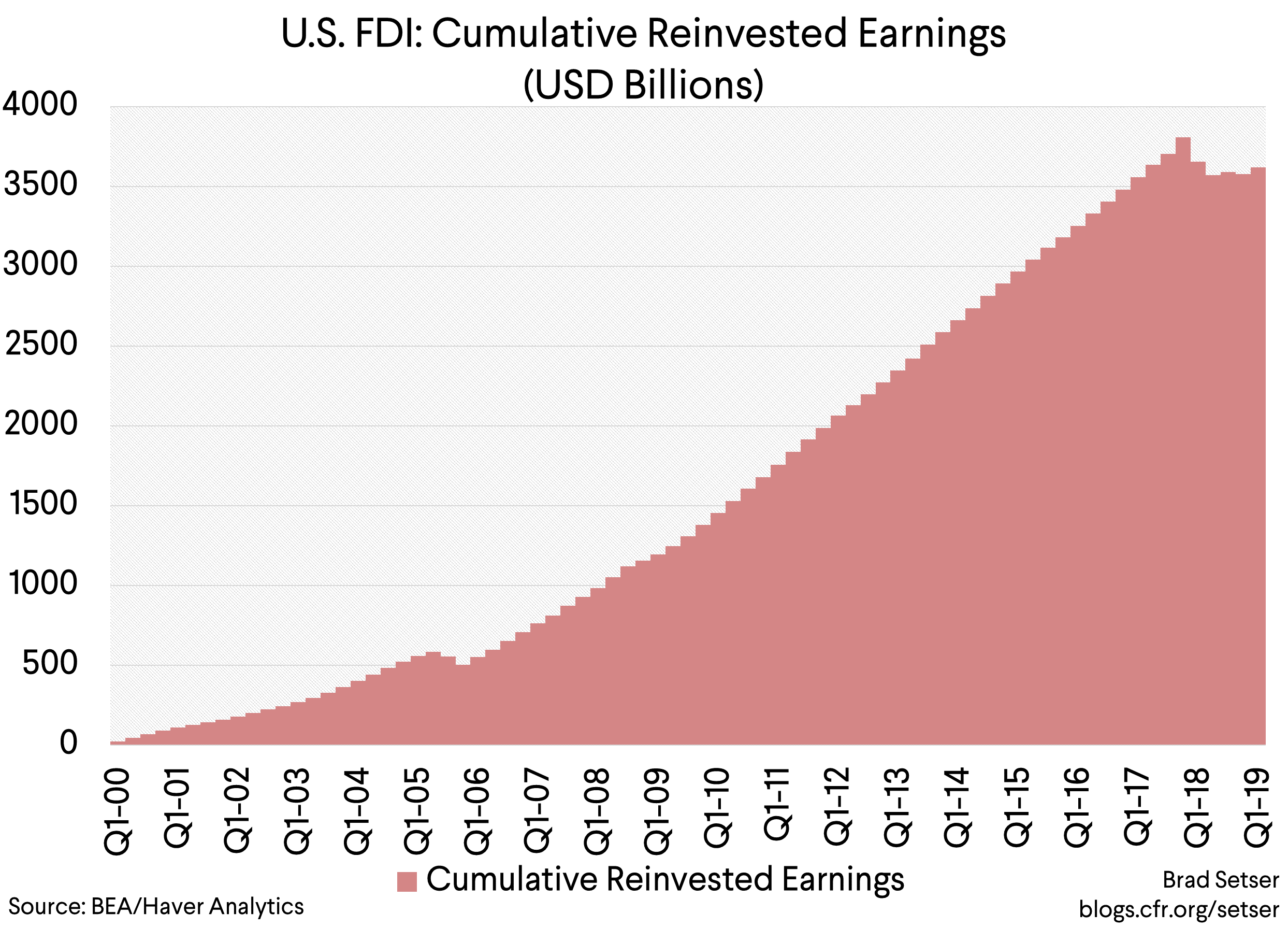

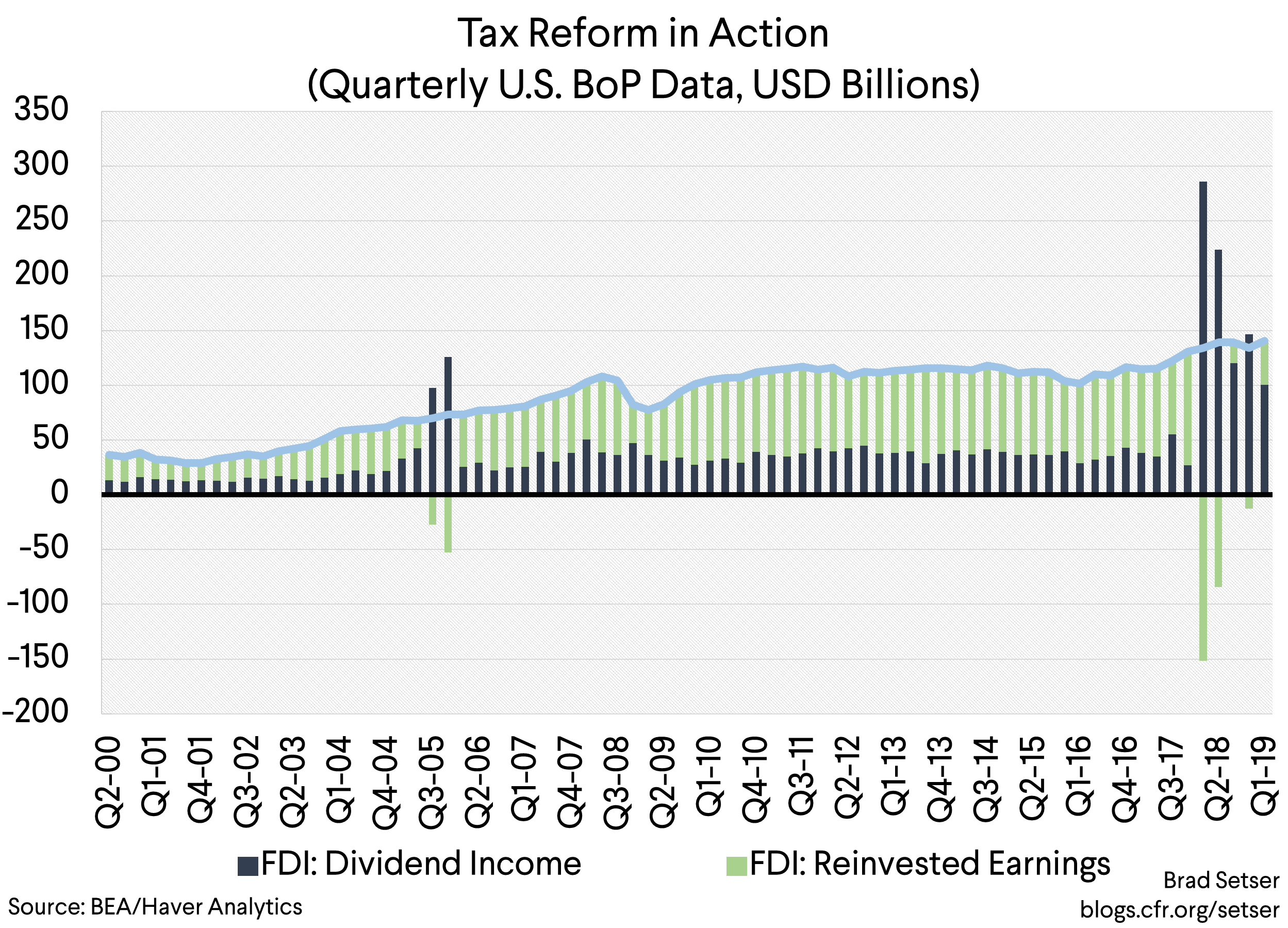

Some money has moved back (as one would expect), but not all that much.

And in the first quarter firms returned to “reinvesting” a portion of their offshore profit back abroad. The cumulative sum of “reinvested earnings” is rising again.

Given all the rhetoric about the cost to the United States of all these trapped profits, the reality that only a small amount, on net, has come back to the United States should be a bit sobering. It turns out that most firms weren’t all that inconvenienced by their large offshore cash balances. Those that really wanted to do a buyback could borrow against their offshore profits. Those that wanted to wait until the tax code changed before doing a buyback could do that too, as the market expected that the bulk of the cash would eventually be returned to shareholders.

Technically speaking, about $248 billion of formerly offshore profit was returned (That is the sum of the “negative” numbers on reinvested earnings, and sum consistent with the findings of the Wall Street Journal, which found a roughly $300 billion drop in the overall cash balance of U.S. firms in 2019). Obviously, the net number masks a more complicated reality, as some firms have reduced their offshore cash while others are “reinvesting” their offshore earnings in real rather than financial assets. If you look at repatriation relative to some kind of baseline, somewhere between $300 and $600 billion came back.***** Those who do forensic accounting by summing up the reported financial assets of the major U.S. firms likely can produce a better number—I personally am waiting for the detailed information on reinvested earnings by jurisdiction that should come out in July, as, well, I like using the balance of payments data for this…

The scale of the return of the “trapped” legacy profits has political resonance, a lot of people perhaps believed that the funds really were “trapped” and could be “unlocked” to fund a wave of investment. But in reality the bulk of the funds were in extremely profitable companies that had no internal use for the cash they were generating, and thus the funds were always going to flow back to shareholders.

Substantively, what really matters is whether the new tax code got rid of the incentive for firms to “offshore” a large portion of their profits.

And the answer is clear.

It didn’t.

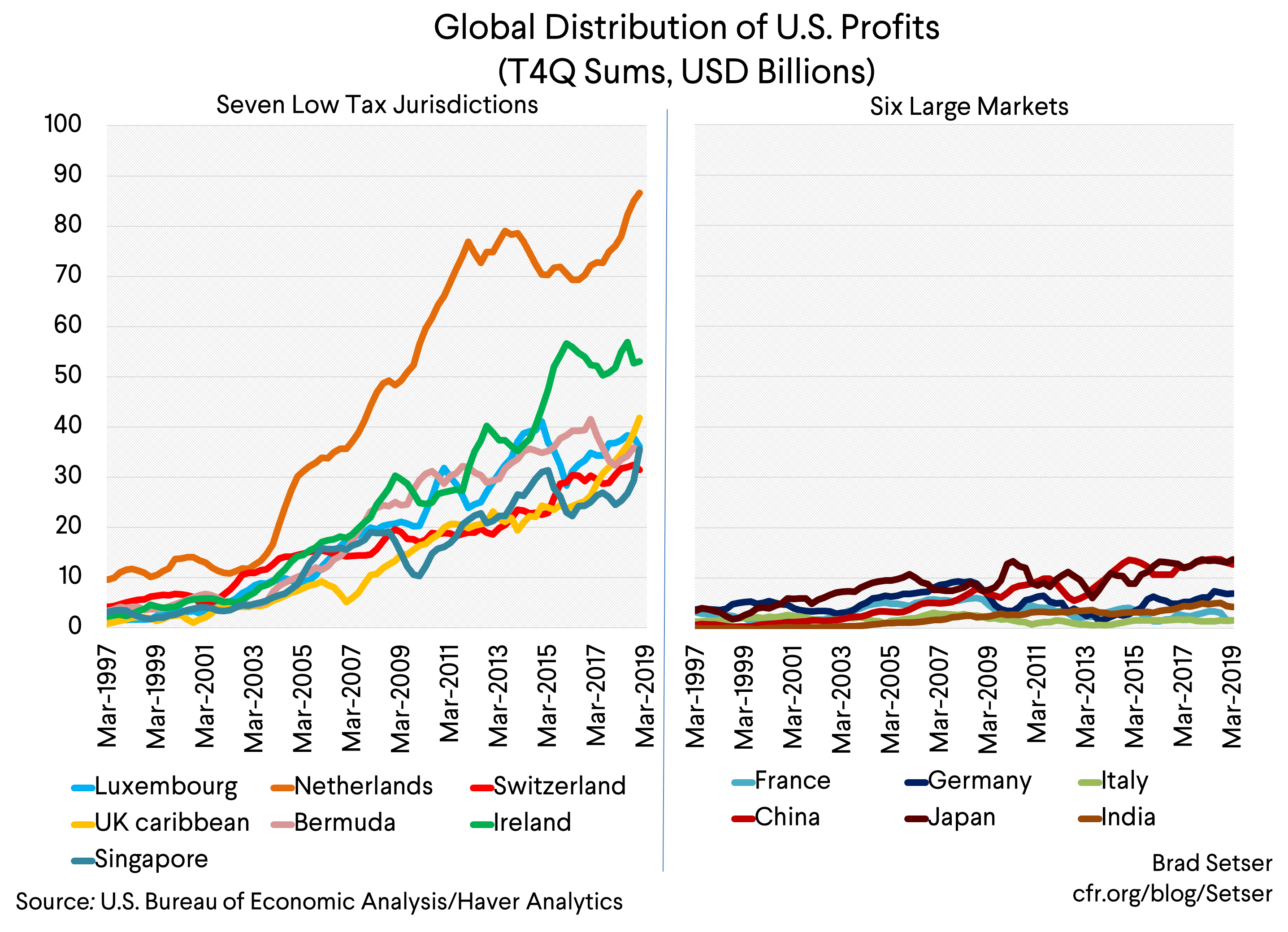

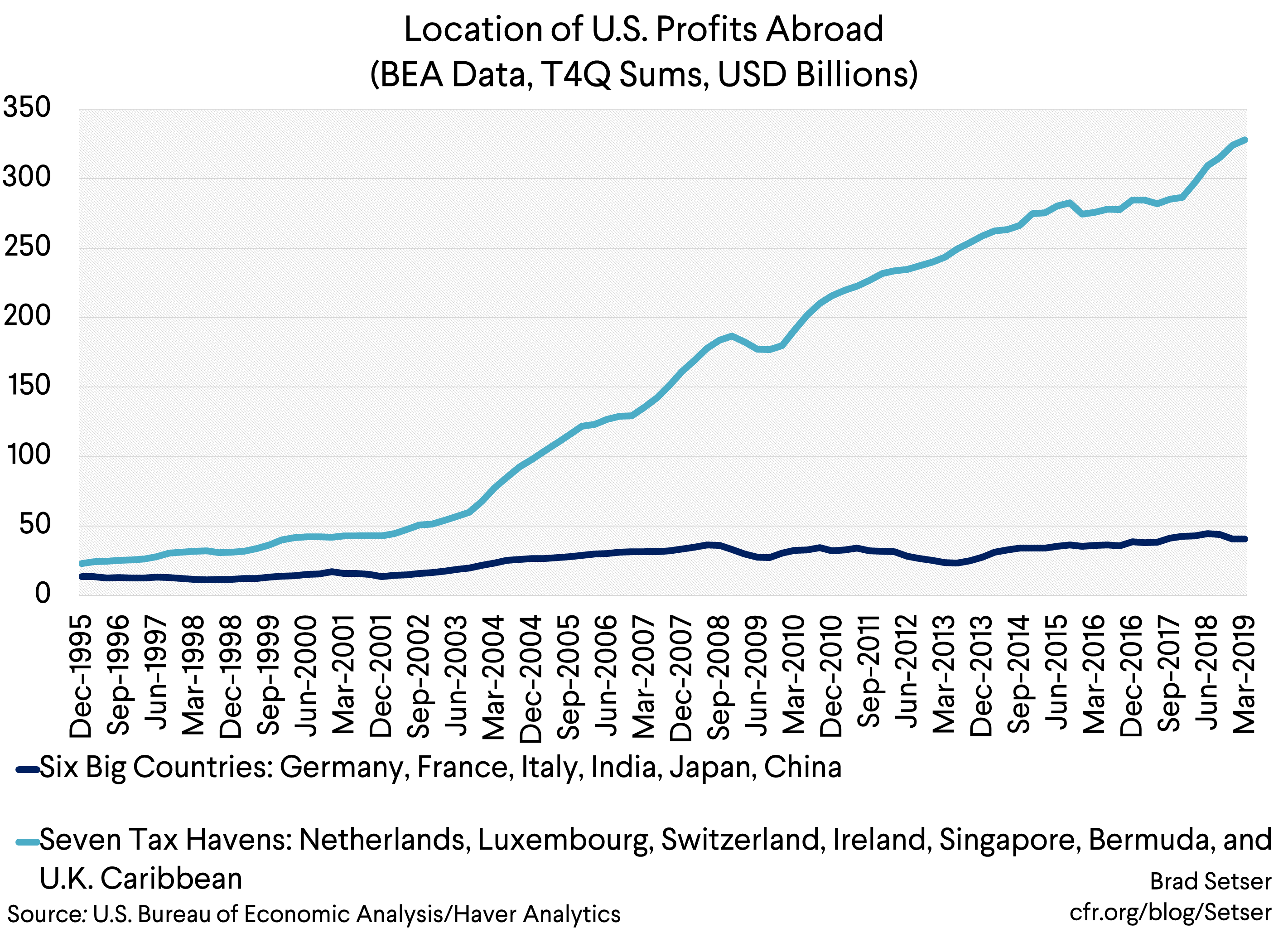

The amount of profit that American firms report in the world’s low tax jurisdictions is the strongest single bit of evidence that the current process of globalization needs to be reformed. U.S. firms report to earn about 1.5 pp of U.S. GDP in Ireland, the Netherlands, Switzerland, Singapore, and a bunch of really small Caribbean islands. That is far more income than U.S. firms report in large market countries like Germany, France, Italy, China, Japan, India, and Mexico. Clearly something is going on (the countries in Europe are well aware of this, the non-taxation of the profits U.S. tech firms earn in Europe has long vexed them).

The data on the global distribution of U.S. FDI tells the same story—the majority of FDI by value is now claims on those same low tax jurisdictions (Don’t trust me? Look at table 1 of the BEA’s release on U.S. direct investment abroad and the IRS data on what kind of profits U.S. firms report and what kind of tax they pay in different jurisdictions).

What happened after tax reform?

The profit U.S. firms report in these low tax jurisdictions went up.

The large offshore profits of the tech and pharma industries didn’t suddenly move to the United States where they would be taxed at 21 percent. Instead, they stayed offshore and were taxed at the global minimum of 10.5 percent. Sort of like one might have expected.

There is an added complexity, as tax reform also created a special low tax rate on the export of intangibles to try to encourage firms to “onshore” their intellectual property. Some firms have used this provision—Qualcomm for example, which is boasting about an effective tax rate in the single digits—but not all that many. At least not to date. There hasn’t been a surge in U.S. intellectual property exports after the tax reform. And well getting those profits “home” by taxing them at a low “offshore” rate is hardly a huge victory—especially as the special low tax rate for exporting intangibles encourages firms to move their tangible assets (think factories) abroad. Onshoring a firm’s IP while offshoring more manufacturing jobs isn’t much of a win.

A bit of background here. The biggest profit shifters in the U.S. economy are the technology and pharmaceutical firms (tax shifting corresponds well with the size of your “trapped” offshore profits, and well, we know the old tax structure of Apple and Microsoft).

But their tax games are a bit different. Most of the tech firms pay U.S. tax on their U.S. profit—their game was to get their tax on the profits they earned on their foreign sales (generally using intellectual property and business models generally developed in the United States) down to zero or close to it. The old tax code encouraged them to export underpriced intellectual property to their subsidiaries in tax havens (or business services—the “R&D cost share” was a standard way to move intellectual property offshore) and then book large profits offshore.

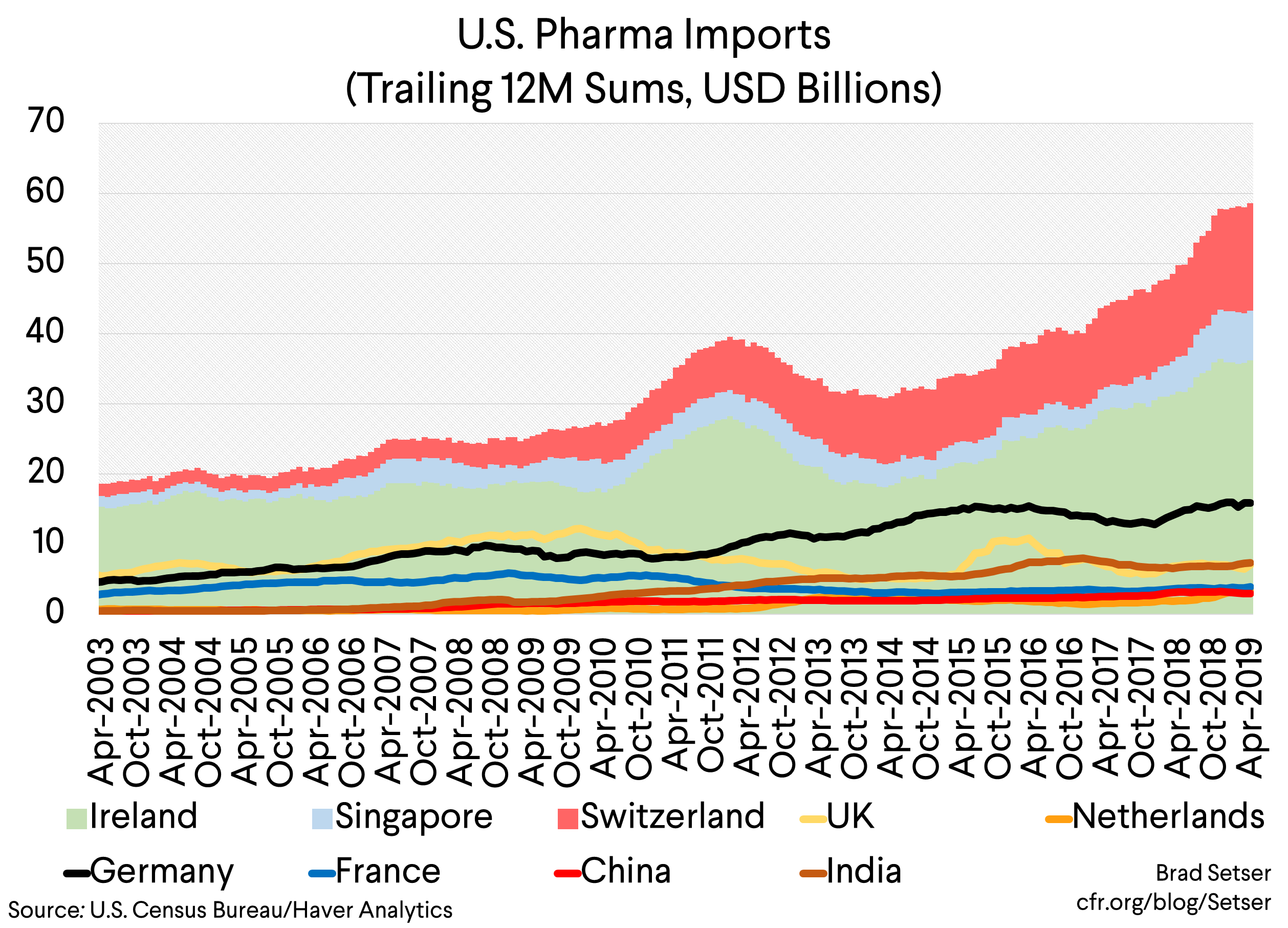

Pharmaceutical companies by contrast typically try to shift some of the profit they earn in the United States (their most profitable market) abroad. That’s why so many of the active ingredients are manufactured in low tax jurisdictions. The “pharma” tax game thus results in a rise in imports (of goods) more than a reduction in exports (though firms of course also produce abroad for the non-U.S. market too).

Some chip design firms have a similar tax game—they used to export their chip designs to an offshore subsidiary (see Qualcomm’s description of why it reversed its structure). And then the firm’s offshore subsidiary would book the profit from the sale of the chips, which typically were produced by one of the big contract manufactures. That overall structure reduces U.S. exports of chips—it is part of the reason why the U.S. chip design industry designs 50 percent of the world chips while less than 15 percent of those chips are made in the United States.

There are of course other tax games—coffee for big chains somehow always seems to be roasted in Switzerland, Pepsi makes Pepsi concentrate in Ireland and Singapore and the like. But the big bucks come from a few sectors and in a few firms. That’s why the top fifteen firms accounted for 80 percent of the “trapped” profits, and that is why five firms hold around a third of all the cash held by U.S. corporations.

There consequently is another way the tax reform can be evaluated—namely, by looking at the balance of trade in those sectors where the old tax code encouraged imports at the expense of U.S. production.

And there too the results have been a little disappointing…U.S. imports of pharmaceutical products, for example, rose substantially in 2018 (less so in 2019). And guess where that rise came from?

Ireland, Singapore and Switzerland…

I think at this stage it is clear that the tax reform didn’t get rid of the perverse incentives created by the old tax code. A real reform would have raised the overall tax rate on those firms that most aggressively shifted profits abroad. That decidedly has not happened.

And so far at least it is also hard to see the impact of the OECD’s base erosion and profit shifting (BEPS) initiative in the overall data…

Then again, the biggest “win” in that process is Ireland’s commitment to unwind all double Irish structures (in a double Irish, a firm has two Irish subsidiaries, but only one is a tax resident of Ireland—the other wasn’t Irish for tax purposes). So firms are looking for new tax structures. Apple adopted a tax structure that keeps a large share of the profit from its intellectual property offshore—in Ireland actually, where it is able to depreciate the “purchase” price of its own IP from another tax subsidiary and thus lower its “Irish” tax rate to under 3 percent (see the Wikipedia entry on the “Green Jersey”). I suspect others will too. But some may follow Qualcomm and onshore their intellectual property (paying the 13.125 percent foreign derived intangible income tax rate, or somewhat less) while keeping production largely abroad.

For now, though, the size of the offshore profit U.S. firms report to earn in a small number of tax havens remains the single best way of tracking the distortions embedded in the current U.S. and global system of taxing corporate profits. And it isn’t telling a very patriotic story.

* “But we expect that it could be — the number started out at about $2.5 trillion; we think it’s going to be close to $5 trillion,” he [Trump] said, speaking to business leaders from PepsiCo, Boeing, FedEx, Mastercard, and Honeywell. “Over $4 [trillion], but close to $5 trillion, will be brought back into our country. This is money that would never, ever be seen again by the workers and the people of our country.” (Source)

** Kevin Hassett: “There is also a literature that looks at the relationship between tax rates and transfer pricing. That literature implies that a corporate tax cut to 20 percent would dramatically reduce the trade deficit and increase GDP accordingly.”

*** The Trump White House: “American manufacturers are optimistic like never before, because President Trump’s tax cuts and relief make them more competitive.”

*** Ireland’s holdings of U.S. Treasuries peaked just over a year ago, but it remains the fourth largest holder of U.S. Treasury bonds in the world. Just ahead of Switzerland, Luxembourg, and the Cayman Islands...

**** Total dividend payments from U.S. owned offshore subsidiaries back to their U.S. parents in 2018 were just over $750 billion. But the pre-tax reform norm was about $150 billion. That makes $600 billion a plausible upper limit. However, as the well known left wing rag the Wall Street Journal notes, the right baseline is really the post-tax reform norm (the idea is to calculate the dividend payments above what would be expected, as those are the “repatriation” of past profits stuffed away offshore. Judging from Q1, the new norm is $400 billion, which puts the “above normal” dividend at around $350 billion. $250 billion is clearly the lower bound, at least that much was returned. The Journal’s roughly $300 billion fall in the cash balance of U.S. public corporations seems about right to me actually (it is derived from work done by Moody’s, and comes from a bottom’s up analysis of U.S. firms).