Why the U.S. Tax Reform’s International Provisions Need to Be Reformed

I wanted to follow up on a few points that I didn’t have space to explore in my New York Times op-ed on the international provisions of Trump’s corporate tax reform.

The first is that, well, there isn’t any real doubt that firms borrowed against their offshore cash. These funds weren’t really offshore: “Of the 15 companies with the largest cash balances—companies that hold almost $1 trillion in cash—about 95 percent of the total cash was invested in the U.S.” And it wasn’t that hard for firms to borrow onshore against their legally but not really offshore cash in order to pay dividends, fund buybacks, or, if they wanted, to increase their onshore investment.

This is well recognized by those who have focused on the impact of the reform on the corporate debt market (see Alexandra Scaggs‘ summary of Zoltan Pozsar). A set of big technology companies had large (offshore) assets and significant (onshore) debts, and they are now likely to slowly run down their cash balances and pay down those debts.

And I suspect it is a big reason why parts of the balance of payments data look a bit funky this year.

This is kind of complicated—when firms had large “cash” balances offshore those cash balances showed up in the U.S. balance of payments data as foreign direct investment (the U.S. parent had assets abroad, and the cash balance was an asset of their 100 percent owned foreign subsidiary so it counted as “FDI”). Yet the portion of FDI abroad that was really “cash” abroad was often invested in U.S. bonds. The net effect then was a rise in U.S. direct investment abroad (typically through reinvested earnings) and a rise in the amount of debt held by the rest of the world (a U.S. subsidiary that is legally located abroad isn’t a U.S. resident for balance of payments purposes).

So what’s happened subsequent to the reform, which ended the incentive to hold cash abroad to defer a portion of a firms‘ tax burden until their was some form of tax holiday?

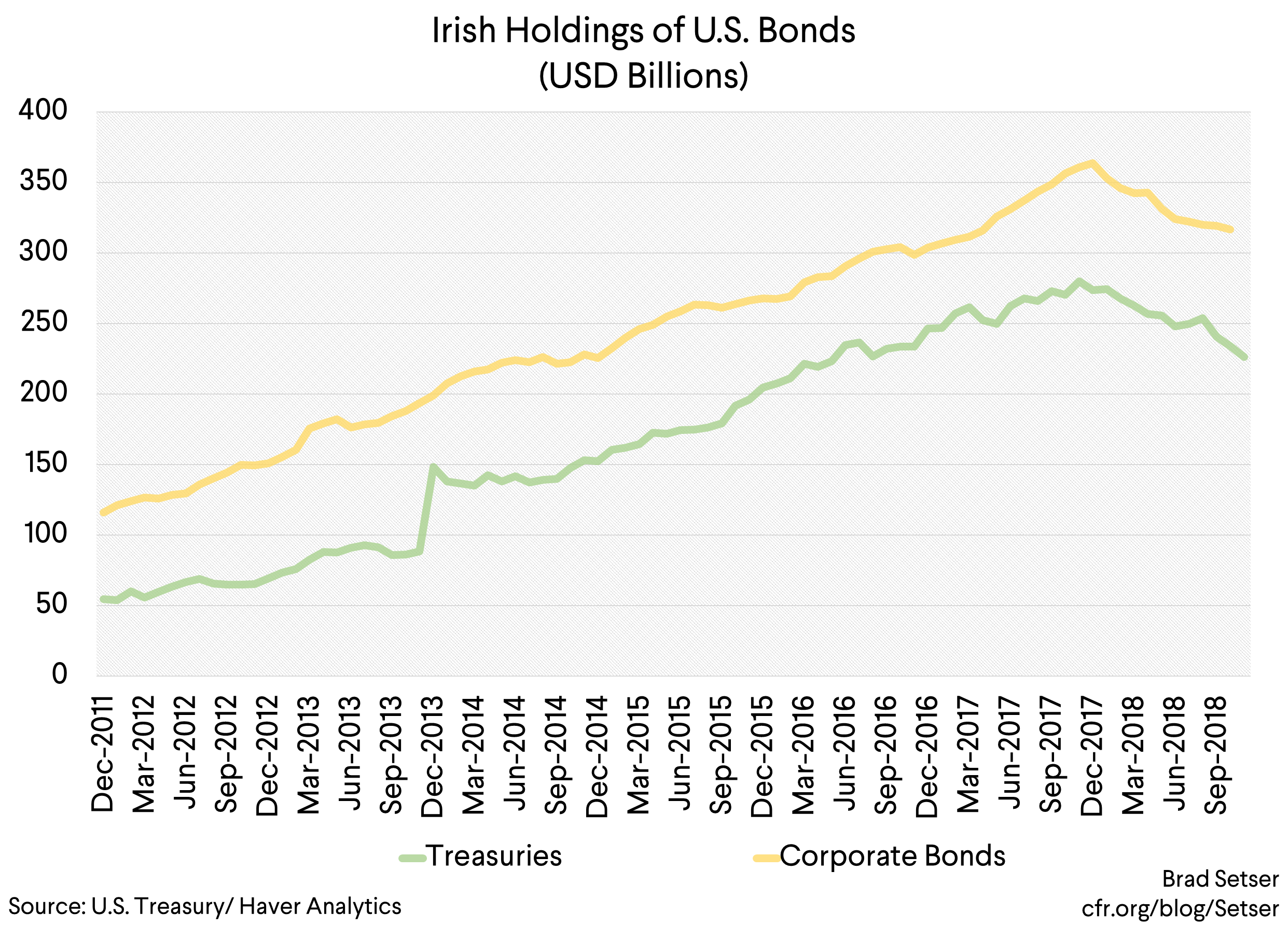

Firms have been bringing some of that cash home (so FDI abroad has been falling) and reducing the bonds held by their offshore subsidiaries. We see this for example in the data for Ireland’s holdings of U.S. treasuries, which have fallen by close to $50 billion since last December. Ireland’s holdings here are also down by about $50 billion.

The second is that the tax reform’s low rate for global intangibles left a lot of revenue on the table.

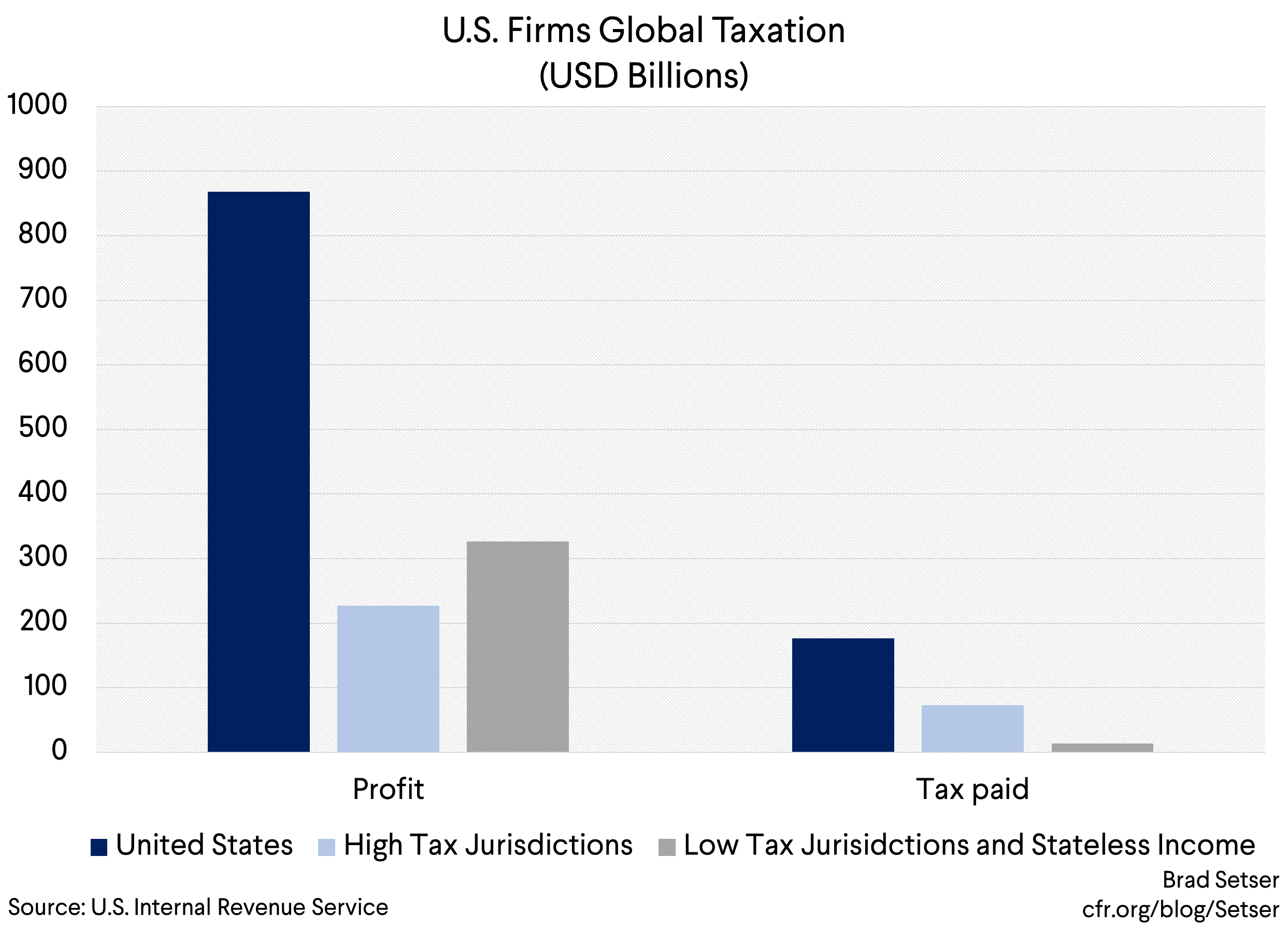

The IRS now has a wonderful data set showing the global distribution of the profits of U.S. firms—and the global distribution of the taxes they actually paid. The numbers are from 2016, so before the tax reform. But they give some sense of the magnitude.

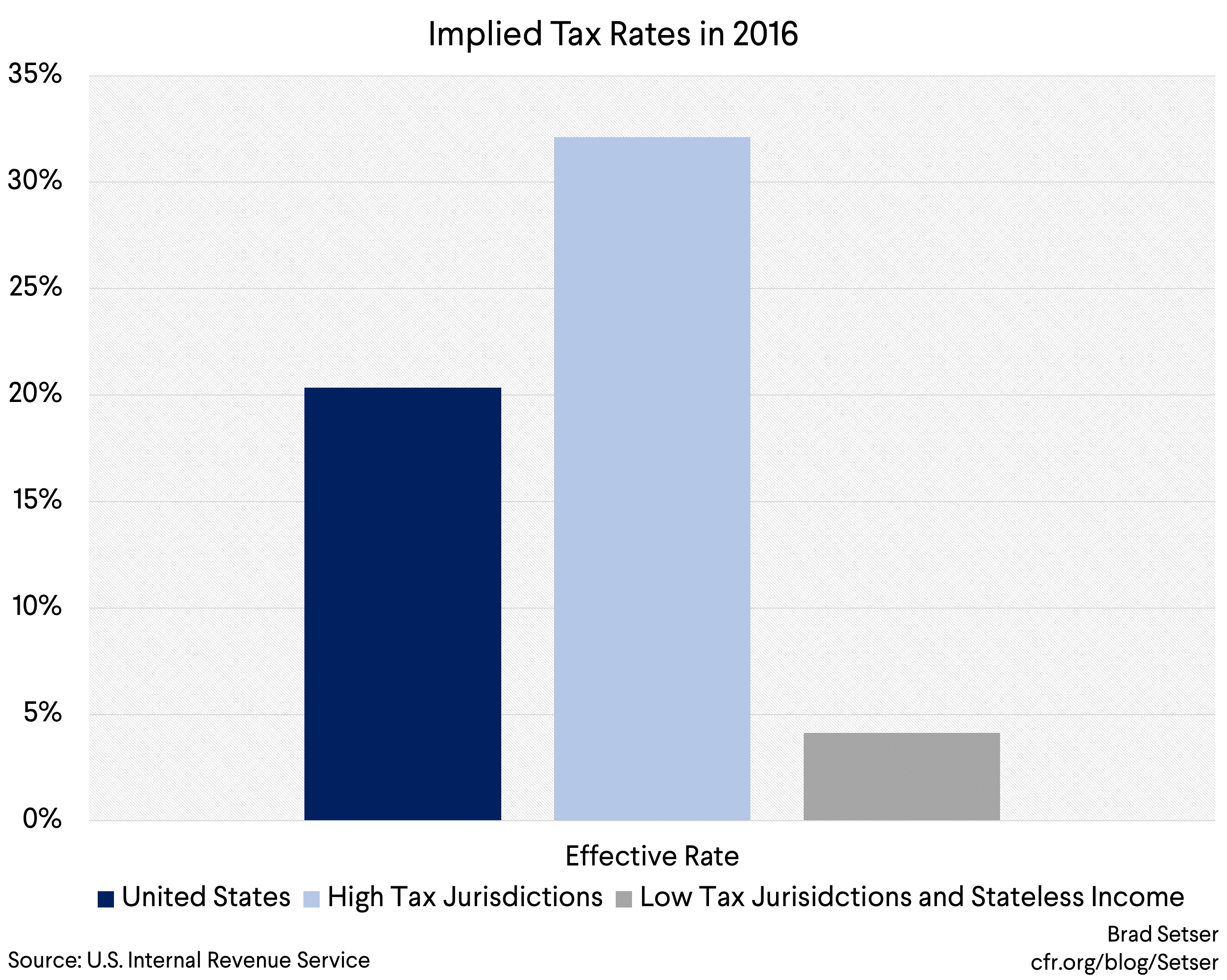

U.S. firms earned around $900 billion in the United States ($870b), and paid about 20 percent of that in federal income tax ($175 billion or so). Even before the tax reform, U.S. firms generally weren’t paying close to 35 percent of their profit in tax.

U.S. firms earned around $225 billion in a set of high tax jurisdictions around the world, and paid about $70 billion in tax—for an effective tax rate of over 30 percent. This includes the high taxes that firms producing in oil states often pay on their earnings, as they pay special income and production taxes and the like.

And U.S. firms earned $325 billion in the world’s low jurisdictions (I included the $39 billion U.S. firms earned in Puerto Rico here, as Puerto Rico functions as a low tax jurisdiction for the pharmaceuticals industry; I also added in the “stateless” income here). They paid less than $15 billion in tax abroad on those profits, for an effective tax rate of 4 percent or so. The residual U.S. tax they owed was deferred, so there was no cash payment in 2016 (the tax act settled that deferred liability on those profits with a one time 15.5 percent tax on offshore cash balances, net of any tax actually paid abroad).

Bottom line: U.S. corporate earnings in the main offshore centers, whether computed using the balance of payments (see my New York Times piece, which has some awesome graphs) or the IRS data, are now about 1.5 percent of U.S. GDP, or about $300 billion a year.

The new law taxes these profits at about 10.5 percent (the new global minimum tax rate on intangibles, or GILTI), or less if a firm has significant tangible assets abroad (the IRS data incidentally has numbers on tangible assets abroad).

The low 10.5 percent rate leaves a lot of revenue on the table. The United States should get most of the difference between the 4 percent pre-reform effective tax rate and the 10.5 percent rate (or it would if the minimum was enforced on a country by country basis).

But raising the tax rate on profits offshored to low tax jurisdictions could raise substantial additional revenues. If you assume that offshore profits in tax havens will grow at 5 percent over the next ten years, increasing the tax rate to the 15.5 percent tax rate used to settle firms deferred tax liability under the old law would be estimated to raise something like $200 billion over the standard ten year horizon used to evaluate the impact of tax changes on revenues. OK, a bit less because the GILTI is set to rise to 13.125 percent after 2026, so my estimate is an estimate against a current policy rather than a current law baseline.

Moving to a system of global taxation at a 21 percent rate assessed on a country by country basis (the details matter) might raise close to $300 billion over ten years. That simple calculation leaves out the impact of raising the GILTI rate to 13 percent, but it also leaves out the gains from moving to a higher tax rate on intangible exports—and thus removes another tax break built into the new law.

Third, there is actually a bit of concrete evidence that firms have been shifting more production offshore as a result of the new tax law, or at least playing transfer pricing games more aggressively to move profits offshore.

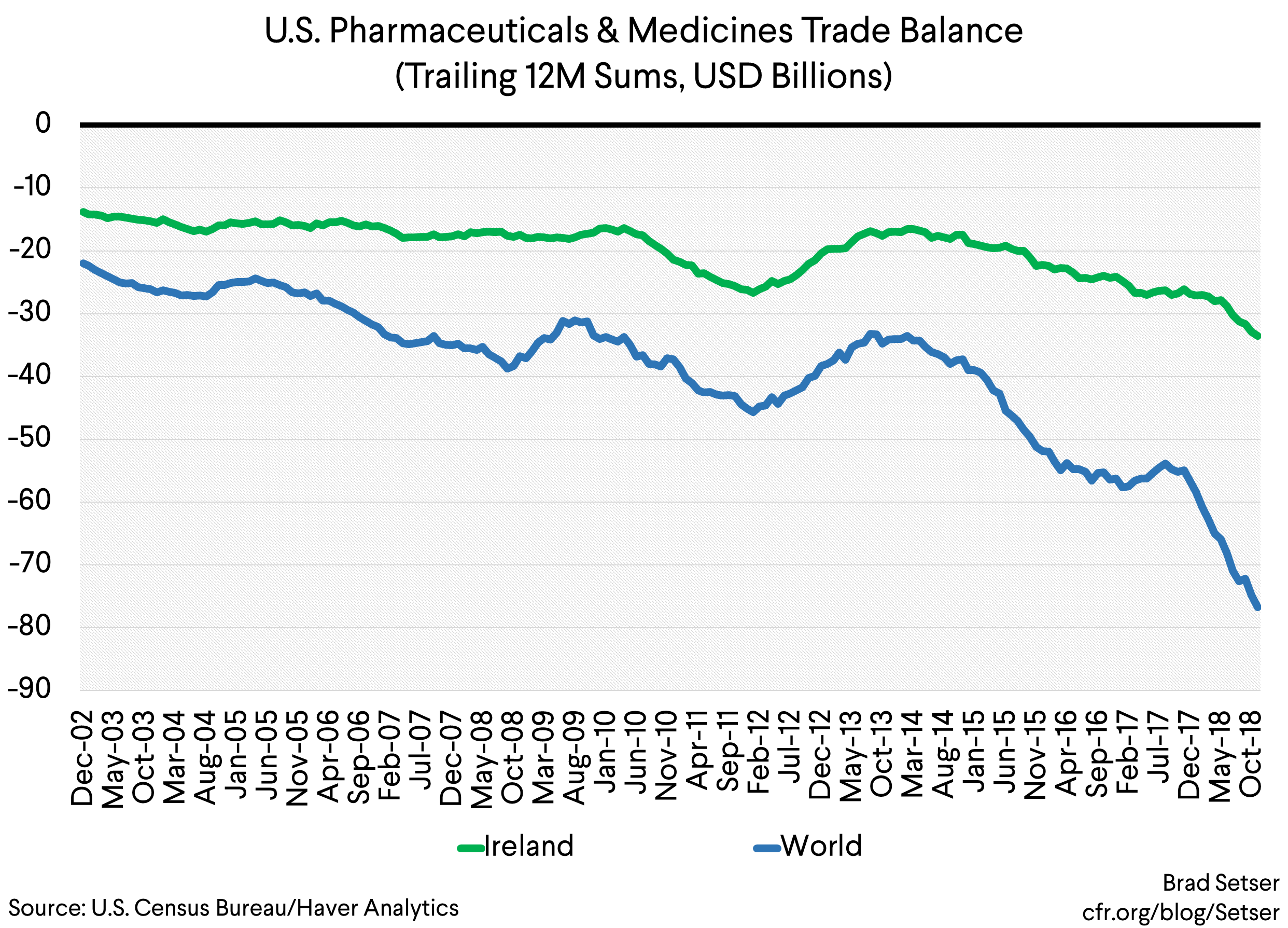

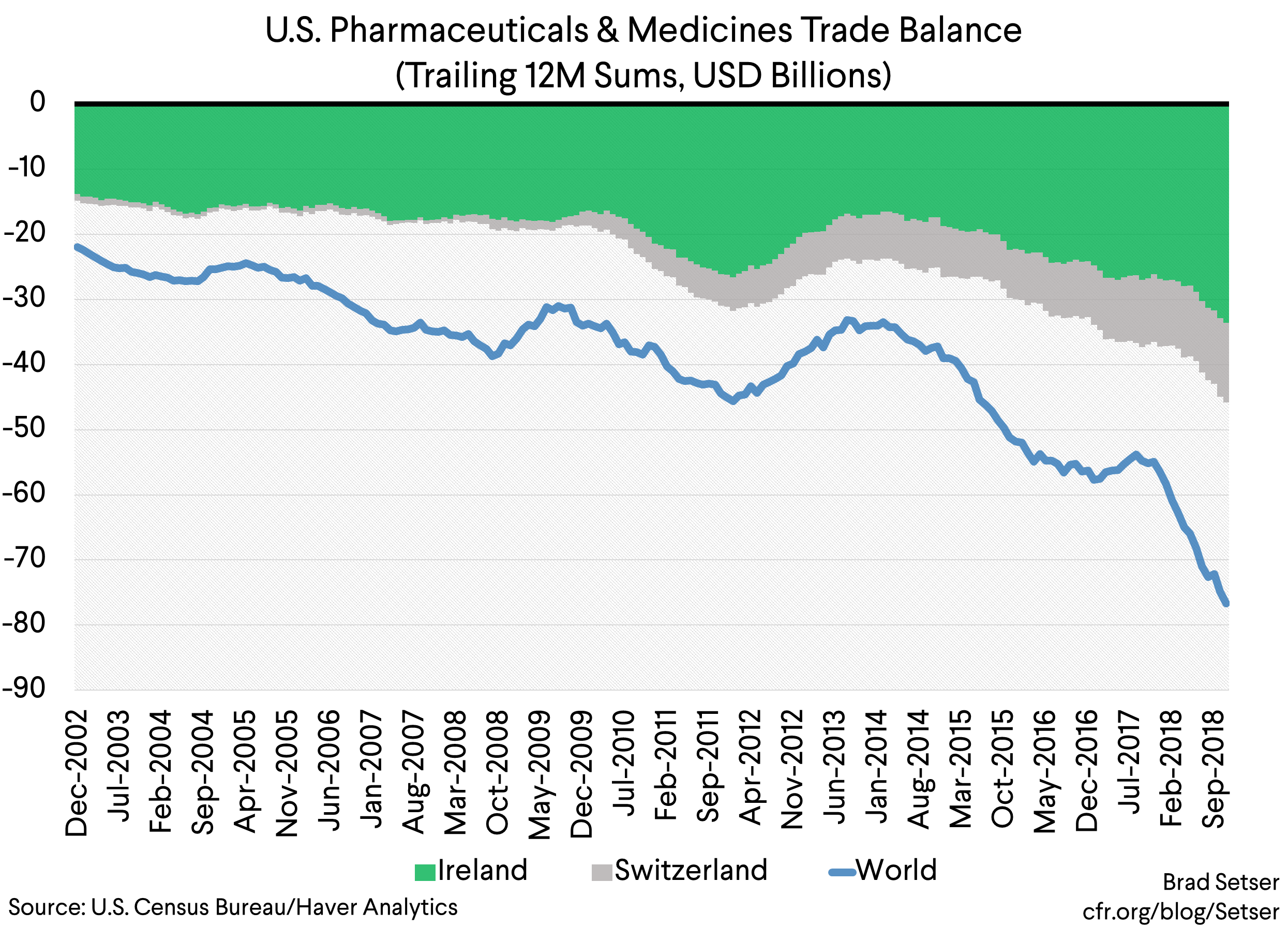

I have long suspected that tax has played a role in explaining the large (and rising) U.S. trade deficit in pharmaceutical products. And the trade deficit in pharmaceuticals looks to have jumped in 2018. Guess where the bulk of those new imports are coming from?

There could be an innocent explanation here. A big new patent protected drug came on market and it just so happens that the relevant firm had long-standing plans to produce that drug in Ireland.

But it certainly doesn’t seem—based on the trade data showing a $20 billion jump in the pharmaceutical trade deficit in the year after the tax reform—that incentives to produce certain drugs offshore so as to transfer the profit on those drugs to a low tax jurisdiction have gone away. And it’s at least possible that Rebecca Kysar’s prediction that the tax law would create incentives to shift tangible assets abroad—and to low tax jurisdictions—is already playing out. More tangible assets (factories) offshore means a lower calculated minimum tax on your offshore intangible income (the patents and the like on a new drug, for example).

One last point.

Profit shifting isn’t just a function of the U.S. tax law—it is a function of the U.S. tax law and how it interacts with global tax rules and the national tax systems of key corporate tax centers. Firms aren’t interested in shifting profits from the United States to Germany—and they wouldn’t be paying the GILTI (the global minimum) if they actually were paying Ireland’s headline 12.5 percent rate.

And, well, I am not sure that much progress is being made globally.

A few years ago Ireland promised to phase out the “double Irish”—a tax structure that involved passing profits between two Irish subsidiaries, only one of which was a tax resident of Ireland—by 2020.

So there was hope.

But, well, it seems like foreign multinationals operating in Ireland have found a new tool—the “green jersey” (which formally uses Ireland’s “Capital Allowances for Intangible Assets “ law). Apple seems to have pioneered this tax structure—as I understand it, Apple moved some of its assets to Jersey, then had its Irish subsidiary buy the rights from its Jersey subsidiary using funds that it nominally borrowed from its Jersey subsidiary. And then it could depreciate the purchase cost against the profits in its Irish subsidiary. It was no longer a tax resident of nowhere (Apple had a unique arrangement, as Ireland viewed Apple Ireland as a tax resident of the United States while the United States viewed it as a tax resident of Ireland and no one collected tax). It was a tax resident of Ireland, but one taxed at a low rate.

Other tech companies are apparently following suit. Ireland is happy too; Irish corporate tax revenues are actually booming (they get a bigger cut out of Apple and perhaps others).

“…the CAIA BEPS tool in particular, which post-TCJA, delivered a total effective tax rate (“ETR”) of 0–3% on profits that can be fully repatriated to the U.S. without incurring any additional U.S. taxation. In July 2018, one of Ireland’s leading tax economists forecasted a “boom” in the use of the Irish CAIA BEPS tool, as U.S. multinationals close existing Double Irish BEPS schemes before the 2020 deadline.”

So, best I can tell, neither the OECD’s base erosion and profit shifting work nor will the U.S. tax reform end the ability of major U.S. companies to reduce their overall tax burden by aggressively shifting profits offshore (and paying between 0-3 percent on their offshore profits and then being taxed at the GILTI 10.5 percent rate net of any taxes paid abroad and the deduction for tangible assets abroad).

The only good news, as I see it, is that the scale of profit shifting is now so big that it almost cannot be ignored—it is distorting the U.S. GDP numbers, not just the Irish numbers.* And in my view, the current tax reform’s failure to change the incentive to profit shift will eventually become so obvious that it will become clear that the reform itself needs to be reformed.

* Seamus Coffee has estimated that the depreciation of intangible assets added an insane Euro 40 billion to Ireland’s gross national income in 2018: “Projections from the Department of Finance indicate that this will be more than €40 billion in 2018.” Ireland’s (inflated) GDP is just over 300 billion Euros.