Turkey Could Use a Few More Reserves, and a Somewhat Less Creative Banking System

Turkey’s currency initially rallied after the central bank raised interest rates yesterday. Perhaps a bit more orthodoxy is all it will take to restore a modicum of stability to Turkey’s markets. Then again, the lira’s rally didn’t last long.

Even if Turkey firmly commits to a somewhat more orthodox monetary policy, Turkey retains substantial vulnerabilities:

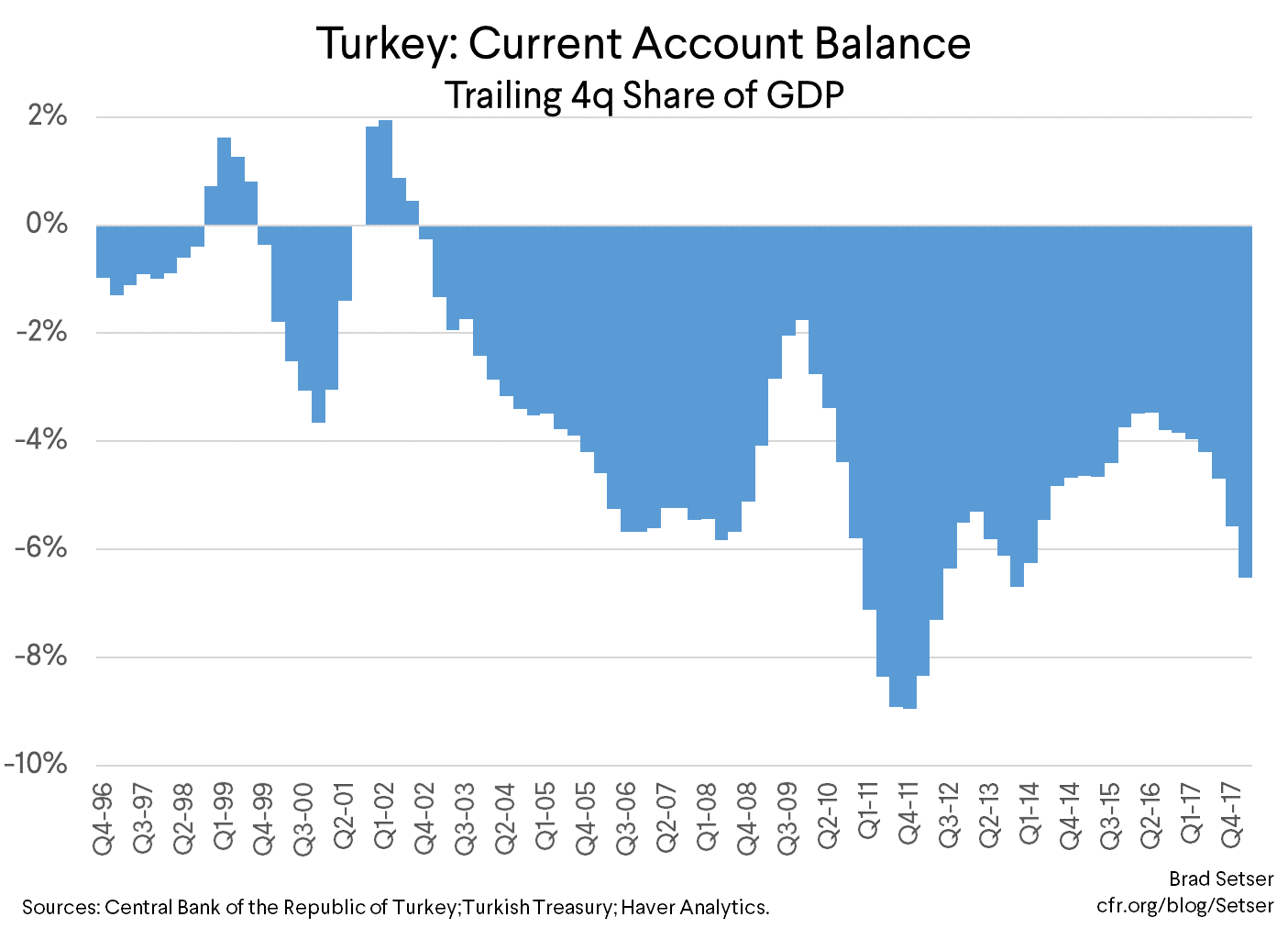

- Turkey’s current account deficit was quite large even before oil rose to $80, and Turkey imports a ton of oil (and natural gas).

- Turkey has a dollarized financial system and trades heavily with Europe. It thus doesn’t benefit much from the rise in imports that Trump’s fiscal stimulus has generated, but gets hurt by higher interest rates on its dollar borrowing.

- Turkey has a decent stock of external debt, and much of that is denominated in foreign currency.

- Turkey’s banks lend domestic dollar deposits to Turkey’s firms, who have more foreign currency debt than they have external debt.

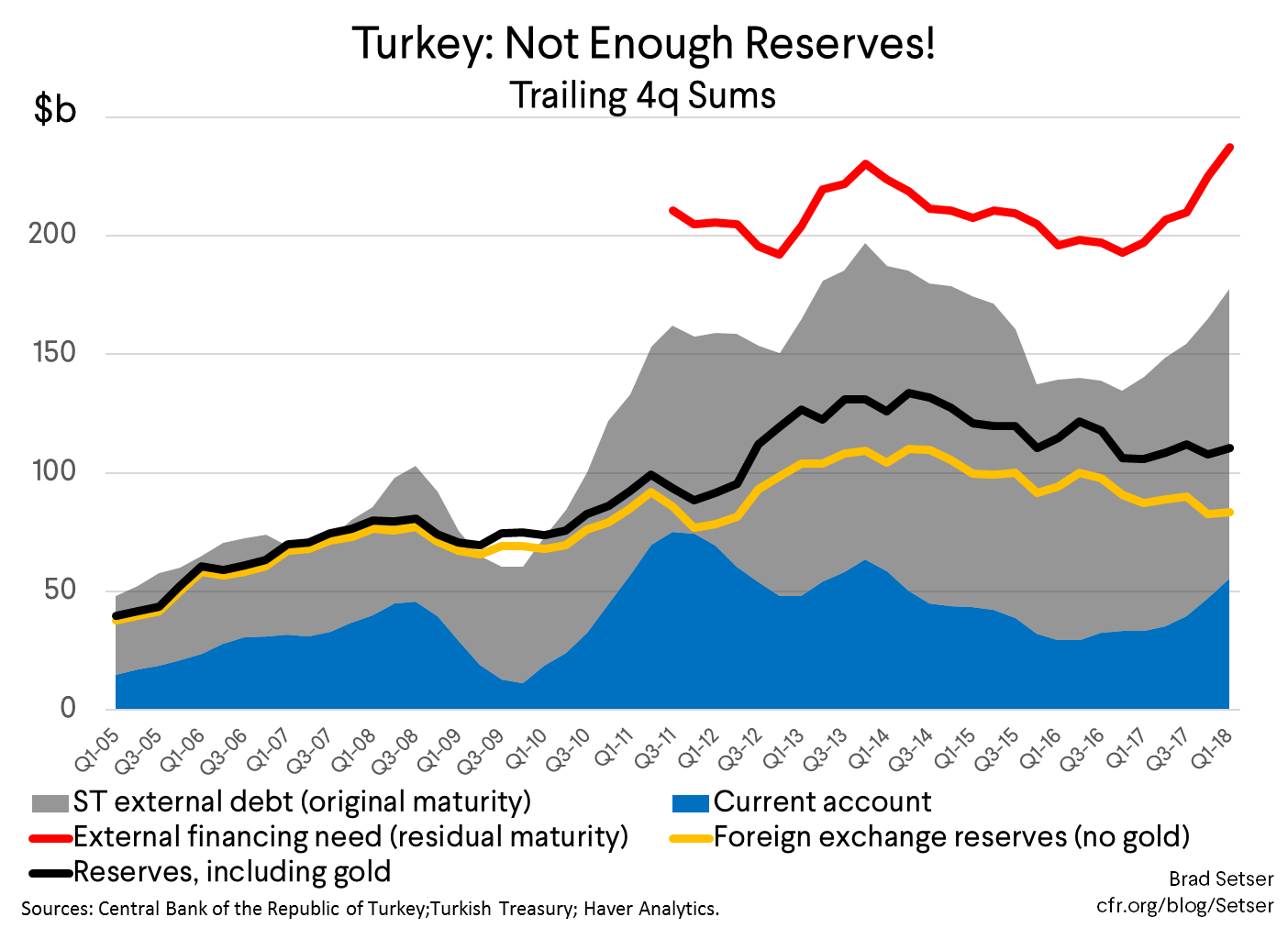

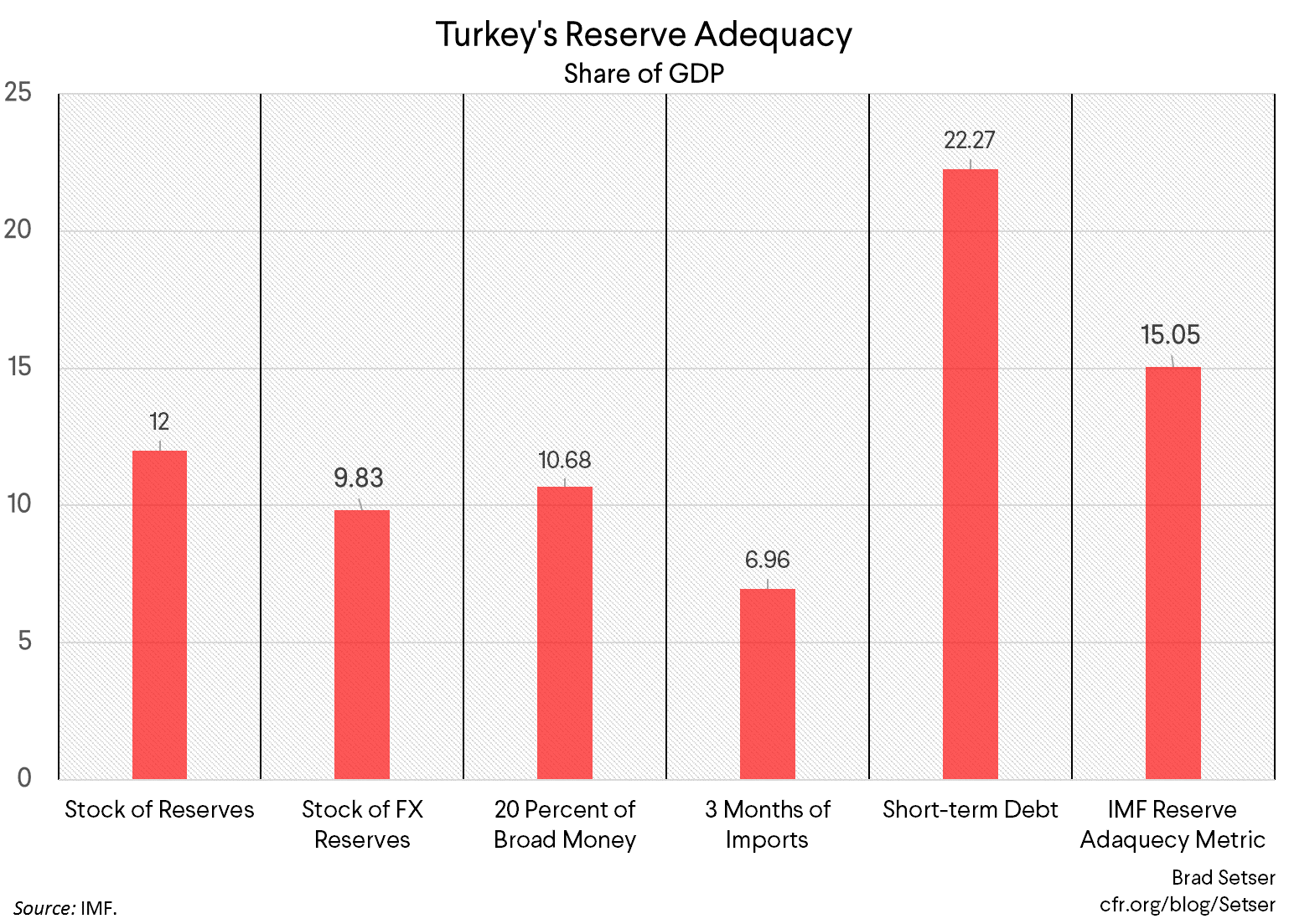

And, Turkey could use a few more reserves. Turkey’s reserves fall far short of covering its external financing need over the next year.

There are three important things to know about Turkey’s foreign exchange reserves.

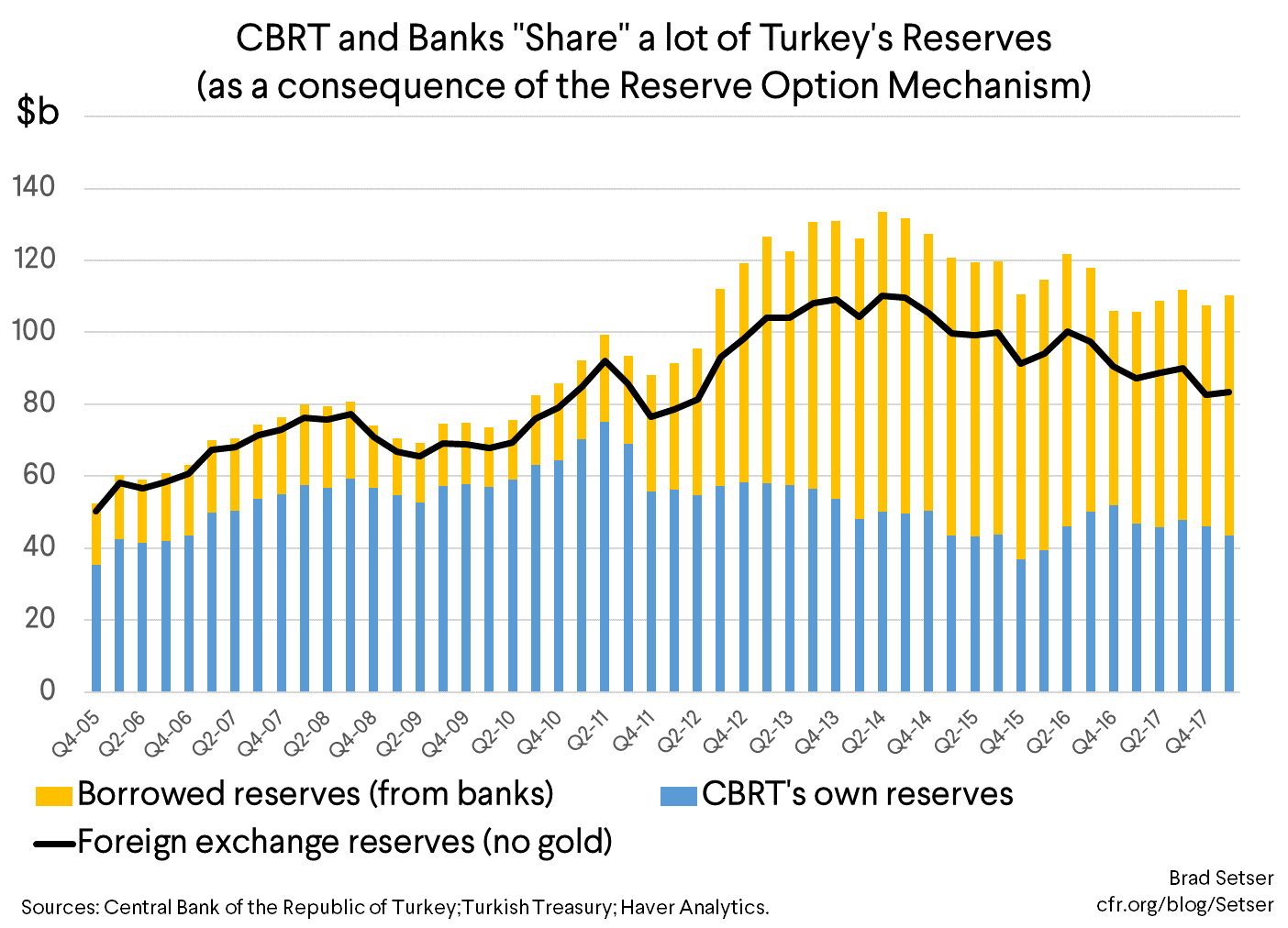

- A lot of Turkey’s reserves are in gold and thus not in dollars or euro. Turkey’s debts though don’t settle in gold.

- A lot of Turkey’s reserves are borrowed from the domestic banks, who can meet their reserve requirement on lira deposits by posting either gold or foreign exchange to the central bank. Most of the gold, and a decent chunk of the foreign exchange, is effectively borrowed. That limits the pool of funds available to intervene directly in the foreign exchange market (though it also provides the banks with a bit of a buffer).

- Turkey’s reserves don’t come close to covering its maturing external debt, let alone its external financing need, no matter how you cut it.

Turkey has about $180 billion in external debt coming due (around $100b from the banks, $65b from firms).* It has a $50 billion (give or take) current account deficit.

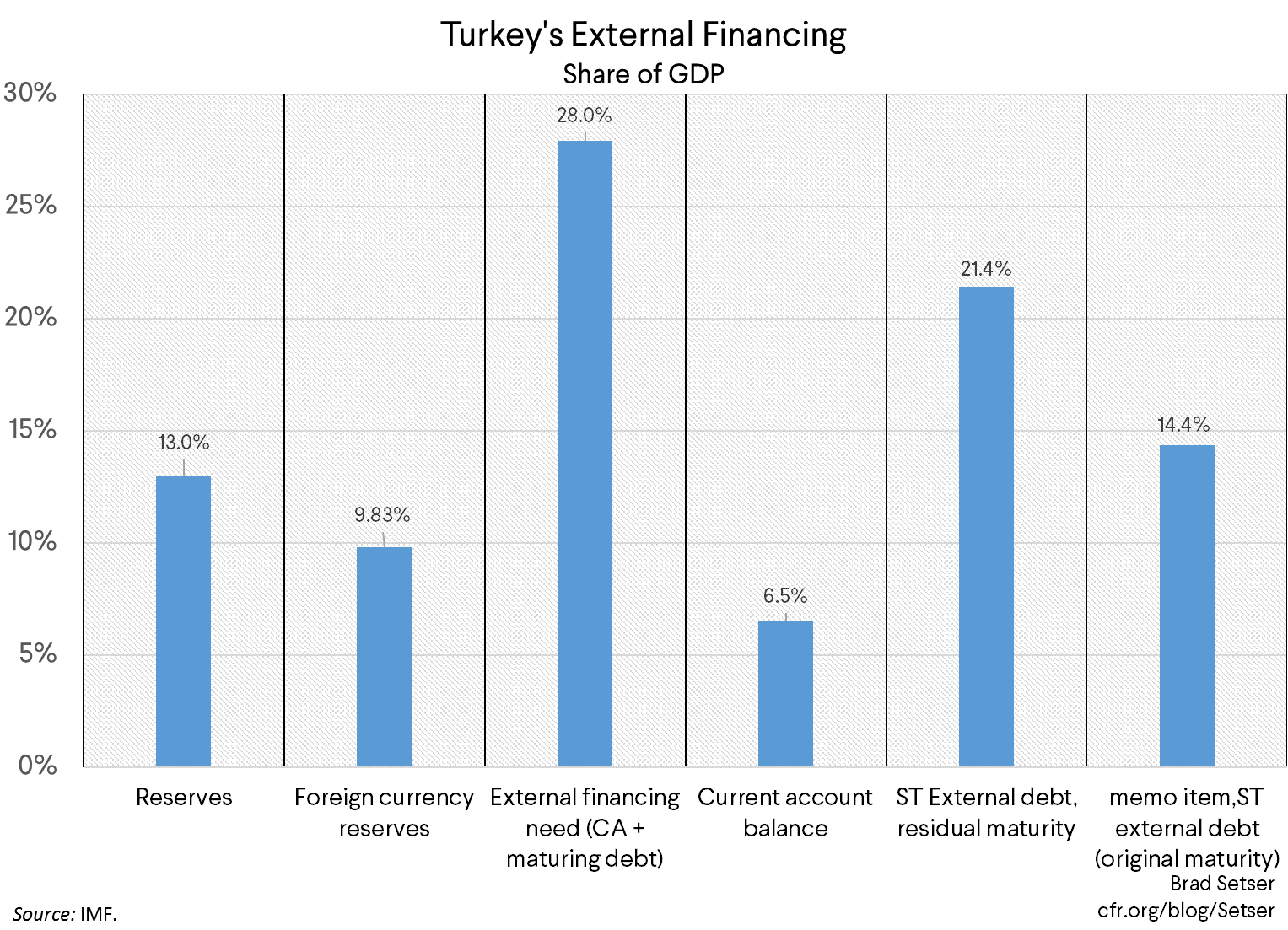

That’s a one-year external financing need of close to 30 percent of Turkey’s pre-depreciation GDP, against 12 percent in total reserves and about 10 percent of GDP in foreign exchange reserves. And the bulk of Turkey’s maturing external debt is denominated in a foreign currency—it thus is a claim on reserves that cannot be depreciated away.

On classic measures of external vulnerability, Turkey—like Argentina–– is much more under-reserved than the IMF’s reserve metric would suggest (M2 and exports aren’t large versus GDP, so they pull the reserves Turkey’s needs to meet the IMF’s standard well below maturing short-run debt). And even if it is graded on the IMF’s generous curve, Turkey falls short (See paragraph 19 of the IMF’s latest staff report).

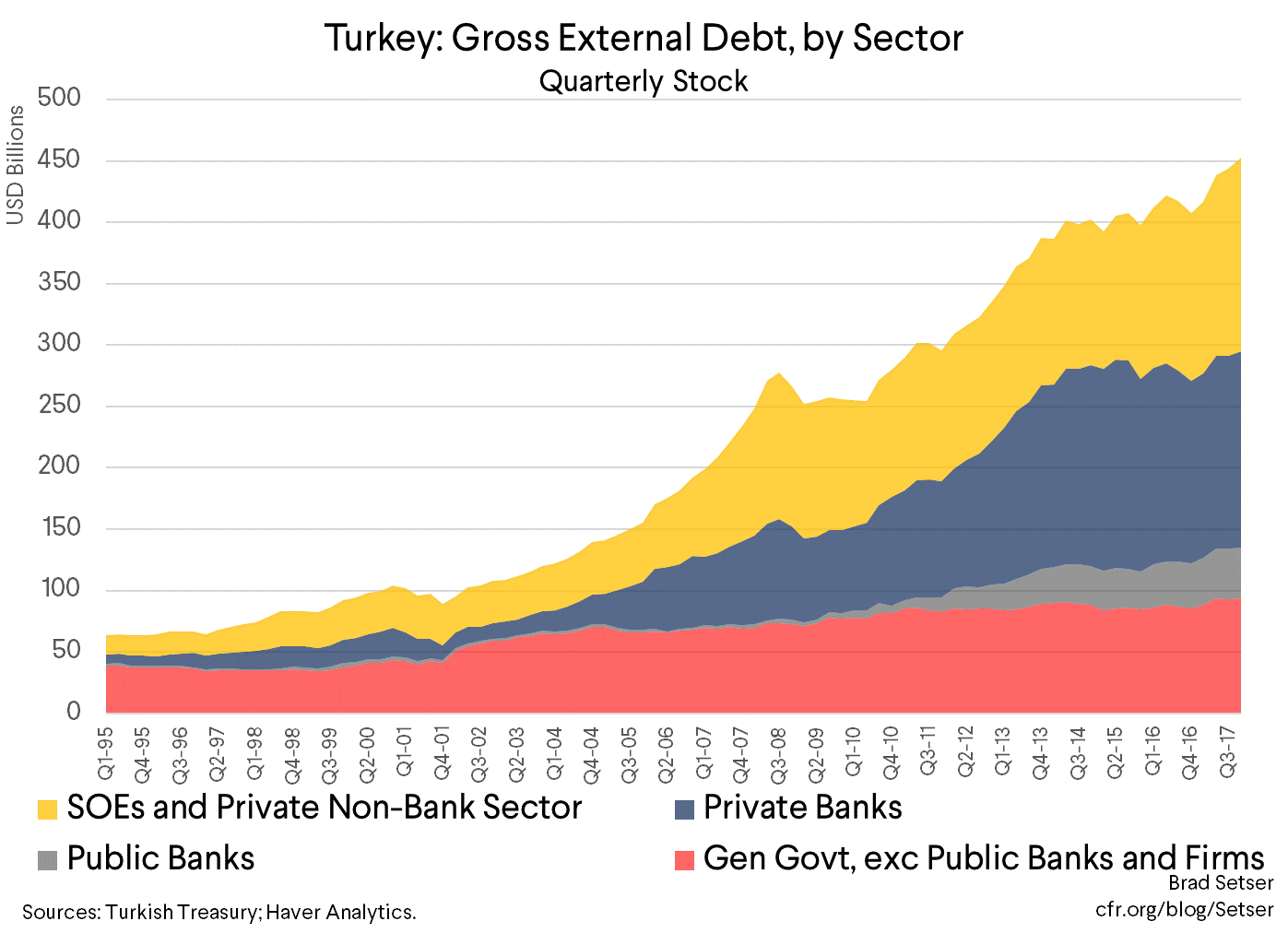

These vulnerabilities aren’t new. Turkey has long looked vulnerable to an Asian style financial crisis—one triggered by a loss of access to bank funding and a bank-corporate doom loop from the private sector’s foreign currency debts. And it has some of Argentina’s old vulnerabilities too, with roughly $200 billion in domestic foreign currency deposits (data from Turkish Central bank)) in addition to $400 billion plus in external debt (see this classic book on emerging market crises for background on the Asian and Argentine crises).

These long-standing vulnerabilities haven’t triggered a full-on crisis yet. Turkey’s domestic deposit base and its external funding has historically been fairly sticky. It has been surprisingly resilient in the past.

Yet there are reasons to think Turkey faces a more difficult challenge now. U.S. rates are rising when oil is going up, and that’s a bad combination for an oil importer with lots of dollar debt. While Turkey has long looked bad on classic indicators of external vulnerability, it now is starting to look really bad—short-term debt has jumped a bit relative to GDP (thanks mostly to a surge in corporate borrowing, which shows up in the “trade credit” line) and the external funding need is now close to three times liquid (non-gold) foreign exchange reserves.

Turkey though differs from Argentina in one critical respect. Its government hasn’t been the biggest external borrower, and it doesn’t have the biggest stock of foreign currency debt in the economy.

That honor goes to Turkey’s firms, who have almost $340 billion in foreign currency denominated debt ($185 billion is owed to domestic creditors, and $150 to external creditors—$110 in loans and $40 in trade credit [source]). The quality of their hedges will be tested: I never have been convinced all foreign currency debt is really backed by export receipts.

What really makes Turkey interesting, though, is its banks. They have a rather fascinating balance sheet and engage in some fairly creative forms of financial intermediation, with a bit of regulatory help.

The core problem Turkey’s banks face is simple.

Turks want to hold a large chunk of their savings in dollars. And foreigners want to lend to Turkey in dollars (or euros).

But Turkish households want to borrow in lira (in fact the banks cannot lend to households in foreign currency—a sensible prudential regulation). So the Turkish banking system has a surplus of foreign currency funding—and a shortfall in lira funding.

There is an easy way to see this. Look at the loan to deposit ratio in foreign currency. It’s clearly below 1, about 0.8. And then look at loan to deposit ratio in lira. It is well above 1—it is now about 1.4. (See the IMF’s 2016 staff report [Paragraph 46], or the most recent financial stability report of the Central Bank of Turkey, starting on p. 50. Chart III.2.4 on p. 51 has the loan to deposit ratio by currency).**

So how do the banks transform dollars into lira?

A couple of tricks:

- They swap a lot of dollars into lira. Fair enough. But the tenor of the swaps is fairly short (see box III.2.1 of the central bank’s financial stability report . The “lira” can run even if the dollars raised by selling longer-dated bonds cannot.)

- And the central bank lets the banks meet their reserve requirement in lira by posting foreign exchange or gold at the central bank (so gold deposits in effect fund lira lending, indirectly). This means the banks have a decent buffer of foreign exchange—which they can draw on if their creditors start to withdraw funding. One secret source of strength of the system is that the banks themselves have a fairly large stockpile of foreign exchange deposits that matches their large short-term external debts.***

Makes for a strange system. So long as the domestic hard currency deposits don’t run, the banks ultimate funding need is in lira.

In addition to transforming foreign exchange funding into lira lending, the banks do a lot of classic intermediation—borrowing short-term (there aren’t lots of sources of long-term lira funding) to fund lira denominated installment loans and mortgages. The banks consequently are exposed to an interest rate shock—in much the same way the U.S. savings and loans were back in the 1970s (they funded long-term mortgages with short-term deposits).

This has a plus—raising domestic interest rates sharply would quickly slow bank lending and reduce demand, helping to close the current account deficit.

But it also encourages a lot of creativity on the part of the central bank, which knows—I think—that the banks ultimately rely on it for lira funding and are vulnerable to an interest rate shock. And historically at least, the regulators have often preferred to use macroprudential limits to cool the economy rather than rate hikes, though it isn’t clear if that would be enough right now.

Bottom line: Turkey cannot really use its reserves to try to defend the lira. Selling off some of its already limited reserves to cover an ongoing current account deficit would create the perfect conditions for a run on the banks’ foreign currency liquidity to develop. A free fall in the lira would cause corporate distress, even if it would take a lot to really threaten the government’s solvency. And raising rates sharply would squeeze the banks ability to lend—slowing the economy, but helping to close the current account deficit. Pick your poison.

* Thanks to $120 billion or so in short-term external debt and the scheduled roll off of a fraction of its long-term claims.

** The CBRT (emphasis added): “Depositors’ FX deposit preferences and the change in favor of the TL in the loan composition of banks led to a widening in the gap between the TL and FX L/D ratios. The difference between TL and FX L/D ratios indicates that banks need TL liquidity. As a result of depositors’ FX deposit preferences and banks’ TL liquidity needs increased FX swap transactions with foreign residents. Therefore, the amount, maturity, cost and counterparty structure of FX swap transactions have recently become important with respect to monitoring the liquidity risk of banks.”

*** It helps that domestic depositors tend to switch out of lira and into domestic foreign currency deposits in periods of stress. The banks can absorb a loss of external funding for a while (they likely have something like $50 billion in liquid assets at the central bank, and presumably could borrow against their gold too) but not a simultaneous loss of external funding and a run on their domestic dollar deposits.