Ireland Really Shouldn’t be Driving the Details of the Euro Area’s GDP Data

The euro area GDP data—thanks to Ireland—is increasingly telling us more about the tax strategies of large U.S. firms and less about the actual composition of activity in the euro area. Large investments in acquisition of their own intellectual property by U.S. firms transforming themselves into tax residents of Ireland ahead of the end of the double Irish are impacting the economic data of the entire currency union.

I admire the Irish statistics office.

Bermuda doesn’t try to report on the activities of all the tax residents of Bermuda. Nor does the Caymans. Or Jersey. Or Guernsey. Or the Isle of Man. Or any of the other islands that are big centers of…umm…corporate tax avoidance.

But Ireland isn’t just a corporate tax haven. While the “Irish” value added of (largely American) multinational tax residents of Ireland reached EUR 125 billion in 2018 (see table 2)—a rather amazing sum when you think about it, as Ireland used to be a EUR 200 billion economy— Ireland also has a real economy. And its statistics office tries to follow international and European conventions.

The net result is that Ireland’s GDP data now tells us something important—even if it isn’t an especially pleasant reality—about today’s global economy. The details of the Irish GDP release now serve as a real time road map to the tax strategies of big U.S. multinationals. I am sure European companies also seek to reduce their corporate tax burden, but perhaps they aren’t quite as obvious about it. The net result spills over into the overall euro area GDP data in some fairly obvious ways.

Let me step back a bit.

Back in the good old days, there was a common tax avoidance technique called the double Irish. The key was to create two Irish companies—one that was a tax resident of Ireland (and paid Ireland’s 12.5 percent corporate tax rate) and one that was legally an Irish company but from the point of view of the Irish tax authorities not an Irish company. Google’s second leg was a tax resident of Bermuda. Facebook’s second leg was a tax resident of the Caymans. Apple refined this strategy to perfection—its old Irish operating company was a tax resident of the United States from the point of view of Irish tax authorities and a tax resident of the Ireland from the point of view of U.S. tax authorities and as a result it was literally a tax resident of nowhere (see the Senate investigative committee report from way back when). Under the U.S. tax law at the time, could defer paying U.S. tax on their offshore profits indefinitely —though they in theory owed the U.S. government the full U.S. corporate tax if they ever repatriated their funds.

The double Irish was a bit too good to last—so as part of the Base Erosion and Profit Sharing (BEPS) process, the Irish committed to phase out all double Irish tax structures by 2020…all Irish companies had to be tax residents of Ireland.

But the Celtic tiger didn’t completely shed its stripes.

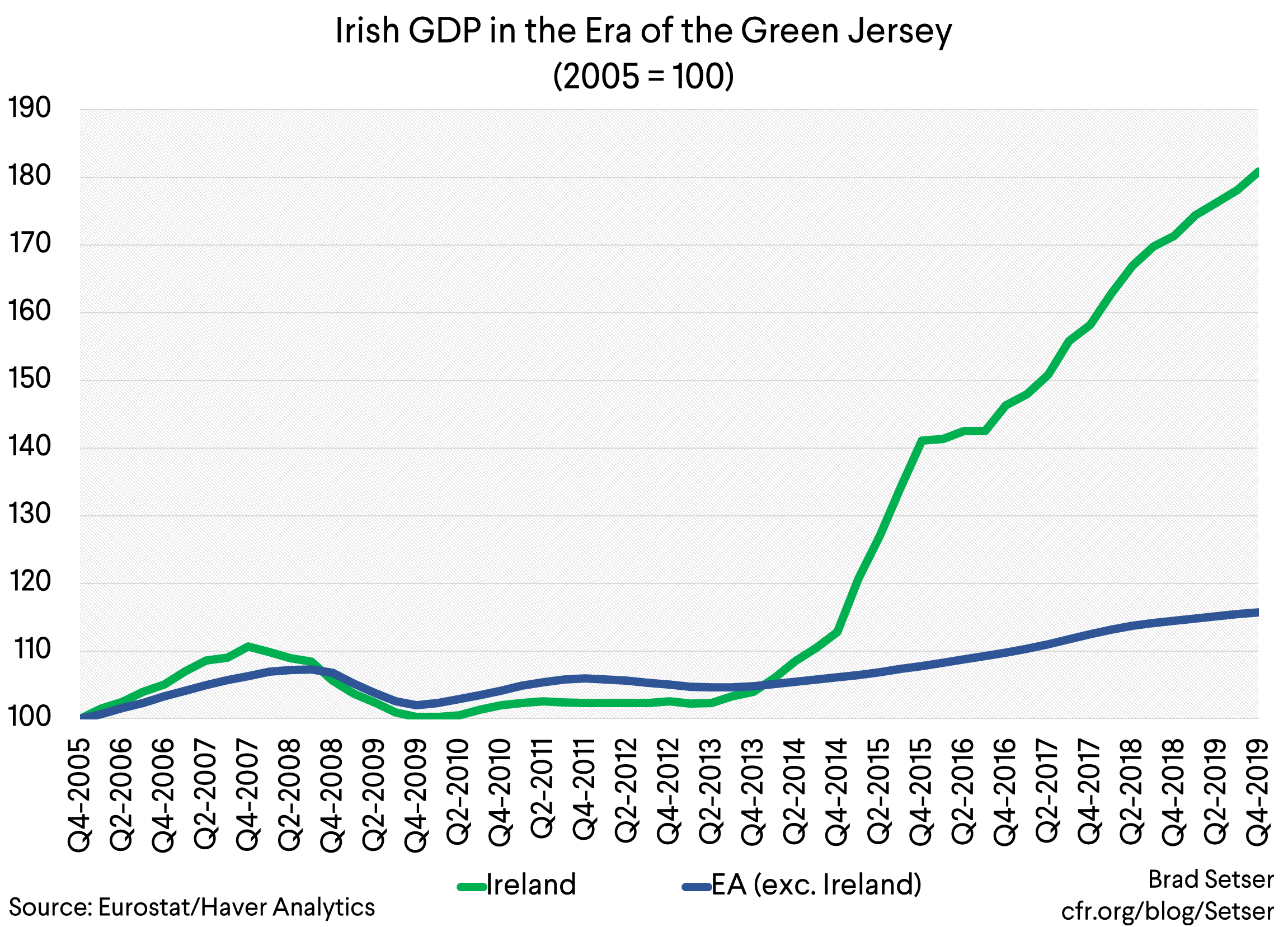

The Irish tax authorities allowed companies to put on what tax justice advocates called a Green Jersey, after Apple’s new tax strategy.

To over-simplify a bit, an Irish tax resident could buy the offshore (from Ireland’s point of view) assets of another subsidiary of their company, and then deduct the (high) purchase price over the next 15 years from their Irish tax bill. And to top it off, this transaction notionally could be financed by a loan taken out by the Irish subsidiary, with the interest paid (notionally) to the offshore subsidiary further reducing the companies Irish tax bill. There is a brilliant Wikipedian who has documented this all…I am in his or her debt.

Apple did this first—

The result though is clear—all of a sudden, a set of companies that previously have (mostly) been tax residents of nowhere (at least nowhere with a competent statistical authority—the Caymans, Bermuda, Jersey, and Guernsey don’t qualify) suddenly became tax residents of Ireland.

And it started entering into the Irish GDP.

Paul Krugman called it Leprechaun economics, a provocative term, but one that I think helped catalyze a broader shift in how the Irish economy was understood.

All of a sudden the Irish GDP data became a synthesis of two different things—the traditional Irish economy (farming and the like), and the modern “Irish” economy (the Dublin financial center, the tech companies tax divisions, pharmaceutical production to register profits made on U.S. sales in Ireland. and a few other things).

Now the Irish are actually quite aware of this. The “two Irelands” are very visible to the Irish.

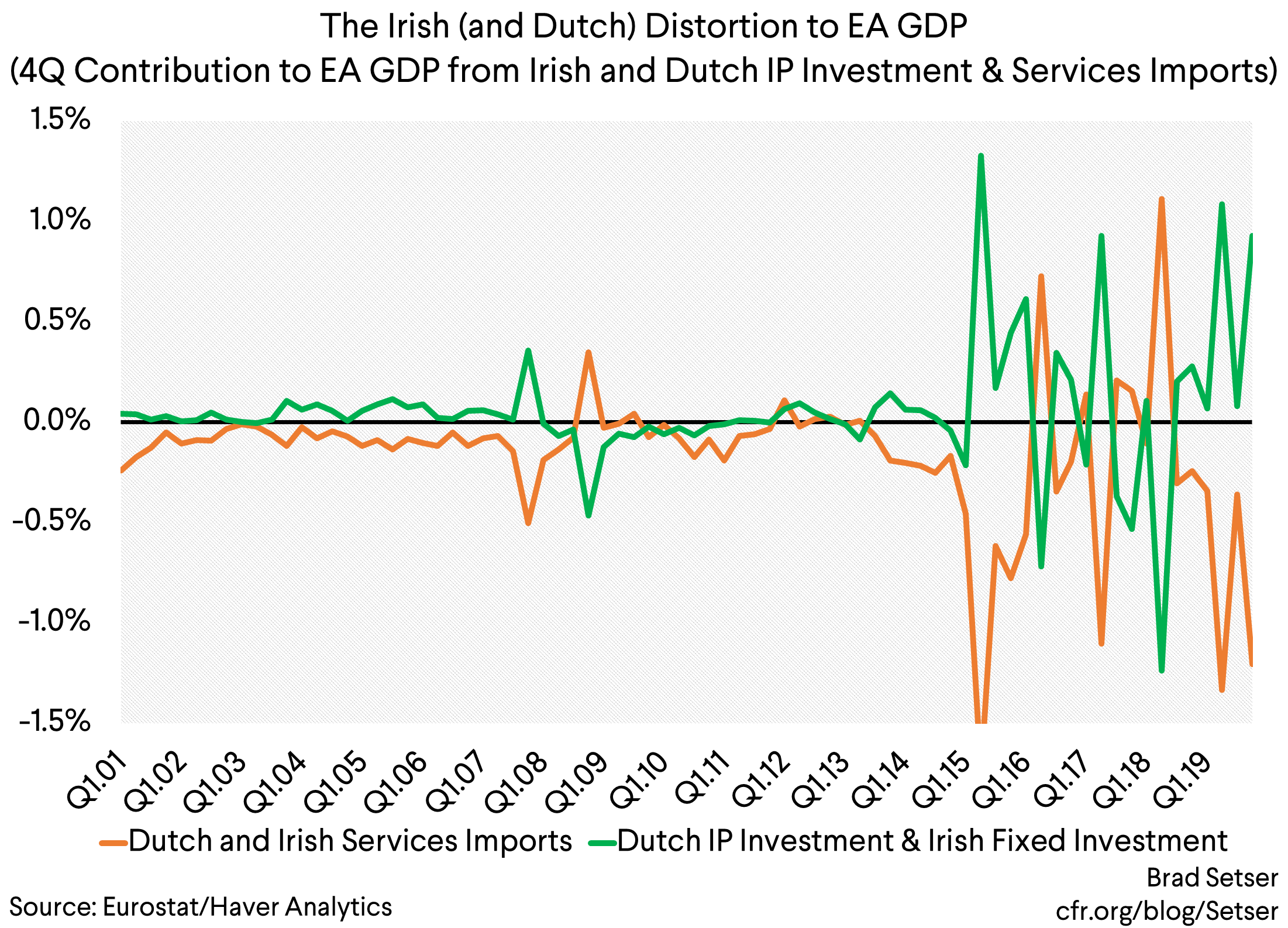

And, well, the distortions have gotten so big that they basically are shaping the euro area’s overall GDP data, so statistical grunts all over Europe now have to struggle with them too.

That very much includes the ECB’s chief economist, Philip Lane, who gave a remarkable speech on this topic two weeks ago. There isn’t any aspect of the euro area’s external data that isn’t shaped by these distortions. The ECB’s research division has done a nice paper on this too.

Let me give a few examples.

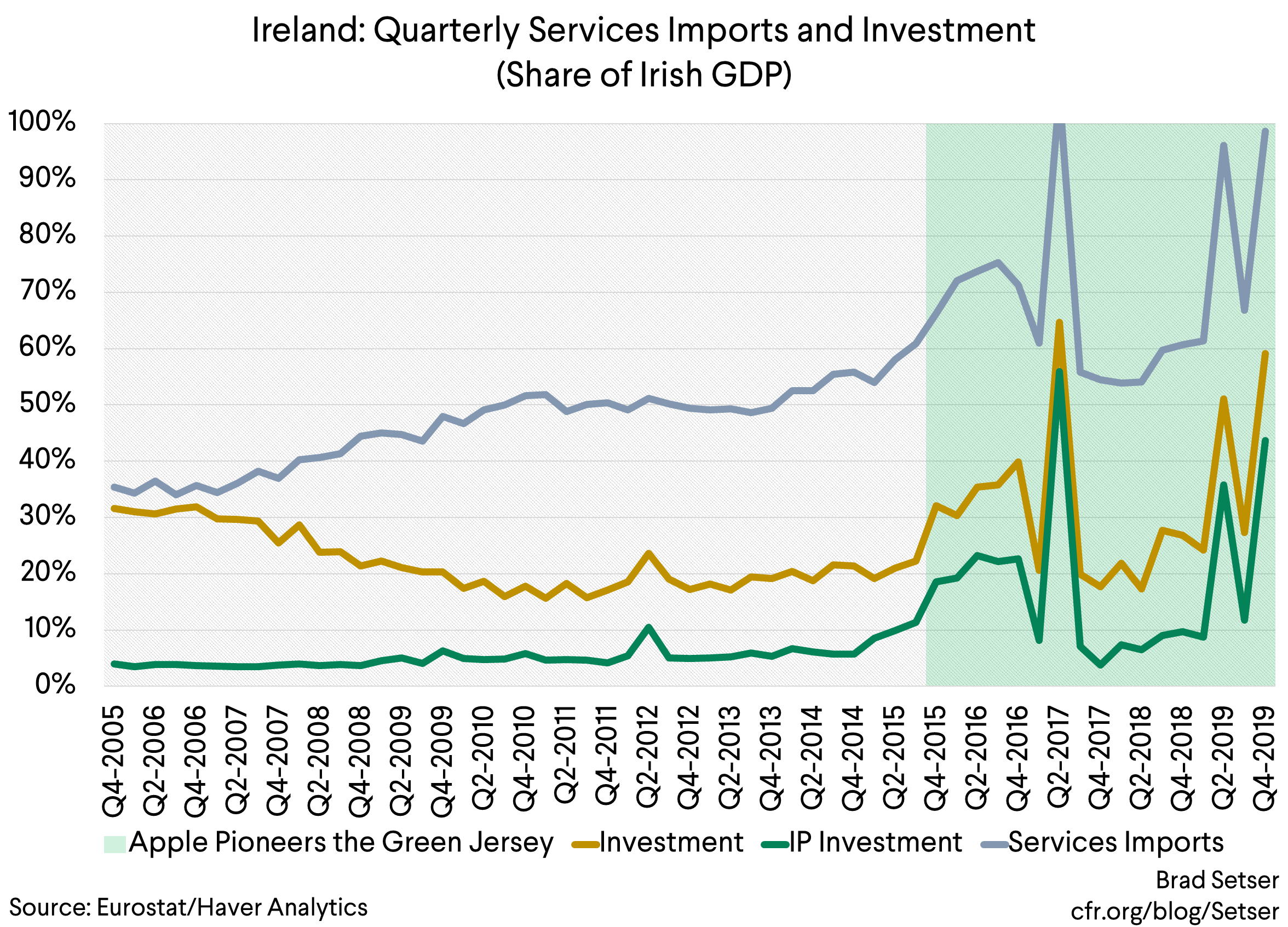

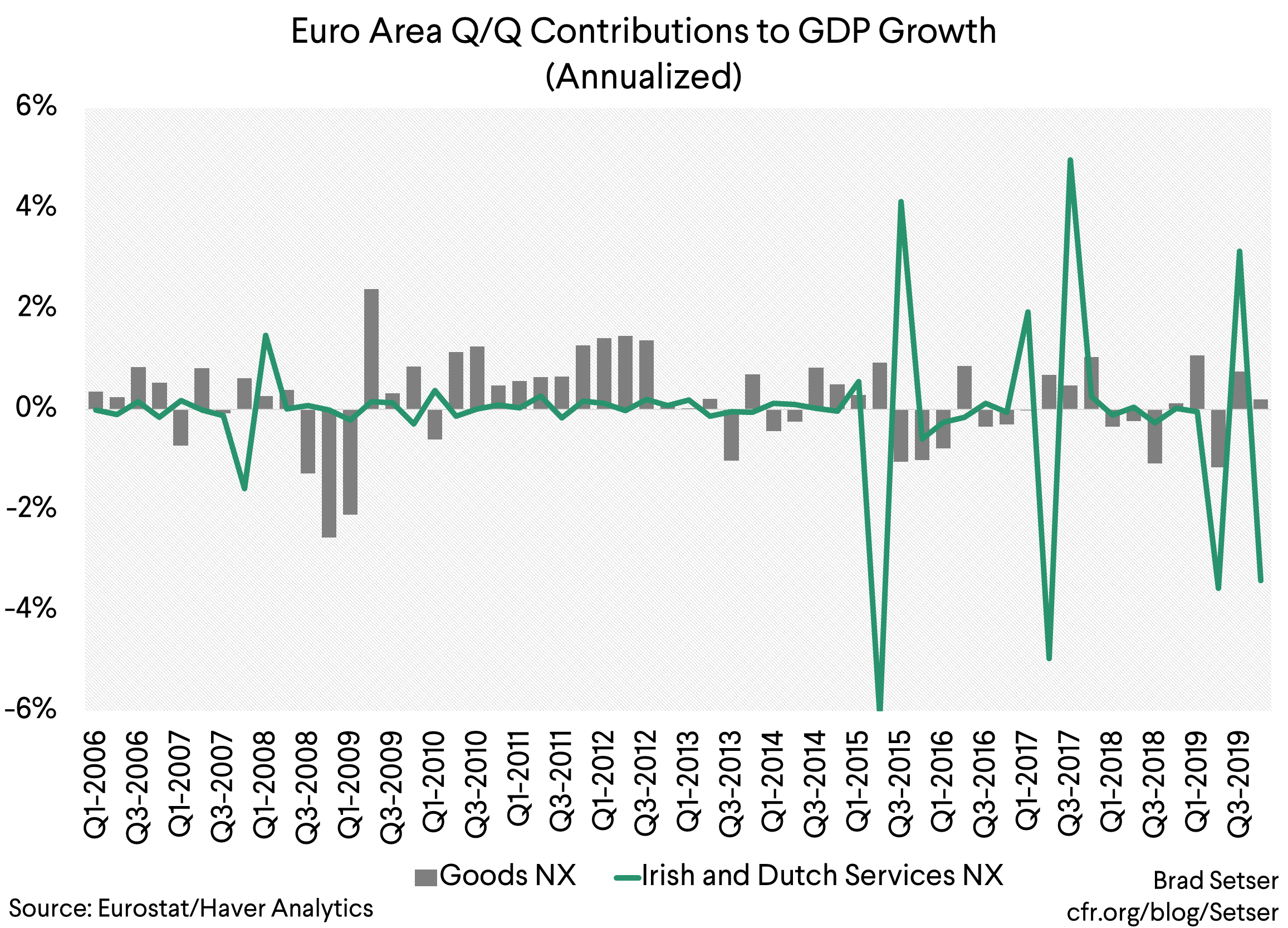

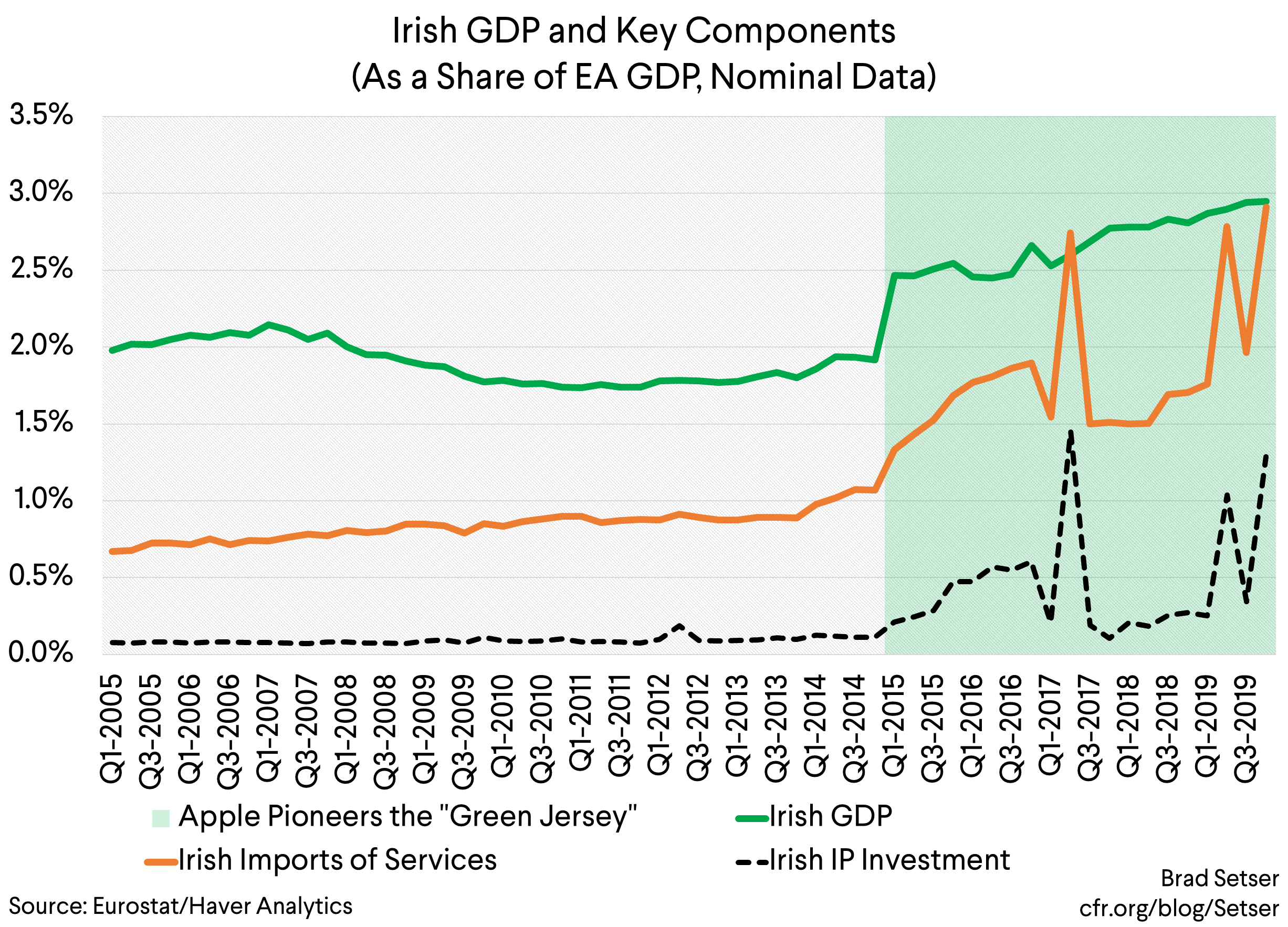

Ireland reported a 30 percent of GDP current account current account deficit in 2019. That is close to a percentage point of total euro area GDP, from an economy that accounts for roughly 3 percent of total euro area output.

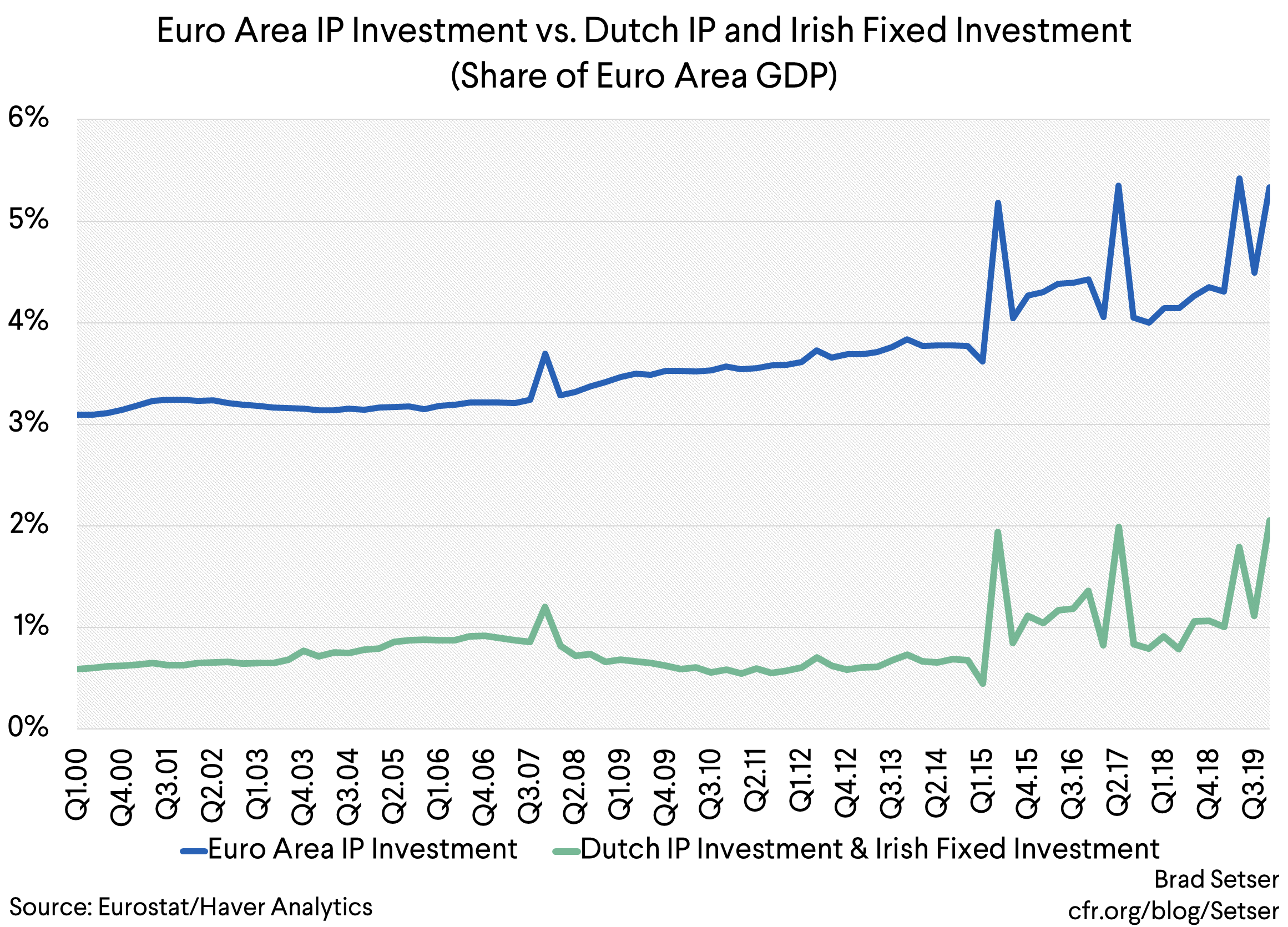

Ireland’s services imports in the fourth quarter jumped to almost 100 percent of Irish GDP, with Irish investment jumping by a similar amount. Of course, these numbers do not make sense. But I equally didn’t make them up.

That means—on a q4/q4 basis the increase in Irish services imports deducted over a percentage point from euro area GDP from the euro area’s trade numbers (there was an offsetting boost to domestic demand from investment).

Basically, the recent volatility in the euro area’s current account can almost all be attributed to the tax transactions of a few large U.S. multinationals—the process of becoming Irish generally means importing a lot of intellectual property rights from the firm’s subsidiaries in other tax havens.

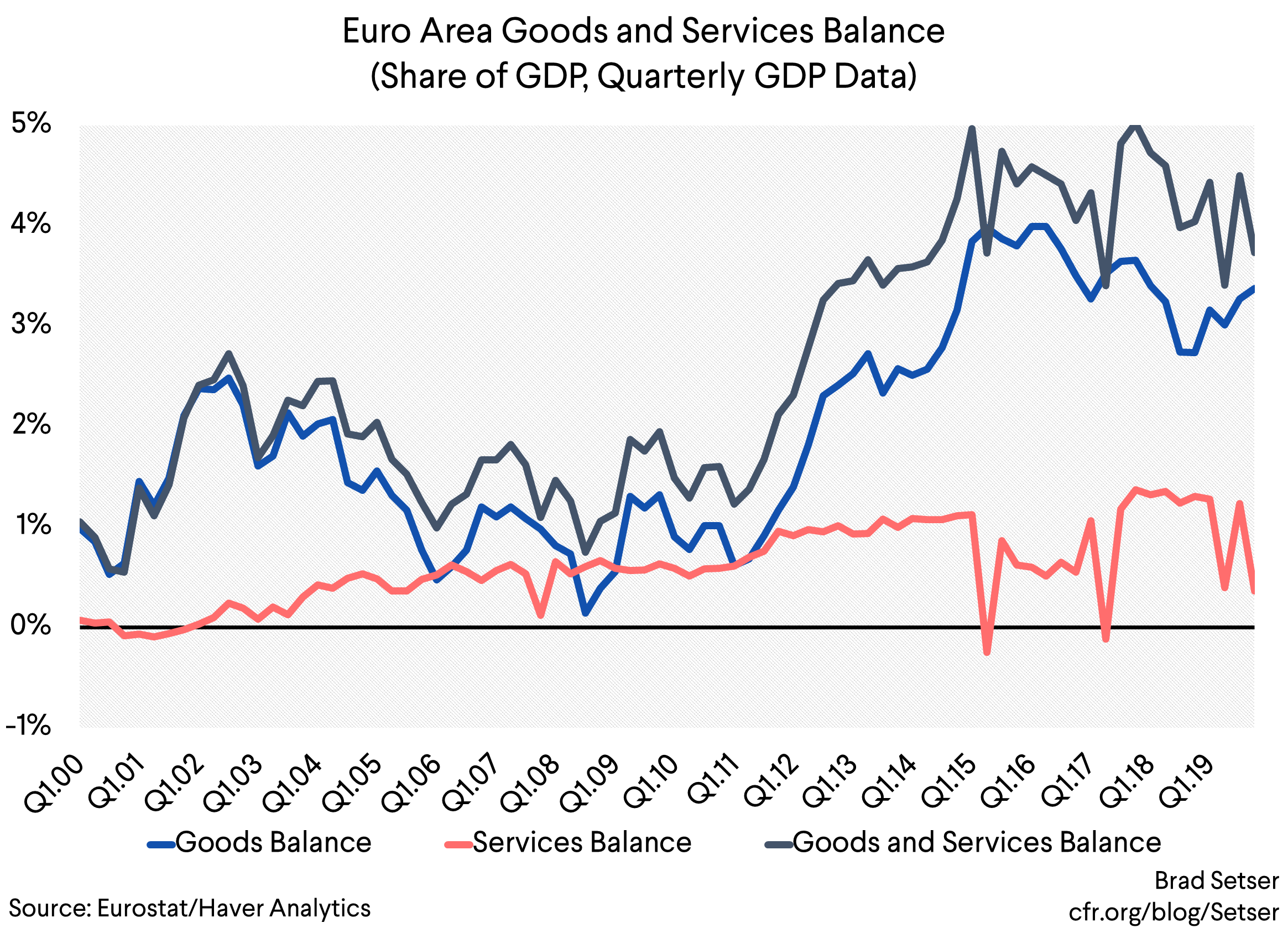

I know this goes against the current conventional wisdom that looking at goods trade alone is misleading, but including services trade actually mucks up the euro area data in a big way right now. Especially the quarter over quarter data (the chart is presented using the U.S. convention of annualizing the q/q data to drive home the point).

Now Ireland’s real economy is doing fine,

But Ireland isn’t really running a thirty percent of GDP current account deficit and pulling in huge sums from the rest of the world. The needed influx of financing here is coming from U.S. and other multinational companies that are borrowing from themselves to buy their own intellectual property. And since the goal here is to generate a large depreciation allowance, they have an incentive to actually pay a fair price.

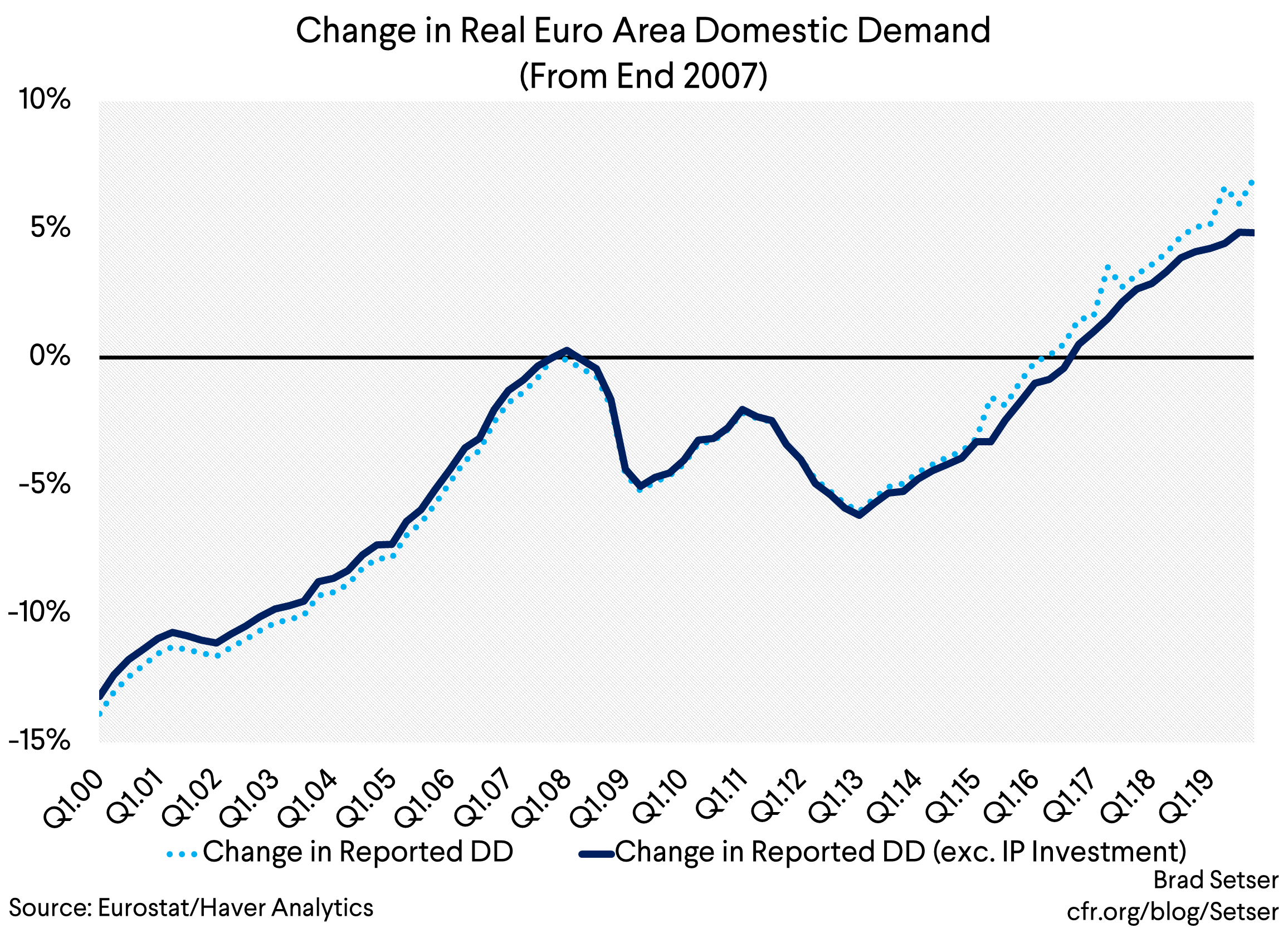

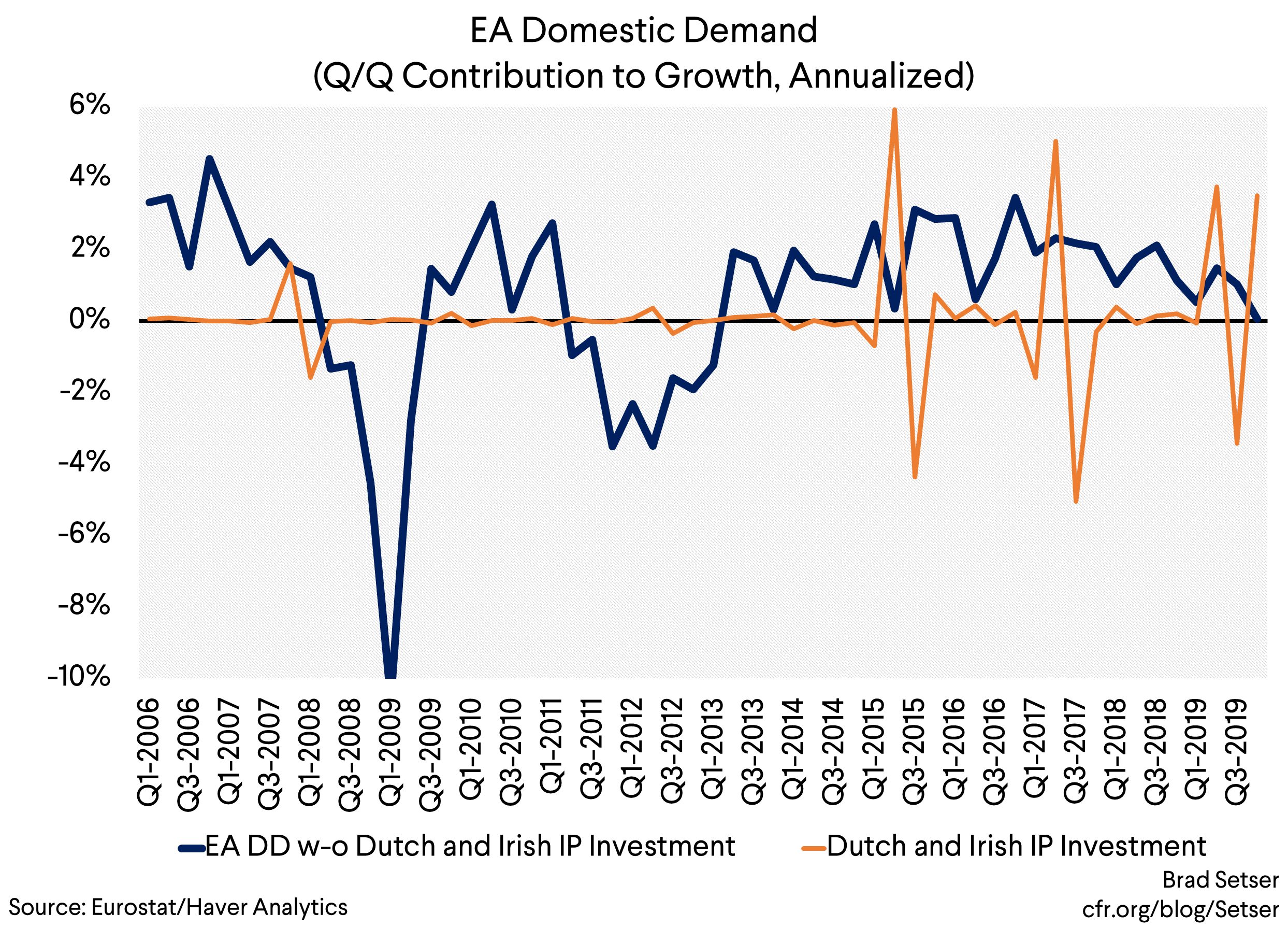

The net result though is that you more or less need to take Ireland out of the euro area data to get a picture of what the “real” euro area economy is doing.

There isn’t an investment boom in the euro area. Nor is Europe sucking in service imports from the rest of the world, generating a big windfall for service producers.

The ECB totally gets it. They understand that you need to look through the Irish impact on the components of euro area demand to see the underlying trend.

Euro area demand growth had stalled even before the corona virus upended the global economy.

But I am not sure that the Trump Administration and the U.S. Treasury understands that the massive shift into Ireland is a function in part of the incentives that were created by the U.S. tax reform. I don’t think the intent of tax reform was to drive a big jump up in Irish GDP. But that has been the effect.

The old tax game was to put your sales subsidiary in Ireland, and have it pay a big dividend to a second Irish company that wasn’t technically a tax resident of Ireland—and then defer your U.S. corporate tax liability (while screaming about how the global U.S. tax system was unfair, and how there were trillions of dollars trapped offshore).

The new tax game is to set up an Irish resident company that can take advantage of the Capital Allowance for Intangible Assets tax structure to get a low single digits Irish tax rate, and then pay the 10.5 percent (net of 80 percent of your actual Irish tax) U.S. global minimum on intangibles.

That’s not much of a change from the point of view of the companies.

But it more or less means that a portion of what should be U.S. GDP now is showing up in the Irish data. That will be more clear once some of the huge accounting moves associated with firms‘ optimization around the end of the double Irish fade, and the nature of the ongoing distortion becomes clearer. The big “investments” made in 2019 will raise Ireland’s reported GDP over time. It just won’t really be Ireland’s GDP.

And, well, with the corona virus shock about to hit the data, I am afraid that the tax distortions that drove the euro area’s 2019 data will soon be forgotten. But they shouldn’t be. Their impact was too big. Some things need to get fixed when the world returns to normal.

---

I want to recognize the work of many Irish economist on this issue (Seamus Coffey, Stephan Kinsella, Philip Lane and no doubt many others). And I also want to recognize the contribution that the Currency—a new Irish publication—has made to enhancing our understanding of contemporary Irish based tax strategies. Thomas Hubert in particular has spent a lot of time deciphering the tax filings of a lot of Irish-American firms. Wikipedia has long been a stunning resource on this topic, thanks to the work of a couple of anonymous contributors.