When Did the China Shock End?

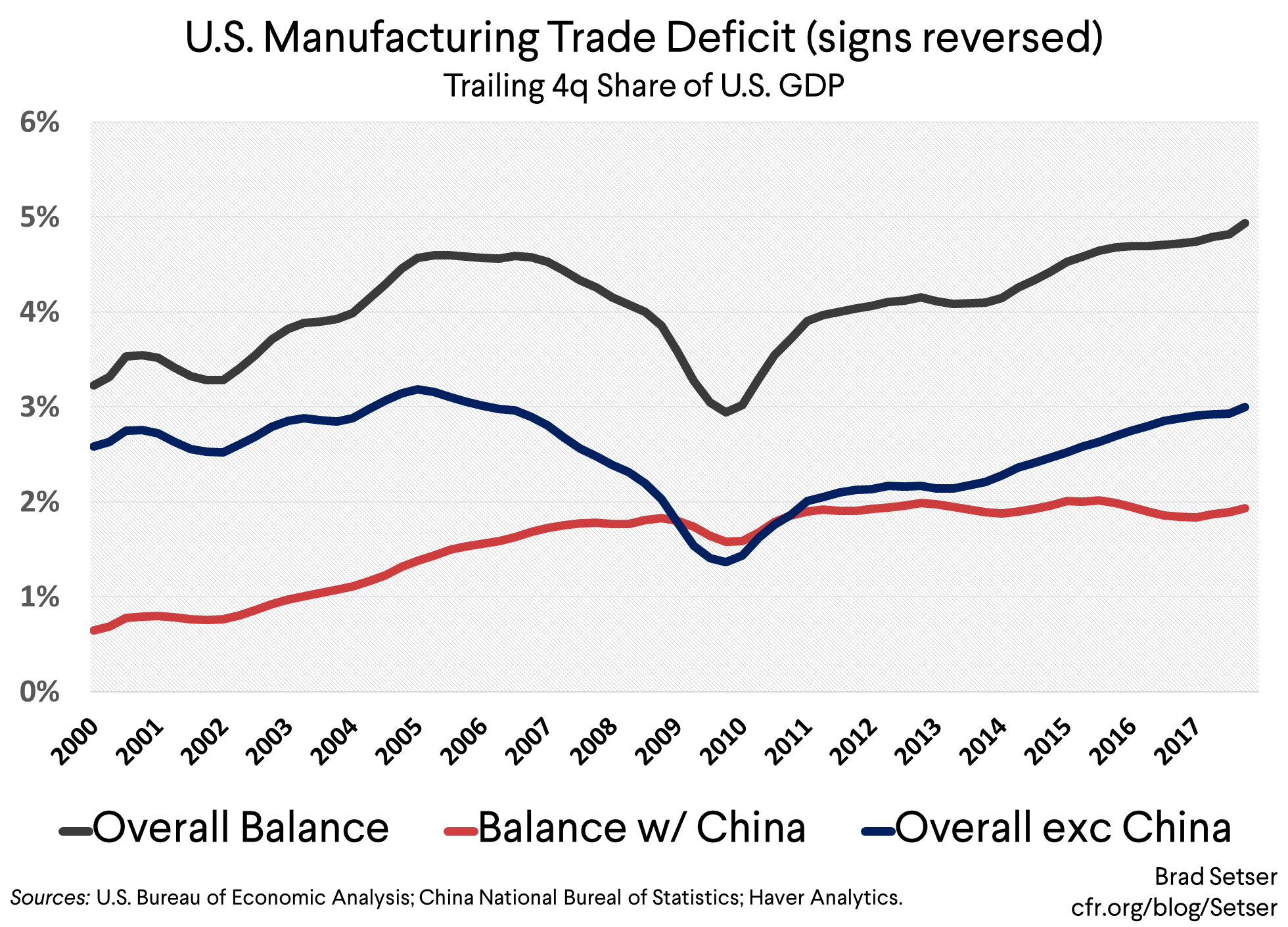

Conventional wisdom among economists is that the China shock ended a decade ago. That is largely because the U.S. bilateral deficit with China has been fairly stable since 2007 (measured as a share of U.S. GDP) while China’s current account surplus fell significantly as a share of its GDP from 2007 to 2017.

Neil Irwin of the New York Times wrote in late March: “globalization, at least in the form we have known it, leveled off a decade ago.”

I have a slightly more nuanced view—I would argue that the China shock continued, albeit in a more modest form, through the North Atlantic financial crisis and didn’t really “end” in aggregate until 2010 or so. More importantly, there are significant differences across different types of goods: the China shock for consumer goods (apparel, furniture, toys, home electronics, and the like) was mostly over by 2006; the China shock for capital goods lasted until at least 2012—and I would even argue that in some sectors the China shock is still ongoing.

The “China shock” of course is short-hand for the impact of rising Chinese imports on U.S. (and European) manufacturing employment in the period immediately following China’s WTO accession.

There was a China shock for commodities too. But that shock was positive—first prices rose, and then volumes rose to meet rising Chinese demand. Soybean farmers in Iowa view China differently than manufacturing workers in Ohio.

I want to focus on the manufactured side as that is the real source of concern—and, be warned, I will make use of bilateral data. Purists who view all bilateral data with disdain can skip to the aggregate numbers at the end.

I do think there is value in using the bilateral data to compare the pattern of U.S. trade with China and the pattern of U.S. trade with the world. China is big enough to influence the overall pattern of trade, and China’s exchange rate hasn’t always moved with the United States‘ other large trading partners. That said, there is no doubt that the bilateral balance with China overstates China’s impact on U.S. manufacturing and understates the impact of the rest of the Asian electronics supply chain.* The U.S. is more likely to displace Korea, Taiwan, and Japan as a source for high-end electronic components than to displace China as a location for final assembly.

Some definitions.

For “manufactures” I mean the NAICS definition and data, using all the codes in the 300s, minus refined petroleum. For some purposes I will also use the end-use data for capital goods and autos, and compare the trend of capital goods and autos with the trend for consumer goods. NAICS manufactures is a slightly broader concept than capital and consumer goods, as it includes the “manufactures” in the industrial supplies end-use category. And when I look at the Chinese data, “manufactures” is defined as Chinese total trade net of trade in what China calls “primary” products.

I generally include Hong Kong with China, as it is clear that many U.S. exports to Hong Kong end up in China (except when I was a bit lazy with the end use data, and for services I don’t think the adjustment adds much as most service exports to Hong Kong aren’t directly reexported to China).

Adding in Hong Kong somewhat reduces (I think correctly) the bilateral deficit with China.**

And everything is in nominal terms and has been scaled to GDP. Scaled real numbers are hard to do, and there shouldn’t be a big gap between nominal and real in manufactures.

What does the data show?

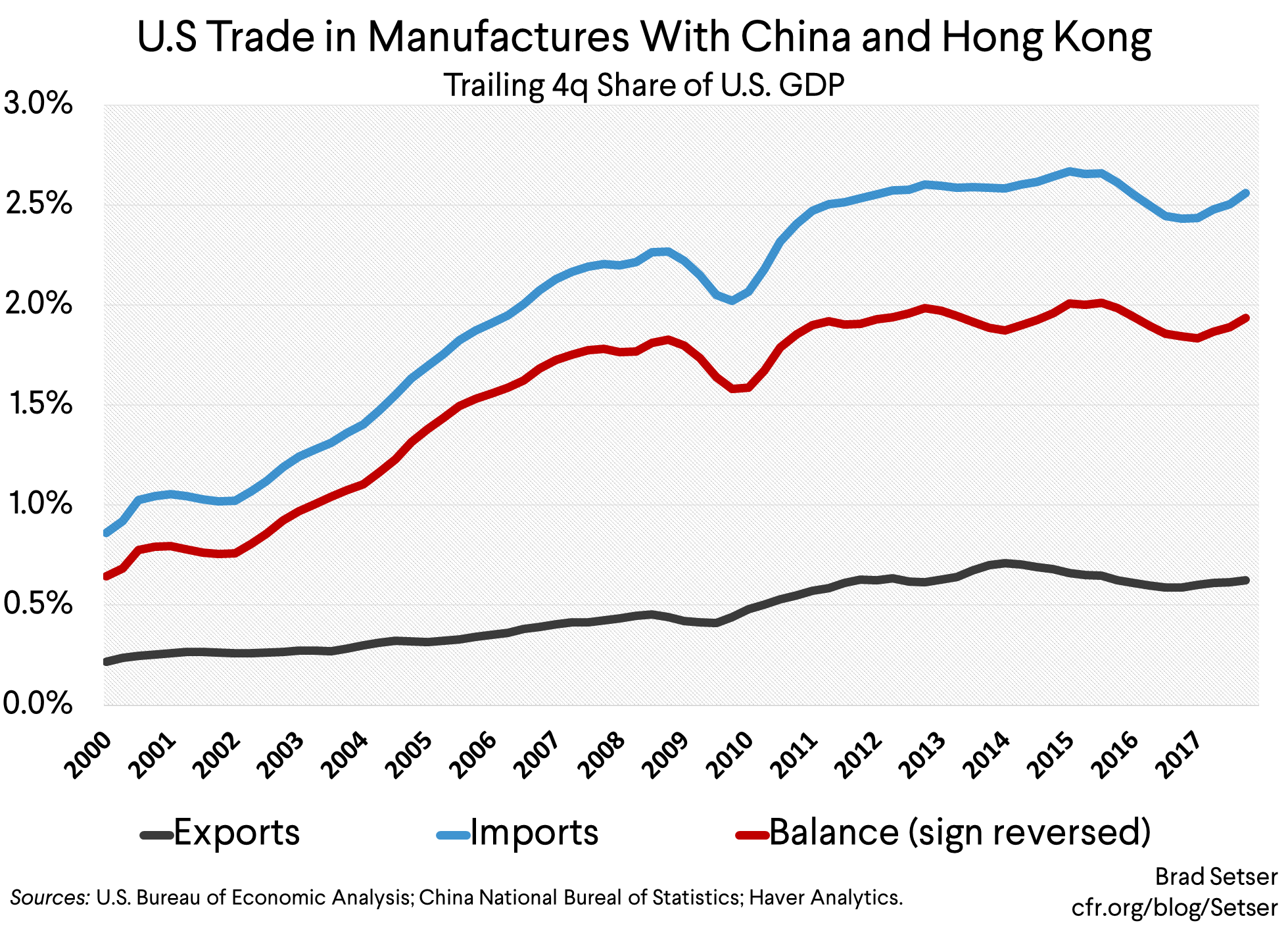

(1) The manufactured deficit (as a share of U.S. GDP) peaks in 2012 (though you can argue it essentially is flat from 2010 on), with an inflection point in late 2006 or early 2007.

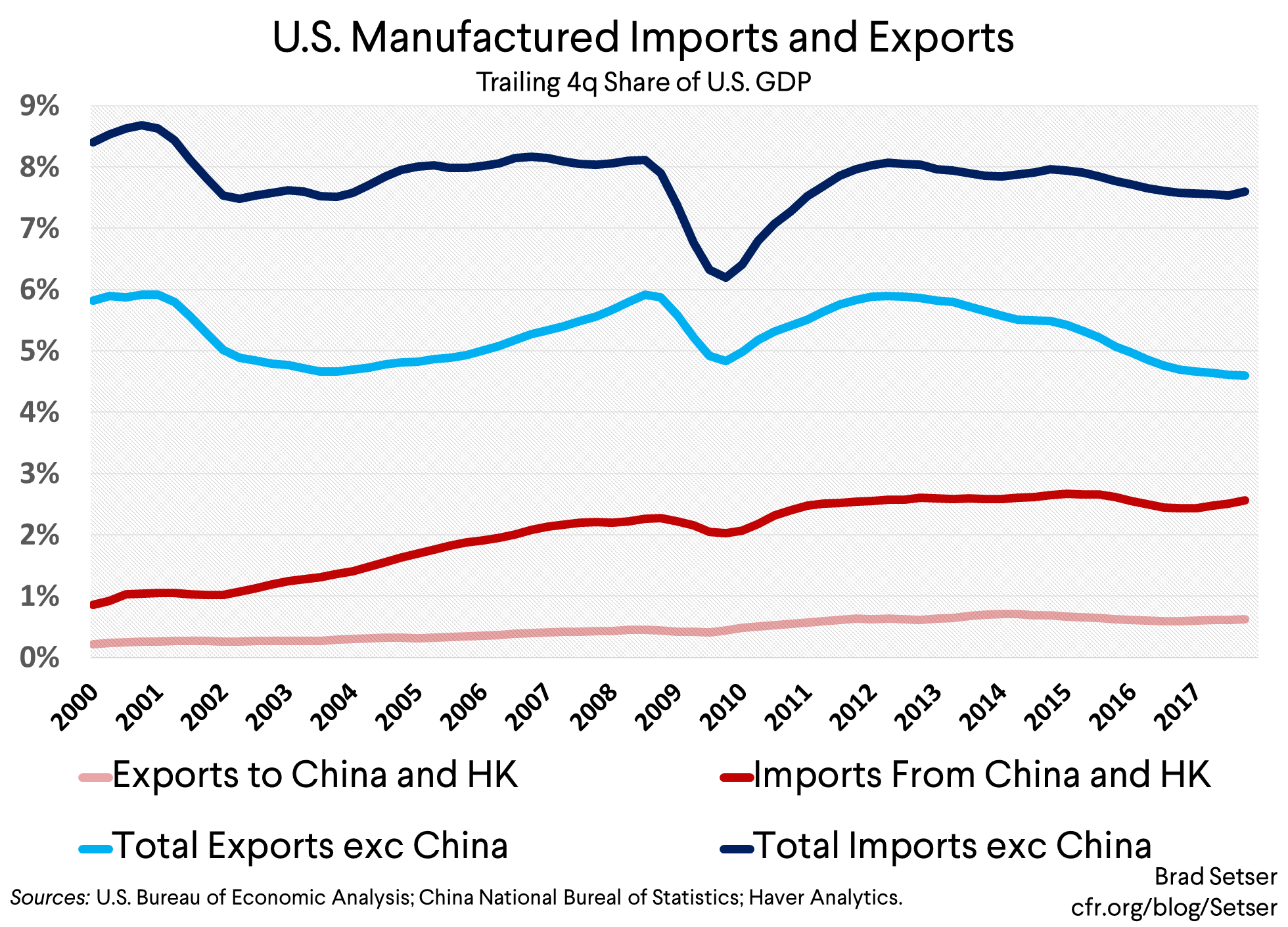

The rise in the overall deficit has mostly been driven by imports as the scale of U.S. exports of manufactures remains modest relative to imports of manufactures. In practice, very few of the manufactured components that China imports for reexport come from the U.S., in part because many U.S. semiconductor design firms use Asian “fabs.”

The rise in imports from China from 2002 on also doesn’t—contrary to a common argument—just reflect a reallocation of final production to China from elsewhere in Asia. If you take China out of the data on manufactured trade, imports from the world are flat from 2002 to 2007—the period when imports from China rise strongly.***

The overall numbers on manufacturing trade tells a story that is very consistent with the findings of Autor, Dorn, and Hanson. It is hard to see how a shift in importing from say Korea to importing from China would have an adverse impact on employment and wages in manufacturing-intensive regions of the U.S..

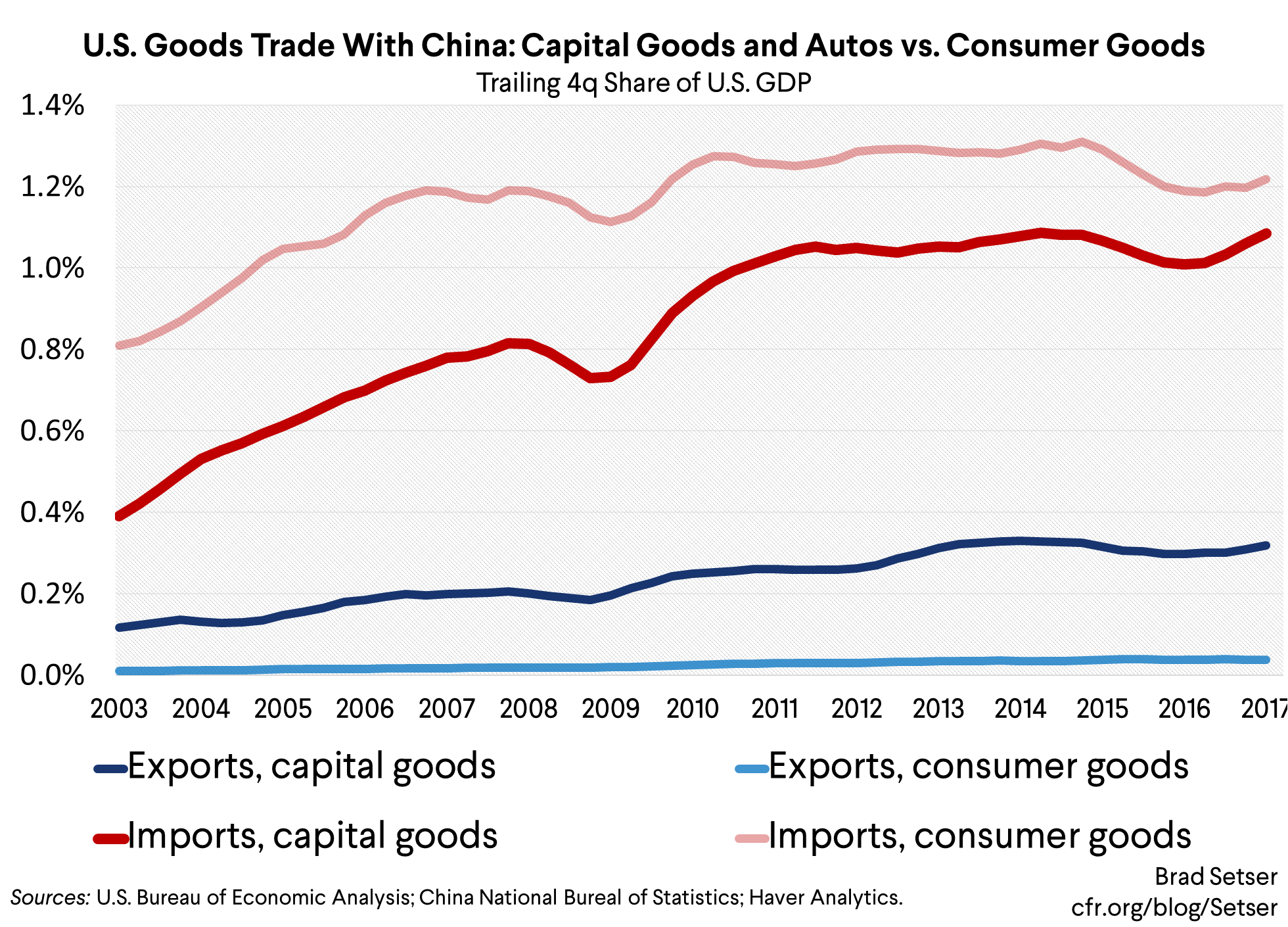

(2) The China shock ends at different points in time for different types of products.

The rise in Chinese exports of consumer goods to the U.S. after China’s WTO accession was fast and furious. It also was largely complete by 2006. That’s the bulk of the China shock. (One small note: cell phones are a consumer good, computers are a capital good).

The rise in capital goods imports by contrast continued through the global crisis. It only really slowed after 2012. And in some specific product categories it has continued. Many of the proposed Section 301 tariffs would hit parts used in the production of capital goods, e.g. the sectors where the impact of the China shock is likely ongoing (and where there is more likely to be U.S. production capacity). ****

(3) Magnitudes are important. The China shock was a swing in the trade balance with China and East Asia of a little more than a percentage point of GDP—and after 2006, the impact of the China shock was balanced by the recovery in U.S. exports to the world that followed the dollar’s 2003 depreciation (with a lag).

Ballpark math based on a change of that magnitude would generate a swing in the number of jobs supported by manufactures of about a million jobs (using the estimates for jobs supported by exports as a proxy for jobs in import competing sectors: see here and here). That is close to the numbers that emerge from the much more sophisticated work of Autor, Dorn, and Hanson (reassuring for me). Their 2 million number includes the indirect job losses—the loss of a factory has a local multiplier, so to speak, that amplifies the regional shock.

One other point: the China shock was so severe in the first part of the 2000s in part because it overlapped with the (lagged) impact of the dollar’s 2000-2003 strength. By contrast, from 2006 to 2008 the improvement in U.S. trade with the rest of the world exceeded the ongoing deterioration in the balance with China.

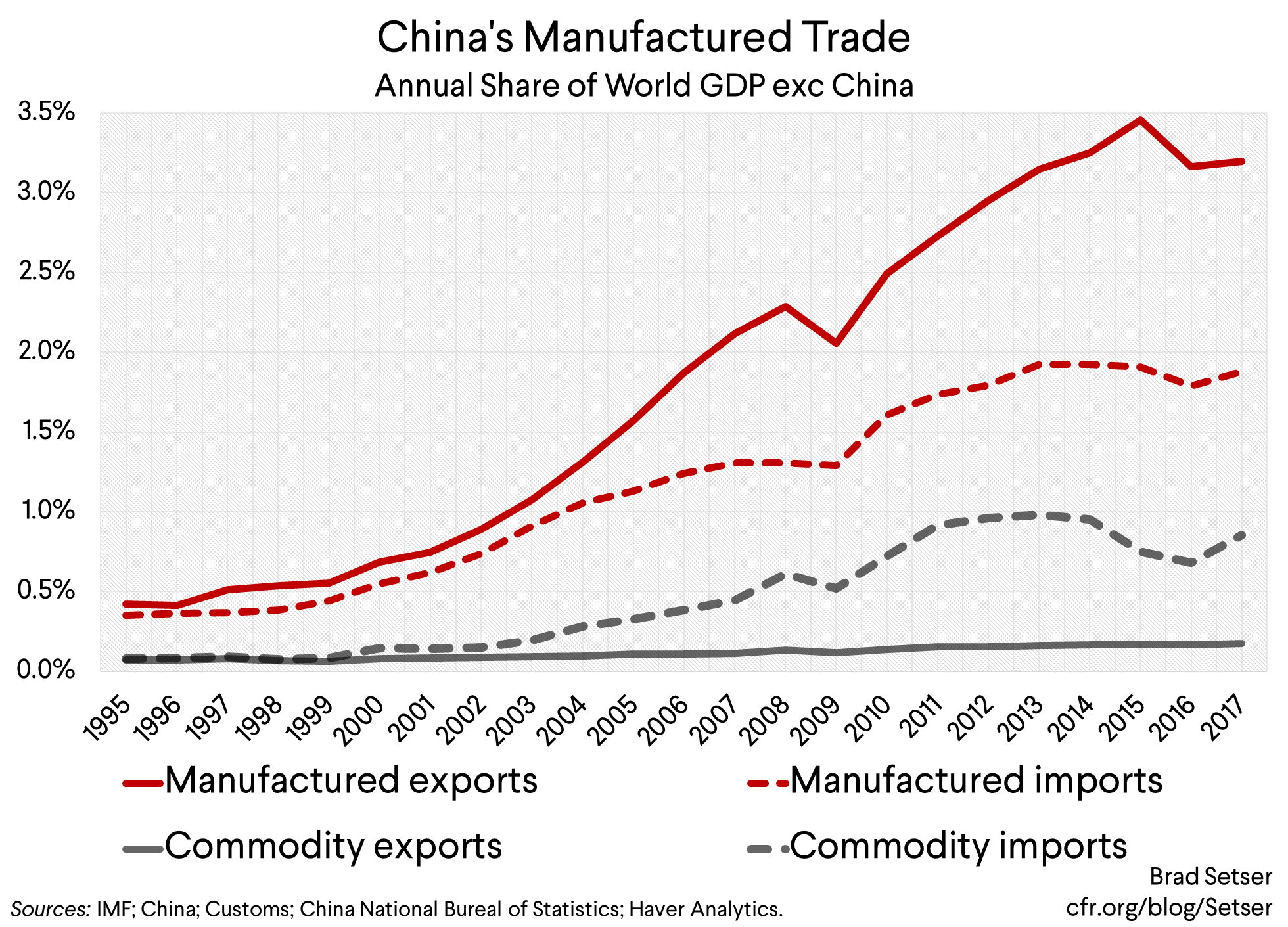

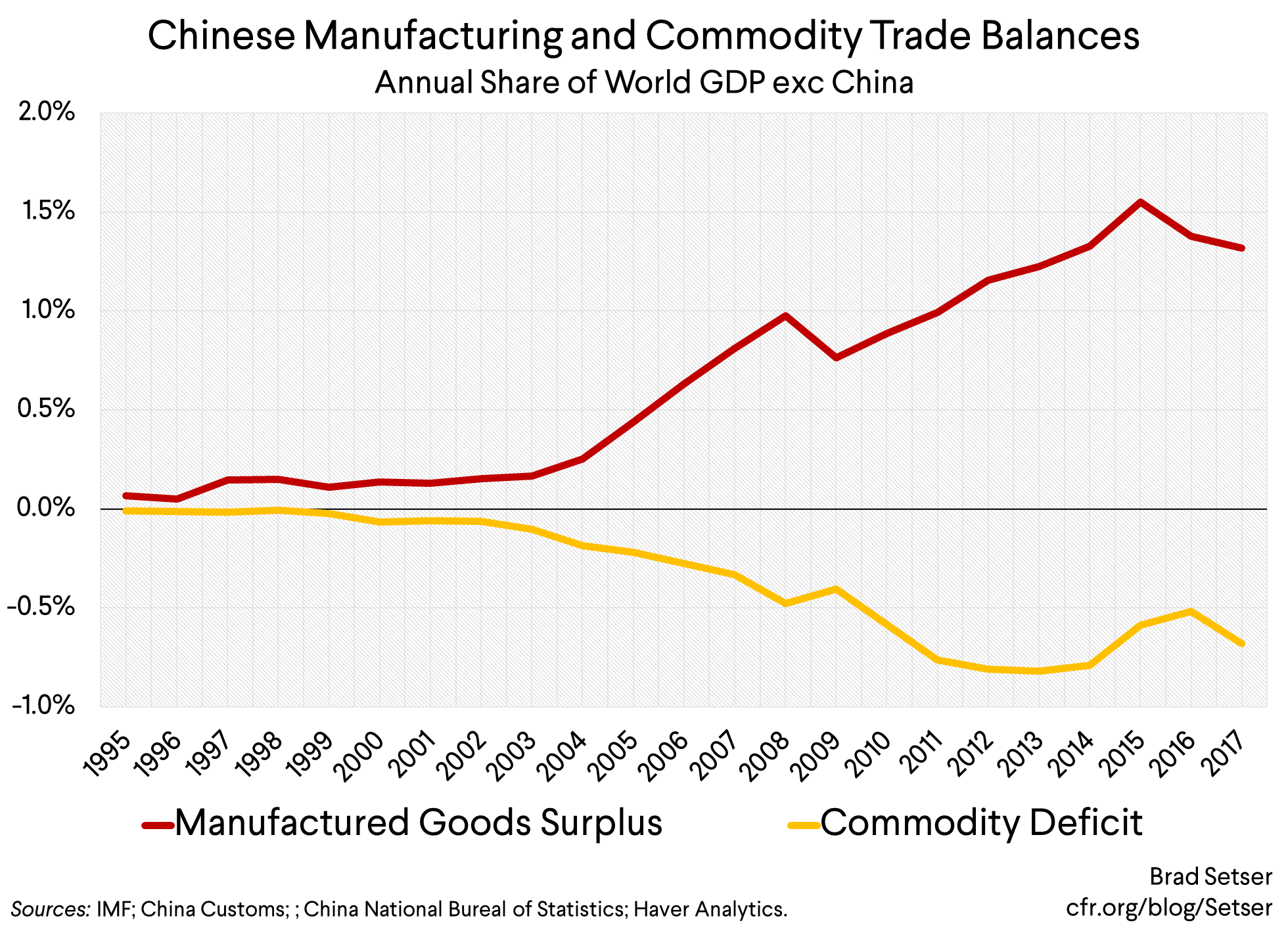

(4) The China shock lasts a lot longer in the Chinese data than in the U.S. data.

China’s exports of manufactures continued to rise relative to the GDP of China’s trading partners through 2015—and China’s total surplus in manufactures similarly peaked relative to the GDP of China’s trading partners in 2015.

A portion of the rise in China’s manufacturing surplus is a function of higher commodity prices in the years immediately after the global crisis—higher oil (and metal) prices allowed the oil (and metal) exporters to afford more imports of all kinds, and a lot of those imports came from China.

One implication of this: a growing share of China’s aggregate impact on the U.S. over time has come from competition for export market share in third party markets, not from imports. It is one reason why U.S. exports of manufactures (as a share of U.S. GDP) haven’t increased over the last twenty years.

Higher end U.S. capital goods often compete both with high-end products from countries like Germany and Japan and with lower end Chinese products. Think of construction equipment, or diesel locomotives for moving freight. In the future, think of aircraft…

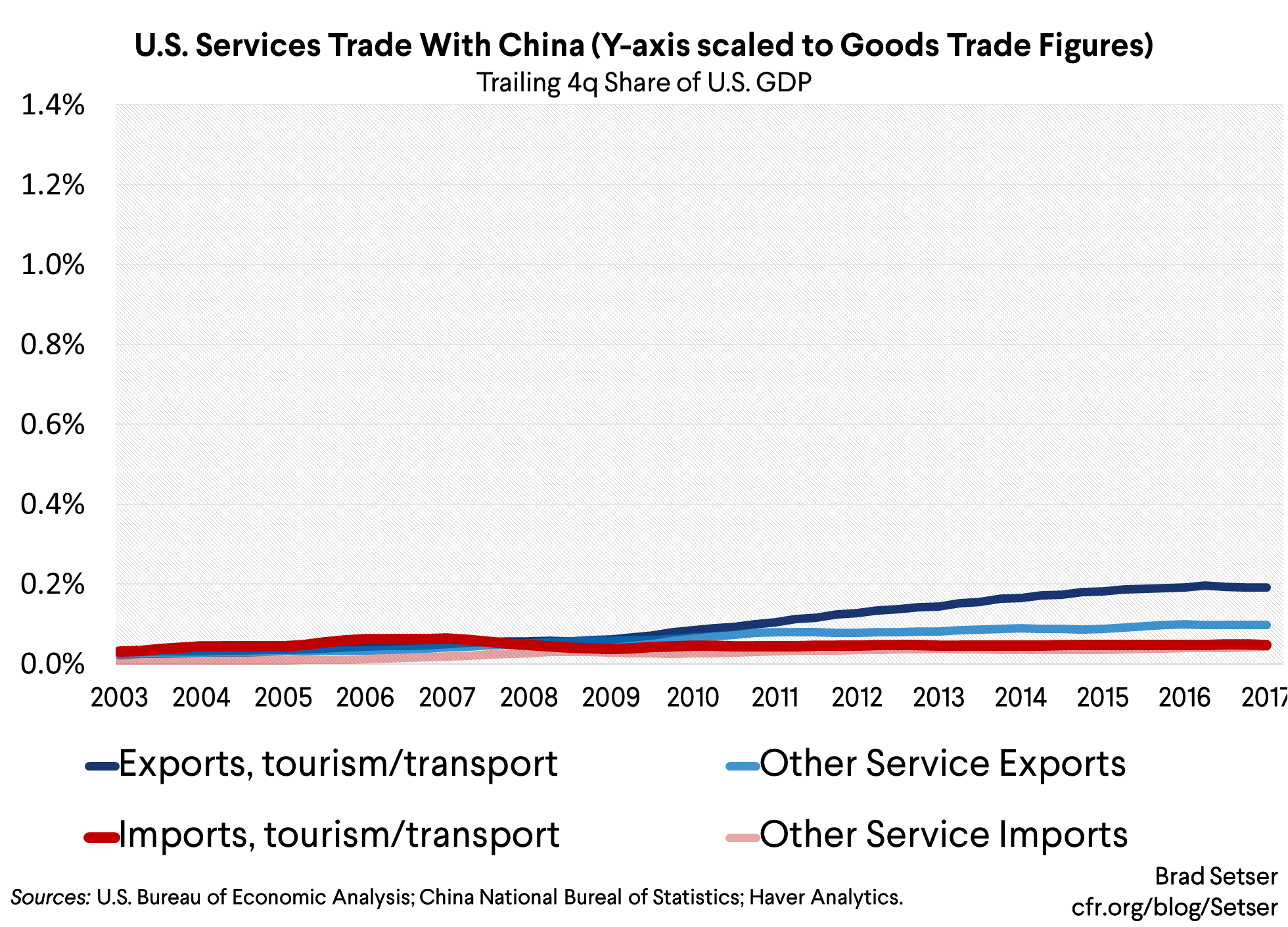

(5) Services haven’t provided a significant offset if you exclude tourism and education.

There is often talk of how U.S. the has a comparative advantage in services. That’s certainly true for many sectors.

But it also true that many services are hard to trade across time zones and legal and linguistic frontiers.

U.S. exports to China of services other than education and tourism (which require the physical movement of people) are around 0.1 percent of U.S. GDP, while imports are about half that. Putting a graph of services trade on the same scale needed for consumer and capital goods illustrates the relative size of trade in goods and trade in services.

Of course the bilateral data can also mislead, and that’s almost certainly the case here.

U.S. firms don’t export that many services to markets that are much more open either. They prefer to export intangibles to their subsidiaries in low tax jurisdictions, and then reexport those “services” at a higher price from places like Ireland and Switzerland and Bermuda. This both shifts taxable profits out of the U.S. to low (or zero) tax jurisdictions and services exports toward Europe and the Caribbean.

But I would caution that just because the U.S. economy is now dominated by the production of services doesn’t mean that “services” trade with China necessarily offers a huge opportunity: relatively few U.S. firms would provide services in China using U.S. workers.

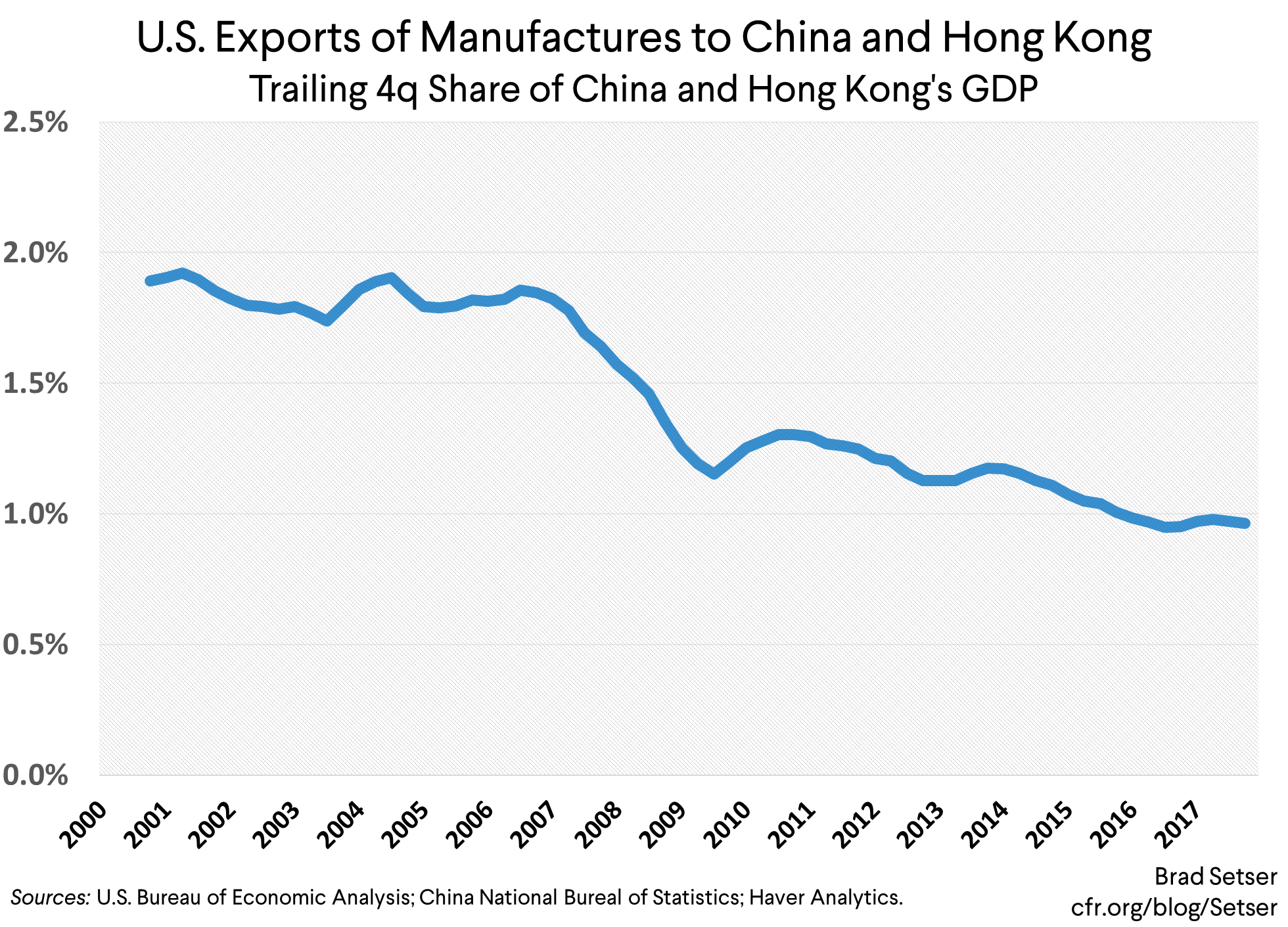

I personally suspect that largest opportunities for increasing the number of jobs supported by U.S. exports to China would come from reforms that raised China’s propensity to import capital goods—or at least policy changes that scaled back China’s plans to displace existing imports of capital goods with Chinese production. U.S. exports of manufactures have lagged the growth in China’s GDP from 2006 on, in part because of Chinese import-substituting policies.

Obviously there is some disagreement here on the relative priority to be placed on goods versus services —but the conclusion matters. The U.S. isn’t going to get everything it wants in a negotiation with China. The Trump Administration will have to set some priorities.

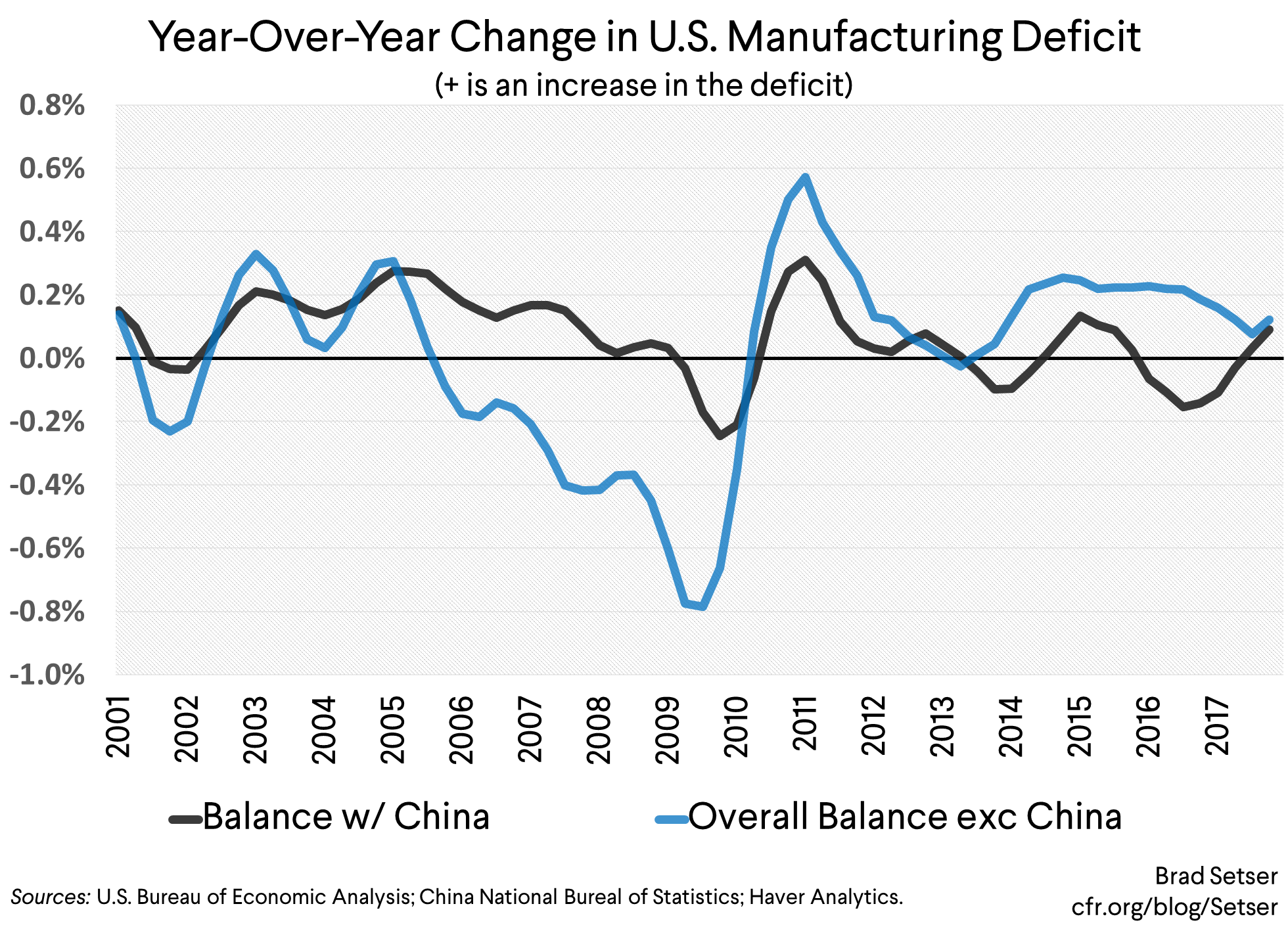

(5) Trade with China isn’t the only thing that matters. Right now the trade data is dominated by the lagged impact of the 2014 “dollar” shock.

Since 2014 there has been a negative “dollar” shock roughly equal in magnitude (over a percent of GDP) to the China shock of the early 2000s (the overall increase in the manufacturing trade deficit from 02 to 05 was a bit bigger than the increase in the trade deficit with China, so the current dollar shock isn’t quite as big as combined China and dollar shock of the early 2000s).

The swing though has been less visible (and less politically charged) because it has come exclusively from a fall in exports.***** Basically, with a stronger dollar, U.S. based manufactures have lost market share to manufactures in Japan and Europe.

The data on manufacturing trade obviously leaves out trade in services. But far more significant is the omission of trade in commodities. With the rebound in the manufacturing deficit after the dollar’s 2014-2015 appreciation, the bulk of swing in the overall trade balance from 2007 and 2017 comes from a single commodity: oil.

And I think it is important to recognize that this particular pattern of adjustment has meant that the manufacturing sector hasn’t directly benefited from the overall improvement in the trade balance, though no doubt it has benefited from increased domestic demand for the machinery and steel needed to drill wells and build pipelines.

*/ A value-added adjustment would reallocate a portion of China’s contribution to the overall U.S. deficit to China’s neighbors in East Asia. That’s a consistent distortion that should be internalized, though the scale of the reallocation varies over time (Chinese value-added has increased over time). There is an argument that the China shock is really an East Asian supply chain plus China shock.

**/ This adjustment also reduces the pace of the post-WTO growth in U.S. exports to China, as some of the initial growth reflected a shift from exporting through Hong Kong to exporting directly to China.

***/ The argument for reallocation compares imports from Asia today to imports at their 2000 peak (rather than from China’s WTO accession in 2002). But I don’t think that’s right—it confuses two separate trends. U.S. imports globally fell when investment fell after the .com boom/bust. And then when the U.S. started to recover, imports went up, with the bulk of the rise coming from China. Total imports of manufactures rose 1.5 percentage points of GDP from end 2002 to end 2007, while imports from China rose 1 percentage point.

****/ Formal models that have attempted to refine Autor, Dorn, and Hansen by say adjusting imports to reflect trade broken down by value-added generally find a strong China shock impact during the period before the global crisis, and much smaller (or zero) impact after the crisis. That doesn’t surprise me. The impact of the China shock on capital goods in the post-crisis period would be much smaller than the impact of the initial shock to both capital and consumer goods, and very difficult to disentangle from the overall recovery that followed the huge Lehman shock. Job market dynamics were essentially driven by the recovery in domestic demand over this period. And more generally, much of the impact of China’s emergence as a capital goods exporter has come from a loss of U.S. market share in third party markets and thus won’t be identified in studies that focus on the impact of Chinese imports on the local job market in manufacturing intensive parts of the country.

*****/ The greater impact of currency moves on exports than on imports is consistent with most formal economic modelling. See the Federal Reserves‘ international transactions model. However, formal modelling would have predicted a bigger rise in imports after the dollar’s fall than was actually observed. I suspect that is because the dollar shock is correlated with a commodity shock, and a shock to the level of real investment in commodity production (investment tends to be capital goods intensive and thus trade intensive).