When it Comes to Exporting (Manufactures), Europe is Now the One from Mars

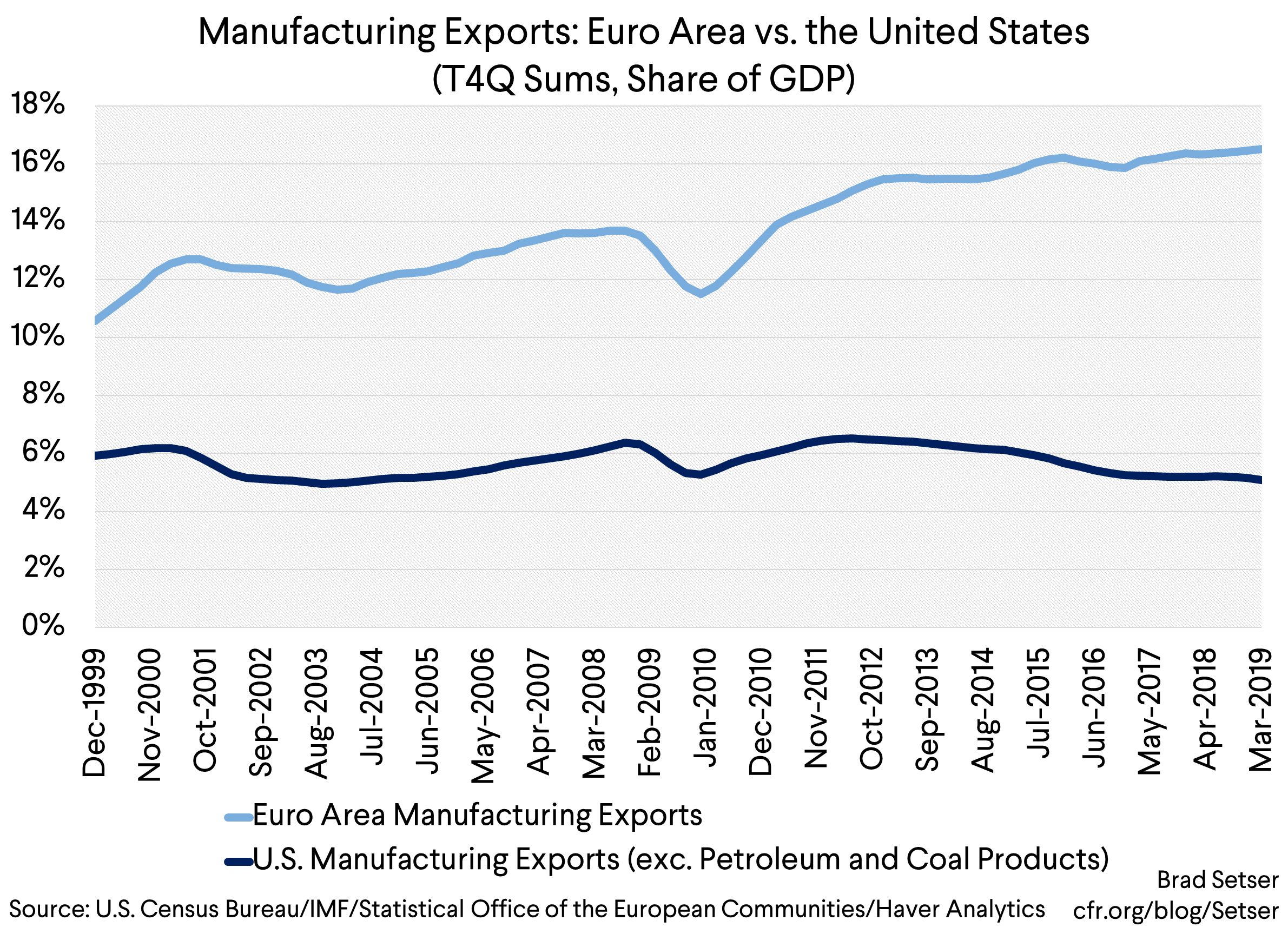

Manufacturing exports are about three times more important to the euro area than to the U.S. economy.

That’s largely because the U.S. now exports very few manuactures.

And China’s imports of manufactures, once you net out imports for re-export (processing) really are quite small.

The United States and Europe are sometimes presented, economically, as the mirror images of each other. The European Union’s common market was, after all, meant to replicate the scale of the U.S. market. And the French at least want the euro to take on an international role comparable to the dollar.

Europe has more taxes and social protection, the United States a rawer and more pure form of capitalism—or so the stereotype goes. Europe also has a far tighter fiscal policy than the United States, and a looser central bank—and the United States is a centralized fiscal union while the EU and the euro area are not. But at the end of the day, the U.S. and European economies are generally considered to be more alike than different.

But, well, in one big and structural way that isn’t true. Not anymore.

U.S. exports of manufactures, as a share of U.S. GDP, are about a third that of the euro area economies.*

That’s a change from the late 1990s, when U.S. exports of manufactures were about half that of the euro area (relative to each country’s GDP).

To get a sense of the magnitude of the difference these days, total U.S. exports of manufactures—as a share of U.S. GDP—are smaller than Germany’s trade surplus in autos. Admittedly, Germany does specialize in autos, and it is a uniquely manufacturing heavy economy.

But it is still a huge difference.

Europe hasn’t adopted the “design it here, make it abroad” model in quite the same way as U.S. business. Julius Krein writes “United States industry is losing ground to foreign competitors on price, quality and technology. In many areas, our manufacturing capacity cannot compete with what exists in Asia.” Judging from the export data, U.S. industry also has had trouble competing with Europe.

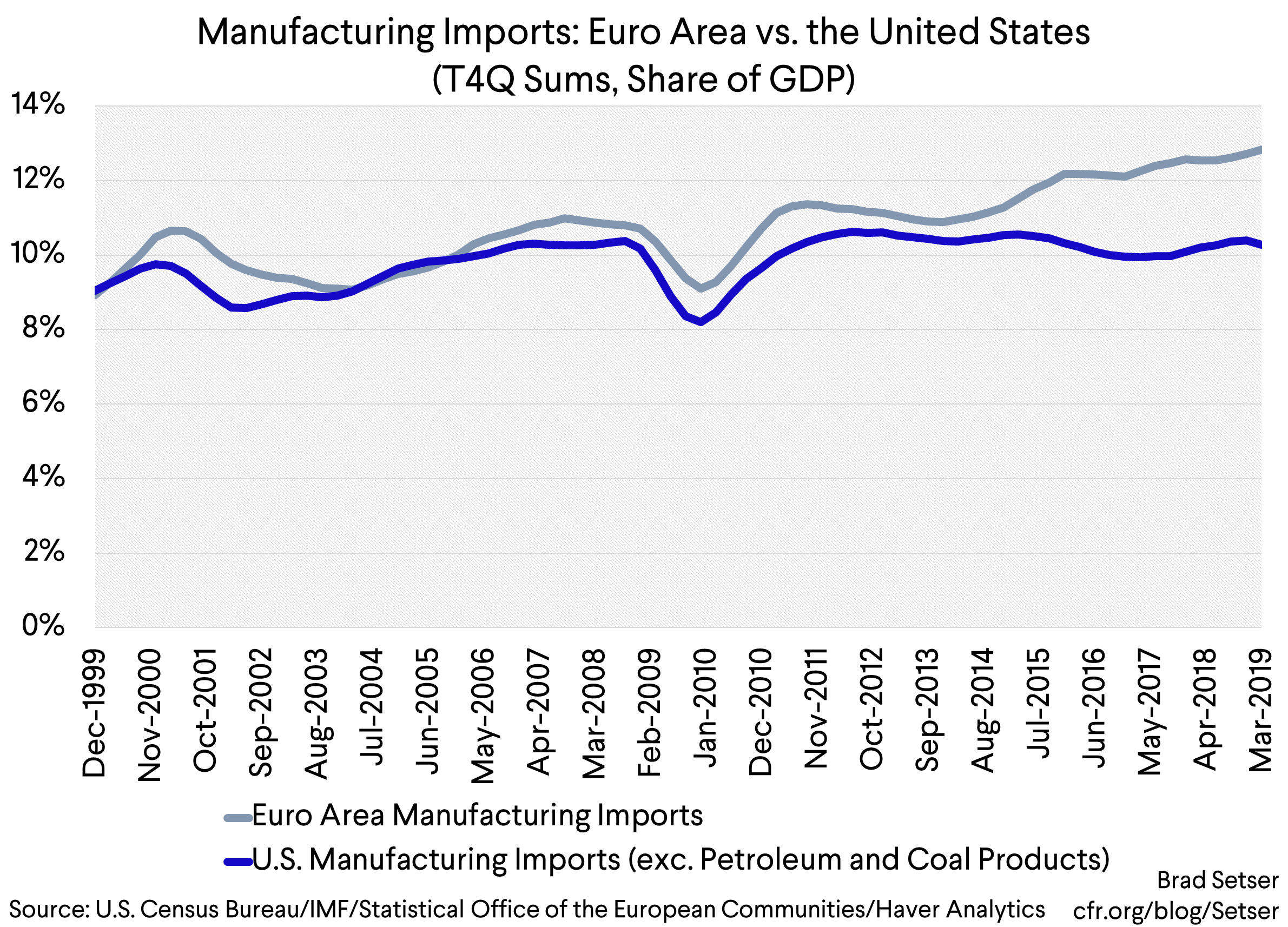

There isn’t a comparable difference between the United States and Europe on the import side. Imports of manufactures are broadly similar as a share of each region’s GDP. Euro area imports are actually a bit higher.

The result of course is that the euro area’s trade surplus in manufactures is roughly equal in size to the U.S. trade deficit in manufactures. In very ballpark terms, in the Commerce department’s data, the United States imports around 10 percent of its GDP in manufactures, exports about 5 percent and runs a 5 percent of GDP deficit (net of U.S. exports of refined petroleum)—other ways of measuring the data would put the deficit at more like 4 percent of U.S. GDP. The euro area’s surplus in manufactures is around 4 percent of its GDP.

To some degree that’s a function of the United States relatively strong resource endowment—back in the 1970s, when the United States was importing a lot of oil (at a high real price), it was a net exporter of manufactures. Thanks to the tight oil revolution, the United States no longer needs to trade manufactures (or services) for oil.

Some say it is a consequence of a U.S. comparative advantage in services —I am not convinced. Once you net out travel and tourism (limited U.S. vacation time acts as an impediment to U.S. imports there, I suspect), U.S. service exports aren’t particularly high relative to U.S. GDP, and services exports actually haven’t been particularly dynamic in the past few years. Plus a lot of non-tourism related services exports are to the world’s tax havens (exports of financial services to the Caribbean, exports of R&D services to Ireland and Switzerland, and so on). “Real” service exports, setting the transport of goods and people aside, to the major economies still tend to be quite modest.

Rather than focusing on services, I would focus on the large offshore profits of U.S. firms. Apple and the internet advertising titans tend to register in the data more as a source of offshore profits than as a source of service exports. These profits help to offset the U.S. trade deficit on the manufacturing side, and also help cover the interest it pays on its roughly 50 percent of GDP in net external debt.

But even so, it is important to note that globalization—as experienced by the United States—has produced far more rapid growth in the offshore profits of U.S. firms than in “made-in-the U.S.A. goods.” For the United States, globalization has meant a rise in manufactured imports relative to manufactured exports—e.g. a secular shift out of manufacturing. And that isn’t true for Europe.

In the long-term, I suspect the United States will need to re-create a stronger manufacturing sector—and not just pay for its manufactured import bill out of the excess profits U.S. firms report they earn abroad (assuming there is a limit to the ability of the United States to borrow to pay for imports). The United States’ net debt position (the “stock imbalance” in the IMF’s jargon) isn’t small.

But in the short-run, the euro area’s export dependence is a bit of a problem—it has left Europe quite exposed to the current global manufacturing downturn.

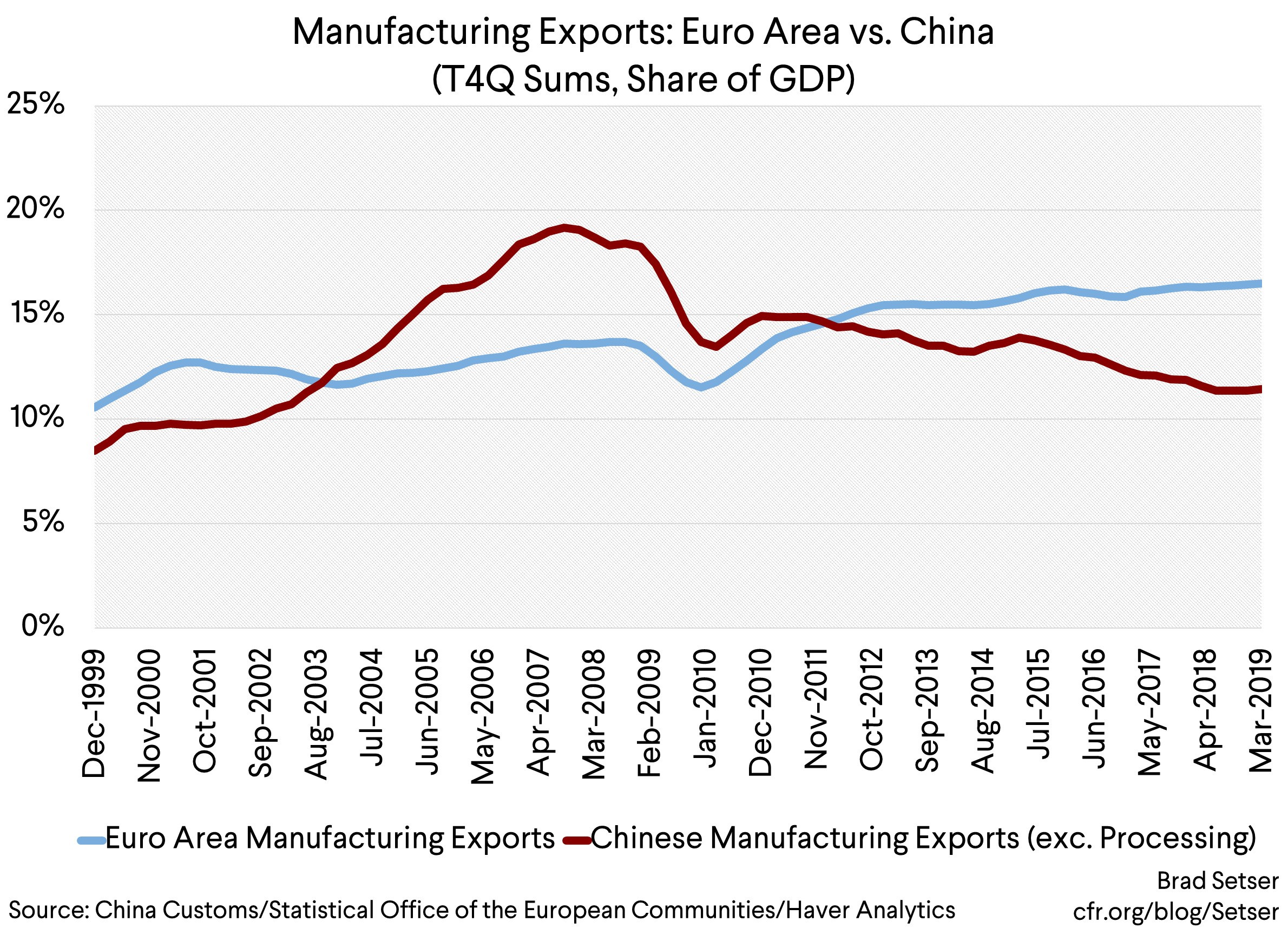

There is of course a secondary question—namely how does China stack up with Europe.

And the answer, on the export side, is that if you net out China’s processing imports, it is a little less dependent on exports than the euro area.

Now arguably that’s a misleading comparison, and the euro area relies on imported inputs too—but it isn’t easy to do a like for like comparison.

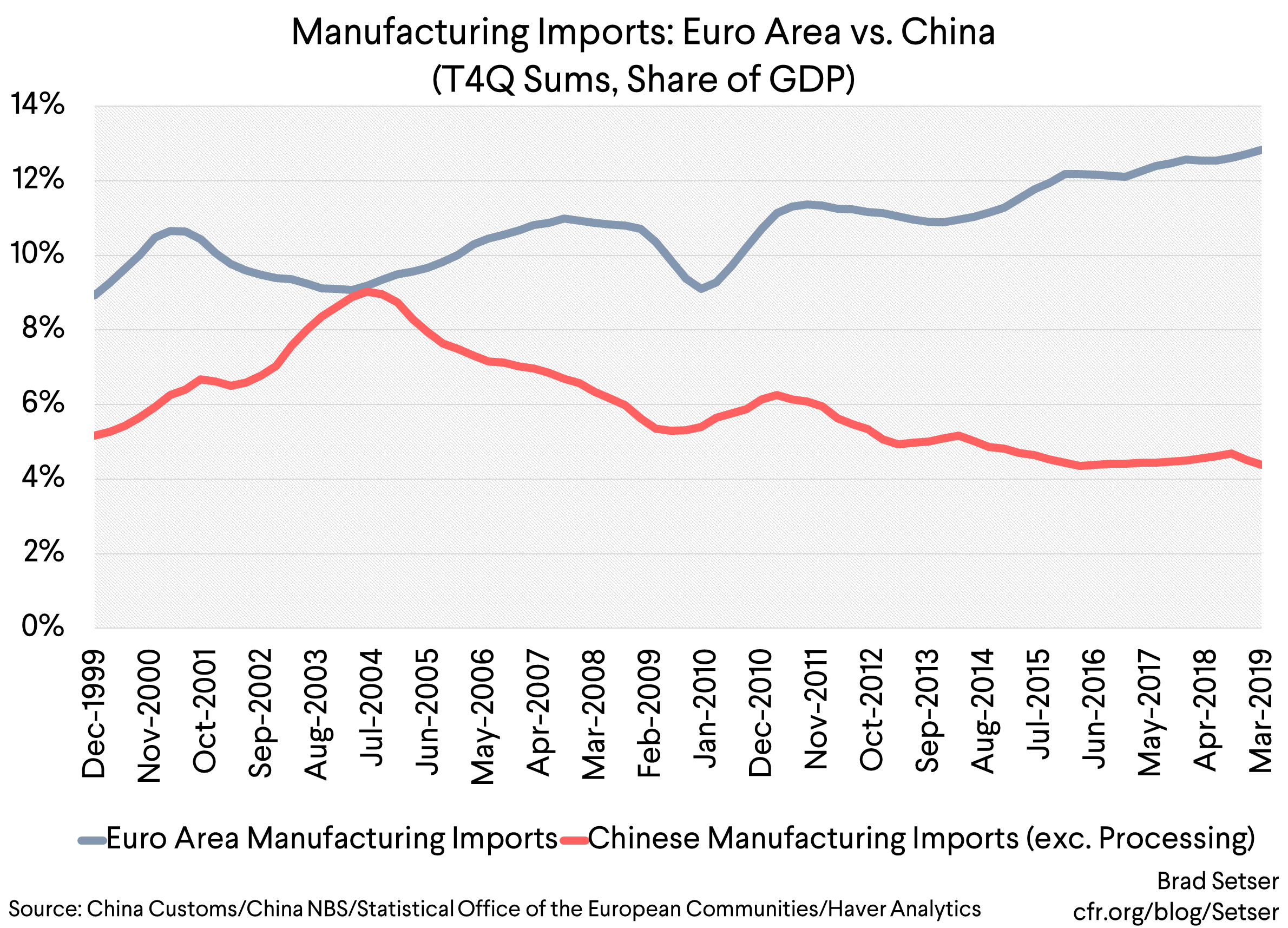

What’s clear, though, is that China’s imports of manufactures, net of its processing imports (imports for re-export) are much smaller as a share of its GDP than Europe’s imports are relative to its GDP.

That’s in part a consequence of China’s relatively high level of commodity imports (tied to its resource endowment, but also its very high investment to GDP ratio—as investment tends to be import intensive).

The net effect, though, is that China’s manufacturing trade is very unbalanced—with far more exports than imports (commodity trade and tourism trade are unbalanced in the other way). China’s manufacturing surplus is almost twice as big as its imports of manufactures. The surplus in manufactures is now around 7 percent of China’s GDP, and manufactured imports (net of processing imports) are about 4 percent of China’s GDP. And that in turn makes China a difficult trade partner for many. Especially now that its surplus in manufactures is trending up again.

* U.S. exports of manufactures to non-NAFTA countries are only something like 3 percent of GDP, with Boeing and the aircraft engine manufactures accounting for something like one quarter of all manufactured exports that leave North America.