Stephen C. Freidheim Symposium on Global Economics

Event date

The 2020 Stephen C. Freidheim Symposium on Global Economics discusses the implications of the coronavirus pandemic on global economic policy.

This symposium is presented by the Maurice R. Greenberg Center for Geoeconomic Studies and is made possible through the generous support of Council Board member Stephen C. Freidheim.

The full agenda is available here.

Keynote Session: A Conversation With Mark Carney

Mark Carney will discuss his perspective on how to rethink valuation within the market economy, as well as economic policies for a post-pandemic world.

Speaker

- Vice Chair and Head of ESG and Impact Fund Investing, Brookfield Asset Management; Former Governor, Bank of England (2013–2020); Former Governor, Bank of Canada (2008–2013)

Presider

- Chairman and Chief Executive Officer, BlackRock; Member, Board of Directors, Council on Foreign Relations

Transcript

STAFF: (Gives welcome remarks.)

FINK: Welcome to today’s Council on Foreign Relations virtual Steven C. Freidheim Symposium on global economic[TT1] s…our keynote session with Mark Carney. I’m Larry Fink, Chairman and CEO of BlackRock and a member of the Board of Directors of CFR and I’ll be presiding over today’s discussion and taking questions. This symposium is presented by the Maurice R. Greenberg Center for Geopolitical Studies, it is made possible through the generous support of the council board member Stephen C. Freidheim. Mark Carney, a friend, is currently the Vice Chairman of Brookfield Asset Management, and head of ESG and impact fund investing. Mark served as governor of two countries, not just one—pretty amazing—of the Bank of England from 2013 to 2020 and prior to that as the governor of the Bank of Canada from 2008 to 2013. He was a chairman of the Financial Stability Board in 2011 to 2018 and he’s currently the United Nations Special Envoy for climate action and finance. Nice resume mark.

CARNEY: Thanks, Larry (laughs)…

FINK: Really good, really impressive. Anyway with that background, let me just start off and ask, where are we, in terms...

Session II: Global Economic Policy After the Coronavirus

Panelists will discuss pressing issues facing the global economy as a result of the coronavirus pandemic, including government debt, fiscal policy, and the role of central banks.

Speakers

- Associate Professor of Economics, London School of Economics and Political Science

- Chief Economist and Macro Strategist, Mellon; Former Director, Division of Monetary Affairs, Federal Reserve; CFR Member

- President, Centre for Economic Policy Research; Professor, International Economics, The Graduate Institute of International and Development Studies; Research Professor and Distinguished Fellow, INSEAD Emerging Markets Institute

Presider

- Sebastian MallabyCFR ExpertPaul A. Volcker Senior Fellow for International Economics, Council on Foreign Relations; @scmallaby

Transcript

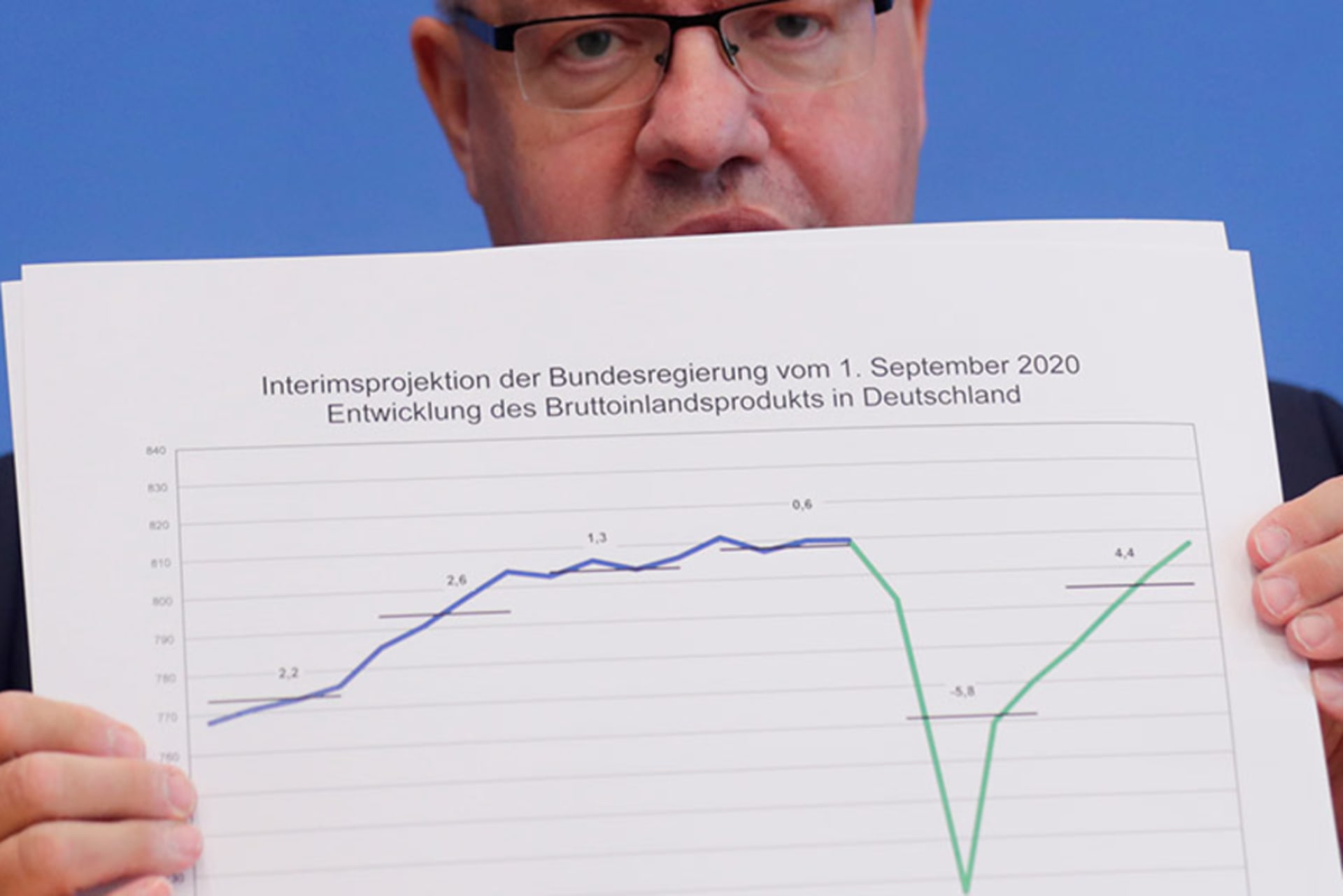

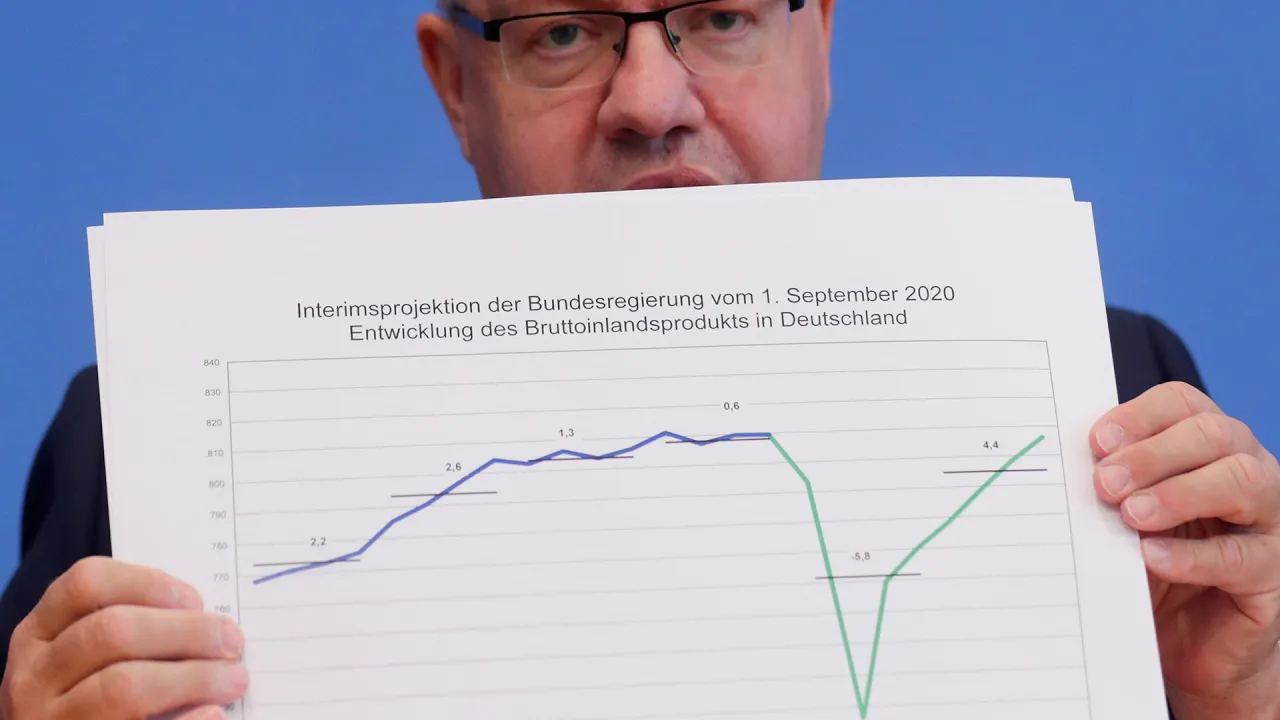

MALLABY: Thanks so much, and welcome everyone to today’s CFR virtual Stephen C. Freidheim Symposium on Global Economics. I’m Sebastian Mallaby, the Paul A. Volcker senior fellow for international economics here at CFR, and I’ll be presiding over today’s discussion. This symposium is presented by the Maurice R. Greenberg Center for Geoeconomic Studies and is made possible through the generous support of Council board member Stephen C. Freidheim. This is actually the second session of this symposium. Some of you may have seen yesterday’s session with Mark Carney, and today we’re going to be addressing global economic policy after the coronavirus. Of course, COVID-19 has already elicited a big policy debate with unprecedented monetary and fiscal responses and forced choices between public health, public safety, and public liberty. Even in the revised, and a bit rosier assessment, published this week by the Organization for Economic Co-operation and Development (OECD), global output is expected to shrink by 4.4 percent this year, making this the worst recession since the 1930s.

The good news, of course, is the rollout of vaccines. And some of you may have heard at yesterday’s session, Larry Fink talking about May as a reasonable target for...