Egypt’s Solvency Crisis

Contingency Planning Memorandum No. 20

Steven A. CookCFR ExpertEni Enrico Mattei Senior Fellow for Middle East and Africa Studies

Steven A. CookCFR ExpertEni Enrico Mattei Senior Fellow for Middle East and Africa Studies

Introduction

Egypt is experiencing a deep economic crisis. The country’s foreign currency reserves are less than half of what they were before the January 2011 uprising, threatening Egypt’s ability to pay for food and fuel. Egypt’s budget deficit is 14 percent of gross domestic product (GDP) and its overall debt, which is the result of accumulated deficits, is more than the country’s economic output. In this difficult economic climate, roughly 45 percent of Egyptians live on less than two dollars per day. Inflation, which reached as high as 12.97 percent after the July 2013 military coup, is currently at 11.4 percent. Tourism revenue—traditionally a primary source of foreign currency along with Suez Canal tolls and remittances from Egyptians working abroad—is less than half of what it was in the last full year before the uprising. Foreign direct investment has dried up outside the energy sector. Unemployment remains high at 13.4 percent. Among the unemployed, 71 percent are between fifteen and twenty-nine years old. This economic weakness makes it politically difficult to address the problems that contribute to a potential solvency crisis because the necessary reforms will impose hardship on a population that is already experiencing economic pain.

Despite these problems, the state of Egypt’s economy has received less attention since the July 2013 coup d‘état because of an influx of financial support from Saudi Arabia, the United Arab Emirates, and Kuwait.

Yet Egypt’s economy remains shaky and the threat of a solvency crisis lingers. Indeed, the continuation of violence, political protests, and general political uncertainty—even after planned presidential and parliamentary elections—along with a hodgepodge of incoherent economic policies, all portend continuing economic decline. This in turn could create a debilitating feedback loop of more political instability, violence, and economic deterioration, thus increasing the chances of an economic calamity and yet again more political turmoil, including mass demonstrations, harsher crackdowns, leadership struggles, and possibly the disintegration of state power.

The Contingency

Insolvency is the inability of an entity—a person, corporation, or country—to meet its financial obligations to lenders. It comes in two forms: balance sheet insolvency and cash flow insolvency. The former occurs when an entity has total liabilities whose value exceeds that of its total assets. Egypt is at greater risk of experiencing the latter, meaning that it cannot meet specific obligations as debt payments are due, and thus defaults. Although its causes were different, Greece’s sovereign debt crisis that began in 2009 provides a baseline comparison of a heavily indebted country that had periods of macroeconomic performance, but ultimately was unable to meet its obligations.

Government debt is 89.2 percent of GDP and overall debt is more than 100 percent of GDP.

The overall picture of the Egyptian economy is deeply worrying. Egypt’s foreign currency reserves stand at approximately $16 billion to $17 billion, not all of which are liquid. This means that Egypt is just above the $15 billion critical minimum threshold of foreign reserves, which is the amount required to cover costs of food and fuel for approximately three months.

Chart 1. Egypt’s Foreign Exchange Reserves

Due to the unsettled and violent political environment, tourism dropped sharply in 2013. In early 2014, Minister of Tourism Hisham Zazou told the newspaper Al-Hayat that “2013 was the worst year on record for Egypt’s tourism industry.” Foreign and domestic investment also declined, in comparison to the five years before the January 2011 uprising. In addition, Egypt’s central bank announced a cut in interest rates with little warning in late 2013, as part of an effort to spur domestic investment. This makes good economic sense, but the move is also potentially inflationary, putting pressure on the currency and foreign reserves as well as on Egyptian consumers.

Government debt is 89.2 percent of GDP and overall debt is more than 100 percent of GDP. It is important to note that the national debt and fiscal deficit are particularly problematic for Egypt because of its debt rating (even though it was recently upgraded from CCC+ to B-). Unlike the United States, Germany, or Canada, each of which has significant levels of debt, it is costly for Egypt to finance its deficit and debt through borrowing. As a result, Egypt has financed its deficit through domestic borrowing from public sector banks and the central bank. According to Fitch Ratings, “bank claims on the government account for 67% of total bank assets.”

There is still an estimated annual $10 billion gap in financing the Egyptian government’s deficit.

Immediately following Mohammed Morsi’s ouster, Saudi Arabia, the Emirates, and Kuwait committed $12 billion to Egypt. The Gulf countries have committed an additional $8 billion as of early 2014. The Egyptians can also tap into an $8.8 billion grant from the Gulf Cooperation Council (GCC) that dates back to the 1990s. This assistance is intended to provide budget relief, replenish foreign currency reserves, finance construction projects, pay for the production of medicines, and make petroleum resources available (though fuel rationing continues).

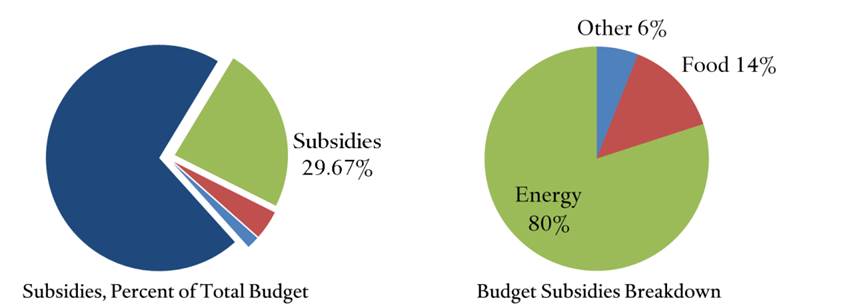

For all of these resources, however, Gulf assistance has provided Egypt with only a bare minimum of relief. For example, there is still an estimated annual $10 billion gap in financing the government deficit. There are two reasons why infusions of more money from foreign donors will not fix Egypt’s economic problems. First, by financing new spending with grants from the Gulf, Egypt is merely shifting fiscal problems into the near future. Second, receiving more assistance only masks problems that are rooted in irrational and conflicting economic policies. These policies—including food and fuel subsidies, a still-robust state-owned sector, and a tax policy that does not produce enough revenue—are the primary reasons why the government burns through anywhere from an estimated $1 billion to $1.5 billion of its reserves per month paying for critical needs and defending the currency. The policies place significant pressure on the government’s budget. Subsidies, for example, account for 29.67 percent of the government’s expenditures.

Chart 2. Egypt’s Subsidies

Yet, the prevailing political uncertainty in Egypt makes it difficult for the government to undertake meaningful reform. The rigidity of Egypt’s system of subsidies, for example, is a critical component of the Egyptian social safety net and an important means of political control. Making fundamental changes to subsidies risks mass demonstrations similar to the 1977 Bread Riots, which erupted after Anwar Sadat proposed alterations to food subsidies consistent with recommendations from the International Monetary Fund (IMF).

Despite pledges to reduce the government budget deficit to 10 percent of GDP (it reached 14 percent of GDP in 2012–2013), Egyptian officials have increased spending, including on a stimulus program and the introduction of a minimum wage for public sector workers. Yet, it will be difficult to reduce the deficit while pursuing expansionary fiscal policy. The new minimum wage of $172 per month will put further pressure on the budget. Likewise, additional economic stimulus packages will also increase the deficit. It may very well be that an expansionary fiscal policy is necessary, but the Egyptians do not have the means to finance it. In addition, despite much discussion of subsidy reform and some rather modest headway in means-testing energy subsidies, the effort to address this major problem is more theoretical than real. Distortions in the markets for bread, fruit, and vegetables also persist, but are unlikely to be addressed for political reasons. This type of ad hoc policymaking seems aimed more at temporarily mollifying various interests than establishing economic sustainability and is a sign of the leadership’s inability to arrest Egypt’s economic decline.

A reduction or suspension of the aid would certainly precipitate a solvency crisis.

The foreign reserves problem is exacerbated by Egypt’s sensitivity to changes in commodity prices, given that it is a net importer of oil and natural gas and the world’s largest importer of wheat. Consider, for example, a run-up in wheat prices, which are critically important given the Egyptian government’s commitment to subsidizing bread. An external shock such as drought, extreme heat, wildfires, political instability, or some other cause of a poor harvest in the major global producers—the United States, Canada, Australia, Ukraine, and Russia—would result in a substantial increase in the global price of wheat, placing an additional burden on Egyptian finances. Another potential shock is the rapid depreciation of the Egyptian pound, resulting from any number of factors including the central bank’s decision to cut interest rates, a move by foreign donors to decrease (though not end) their financial assistance to Cairo, or an unforeseen political event that encourages Egyptians to change pounds into dollars. With limited foreign reserves at its disposal, Egypt’s central bank would be hard-pressed to defend the currency, resulting in inflation. Under these circumstances, Egypt might be forced to print money, which would compound the inflationary pressures associated with depreciation.

No single event alone would trigger a solvency crisis, but multiple political and economic factors already present could potentially make Egypt default. Saudi Arabia, the United Arab Emirates, and Kuwait seem willing to underwrite Egypt with few conditions or limits. Yet, Gulf support may not be sustainable over the longer term, if Egypt’s financial needs prove to be greater than anticipated, if political rifts develop with Cairo, if the priorities of the Saudis, Emiratis, and Kuwaitis change, or if any of the three Gulf states face budgetary or political pressures of their own. A reduction or suspension of the aid would certainly precipitate a solvency crisis.

The most likely trigger for insolvency, however, is the continuation of current economic policies, which place significant and ultimately unsustainable pressure on the country’s finances. Egyptians may enjoy a respite with an upcoming presidential election and the false sense of “turning the corner” it might provide. As the Egyptian government continues to pursue incoherent fiscal and monetary policies, the foreign reserves situation will deteriorate, rendering Egypt insolvent. The onset of this crisis may be long in the making, but its effects will likely be felt quickly. Egyptians would once again be unable to buy fuel, medicine, basic foodstuffs, and other important goods. Such a situation could potentially bring large numbers of people into the streets in opposition to the government. Given the tendency of Egypt’s internal security services to respond to demonstrations with too much force—which encourages people to join protests—rallies could spread throughout the country. This revolutionary bandwagon could overwhelm the government, but this time it may be even more difficult for the military to maintain stability and its control of the state. The Gulf states would likely again provide financial support to Cairo to avoid this outcome. However, infusions of aid will neither resolve nor mitigate the adverse effects of economic policies that have led to the solvency crisis.

Warning Indicators

The following warning indicators should help U.S. officials and other observers determine whether Egypt is facing an imminent solvency crisis:

- The government tightens currency controls. Should the government prevent individuals and firms from transferring certain amounts of hard currency out of Egypt, it would be a clear signal that Egyptian officials are concerned about the country’s solvency. Beginning in January 2014, individuals can transfer up to $100,000 in hard currency out of the country, which is a relaxation of previous controls established during the Supreme Council of the Armed Forces–led transitional period after former president Hosni Mubarak’s ouster that limited transfers to $100,000 over a lifetime. Egyptian officials have left open the possibility of changing exchange-rate controls in 2015. A tightening of restrictions would preserve foreign currency, but at the expense of scaring away current and potential investors.

A rise in Cairo’s overdue debts is perhaps the clearest indicator that Egypt is headed toward insolvency.

- The government restructures its debt, forcing banks to buy debt instruments. Restructuring government debt would require the Egyptian government to force banks to exchange old debt for new debt or to impose new taxes on their returns. Imposing debt restructuring on the banks would place additional pressure on Egypt’s financial sector. In addition, the extent to which authorities are forcing banks to buy bonds and treasury bills to finance the deficit, or the Central Bank of Egypt is financing government purchases, indicates that the country is nearing a solvency crisis.

- Egypt’s arrears rise. Observers should pay careful attention to Egypt’s arrears. A rise in Cairo’s overdue debts is perhaps the clearest indicator that Egypt is headed toward insolvency. A rise in arrears may be the result of settling certain obligations before others, but it does indicate that default is a strong possibility.

- Egypt suddenly demonstrates an interest in an International Monetary Fund standby agreement. The Egyptian government is counting on Gulf assistance to float the economy. In addition, an IMF standby agreement is a politically difficult proposition for Cairo. Thus, although signing a deal with the Fund seems—from the outside—to be prudent, it is politically difficult. Under these circumstances, a sudden Egyptian interest in negotiating with the IMF would indicate that Cairo is worried about its solvency

Implications for U.S. Interests

Insolvency in Egypt would damage U.S. interests, threatening the safety of American citizens and U.S. property while putting U.S. business assets at risk. The largest American investor in Egypt, the Houston-based oil exploration and production company Apache Corporation, reduced its exposure to Egypt by bringing on Sinopec as a partner in late 2013. Egypt’s total share of Apache’s overall production declined from 26 percent to 16 percent. Other large multinationals such as Coca-Cola continue to operate in Egypt with little disruption, but an economic crisis and the concomitant political instability might negatively affect those firms.

The northern Sinai . . . has become a staging ground for attacks on Israel’s southern cities and towns.

Breakdown in Egypt would also affect U.S. forces and military posture in the Persian Gulf. The U.S. Navy places a premium on expedited transit through the Suez Canal. In addition, multiple daily U.S. Air Force overflights through Egyptian airspace en route to the Gulf could be curtailed or halted as a result of an Egyptian collapse. Finally, the United States and other interested parties, including European and Gulf states, would confront a major humanitarian crisis in Egypt, which would have trouble securing basic necessities for its eighty-six million people.

An economic collapse triggered by insolvency and the subsequent political fallout in Egypt would also threaten Israeli security. The northern Sinai, where the military is fighting a low-level insurgency, has become a staging ground for attacks on Israel’s southern cities and towns. If one of those attacks killed or injured large numbers of Israelis, it would force the Israelis to respond, potentially compromising the Egypt-Israel peace treaty—a pillar of U.S. policy in the Middle East.

Preventive Options

Although the United States has its own fiscal problems, it can still pursue several discrete measures that could help prevent a solvency crisis and potentially stave off Egypt’s economic collapse.

- Provide loan guarantees. The United States, European Union (EU), and Asian allies could pool resources and provide loan guarantees for Egypt. The United States has successfully pursued a similar policy in Jordan. Loan guarantees offer two primary benefits to donors and recipients: they are an effective way of leveraging large amounts of money with a limited commitment of resources—unless Egypt defaults—and they allow Cairo to borrow on commercial markets at significantly lower interest rates than a country with a B- rating would otherwise be able to obtain. Recognizing the sensitivity in the United States to offering the Egyptians what some consider a “blank check,” there would need to be a prior agreement with Cairo that the loans would be used for Egypt’s greatest needs, specifically food, fuel, and medicine. There are also some practical problems associated with loan guarantees. The loan guarantees involve expenditures that would require authorization from the U.S. Congress and subsequent spending cuts to offset the resources spent guaranteeing loans for Egypt. In addition, even with the backing of the United States, Europe, China, Japan, South Korea, and other global economic actors, Egypt’s ability to borrow on commercial markets with its poor rating represents a significant challenge.

- Relieve the debt. Egypt’s foreign debt is $47 billion as of the end of January 2014, of which $3.5 billion is owed to the United Sates. This external debt is relatively small as a percentage of GDP compared to domestic debt. Still, it could send an important signal to other holders of Egyptian debt if the United States took steps to relieve Cairo’s financial burden. In 2011, the United States sought to “swap” Egypt’s dollar-denominated debt for payment in Egyptian pounds that would then be used to pay for programs like education and youth employment. This scheme was dropped over objections from the Egyptian government. But the Obama administration proposed a debt swap for good reasons—specifically, to encourage Egyptians to invest in areas that were in dire need of resources and would benefit Egypt in the future. Given developments over the last three years and the state of the economy, relieving Egypt’s debt to the United States is still prudent. It is important to note that debt relief, like loan guarantees, requires congressional authorization and spending cuts to offset this assistance, though it would be less than the amount of the debt.

- Pay down domestic debt. The United States should encourage the Egyptians to use foreign assistance to pay down public domestic debt, which stands at $240 billion, instead of increasing expenditures on subsidies, a minimum wage, and a stimulus package that Cairo has no way to finance.

Armed forces remain the only truly national institution Egypt has.

- Keep the lights on. Although not as acute as they were in the spring and early summer of 2013, fuel shortages and blackouts in Egypt continue. In early June 2013, the Saudis and Egyptians signed an agreement to share energy by linking the two countries‘ power grids. This is a step toward relieving shortages, but the project will take two to three years to complete. Gulf fuel transfers since the coup have helped mitigate the problem, but demand remains high and Egypt’s production of natural gas has declined. Rather than leaving the issue to Saudi Arabia, the United Arab Emirates, and Kuwait, the United States could establish a consortium of international donors to facilitate Egypt’s import of the natural gas necessary to generate electricity, freeing up money in the budget to focus on longer-term threats to Egypt’s economic stability. Once again, the U.S. Congress might be reluctant to assist Egypt in this manner given the need for budget cuts with any new expenditure.

Mitigating Options

In the event that Egypt defaults on its debts, the United States has several options to alleviate the consequences and reduce the likelihood of a political collapse in the country and its attendant strategic and humanitarian problems.

- Support the military. In the event of a solvency crisis and its attendant political consequences, it is likely the military would intervene in politics. The United States should offer political and diplomatic support to the senior command to prevent Egypt from becoming a failed state. This means recognizing any new government that results from such an intervention and using Washington’s diplomatic clout with allies in the region, Europe, and Asia to do the same. It will also entail additional economic support. American support for the Egyptian military, along with Washington’s response to the 2013 coup, is controversial in both Egypt and the United States. The unpleasant fact, however, is that the armed forces remain the only truly national institution Egypt has. Its civilian political class lacks dynamism, and its other government ministries barely function and command few resources. In the event of insolvency, the officer corps will be the only relatively organized and coherent force capable of preventing a descent into chaos.

- Provide immediate infusions of financial assistance. The United States could establish an Egypt Contact Group so that wealthy countries can extend immediate financial assistance to Egypt. The Group would include the United States, EU, major Asian countries, and the Gulf states. As noted above, Egypt could potentially experience a solvency crisis even with assistance from wealthy countries in the Gulf, which is why it is incumbent on the rest of the world to marshal even greater resources to refloat the Egyptian economy.

- Restore food aid. Food aid to Egypt ended in 1992; it could be started again. Egypt is particularly sensitive to changes in the global price of wheat. Indeed, between 2009 and 2011, food insecurity in Egypt increased by 3 percent. Economic collapse would only increase food insecurity.

Recommendations

The United States has limited diplomatic and economic tools at its disposal to help the Egyptians. Even if Washington could bring billions to bear on Egypt’s economic difficulties, it would do little to mitigate the underlying economic problems that place the country at risk of a solvency crisis. It is up to the Egyptians to undertake reforms to forestall this outcome. Given the fact that the Egyptians have done little in this regard, a solvency crisis is entirely plausible. Consequently, the United States has a strategic responsibility to do what it can in Egypt to prevent the causes of insolvency and its attendant political consequences. In addition to implementing the preventive measures outlined above, the Obama administration should do the following:

- Work with the U.S. Congress to support Egypt with additional aid. There is resistance in Congress to increasing aid to Egypt. But the $250 million in economic support funds is a paltry sum given Egypt’s needs. Again, additional funds will not by themselves resolve Egypt’s economic problems, but they will give Egyptian policymakers time to undertake politically controversial reforms. Ideally, the United States would condition this new assistance on much-needed economic reform. This is unlikely to work given that Gulf aid is available without explicit prerequisites, which is why Washington should focus its diplomatic efforts on convincing wealthy Arab states and others to encourage Cairo to undertake meaningful reforms. Still, the Obama administration and legislative branch should take a long view of Egypt; while the status of Egypt’s Copts, the government’s commitments to human rights and democracy, and Egypt’s relations with Israel are important, they are secondary to a solvency crisis that threatens Egypt’s collapse, which would surely affect all of the issues over which Congress has expressed concern.

- Establish an interagency Egypt crisis monitoring group. The U.S. State Department, Central Intelligence Agency, Department of Defense, and Treasury Department should increase their surveillance of the Egyptian economy in order to better prepare the government to respond to an Egyptian crisis. This interagency group would be particularly important given that the Egyptian government tends not to be forthcoming with accurate economic data. The United States should share its information and findings with friendly governments that are also committed to preventing an Egyptian solvency crisis.

- Push others to do their part. The United States should prepare for the moment when Egypt’s economic problems overwhelm even Gulf-based aid and use its diplomatic clout in other parts of the world to secure additional assistance for Egypt. Countries in Asia and Europe are understandably reluctant to commit resources to Cairo without Egyptian policy reform, which is why Washington should also encourage Egyptian officials to resume negotiations with the IMF. The Fund should play an important role in assisting the next government to redraw Egypt’s social contract in a way that is both politically acceptable at home and can command the strong support of the rest of the world. Central to the plan is the development of a bridge to a new system that better targets subsidies while providing a safety net for those who no longer qualify for subsidized goods and one that establishes a transparent and regular mechanism of price and subsidy changes, thus reducing their political toxicity. This means that foreign donors will need to accept a slower reduction in subsidies than under a conventional IMF program in order to increase the likelihood that Egyptians can make headway on reforms in a coordinated and more coherent manner.

Conclusion

Egypt is perilously close to becoming insolvent. Despite Gulf assistance, the combination of the country’s economic needs, the legacies of Cairo’s incoherent economic policies of the past along with their continuation today, the political challenges to economic reform, and the potential for exogenous economic shocks all make a solvency crisis a significant possibility. The United States and its allies in the Persian Gulf, Europe, and Asia should be prepared for this outcome. Increased attention to this issue among policymakers and plans to prevent or mitigate the consequences of Egypt’s default are focused principally on infusions of additional aid. This will certainly help Egypt to purchase food, fuel, and other critical goods, but external aid will not resolve the problem. At best, it will give Egyptian policymakers some breathing room and thus an opportunity to undertake economic reforms.t

Report

Report Report

Report Report

Report Report

Report Report

Report Report

Report