Fiscal Breakeven Oil Prices

Uses, Abuses, and Opportunities for Improvement

- Michael LeviDavid M. Rubenstein Senior Fellow for Energy and the Environment and Director of the Maurice R. Greenberg Center for Geoeconomic Studies

- Blake ClaytonAdjunct Fellow for Energy

Introduction

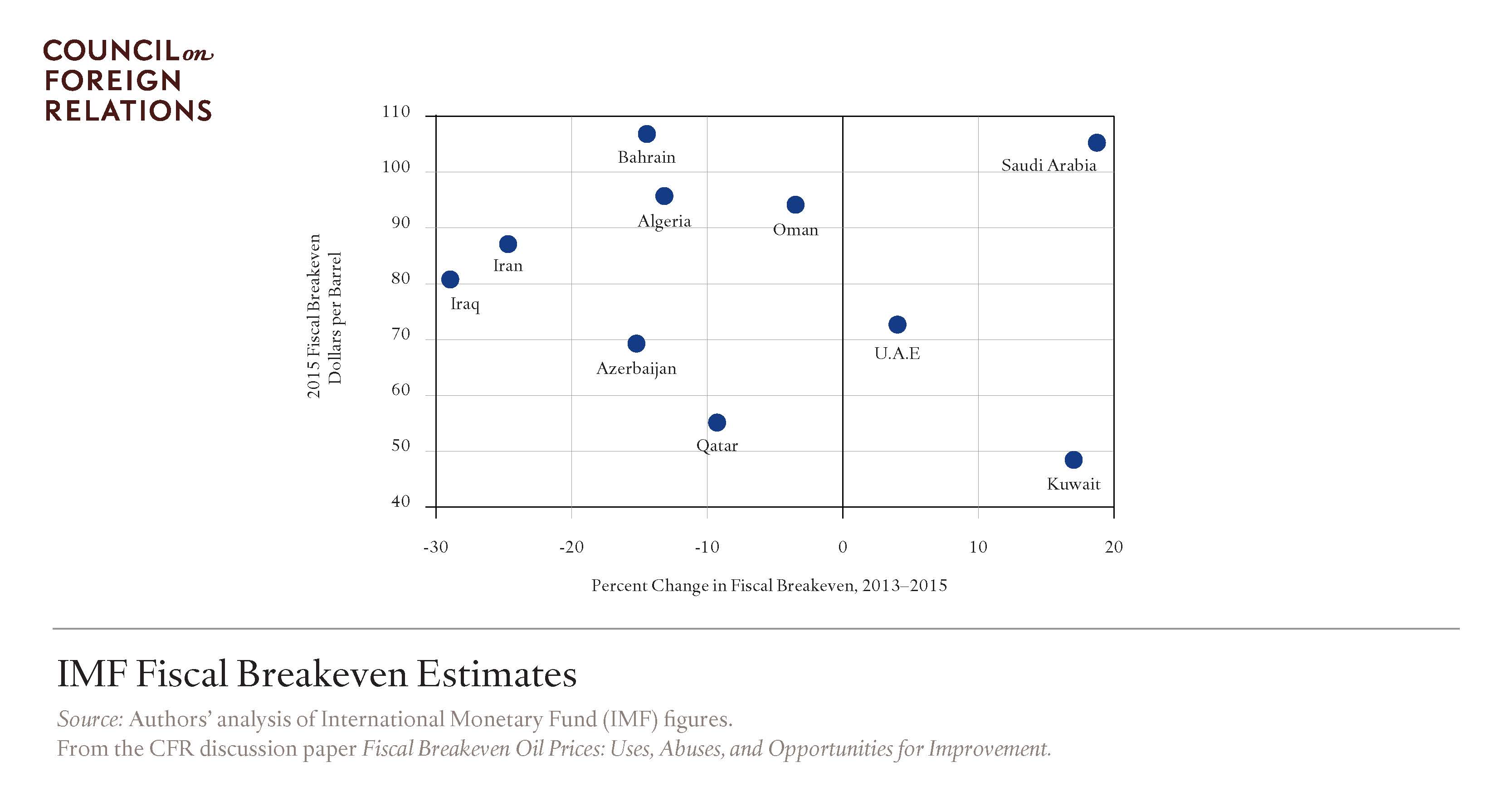

An oil-exporting country’s “fiscal breakeven” oil price is the minimum price per barrel that the country needs in order to meet its expected spending needs while balancing its budget (figure 1). Oil prices below this level should result in budget deficits unless government policies change. Breakeven prices have become popular among analysts and decision-makers in public and private sectors as indicators of oil-producing countries’ economic and political stability and as ingredients in oil price forecasts. In recent years, for example, analysis based on fiscal breakeven prices was used to forecast instability in Russia and Iran, and—driven by an assumption that Saudi Arabia would cut its production in order to prevent prices from falling below its fiscal breakeven—to predict that oil prices would never fall far below one hundred dollars a barrel.

A government in deficit can face pressure to raise revenues, cut spending, or default, each with broader fallout.

There are, however, sharp limits to the insights that fiscal breakeven prices provide, and dangers in relying on them narrowly. Based on a review of public discussions around breakevens, interviews with officials in the U.S. government and international institutions, and an examination of methodologies used to estimate breakeven figures, the CFR Discussion Paper “Fiscal Breakeven Oil Prices: Uses, Abuses, and Opportunities for Improvement” assesses the potential value and most important pitfalls involved in using fiscal breakeven oil prices. It also reviews the track record of the International Monetary Fund (IMF)—the source of the most widely used fiscal breakeven price figures—in estimating fiscal breakeven prices and recommends improvements for them and for all analysts who produce breakeven figures.

Figure 1.

Potential and Pitfalls

Knowing a country’s fiscal breakeven price can be useful to geopolitical and market analysts and to policymakers trying to shape oil-exporting countries’ behavior. Breakeven prices can provide:

Political insight. Breakeven prices can provide a window into the demands facing decision-makers in oil-producing countries. A government in deficit can face pressure to raise revenues, cut spending, or default, each with broader fallout. Moving from surplus to deficit is also politically undesirable if it provides ammunition for domestic political opponents or signals weakness to geopolitical rivals even if it doesn’t result in economic crisis.

Oil market insight. Fiscal breakeven prices can reveal pressures that shape oil-production decisions. One popular model of oil-exporter behavior imagines that oil producers are inclined to keep production levels unchanged as long as prices are sufficient to meet their budgetary obligations. This implies that an oil-exporting country’s production policies could undergo sharp and surprising changes as oil prices cross a country’s fiscal breakeven level.

Oil exporters have proven resilient to sub-breakeven oil prices.

Help communicating the need for fiscal reform. Interviews with officials suggest that, because breakevens link neatly with real-world oil prices and provide an intuitive sense of available fiscal space, they can help interested parties (inside and outside the government in question) press for economically valuable fiscal reform.

With the simplicity of fiscal breakeven figures, however, comes significant limits. Most of the officials interviewed for the paper expressed skepticism about using fiscal breakeven price estimates as strong indicators of fiscal, social, or political stability, but simultaneously warned that others were abusing them. Errors include:

Overconfident geopolitical risk predictions. National security analysts and well-respected media outlets frequently use fiscal breakeven prices as thresholds for political stability, warning that sub-breakeven oil prices sharply increase a country’s risk of social unrest or other geopolitical fallout. Oil exporters have, however, proven resilient to sub-breakeven oil prices. They often have substantial savings, and they often can adapt.

Overconfident predictions of future oil prices. Prior to the collapse of oil prices, many oil market analysts predicted that breakeven prices would act as a price floor, forcing producers to curtail production and keep prices high. These predictions were wrong. Fiscal breakeven prices also are not a floor on long-term oil prices.

IMF Breakeven Price Estimates

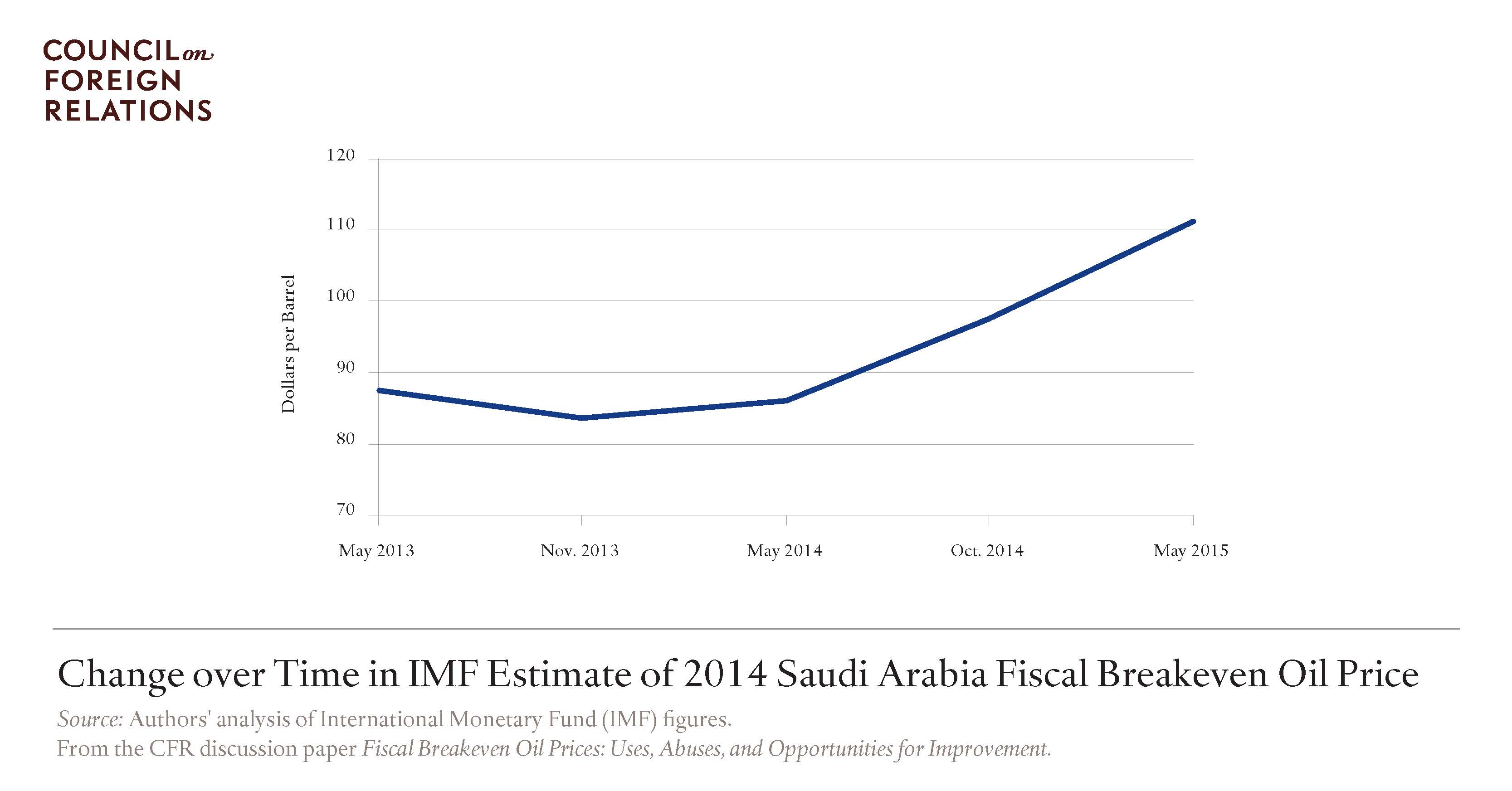

Analyzing the widely used fiscal breakeven figures produced by the IMF provides insight into the reliability of fiscal breakeven prices, and areas for improvement. The paper examines all IMF fiscal breakeven estimates published since 2008. It finds that IMF estimates of fiscal breakeven prices for a given year vary considerably over time (estimates for any one year can be revisited four or more times over the span of two or more years). In recent years, estimated breakeven prices for a given country and year regularly varied by more than 20 percent as the IMF updated its estimates (figure 2). Factors driving variation in breakeven price estimates include changes in expected oil production and exports, inaccurate projections of government spending, exchange-rate changes, inaccurate projections of non-oil tax revenues and other revenue sources, and analyst discretion.

Figure 2.

Recommendations for Improving Breakeven Analysis

In light of the popularity of breakeven analysis and its attendant hazards, the paper offers several strategies for improving breakevens’ analytical value, which include the following, in addition to others detailed in the full text:

Improve model transparency. The formulas behind breakeven price estimates are often considered proprietary. This opacity limits analysts’ understanding of what fiscal breakeven prices represent and impedes scrutiny that could further refine models. There are ways to improve transparency while safeguarding private information.

Explain revisions to breakeven estimates. Institutions that publish recurring breakeven estimates do not typically discuss the rationale behind changes. Explaining changes in the figures would provide an opportunity to improve transparency and illustrate the relationship between macroeconomic trends and changing breakeven prices.

Acknowledge uncertainty. Producers of breakeven figures should augment breakeven price estimates with uncertainty bands and sensitivity analyses, demonstrating to users that the figures are not intended to be interpreted as precise, and providing greater insight into the most important drivers of their estimates.

Account for additional variables. Many breakeven estimates would benefit from increased consideration of non-macroeconomic and second-order variables that can influence breakeven prices, such as the performance of state-owned enterprises and returns from sovereign wealth funds.

Increase focus on sovereign debt sustainability. Analysts would be wise to bolster breakeven analysis with the use of other, more comprehensive analytical tools such as the IMF’s Debt Sustainability Analyses (DSAs). Along these same lines, the IMF should also conduct more regular DSAs of major oil exporters, focusing on oil shocks.t

Report

Report Report

Report Report

Report Report

Report Report

Report Report

Report