Global Economics Monthly: May 2016

Venezuela’s Descent Into Crisis

- Robert KahnSteven A. Tananbaum Senior Fellow for International Economics

Bottom Line: The crisis in Venezuela continues to escalate, with no recovery or relief in sight. A messy and chaotic default looms, and the rescue will likely involve a tough adjustment program, large-scale financing from international policymakers, and deep sacrifices from Venezuela’s creditors and, most of all, the Venezuelan people. China’s role, as Venezuela’s largest creditor, will be critical and precedential for other emerging market commodity exporters with too much debt.

The economic and political disintegration of Venezuela has reached a critical moment. Economic activity is falling sharply and the seeds of hyperinflation have been planted, a downward spiral reinforced by political paralysis, widespread electricity shortages, and a breakdown in social order. Reserves are falling sharply, driven by capital flight and a fiscal deficit that has swelled to over 20 percent of gross domestic product (GDP). Although the government has made enormous efforts to continue making debt payments, a default now appears likely sooner rather than later, and possibly even ahead of large debt service payments due this fall (see figure 1).

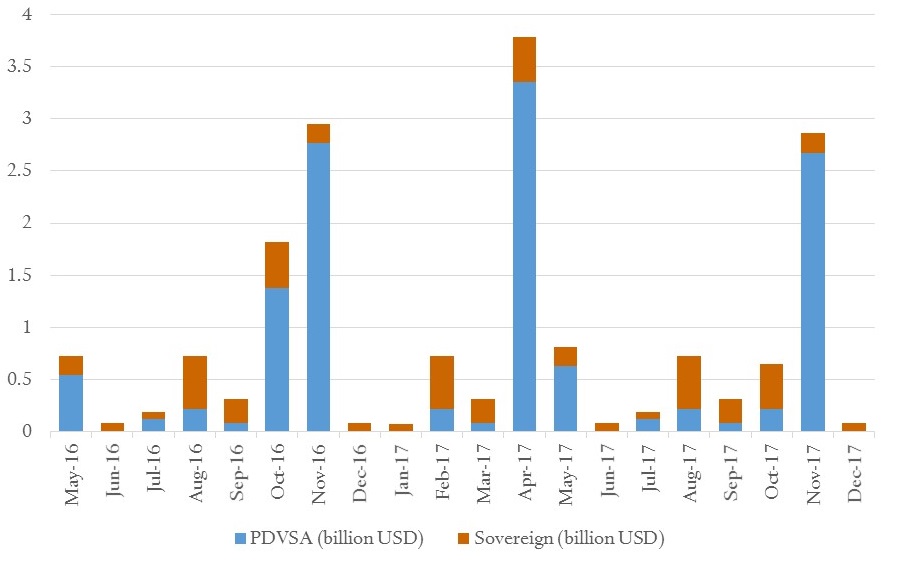

FIGURE 1. VENEZUELA’S BOND AMORTIZATION SCHEDULE (2016–2017)

A great deal of uncertainty lies ahead, but four things can be said with some confidence, courtesy of Game of Thrones.

Winter Is Coming

While the domestic economic and political crises have worsened, the Venezuelan government has made an impressive effort to delay default, running down reserves to $12.7 billion (not all usable) from nearly $20 billion a year ago, selling assets (often for pennies on face value), and running arrears to suppliers. In part, these actions may reflect the view that default could be politically devastating for a government already losing authority; in part, it is a gamble for resurrection should oil prices recover dramatically. But such delaying tactics come at a high cost: extending policies that are disruptive and clearly unsustainable are resulting in social and economic distress. The government has reaffirmed its commitment to pay but the numbers simply do not add up. As my son once told me, “Math is hard.”

Market optimism is misguided, and the coming default will be chaotic and disruptive.

Many Venezuelan analysts still see room for a smooth transition away from the Maduro government, perhaps to one based on national unity, and for a recovery in the economy that might require some refinancing of the debt but not a default. Indeed, a recent investor survey by JPMorgan found more than 50 percent of investors expecting no restructuring and a continued muddling through this year; only 15 percent foresaw a disruptive default and deep haircut. I find such optimism misguided. Indeed, if the history of emerging market crises is a guide, the coming default—whether this year or next—will be chaotic and disruptive.

In October, the state-owned oil company PDVSA faces a $1.3 billion debt repayment (including $1 billion in principal). In November, additional interest payments totaling $2.9 billion are due (although some of this debt may already have been bought back by the government). Add in payments to China and arrears to suppliers, and a financing gap in excess of $20 billion is possible for this year. The outlook for 2017, when more large debt payments are due, is no better. The timing of default is difficult to predict, as the government will likely continue to seek delaying the inevitable. But economist Rudi Dornbusch’s injunction was never more relevant: “The crisis takes a much longer time coming than you think, and then it happens much faster than you would have thought.” That’s exactly the Venezuelan story. It will take forever and then it will happen overnight.

Chaos Isn’t a Pit. Chaos Is a Ladder.

Absent a change in government, an IMF rescue program is unlikely.

The current government in Venezuela has signaled strongly that it is uninterested in working with international policymakers on a rescue program, and these policymakers have returned the favor. Absent a dramatic change in the political environment, there would need to be a change in government, and a green light from the United States, before officials from the International Monetary Fund (IMF) would board a plane to Caracas to begin negotiations on a rescue program. By then, the chaos could be severe.

The IMF also will have a lot of catching up to do: the Fund’s last comprehensive review of the Venezuelan economy was in 2004, and its last visit in 2007. Its assessment, and the financing gap that will need to be filled, will be a moving target at a time when international pressure to get a program going and money flowing will be intense. Still, the economic building blocks of a rescue program that the international policymakers would back are not hard to imagine. They include a float and unification of the exchange rate, as there will not be adequate reserves to allow intervention, and an extended period of capital controls to stem flight; a multistep increase in domestic energy price to world prices, allowing prices to be flexible going forward in response to market developments; a tighter fiscal policy consistent with available resources; a targeted safety net, replacing the pervasive and inefficient subsidies now in the system; a comprehensive restructuring of the banking system, which is likely to be quite costly given reports of deep-seated corruption; and broad measures to address corruption and rule of law.

This is a conventional economic program, similar in many respects to the Ukraine 2014 reform effort. As illustrated by the experiences of other countries in deep crisis and attempting similar IMF-backed adjustment efforts, the external accounts are likely to improve quite sharply following a large devaluation, but returning to growth requires an extended period for economic stabilization and the rule of law to take hold and create conditions for effective new investment. This suggests that the large oil reserves, while critical to Venezuela’s long-run future, are unlikely to be a major support for the economy in the early months of a crisis stabalization effort (especially given the extent to which the current government has undermined the efficiency of PDVSA). But oil in the ground would provide the basis for an optimistic future once a root-and-branch reform of the old system has been undertaken.

The Man Who Passes the Sentence Should Swing the Sword

The sentence, in this case, refers to the fate of private debt. The IMF will pass the sentence (and swing the sword) on whether there should be a restructuring. It is too early to be definitive, as the IMF will respond to events when they arrive. Further, new IMF lending rules passed in December 2015 (for private restructuring) and January 2016 (for arrears to governments) create a great deal of flexibility around restructuring terms and conditions when in the gray zone (IMF jargon for large lending programs where substantial uncertainty exists). But a few things seem clear.

First, the debt will look unsustainable, given current market conditions, when the Fund does its analysis. In the middle of a crisis, the exchange rate will likely overdepreciate compared to its long-run value, but the Fund will have a hard time forecasting with confidence if and when it will rebound. As in Ukraine, that will make the debt (much of which is denominated in dollars) look large, by some estimates as much as 125 percent of GDP. Second, a critical focus for the IMF will be cash flow and the adequacy of financing for the program. Venezuela has a small IMF quota (around $5.3 billion), and the Fund’s rules governing “exceptional access” (above what the normal quota-based limits allow) require a higher standard of confidence in the program. Although resuming its relationship with the IMF would also open World Bank and Inter-American Development Bank support, this looks unlikely to be enough to meet financing needs or provide a high standard of confidence. Most likely, in my view, these considerations will push the IMF to take a cautious approach to its own lending and seek a deep restructuring with material cash-flow relief.

The Iron Bank Will Have Its Due

China’s role in Venezuela’s debt restructuring will be critical and precedential.

Ultimately, any debt workout is likely to involve a substantial reduction in value (measured in net present value) of the debt. The timing and extent of that reduction will depend predominantly on the role taken by Venezuela’s largest official creditor. China has extended nearly $60 billion in loans over the last ten years, mostly backed by oil, and although the facilities offer little transparency, Venezuela is estimated to owe roughly $7 billion in 2016 on a total debt of around $30 billion. China has reportedly already provided material cash-flow relief to Venezuela, but would need to be a part of any debt restructuring effort both because its claim is so large and because private creditors would want China to share the burden if asked to restructure.

However, Beijing is unlikely to provide easy concessions to a new government, due to concerns over the credibility of the adjustment effort and the risk to its balance sheet at a time of increased debate at home over the quality of its overseas investments. In a blog post, I argued that restructuring the Chinese debt owed by Venezuela is best done by China joining the Paris Club of official creditors, and agreeing to restructure on comparable terms to other official creditors. But short of such a decision, China could still participate in a financing package in parallel to other creditors. Whatever China decides in Venezuela will likely set a precedent for other countries that owe China much debt and have been battered by low commodity prices and slow global growth—countries that will seek restructurings in coming years. The decisions made in this case will be consequential.

Conclusion

Markets are too sanguine about the risk of a disruptive default in Venezuela. If it happens, the IMF will need to move quickly to assemble a comprehensive financing package. China’s support for that package, and any related debt restructuring, will be critically important for the package to be credible and to provide appropriate incentives for participation by other creditors.

Looking Ahead: Kahn’s take on the news on the horizon

Puerto Rico

The Government Development Bank for Puerto Rico declared a moratorium on most of its $422 million debt payment, which was due on May 2. To date, the negotiation between Puerto Rico and creditors has made limited progress, while slow action from the U.S. Congress is delaying a comprehensive plan to restructure the island’s debt. The debt crisis could deepen as the next big payment of $2 billion comes due in July.

Saudi Arabia

The Saudi government unveiled its reform program Vision 2030, including partial privatization of the state oil company and restructuring of its sovereign wealth fund. Persistently low oil prices and widening fiscal deficit provide political momentum for reform, but political hurdles appear high.

Argentina

After fifteen year of isolation, Argentina returned to international capital market with its triumphant issuance of $16.5 billion in sovereign bonds. JPMorgan estimates that Argentina could issue $30 billion of debt this year, including instruments of provincial governments and the corporate sector. The country could return to growth (2.8 percent) in 2017.t

Report

Report Report

Report Report

Report Report

Report Report

Report Report

Report