Rebuilding Ukraine

Priorities and Strategies

Overview

To rebuild Ukraine’s economy successfully, argue the authors, policymakers should help facilitate the return of Ukrainian workers and private investment by developing a long-term recovery strategy.

- Charles BeckerResearch Professor of Economics, Duke University

- Peter DevineAssistant Professor of Practice, Department of Economics, Boston College

- Aaron LamUndergraduate Research Assistant and Mentor, Duke University

- Michelle SchultzeUndergraduate Research Assistant, Duke University

- Eva SpektorovUndergraduate Research Assistant, Duke University

This report is part of the Council Special Initiative on Securing Ukraine’s Future.

Executive Summary

Ukraine’s long-term stability and security depend on its ability to recover economically. While Western policymakers have prioritized military aid and large capital transfers, these alone will not rebuild Ukraine’s economy. A successful recovery requires specific actions that will alter the trajectory of Ukraine’s labor force, attract private investment to ease the burden on public finances, and provide long-term economic stability. Without those, Ukraine’s economy will stagnate and be significantly more vulnerable to Russian expansionism in the future.

Ukraine faces three major challenges that threaten its economic recovery. First, Russia’s invasion dramatically accelerated the decline of Ukraine’s labor force, which has been shrinking since the Soviet dissolution. The loss of nearly a third of its population to displacement and emigration, when added to the loss of workers who were taken from productive economic activities and sent to the front, threatens the country’s long-term economic growth more than any other factor. Without targeted incentives for return, Ukraine’s workforce will remain stunted, permanently weakening its economy. Second, low private investment and structural weaknesses will raise the burden on Ukraine’s public finances. Ukraine historically has struggled to attract foreign direct investment, and war-related uncertainty has further deterred investors. Third, current Western strategies are blind to both those vulnerabilities, but especially the mission-critical need to reverse Ukraine’s population decline. So far, other than considerations for rebuilding infrastructure and demining, Western planning for Ukraine’s recovery has been negligently deferred until after the war. Ukraine and its supporters should take the following steps to strengthen the country’s postwar economic outlook:

In short, Ukraine is in a highly stressed position, but there is some bright economic news. The challenge facing its international supporters is to build on those positives to sustain long-run economic growth.

- European Union (EU) nations should ensure that workers returning to Ukraine retain pension entitlements earned elsewhere and gain credit toward residency rights in supporting EU countries based on work in Ukraine.

- Ukraine, the EU, and other supporting nations should provide transitional housing, health care, and education for the families of returning workers and offer returning refugees short-term financial support to ease reintegration.

- Ukraine’s supporters should expand the underwriting of private investments while Ukraine should strengthen anti-corruption measures by funding independent watchdog organizations and increasing defined public financial transparency mechanisms.

- The EU and the United States should formalize support for a currency board backed by international reserves to stabilize its currency and build investor confidence.

- Ukraine should reopen a commercial airport, such as in Lviv, to facilitate business travel and investment inflows.

Implementing those policies would reduce Ukraine’s dependence on aid, enhance regional stability, and create a stronger, self-sufficient economy and defense capability. Failing to make those or similar changes would swiftly risk entrenching Ukraine’s economic decline and undermining its postwar recovery.

Introduction

The Donald Trump administration has stated that it plans to quickly negotiate an end to the war in Ukraine. While the feasibility of this goal is still unclear, Western policymakers should accelerate their planning and ability to execute a recovery strategy when hostilities sufficiently decline.

A stable, growing, and self-reliant Ukraine would be a significant strategic win for the United States. Incorporating Ukraine’s front-line experience in modern warfare tactics and technologies into the Western alliance, as well as its defense and cyber industries, would directly deter Russian aggression and give pause to expansionist regimes globally. Furthermore, the cost of recovering Ukraine is a small fraction of the broad fiscal liabilities the United States and the NATO alliance more broadly will face if Ukraine fails to rebuild sufficiently for long-term security. Therefore, designing a recovery strategy to achieve this strategic win—a thriving Ukraine—should be a high priority. This strategy needs to account for Ukraine’s needs, the timelines those needs must be met by to avoid a cascading failure, and the changing political climates those policies need to withstand in the West.

Ukraine’s economic recovery is far from straightforward. Policymakers will have to grapple with specific questions—such as whether a particular road should be rebuilt while there is still fighting or after a peace agreement—and broader, structural decisions—such as which industries should be Ukraine’s new economic drivers. All are important. Within this spectrum, however, one question stands out as a true lynchpin: how to restore Ukraine’s decimated labor force. If Ukraine does not increase its labor force within a few years, nearly every other economic effort will be rendered moot. This critical concern has been virtually unacknowledged by Ukraine’s allies. This lack of attention needs to be corrected. A multinational population return plan should be developed now to be implemented as soon as conditions allow, so that Ukraine does not miss its vanishingly small window to stabilize and grow.

The United States is not adequately preparing for Ukraine’s economic recovery. The U.S. security apparatus argues that any economic recovery needs basic security guarantees as a precondition. Therefore, they argue, as long as hostilities are ongoing, the United States’ efforts should focus on security. Meanwhile, although the Treasury Department has the analytical ability and international economics expertise, it is bogged down in making sure Ukraine’s balance of payments regularly clears (i.e., the Treasury Department is coordinating financial aid, exchange rate management, debt restructuring, export financing, and the enforcement of Russian sanctions to guarantee Ukraine’s government can cover essential expenses without resorting to hyper-inflating money printing). Both efforts are critical, but when the defense half of Washington is focused on immediate battlefield needs and the economic half is stuck in short-term economic firefighting, no one is left to plan a long-term recovery strategy.

The Western alliance cannot move Ukraine away from Russia’s border. So, Ukraine’s best chance for long-term security is to grow its economy at a rate that outpaces Russia’s, especially given how much Ukraine lags behind Russia in per capita income. This approach would allow Ukraine to maximize its ability to withstand a future invasion with its returned population and accelerated productive capacity. Rapid growth will not happen passively, however: a strategy is needed to achieve it. While Ukraine itself has made major structural reforms and slowly developed a recovery strategy, its international supporters have done little.

Western policymakers are making three mistakes that, unless corrected, will doom Ukraine’s chance of long-term growth and a more stable security environment. First, they assume that a large capital transfer on its own will be sufficient, without understanding Ukraine’s needs. Second, they are modeling Ukraine’s labor and capital return levels as exogenous, or predetermined, rather than objectives that can be achieved through planning. Third, they are content to wait for peace before developing a recovery strategy.

The U.S. government has left it up to the World Bank and the International Monetary Fund (IMF) to model Ukraine’s wartime economy, showing how much output has fallen and how much capital and total factor productivity need to increase to recover to prewar trends. The World Bank estimates that the cost of damage and reconstruction in Ukraine is $486 billion over 10 years—almost 2.5 times Ukraine’s pre-invasion gross domestic product (GDP). That calculation is the product of careful work, but the United States and other supporters have taken that number to mean far more than it does. This estimate includes the replacement costs for physical damage and lost output due to the war, as well as factoring in a green transition, and does not reflect the changes and new inputs Ukraine needs to reverse its economic future. Worst of all, the high sticker price allows policymakers to incorrectly assume that simply achieving that level of capital will recover Ukraine’s economy. In reality, Ukraine needs precise inputs and conditions in place for its economy to take off. Without them, simply wiring a large check to the central bank is dangerous and even counterproductive.

The U.S. government’s current economic strategy is implicitly taking the basic inputs of Ukraine’s postwar economy (labor and capital) as exogenous parameters when, in reality, they need to be strategically developed and achieved. The U.S. Treasury Department uses the IMF’s macroeconomic model of Ukraine. The IMF model is a solid contribution and shows the potential growth outcomes Ukraine could achieve if different population return and private capital flows were to happen. But the model takes these as exogenously determined, static parameters (high, medium, or low values). While a model can do that, governments planning Ukraine’s recovery cannot. Ukraine needs to achieve a high population return rate, and to a lesser extent high private capital investment. Any Ukrainian economic recovery strategy needs to specify how it will achieve the highest possible return rates for both population and private capital.

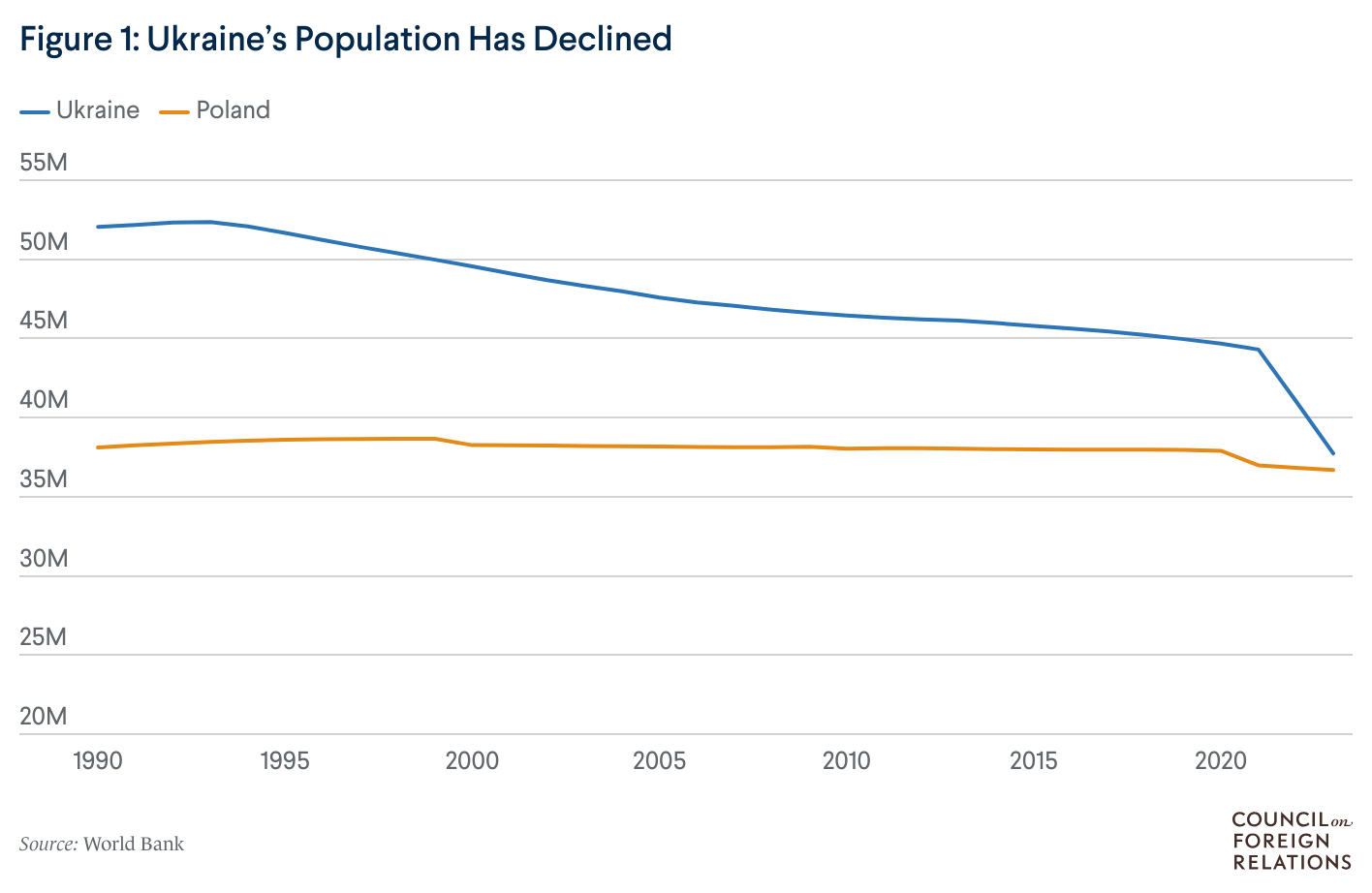

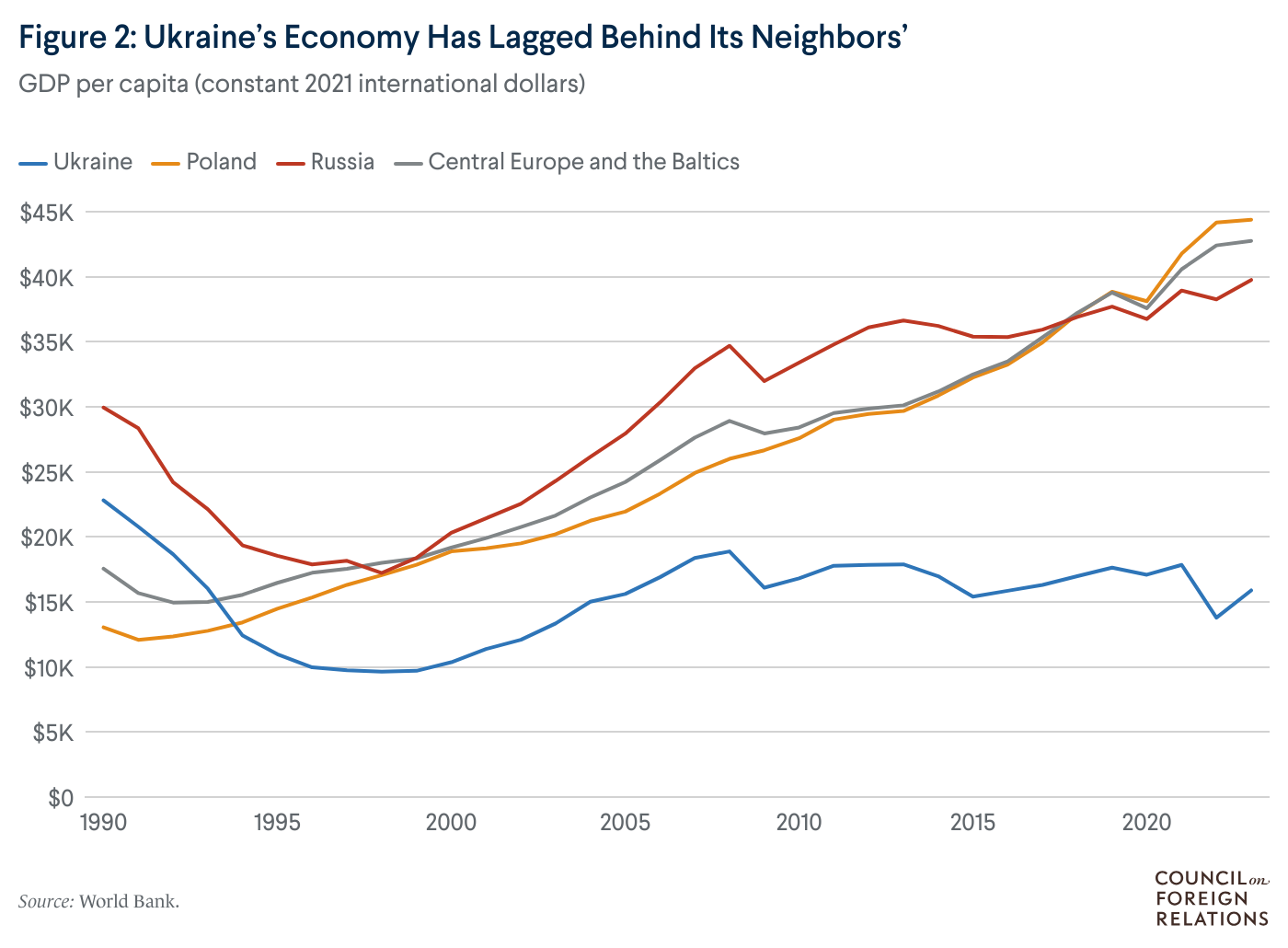

The window for Ukraine to achieve such an economic turnaround is small. Observations of post-conflict population loss in the Balkans indicate that Ukraine will only have a few years after the war to grow its labor force, secure private investment, and recover its economy before the situation deteriorates for the foreseeable future. Worse yet, Ukraine’s population has been in long-run decline since the fall of the Iron Curtain, which has played a role in stagnating its economy ever since. (See figures 1 and 2.) Waiting until hostilities end and then hoping for Ukraine’s economy to miraculously grow without the necessary inputs in place is not a viable plan. The United States and EU need to have a strategy prepared ahead of implementation.

There is a silver lining. Refugee repatriation is an area where good policy is also good politics. The United States and some parts of the European Union have the political will to encourage refugee return. Policies encouraging repatriation will help make Ukraine economically self-sufficient and keep upfront costs low for supporting nations. Ultimately, addressing Ukraine’s population and labor force are necessary to turn Ukraine into a net-contributing member to the Western alliance, a desire of the Trump administration.

The economic problems facing Ukraine during the war and after the cessation of hostilities are manifold. Any recovery strategy needs to create incentives to restore Ukraine’s labor force. Those incentives cannot be developed by the Ukrainian government in isolation. Rather, an effective program will require a series of parallel steps by Ukraine’s international partners. If Ukraine is to maximize its chances of economic recovery and long-term security, time is of the essence.

The Challenges Facing Ukraine

Ukraine was a sick man of the former Soviet states well before the invasion. Prior to February 2022, Ukraine had low levels of both domestic and foreign direct investment (FDI) relative to economically comparable countries such as Poland and Turkey.1

A litany of problems, including corruption, state interference, insecure property rights, distance from markets, infrastructure gaps, deterred those with limited appetite for risk. So did the country’s proximity to Russia. (To paraphrase the nineteenth-century Mexican dictator Porfirio Diaz, “Poor Ukraine—so far from God, so close to Russia.”) Russia’s seizure of heavy industrial areas in or near the Donbas has been a further, crippling blow.

For the past fifteen years, Ukraine has had poor-to-disastrous economic growth, overall investment, and FDI rates. It is difficult to imagine a sustained economic recovery without increases in both domestic investment and foreign capital inflows.

After a crippling decline in real GDP per capita of more than 50 percent between 1990 and 1998, significant recovery followed until the 2008 global financial crisis, after which stagnation ensued. Despite considerable success in exports, Ukraine has yet to return to Soviet-level real per capita incomes. In contrast, while Poland, Kazakhstan, and Belarus were all poorer than Ukraine in 1990, by 2023, Poland was a high-income economy, Kazakhstan nearly so, and Belarus an upper-middle income economy.

Ukraine’s FDI-to-GDP ratio from 1995 to 2022 has underperformed peers: its 2.96 percent average over the twenty-eight-year period trails the ratios for Hungary (13.9 percent), Georgia (8.1 percent), Kazakhstan (6.7 percent), Moldova (4.7 percent), Armenia (4.6 percent), Poland (3.5 percent), and Slovakia (3.5 percent), exceeding only inward-looking Belarus (2.2 percent) and Uzbekistan (1.6 percent). Domestic investment rates are also low, held back by a stunted banking system and nearly nonexistent stock market.2

Ukraine’s policy responses since early 2022 have moved in the right direction, but war-related destruction and uncertainty will deter prospective investors for years to come. Corruption has been reduced markedly despite the war (which itself offers an invitation to theft), and public policies have become more investor friendly. However, Ukrainian government efforts alone will not suffice to attract international investment. Supporter nations will have to boost Ukraine’s economic recovery by encouraging private investment.

Ukraine’s capital needs are better understood than its labor shortage, which is the more significant threat to its economic recovery. Refugee repatriation is particularly important given Ukraine’s prewar population trends. Even before the 2022 invasion, Ukraine suffered from higher mortality and lower birth rates than its neighbors, with the birth rate below replacement levels. Some of those trends are structural in the near term: given the 1990s post-Soviet collapse in fertility, new generations entering the labor force in recent years have been unusually small, which in turn impacts new births, perpetuating the cycle. In essence, Ukraine is experiencing a demographic echo effect that was evident even before the invasion. Recent forecasts indicate a further decline in population to as little as thirty million by 2035, leading to panicked media stories about catastrophic labor force levels.3

Compounding the demographic crunch, the UN High Commissioner for Refugees estimates that there were 6.48 million external refugees from Ukraine as of mid-May 2024, and the UN’s International Organization for Migration estimates 3.31 million internally displaced persons in Ukraine as of June 2024. The Russian invasions of 2014 and, especially, 2022 substantially disrupted the remaining labor force and employment.

There is empirical evidence that returning refugees will be essential to Ukraine’s economic recovery. Estimates of the impact of refugees returning to the former Yugoslavia from Germany after the civil wars in the 1990s indicate a large positive effect on exports at the sectoral level and in the growth rate of those exports. In addition to increasing labor supply, returning refugees also transfer “knowledge, technologies, and best practices.”4

While studies of recovery in post-war Bosnia and Herzegovina indicate that most people do return, population and labor force remain a problem nearly three decades later. Young, educated Bosnians are far more likely to emigrate even today than other Bosnians, leading to an ongoing skill deficit.5 Emigration rates from Bosnia have actually increased since 2010, and by 2017, the Bosnian diaspora equaled 44.5 percent of the domestic population. A 2019 survey indicated that 35 percent of Bosnian residents had aspirations for permanent emigration. The lesson for Ukraine is that only a short window exists to bring about an economic recovery before postwar population loss sets into a vicious cycle.

Moreover, permanent population flight following a war or disaster can have compounding effects, depressing future investment demand as well as curtailing the effective use of aid earmarked for recovery. The experience of Puerto Rico following Hurricane Maria in 2017 is instructive: population loss prevented the local economy from absorbing capital transfers, thereby stunting recovery efforts. And as Jocelyn West from the University of Colorado has found, Puerto Rico’s permanent population loss was greatest in the most socially vulnerable population tracts.6

By 2023, Ukraine’s population had already declined by 20 percent since independence from the Soviet Union, to a level just under thirty-eight million; further declines are on the horizon even if the war were to end today.7 Failing to reverse this demographic trend could render all other economic recovery efforts moot, as Ukraine would not have enough economic activity left to absorb capital transfers.

Ukraine’s Wartime Economy

Despite the crushing effect of the war, Ukraine’s labor market in much of the country is surprisingly vibrant. Wages are stable or rising, and labor demand in much of the country is rising. Ukraine has moved from being a diversified emerging-market economy with strong transportation and agriculture bases to a wartime economy producing for its immediate, rather than long-term, needs. The change in demand structure is even more drastic for cities near the front line. However, wages in major refugee destination countries are far higher than in Ukraine, discouraging population return.

Natalia Zaika and Volodymyr Vakhitov at the American University Kyiv surveyed Ukrainians living in Poland (mainly refugees) and found that only about half of those who were refugees (and one-third of prewar migrants) intend to return to Ukraine. Reluctance to return is especially great among younger refugees.8 Moreover, some 74 percent of refugee respondents were women, reflecting both the inevitable gender imbalance in a setting where men are prohibited from leaving the country and the likelihood that more skilled male workers have settled further abroad.

Studies published by the Center for Economic and Policy Research and Zaporizhzhia National University show detailed evidence that the Ukrainian labor market was faring poorly before 2022, and that it worsened with the COVID-19 pandemic and subsequent Russian invasion.9 Specifically, those studies found the following:

- The number of officially registered job vacancies plummeted from 1,200,000 in 2019 to 800,000 in 2020, 400,000 in 2022, and about 350,000 in 2023.[10]

- The number of registered job seekers rose from 1,000,000 in 2019 to 1,200,000 in 2020–21 before falling below 900,000 in 2022 and below 500,000 in 2023.[11]

- Ukraine’s labor market never had a good year. Even before COVID-19 and the 2022 invasion, unemployment rates bounced between roughly 8 percent to over 10 percent, and were highest in industrial and less skill-intensive services.[12]

- Labor force participation rates have been low by global standards since the Soviet era, and, of course, were worsened by COVID-19, especially for women and those in unskilled services and the informal sector.[13]

- The war brought a further decline in labor demand, but emigration flows and the expansion of the Ukrainian military were even greater. It appears that large numbers have left the labor force, and for many, this will be a permanent departure.[14]

Furthermore, a review of state labor force data suggests that there is a much greater relative demand for skilled labor than unskilled labor.15 This is problematic for Ukraine because skilled jobs command a lower wage premium.16 That is, a skilled worker in Ukraine—say, a software coder—will be paid more than an unskilled manual laborer, but the difference in their wages will be less than in a country such as Germany, where skilled workers make even more. As such, Ukraine is in a difficult position: its economy needs skilled workers, but those skilled workers can get a better deal living abroad.

Firm-level employment offerings and job search data from Work.ua, the webpage for the government’s employment agency, currently lists roughly 93,000 job offerings, along with resumes for a comparable number of job seekers. However, these offerings and seekers do not balance by occupation, skill-level, or region. Additionally, online sites do not tend to cover agriculture, petty commerce, or informal sector jobs.

Job offerings crashed following the Russian invasion in February 2022 and remain far below baseline 2021 levels in eastern and southern cities, though the proportionate decline in Dnipro is surprisingly small. In contrast, job vacancies have grown in central regions such as Poltova and Cherkasy, and consistently in western Ukraine—especially in Lviv, where job vacancies have grown by nearly three thousand in the past three years. Salary movements are far more muted: areas of job loss have been accompanied by labor force shrinkage. In essence, both demand and supply curves have shifted back, so quantity falls, but wages remain stable.

The type of employment has also dramatically changed since the invasion, shifting to emphasize immediate needs like hospitals, services, and the defense industries. Surprisingly, information technology (IT) and tech have dropped along with durable goods. Figuring out why IT and tech, potentially powerful drivers of the future economy, are lagging is important for a complete strategy.

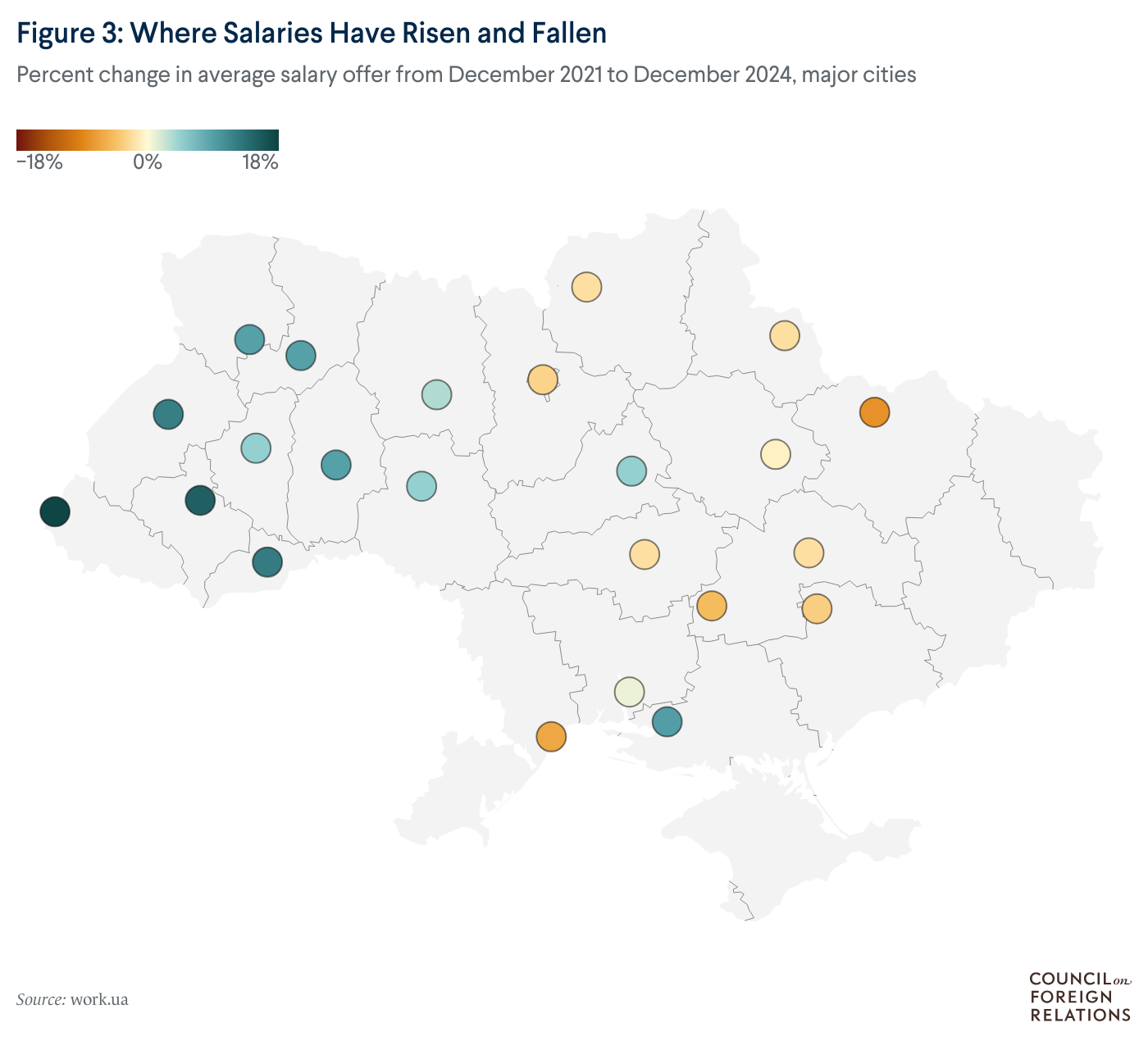

Figure 3 provides information on the change in mean values of employers’ monthly salary offers across cities from December 2021 to December 2024. Excluding Russian-occupied or threatened cities, December 2024 mean values range, in U.S. dollars, from $397 in Sumy to $625 in Kyiv.17

The Ukrainian economy is not collapsing, but it has shifted, and its labor and capital demands need to adjust accordingly. Indeed, 2022 was a tremendous negative shock, with the number of job offers collapsing and their mean offer wages falling roughly by 13 percent, but the recovery since late 2022 has been dramatic as well. This is especially true in Lviv, where offered wages in 2024 substantially exceed 2021 values in U.S. dollar terms. While offered wages in Kyiv and Odesa have not yet returned to 2021 levels, they have gone up. In contrast, wage offers in threatened Sumy in the northeast fell by 45 percent between June 2021 and 2022, and even as of June 2024 remain 12 percent below the 2021 levels.

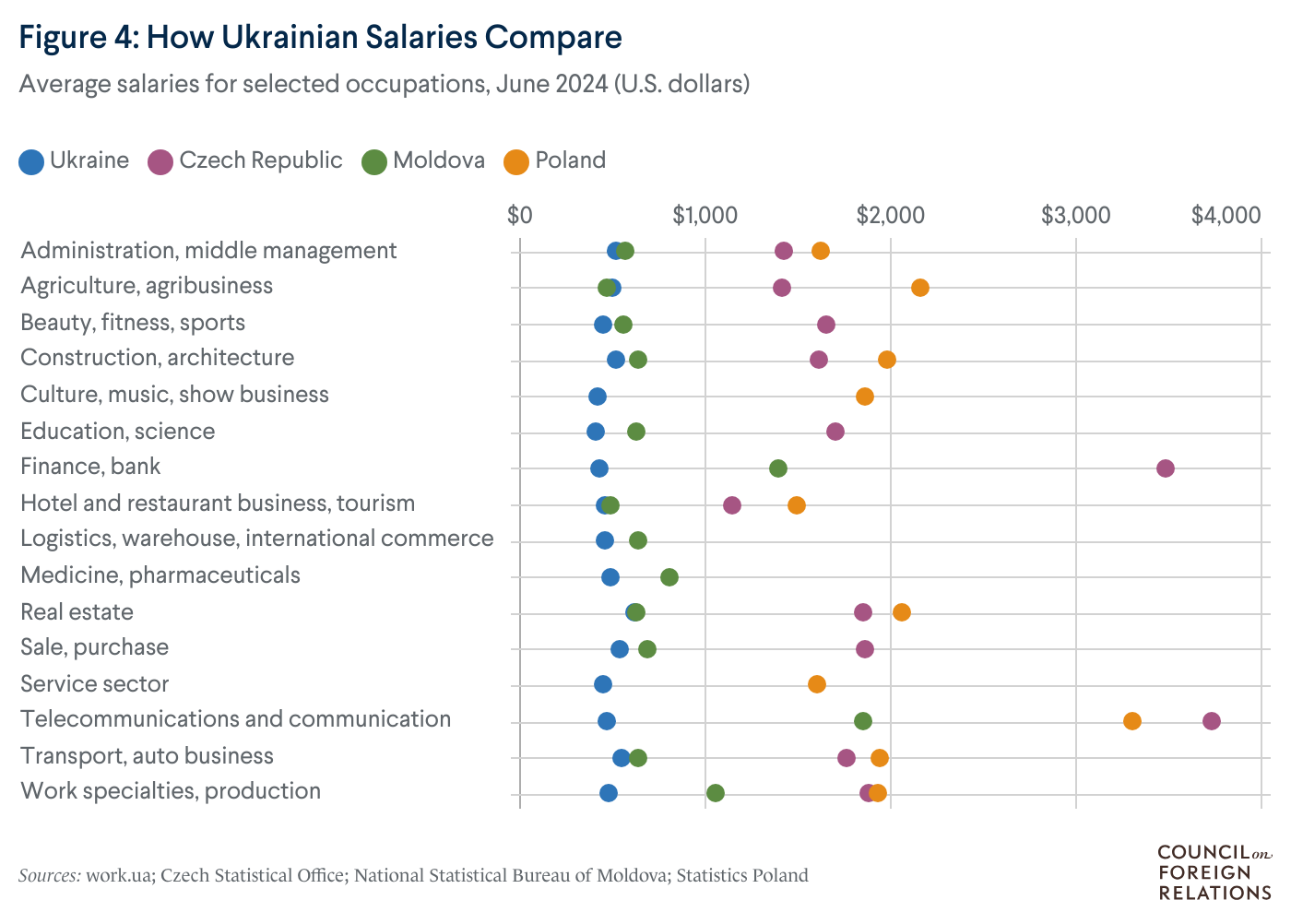

Challenges remain. Salaries are lower in Ukraine than in the European Union (EU), disincentivizing refugee return. A recovery strategy needs to first target refugees in low-wage countries, then shift to higher-wage countries as Ukraine’s economy gains steam and the wage gap closes. For example, U.S. dollar wages in Polish cities are roughly four times as high as for their Ukrainian counterparts. This pattern also holds by occupation (see figure 4), ranging from a dismal six-to-one pay ratio in telecommunications to a simply dispiriting three-to-one pay ratio in hotels and restaurants. Figure 4 also contrasts sectoral differences between Ukraine, Moldova, and the Czech Republic. (Note that not all occupations have values for each country.) Wages in the Czech Republic tend to be slightly below those in Poland but vastly exceed those in Ukraine. In contrast, Moldovan wages tend to be closer to those in Ukraine. Those premiums appear to rise with skill level. Given the greater language barrier for Ukrainians in Moldova (and Romania), as well as the much lower wage gaps, efforts to encourage repatriation should initially focus on these lower-wage countries, even though they only account for a small proportion of the refugee population.

On top of the wage gap, there are significant uncertainties caused by returning to a wartime nation. Compensating incentives will be important even after the fighting stops. To reiterate, Ukraine is very much a wartime economy, and long-term recovery will require major investments in manufacturing, IT, and capital goods sectors, as well as in infrastructure.

In short, Ukraine is in a highly stressed position, but there is some bright economic news. The challenge facing its international supporters is to build on those positives to sustain long-run economic growth.

Recommendations

Current nonmilitary support for Ukraine emphasizes temporary refugee status, large capital transfers aimed at recovery from war damage, and, ultimately, Russian reparations. Those measures are important but not sufficient for recovery: attracting inflows of new capital and the return of workers is necessary as well. Ukraine’s declining labor force and weak economic performance before the 2022 invasion exacerbated the effects of labor flight and low capital inflows and investment after the invasion, making reversal especially critical. The Ukrainian government itself has undertaken several critical reforms especially in anti-corruption and public transparency, making complementary moves by international supporters especially valuable.

Ukraine’s international supporters should offer a wide range of social security commitments to encourage refugees to repatriate. Because the largest proposed commitments are options in an insurance mechanism, if people are successfully incentivized to return to Ukraine, Ukraine’s economy will grow, and a smaller fraction of returned refugees will exercise those options. This means the actual cost of these policies is much less than the initial commitment. In parallel, to attract international investors, the United States and Ukraine’s other allies need to expand the capacity and scope of investment underwriting, or guarantee funds. Stabilization also requires commitment to a currency board and reopening at least one international airport in Ukraine.18 A currency board with international underwriting would represent a permanent commitment—thereby dispelling investors’ and citizens’ concerns (and Russian hopes) that changing political winds in supporting countries could lead to a withdrawal of support.

Designing the right structural incentives will be a—if not the—key part of international assistance. In addition to military success, demining, rebuilding infrastructure, and financial support, reconstructing Ukraine will require both a secure environment and rule of law. Risk-mitigating insurance mechanisms make those additional requirements attainable. Outside the vast set of domestic structural changes and policy measures needed, international partners will play a critical role, particularly through incentives.19 Those incentives can be divided into those aimed at attracting and reintegrating refugees, those aimed at attracting physical capital investment, and those with broad stabilizing effects.

Refugees and Labor

A reconstruction strategy that focuses on incentives for businesses to invest and for workers to return to Ukraine complements the dominant approach emphasizing large capital transfers and reparations (which assumes that massive capital flows will draw in businesses and workers). Capital transfers are essential, especially with respect to building social and physical infrastructure, demining, and efforts to support agriculture and generate business credit.20

To attract returning refugees once fighting is contained, people will need to believe that they have a secure backup option in the event of further fighting or economic collapse. In addition to Ukrainian government efforts to realize this, international supporters can provide insurance guarantees to make returning desirable. Specifically, Ukraine’s supporters should do the following:

- They should guarantee pension entitlements, whether defined benefit or defined contribution, from earnings already accumulated outside of Ukraine, and make them portable.

- They should give work-years-in-Ukraine credit to entitlements in supporter countries, where a quantity of years worked in Ukraine entitles a person (and their family members) to a certain quantity of years of authorized residency and the ability to work (and accumulate pension assets) in supporter countries, as well as retirement benefits and/or health care benefits in supporter countries.

- They should guarantee housing, health, schooling, and welfare payments to family members who have returned to Ukraine and are not in the labor force, for a transition period. All major supporting countries have taken these steps. However, additional steps should include offering refugees welfare payments for a period upon return to Ukraine; supporting returning refugees to undergo retraining or further education; providing continued support and social services to dependents of refugees who return to Ukraine (at a higher level than those whose household heads do not return); and supplemental programs aimed at women with major family care commitments (e.g., supplemental payments upon return for external family care support).

- They should encourage the Ukrainian government to raise the retirement age to sixty-five years. While this undoubtedly would be unpopular, it signals that Ukraine values the labor efforts of its older citizens, and that in a wartime setting, early retirement is appropriate only for citizens with disabilities. This encouragement can be matched by allies with graduated payments to those who return from supporter countries. Variation in life expectancy across regions in Ukraine is strikingly low, reducing equity issues that arise from adjusting defined-benefit pensions.

Those guarantees would reduce the risks of returning home and provide supplemental incentives that, beyond monitoring costs, have almost no immediate budgetary consequences for contributing nations. Augmenting Ukraine’s labor force would increase its chances of economic growth, its military resilience, and its economic self-sufficiency. The greater the uptake of programs along those lines, the larger the return flow and, consequently, the less likely it will be that former refugees who returned to Ukraine will emigrate again. A further psychological benefit is that such measures more strongly link Ukraine to central and western Europe and, ultimately, increase the likelihood of EU accession.

Note that the cost of those commitments will be borne overwhelmingly by European governments. To equalize effects, the United States, Canada, Japan, and South Korea should consider setting up and contributing to a cost-sharing fund.

Insuring Capital and Fighting Corruption

For private sector investors, a strong international insurance program can be a necessary catalyst or condition to secure private sector infrastructure and industrial investment. Such investments typically are long-term, geographically fixed, and involve significant financial commitments. With insurance, many risks can be hedged and covered. Without insurance, uncertainty about the war (and whether such investments would be targets), domestic stability, and the environment will be barriers. Such insurance effectively strengthens the international partnership and movement toward EU accession.21

Providing insurance and expediting private investment into Ukraine would ultimately reduce costs to supporting countries’ taxpayers by outsourcing reconstruction to market forces rather than being underwritten by the public sector. For a fraction of the cost of reconstruction efforts related to industry, a large, multidecade insurance product would draw in complementary private international investment. In essence, the relatively small cost of insurance would enable the private sector to spearhead reconstruction with best-available technology, business practices, and modernized products.

There are still risks. Channeling funds through DFC-like organizations is expensive, and competent monitoring will be essential to minimize corruption and ensure the effectiveness of investments. If DFC-like loans and associated monitoring are extended to funds provided to Ukrainian investors, domestic corruption also could be lowered (those loans could be jointly administered with the Ukrainian government to ensure its sovereignty).

Ukraine has greatly improved its efforts to control corruption, but there is more to be done: a flood of capital with limited supervisory capacity is an invitation for massive corruption. In addition to a supervised publicly backed loan strategy, Ukraine’s supporters can provide incentives for consumers and clients to report transactions that could be fraudulent or involve tax avoidance. For example, the government of Uzbekistan encourages consumers to demand receipts for purchases and then upload them onto a government site.22 The tax authorities then match submitted expenditures against firm reports; if evasion is suspected and documented, consumers share 20 percent of the value of fines. Tax compliance has risen by 30 to 40 percent. This practice could be extended beyond consumer goods.

Corruption monitoring and control efforts can be outsourced to local organizations. Donors would fund watchdogs like Transparency International-Ukraine and research projects like Vox Ukraine. This is an inexpensive proposition, and it is healthy to have the critiques coming from domestic sources rather than foreign governments.

Yet another measure would mandate public reporting of all public meetings and expenditures. Ideally, all local reports and information about expenditures would appear in a searchable database. That way, investors and researchers could use standard statistical techniques to identify potential excess charges. Specifically, since 2015, the Ukrainian government has operated a self-described fully transparent e-procurement system, ProZorro. While military spending does not go through ProZorro, a substantial portion of it likely could.

Given the major efforts to curb corruption, the Transparency International ratings could be biased downward, reflecting lagged effects from earlier years. Nevertheless, there are lingering questions about perceived corruption in the judiciary and in customs and tax collection. Such lack of confidence makes international guarantees all the more important to investors. At the same time, those guarantees would signal to the Ukrainian government that international supporters will be engaged, since they have skin in the game.

Demonstrating Stability

Several possible measures could enhance confidence in the Ukrainian economy. Two in particular merit attention: creating a currency board and reopening a commercial airport. Both are important to investors and broader public confidence.

Currency Board

A currency board is essential to exchange rate stabilization. Domestic and, especially, international investors will be deterred if Ukraine’s currency, the hrivnya, is unstable, or even potentially unstable. Stability has not been a problem since the initial post-invasion currency crash, but that stability was maintained by external lenders and donors. The National Bank of Ukraine also appears to have moved from a fixed exchange rate policy toward a bounded float.23 Indeed, a primary incentive for seizing Russian assets abroad was that it would allow the Ukrainian government to continue to run large deficits for several years. However, this is not an indefinite solution, with the government deficit currently running at about 20 percent of GDP. There also is growing urgency: as of August 2, 2024, Standard & Poor’s lowered Ukraine’s sovereign debt to the level SD—selective default.

University of Miami Professor Michael Connolly has suggested an initial system that would fix the hryvnia to the euro in a currency board, backing high-powered money with euro reserves. Ukraine could get some seigniorage from issuing the hryvnia to the public; it also could then apply to join the euro zone, as Croatia has done. The problem in the long run is the source of euro reserves. Subject to responsible spending guarantees (in essence, IMF approval of fiscal policies), Ukraine’s international supporters could need to commit to supply some or all reserves over a specified period.

A currency board for Ukraine is not a new suggestion. U.S. Senators Ted Cruz (R-TX) and Marco Rubio (R-FL)—now Trump’s secretary of state—pressed the Barack Obama administration to work with the IMF to create such a board, albeit without apparent concern about funding.24 The advantage of a currency board with international underwriting is that it represents a permanent commitment, a major driver of confidence in the government.

The Ukrainian economy today is not large (Ukraine’s 2023 GDP was $179 billion—slightly smaller than that of another wheat-producing entity, Kansas, which had a 2023 gross state product of $182 billion). As Ukraine’s economic recovery occurs, the international debt incurred while propping up a currency board will shrink as a share of GDP. In the interim, supporting a currency board would require a global commitment of about $16 billion.

A currency board operates by pegging a country’s currency to a foreign currency at a fixed rate, while also holding reserves of that foreign currency to back the entire money supply, thereby limiting the scope for discretionary monetary policy. This arrangement is seen as a commitment mechanism that can anchor expectations and prevent runaway inflation, particularly in countries with a history of monetary mismanagement.

Estonia and Lithuania adopted currency boards during their transition from centrally planned economies to market economies after the dissolution of the Soviet Union. Those currency boards played a crucial role in stabilizing their economies, maintaining low inflation, and facilitating their eventual accession to the European Union and the eurozone. Estonia was able to maintain a currency board with minimal disruptions thanks to its strong fiscal discipline and conservative monetary policies. It and Lithuania experienced rapid economic growth, low inflation, and increased foreign investment following the adoption of those regimes.25

Success is heavily contingent on sound governance and self-fulfilling cycles of confidence and international credibility. Countries that use the favorable conditions provided by a currency board to achieve fiscal balance, manage real appreciation, and handle capital inflows wisely can secure long-term economic benefits at a relatively low cost.26

However, failure to implement those policies can lead to significant economic distortions and eventual crises. A currency board with international supporters’ backing seems destined to succeed, provided Ukraine follows appropriate credit and other economic policies. International support would make the currency board credible. In addition, that support would signal a long-term commitment to Ukraine, further bolstering financial and nonfinancial actors’ confidence in the economy.

Commercial Airport

A second stabilizing measure would be to reopen one or more of Ukraine’s main airports—as Ukraine recently announced it aims to do in early 2025. This proposal is a tricky one that has been discussed regularly since 2022 once the February invasion was blunted.27

There are major potential advantages. An increase in passengers flying into the country (on U.S. carriers) has a positive relationship to total FDI, increasingly so as the number of passengers grows, even when controlling for battle fatalities, GDP, and other metrics. This supports the hypothesis that opening an airport in Ukraine, even during wartime, would likely increase FDI and economic growth.

The strategic and safety issues of reopening an airport are complex. The EU Aviation Safety Agency would first need to green-light the opening, which would enable private insurers to cover flights and passengers. Approval—and whether it is a sufficient condition—will depend on Russia’s expected response.

The Russian government has no interest in declaring that it will not shoot down commercial airliners landing in a Ukrainian airport. Yet it seems unlikely that Russia will target a commercial airliner; the costs of the near-certain retaliation are high. Russia is especially unlikely to target a civilian plane if the airlines in question are neutral countries’ national carriers that also fly to Russia (notably, Turkish Airlines, Emirates, Qatar Airlines, or possibly El Al).

The more serious problem is that of mistaken identity. Commercial airliners are almost always targeted in conflict out of error in identification rather than malice, as happened with an Azerbaijani civilian airliner above Grozny in December 2024. The threat to commercial air increases with time and proximity to active conflict. Additionally, the Russian Ministry of Defense has imperfect control over its forces in or near Ukraine, and some of them might not follow due diligence in targeting or care about attacking a commercial airliner with a surface-to-air missile or drone. Furthermore, while European fighters could escort commercial airliners for the last or initial few minutes of flight, fending off surface-to-air missile attacks is extremely difficult in the best of circumstances. Any insurance mechanism would be significantly cheaper and more effective at an airport away from the front lines.

Either Kyiv or Lviv should be the first airport open. (Reopening airports in the eastern and southeastern industrial heartlands is impractical for security reasons.) Ukraine’s exports of goods and services are dominated by Kyiv, as are its imports. The immediately surrounding area adds to its dominance. Lviv is fourth in terms of exports and second in terms of imports.

Despite the economic dominance of Kyiv, the costs of reopening Boryspil Airport could be prohibitive at this time. The airport itself can be defended against missile attacks and deliberate attacks on civilian airliners are unlikely, but the risk of mistaken identity is substantial, and the cost of insurance (and prospective passengers’ reluctance to fly) likely makes reopening Boryspil infeasible. The ubiquity of rapid passenger train service further enhances the relative attractiveness of Lviv. That is reflected in Ukraine’s announcement, on October 30, 2024, that it plans to reopen Lviv airport in 2025.

Three econometric approaches using cross-country data can be used to get an upper-bound sense of the economic impact of reopening an international airport. While none of the approaches fully control for unobserved correlates of airport reopening, those unobservable factors also likely have positive economic effects, thereby biasing up airport reopening coefficients.28

The models are consistent with each other: each estimated approximately 7 to 13 percent FDI growth associated with each 100 percent increase in flights. Both contemporaneous and lagged air traffic is associated with increased foreign direct investment, especially for countries and airports with modest traffic. When there is a higher number of battle fatalities, the predicted effect is stronger. Beyond omitted variables and endogeneity, the obvious criticism of this approach is that the terms are likely cointegrated. However, the positive significance of an air traffic surge in areas with high battle fatalities on FDI seems more likely to be unidirectional: it seems unlikely that FDI has a non-idiosyncratic causal impact on battle fatalities.

Conclusion

Given that the war continues, the primary focus on arms and other military support to Ukraine is entirely appropriate. Nevertheless, failing to plan for Ukraine’s labor, capital, and economic stabilization risks its entire recovery and long-term security.

A series of measures intended to leverage international infrastructure support and insurance mechanisms is necessary to create incentives for private capital investments and, most importantly, the repatriation of refugees to grow Ukraine’s labor force. Those incentive measures are inexpensive and politically viable, and the potential gains are significant. Most of them can be implemented immediately while the war continues. In addition to having real economic impacts, the measures have signaling value—to displaced Ukrainians, those who have not left, prospective investors, and the Russian government. Russia is counting on the international community to grow fatigued with Ukraine; the measures sketched above would show that Ukraine’s supporters are standing firm.

Acknowledgments

We gratefully acknowledge valuable data assistance from the staff at Work.ua, as well as exceptionally useful commentary on earlier drafts from General Philip Breedlove, Michael Connolly, Patrick Duddy, Maryna Kapustina, Pavlo Prokopovych, Jon Queen, Howard Shatz, Paul Stares, Edward Tower, Volodymyr Vakhitov, and Nataliia Zaika. All omissions, misinterpretations, errors, data and econometric flaws, and other limitations are solely our own.t

Report

Report Report

Report Report

Report Report

Report Report

Report Report

Report