The 2014 Dollar Rise is no Longer Impacting U.S. Trade

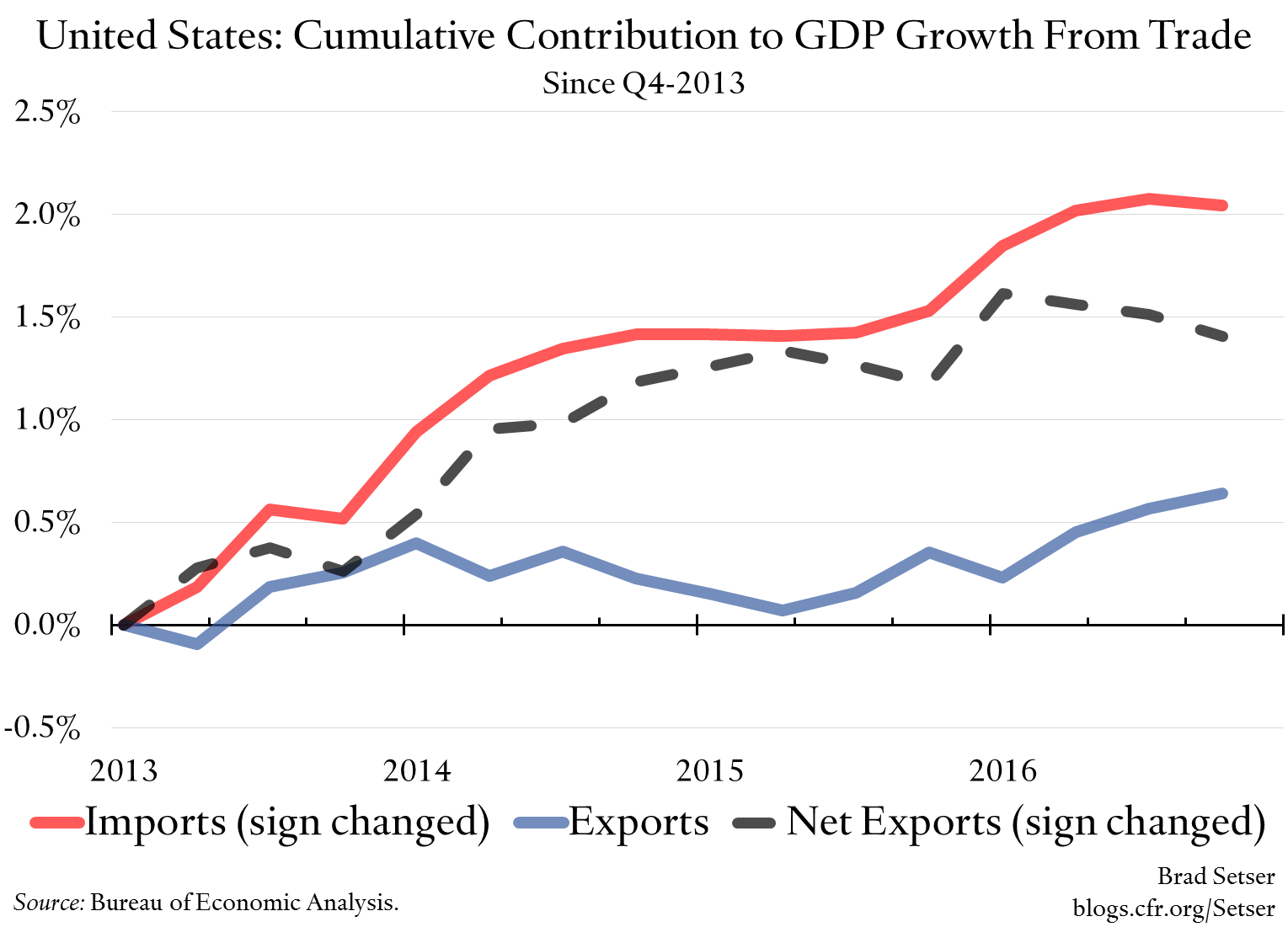

One reason why headline GDP has increased by around 3 percent (q/q, annualized) in the last two quarters is that net exports contributed positively to growth. Not in any big way, but they contributed.

That to be honest has surprised me. Going into the year I expected net exports to be more of a drag, for three reasons:

- Imports had been surprisingly weak in the first part of 2016, and I expected a bit of payback in the 2017 data.

- There is evidence—notably from the slow response to the dollar’s 2003 depreciation—that the trade response to a big exchange rate change now takes longer, and it can take up to three years to see the full effect. So I was expecting some additional drag from the dollar’s 2014 appreciation.

- The dollar rose strongly in q4-2016, and I expected that to have an impact.

Broadly speaking, none of these three effects have played out quite as I expected. There was a bit of payback for weak import growth early in 2016 in q4-2016—and to a lesser degree in q1-2017. But in q1 the rise in imports was offset by a boost to exports. The impact of the 2014 dollar appreciation seems to have petered out, exports are rising again (though slowly). And the dollar’s late 2016 appreciation reversed over the spring and summer.

At this stage there is no reason to think that the trade impact of the 2014 dollar move isn’t mostly, so to speak, already priced in. Three years have elapsed from the dollar’s big move in late 2014—and manufactured exports are about a percentage point of GDP lower now than they were in 2013.*

So I no longer expect a large drag from trade if the dollar stays at roughly its current level,** though if the Fed keeps tightening ,the current account would deteriorate from the mechanical impact of a higher interest bill on the United States external debt.

But the stability of the dollar at roughly its current level isn’t a sure thing. Any of three things could change:

- The Mexico peso could fall further, if NAFTA talks collapse and Trump gives notice of his intent to withdraw.

- The Chinese yuan’s current stability—both against the dollar and against the basket—might give way to a new bout of depreciation pressure should China’s growth falter, or should China proceed too quickly to liberalize its capital account (the needed prerequisites for an orderly liberalization of outflows in particular are not in place).

- The euro could reverse its 2017 appreciation, whether because the eurozone’s recovery falters and the market stops anticipating a future point when the ECB will start actually tightening (rather than doing a bit less easing) or because the market starts to expect more rapid tightening from the Fed.

And, of course, the most obvious thing that could lead the market to anticipate a faster pace of monetary policy tightening—apart from a new Fed Chair—is a major change in U.S. fiscal policy, such as a large tax cut that boosts demand (albeit inefficiently) at a time when the economy doesn’t need a cyclical boost.

* I do wonder if the lags on the export impact from dollar depreciation are longer than the lags on the impact of dollar appreciation, but that is a story for another time.

** I also tend to think that the dollar needs to depreciate slowly over time to keep the trade balance stable, but that is a separate effect.