Make the Foreign Exchange Report Great (Again)

The Trump Administration wants to bring down the U.S. trade deficit.

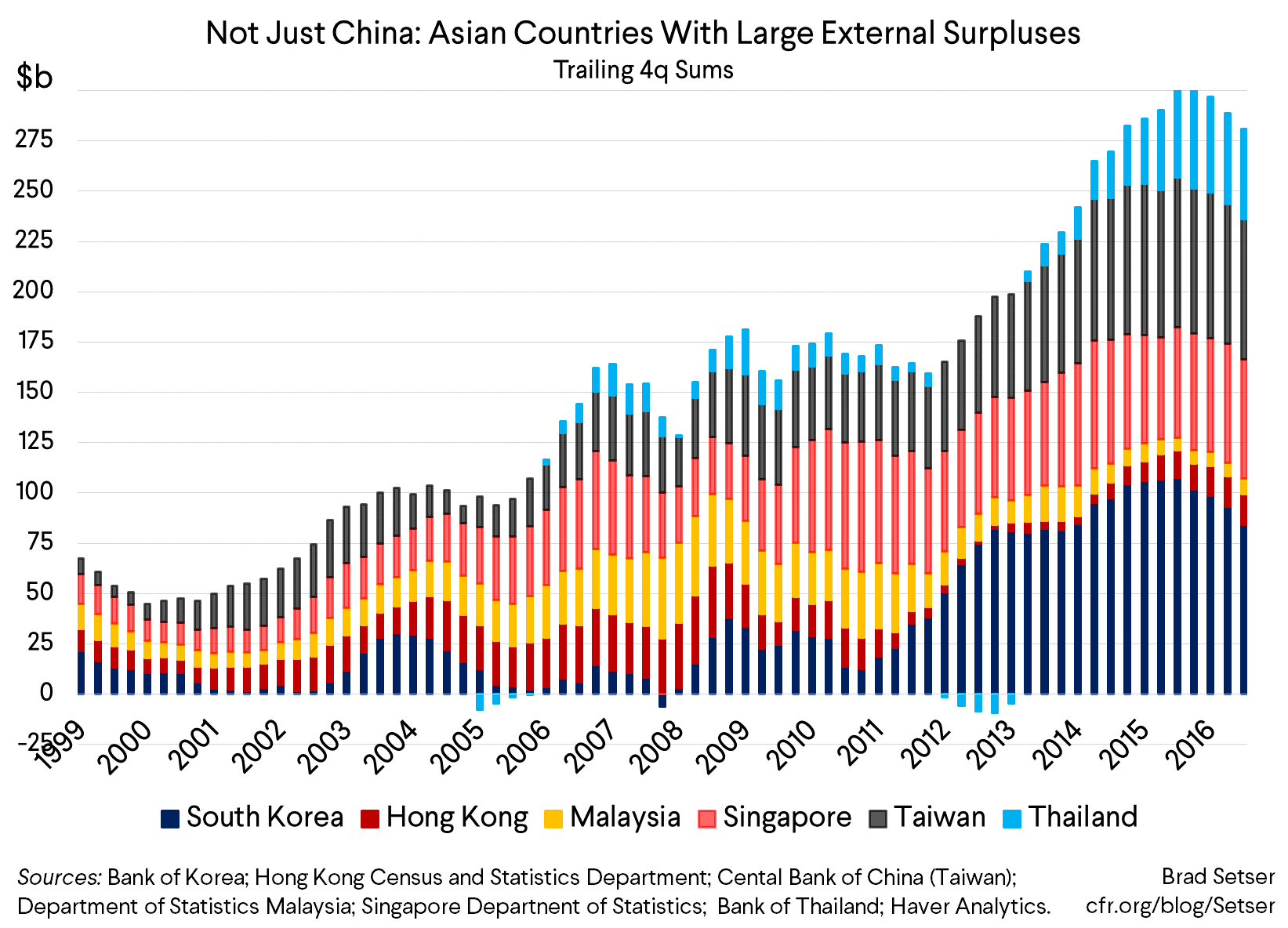

A number of manufacturing-heavy Asian economies run sizable current account surpluses. Over the course of the summer, some of them were clearly intervening to keep their currencies from rising against the dollar.

But, somewhat surprisingly, this hasn’t caught the attention of the Trump Administration.

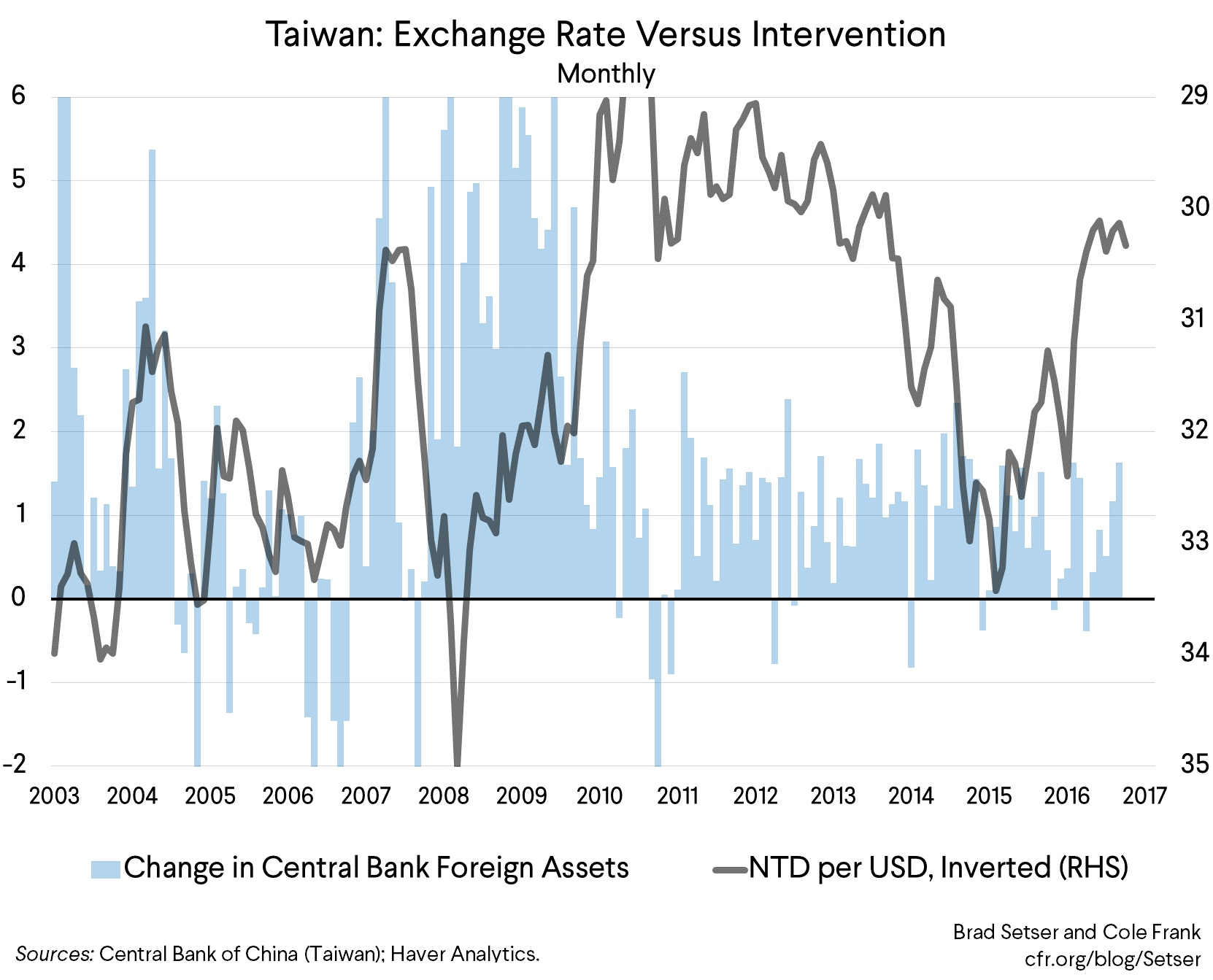

The latest Treasury foreign exchange report removed Taiwan from the Treasury watch list even though Taiwan intervened over the summer to keep the New Taiwan Dollar from rising (at the 30 Taiwan dollars to the U.S. dollar mark).

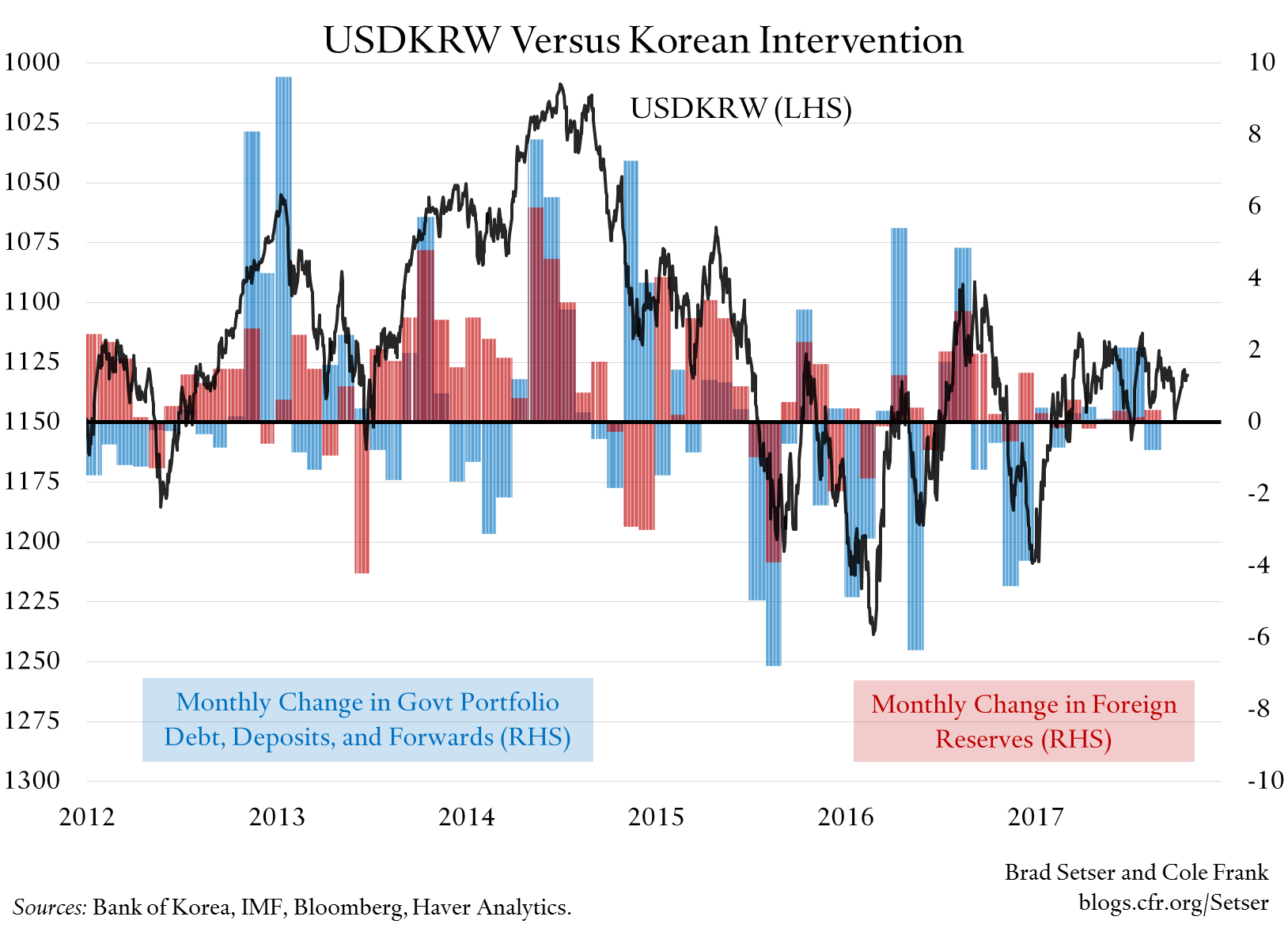

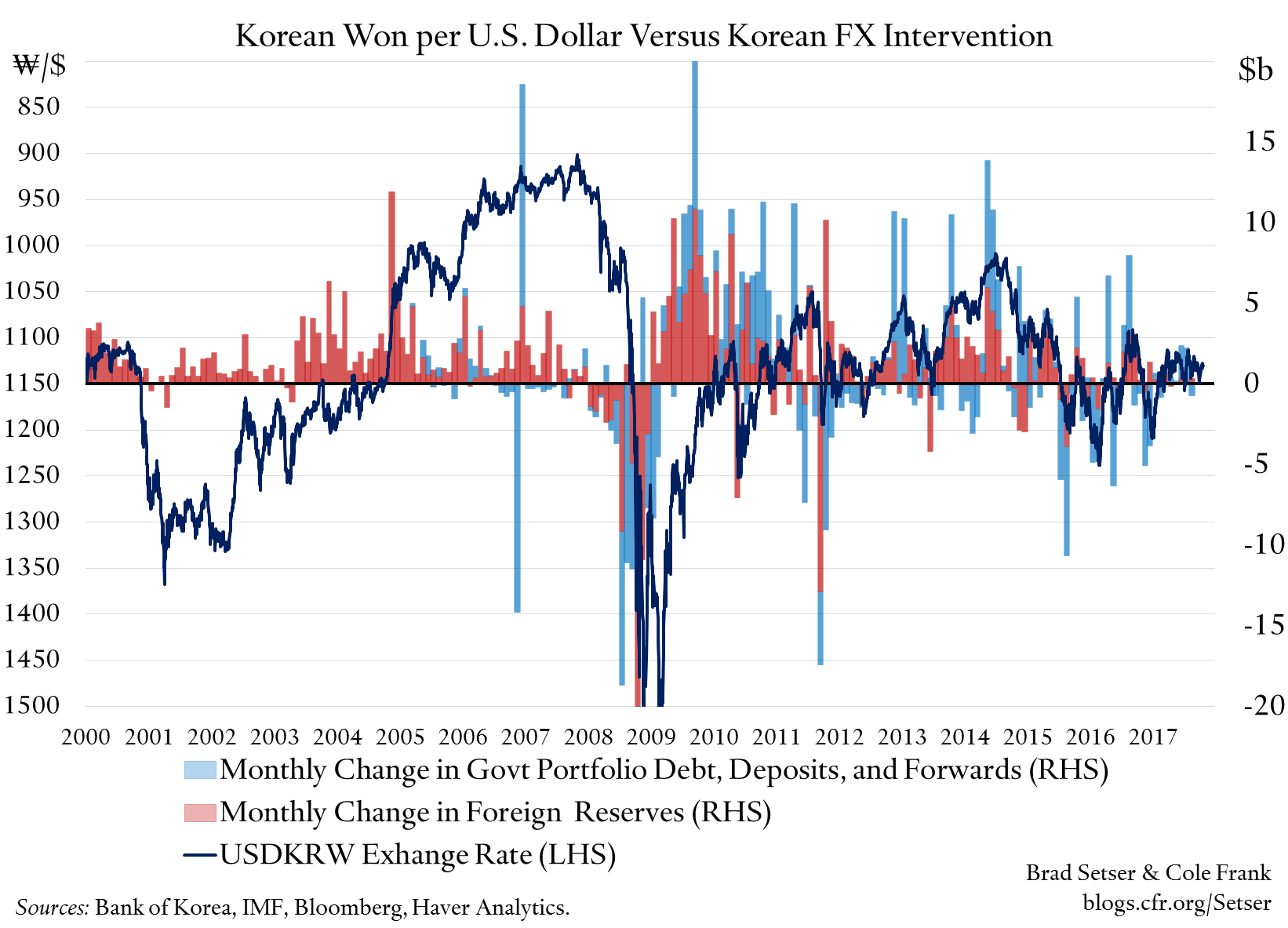

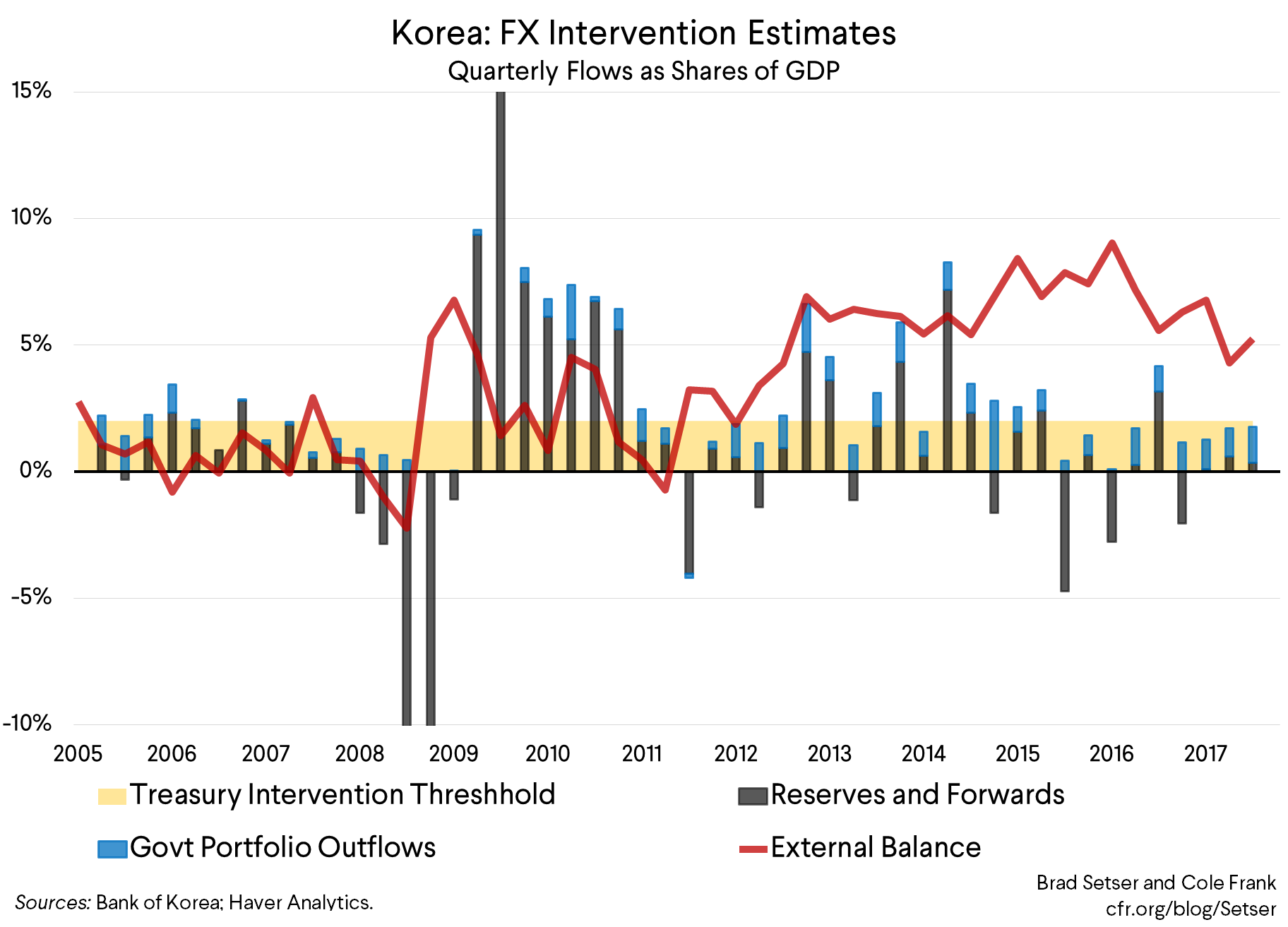

The report didn’t display any noticeable irritation at Korea’s continued propensity to buy dollars to keep the won from strengthening through the 1100 Korean won to the dollar mark. Korea bought foreign exchange in July, before the North Korean missile crisis intensified.

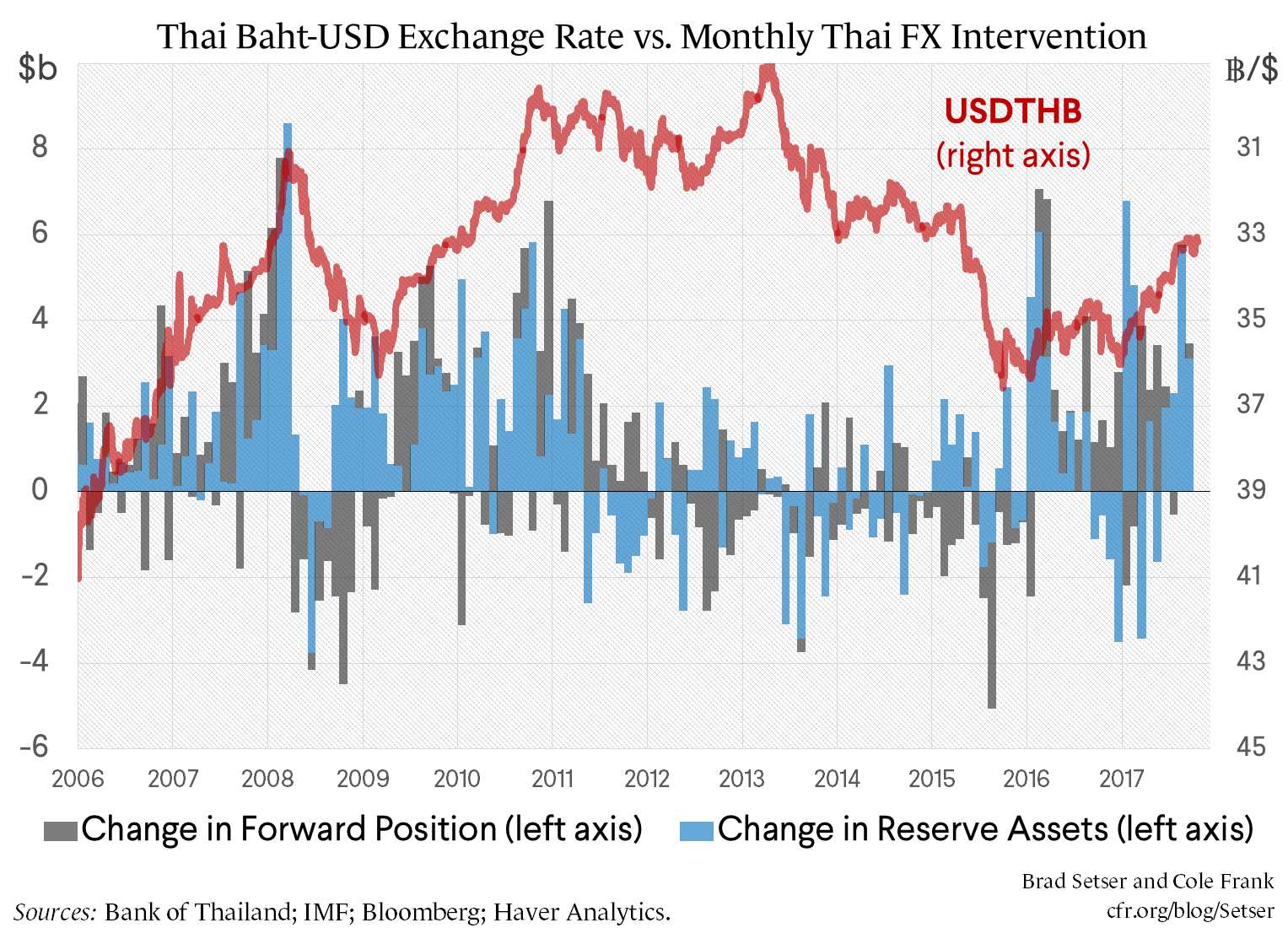

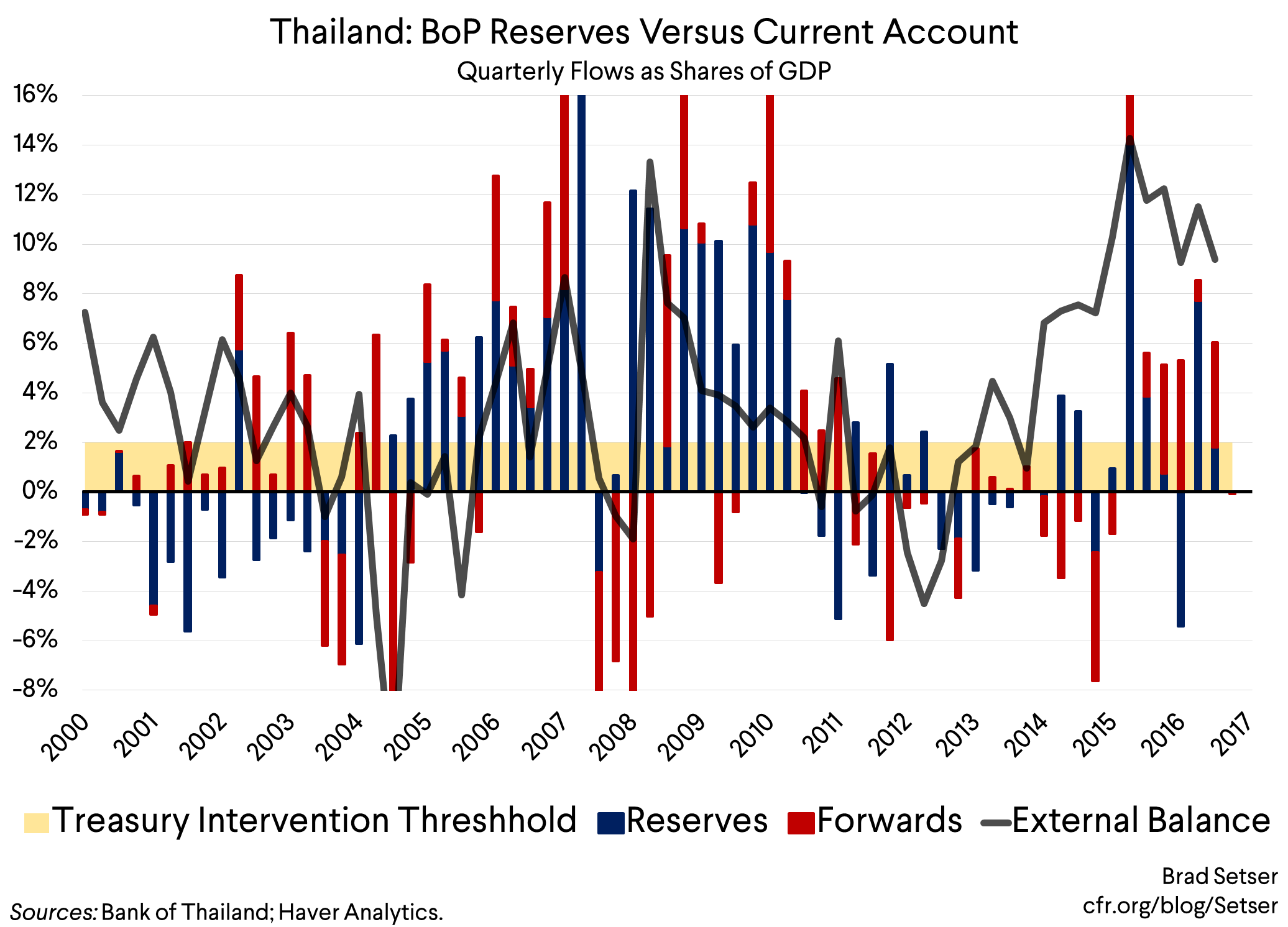

The report continues to ignore Thailand, even though Thailand comes very close to meeting all three of the Treasury’s stated criteria for identifying manipulators (a bilateral surplus with the U.S. of over $20 billion, an overall current account surplus of more than 3 percent and intervention in excess of two percent of GDP).

And Singapore got yet another free pass.

These countries, not China, are at the epicenter of the recent return of foreign exchange intervention in Asia. India and Indonesia have also intervened, but they get off because they run current account deficits.*

If you think countries with large current account surpluses shouldn’t be intervening in the foreign exchange market to help keep their currencies weak, there is plenty to complain about right now—more so than at any time since the dollar’s late 2014 appreciation. The combined current account surplus of these smaller Asian economies ($250 billion) is up substantially from 2007, and for that matter from 2012. And practically speaking, currency moves have a fairly predictable impact on the trade balance—convincing a number of Asian countries to let their currencies appreciate would likely have a more significant impact on the U.S. trade deficit than Trump’s high profile attempts to renegotiate existing trade agreements.

Centering the Treasury’s report around the three criteria set out in the Bennet amendment has strengthened the report’s analytical underpinning. At times in the past the report veered a bit too far from actual developments in the foreign exchange market—particularly in its description of the policies of individual countries.

But I suspect that applying the three criteria too mechanically creates problems of its own—not the least because it is relatively easy for a country that is paying attention to engineer around the reserve accumulation criteria.

At risk of intervening too much? Get your social security fund to buy a bunch of foreign assets in a new “diversification” push. Or have the finance ministry issue local currency bonds to set up a sovereign wealth fund that will buy foreign exchange from the central bank on an ongoing basis. Or let your forward book rollover directly to your sovereign wealth fund. Or ask your state banks to buy foreign exchange and provide them with an (undisclosed) hedge.

I didn’t make any of the examples above up. The irony is that the more experience a country has with intervention, the easier it often is to hide the intervention.

Concretely, I think the Treasury should make five adjustments to the foreign exchange report.

(1) Assess more countries against the Bennet criteria.

This one is easy. Expand the report to the top twenty trading partners. And automatically assess any country with its own currency and a current account surplus of over 3 percent of GDP. There is no good reason why the foreign exchange report right now doesn’t cover Thailand—which is less than $1 billion dollars away from meeting all three Bennet criteria (its bilateral surplus with the U.S. is $19 billion and change).

(2) Deemphasize the bilateral balance.

This one is a little tricky. The Trump administration has made the bilateral balance a key measure of trade success (it isn’t, especially in a world where bilateral trade is often heavily motivated by tax concerns. The focus right now is on goods trade, but the bilateral services data is even more problematic: the U.S. runs a healthy services surplus with Ireland and the “UK Caribbean”).** And well, the bilateral balance criteria is mandated by Congress: the Treasury cannot legally toss it aside entirely.

But the bilateral balance currently has the effect of letting some countries that should get more scrutiny off the hook.

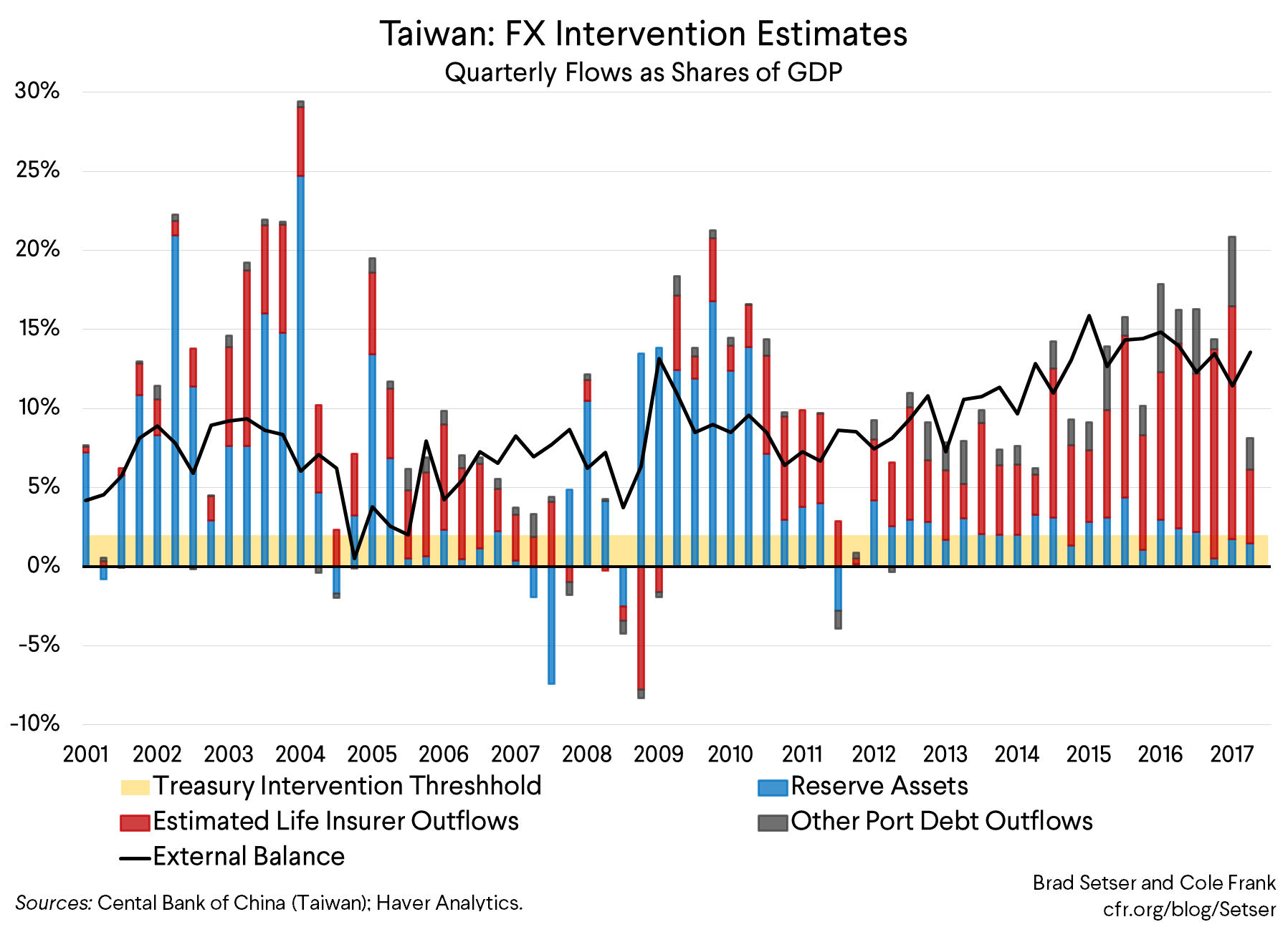

Taiwan for example. Its bilateral surplus with the U.S. doesn’t breach the $20 billion threshold even though its overall current account surplus easily tops 10 percent of its GDP.

Taiwan produces a ton of semiconductors (some based on licensed designs, with the royalties paid—I would guess—in no small part to the offshore subsidiaries of U.S. multinationals for tax purposes; some based on Taiwanese intellectual property) that are sold to Chinese firms that assemble electronics for reexport. Taiwan’s value-added bilateral surplus is far higher than its reported bilateral surplus with the U.S.

The same is true of Korea. Korea now exports more semiconductors than autos. But the bilateral trade data shows only limited U.S. imports of Korean semiconductors (and for that matter, only modest imports of smart phones). Korean electronic components are often assembled elsewhere for re-export globally.

And making a deficit in bilateral trade one of the currency report’s three criteria has let Singapore permanently escape the scrutiny its heavy intervention deserves, as Singapore runs a bilateral surplus with the U.S.*** Singapore is small, but its currency policy has long set a bad example for its neighbors.

(3) Stop giving countries a free pass on a large existing stock of reserves.

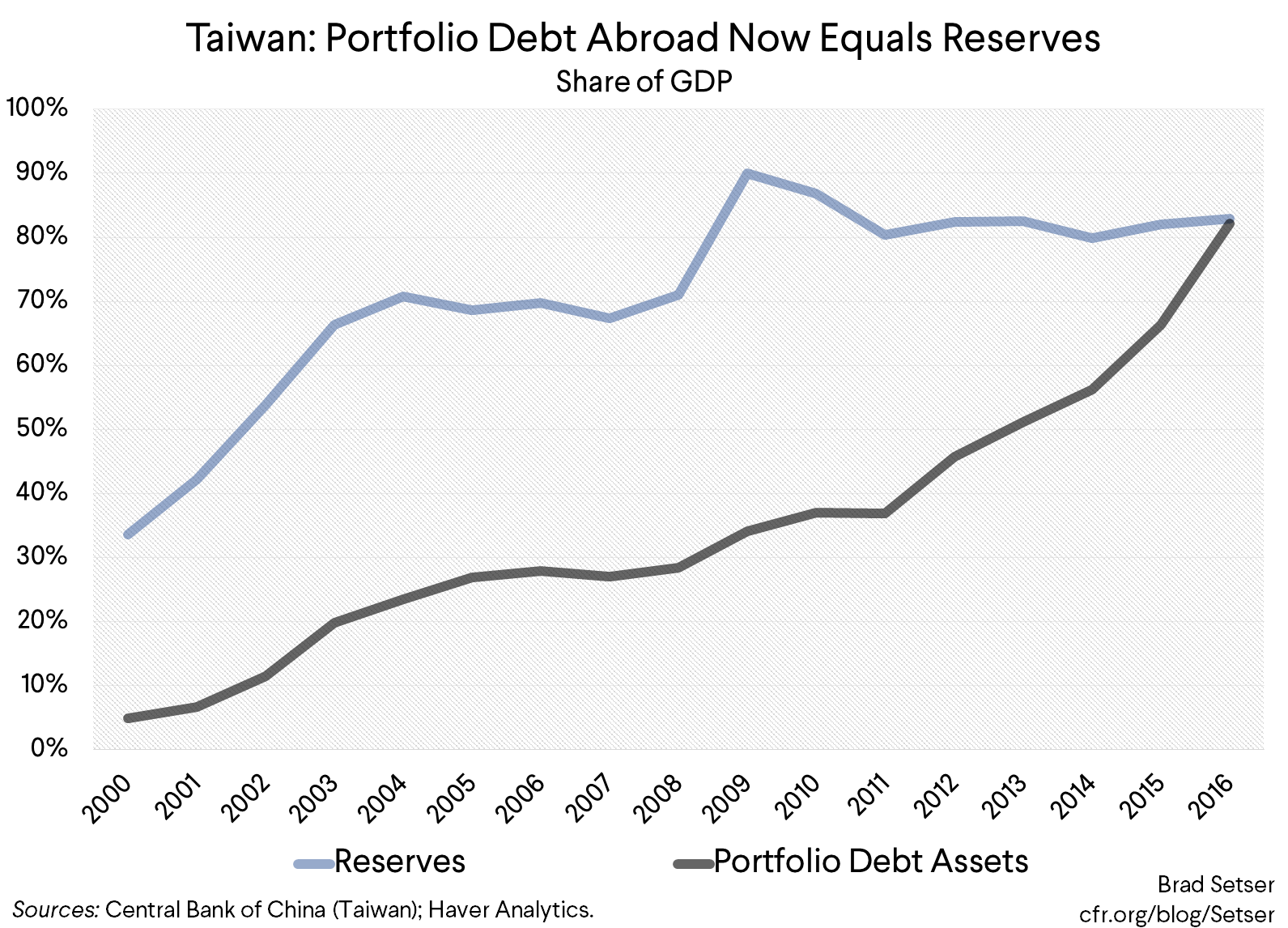

Right now the Treasury deducts estimated interest income on a country’s existing stock of reserves from its estimate of intervention. That has the effect of giving a country like Taiwan—with reserves equal to 80 percent if its GDP—a pass on reserve growth of about one percent of GDP, if not a bit more.

In my view, countries with high levels of reserves and large current account surpluses should be encouraged to sell the interest income for domestic currency and in turn use the domestic currency to pay the interest on their sterilization instruments or to remit profits back to the finance ministry. In Taiwan and Korea that would provide a revenue stream that could be used, for example, to pay for expanded social insurance.

Counting interest income toward the two percent reserve growth threshold also is a way of recognizing that a large stock of reserves from past intervention has an impact on the current account (as Dean Baker emphasizes) not just intervention today.

(4) Do not ignore the exchange rate at which a country intervenes.

At 1100 won to the dollar, Korea generally runs a large current account surplus globally, and will export a ton of autos to the U.S.

At 900 won to the dollar, Korea ran a much more modest surplus globally, and Korean auto makers have a strong economic incentive to produce in the U.S. rather than in Korea.

The right level of the won to the dollar of course depends a bit on Korea’s own economic conditions and a bit on the dollar’s overall strength or weakness. But if the won is being kept too weak against the dollar, it is likely to be too weak against most currencies most of the time.

The Treasury currently just looks at the quantity of intervention, not the timing of the intervention – and it doesn’t assess whether a country is stepping into the market at the right or the wrong level. The Treasury’s October report, for example, lauds Korea for reducing its intervention (the lower level of intervention is a function of large sales last fall when the dollar was appreciating strongly and Korea faced significant political uncertainty, Korea has resisted appreciation pressure by buying dollars at various points this year). But last I checked, Korea continues to have a policy of intervening to block appreciation when the won approaches 1100. And intervening at 1100 is a step backward in the grand scheme of things. In the years before the crisis, Korea waited for the won to appreciate to 900 before intervening (that was Korea’s policy in 2006 and 2007) and at times after the crisis it has waited for the won to approach 1000 before stepping in (admittedly, the won only reached 1000 once, in 2014; Korea usually stepped in at the 1050 mark).

Looking at objective criteria like the amount of intervention was meant to take subjective judgments about the “right” level of the currency out of the report. I don’t think it works. Intervention at the wrong level should be called out even if it isn’t big enough to cross the “sanctionable” threshold, particularly in a context where the government is actively encouraging a broad range of domestic investors to buy foreign currency.

(5) Stop ignoring shadow intervention (e.g. the accumulation of foreign assets by actors other than the central bank).****

Here is a prediction: China, Korea, Taiwan, and Japan will never “show” reserve growth in excess of two percent of GDP when they meet the other two criteria for being named. It is too easy to shift foreign exchange off the central bank’s balance sheet and onto the balance sheet of other state actors.

Korea for example has decided to invest a large share of the assets of its national social security fund abroad (the national social security fund is already huge, and—thanks to Korea’s high contributions and miserly social benefits—adding rapidly to its assets). Call it diversification if you want. It clearly has had the effect of structurally reducing Korea’s need to intervene in the foreign exchange market.

Japan’s government pension fund has a huge pool of domestic assets that it could sell (to the central bank) in order to invest abroad if Japan had reason to be concerned about yen strength.

China’s Belt and Road Initiative was originally designed, in part, to help the PBOC reduce its headline reserve growth—though it has subsequently taken on a life of its own.

And Taiwan has encouraged outflows from its life insurers on a rather massive scale. I would be a bit surprised if they don’t have an explicit or implicit hedge with the government. The growth in their holdings of foreign debt mechanically has explained how Taiwan has been able to keep its intervention limited even with a massive surplus. Taiwan’s financial institutions now hold almost as much foreign debt as Taiwan’s central bank, and clearly have been doing most of the recent buying.****

In many ways this is the right time to try to establish a new global norm, one where countries with large current account surpluses don’t intervene to block appreciation—or encourage their state institutions to diversity into foreign assets—to help keep the currency weak. Korea, Singapore, Taiwan and Thailand all have current account surpluses of over five percent of their GDP; Singapore, Taiwan and Thailand have current account surpluses of over ten percent of their GDP (over the last four quarters of data).

Setting out the norm when most countries are in violation of it is difficult, practically speaking. Better to spell out it out ahead of time and give countries a chance to adjust.

That’s why the October report was a missed opportunity. The Treasury took the heat off just when several countries should have been put on notice for their intervention over the summer.

* Switzerland has intervened heavily at times this year too, but the euro’s recent appreciation has taken a bit of pressure off the Swiss National Bank.

** The bilateral services trade is in its own way quite interesting. The U.S. runs a massive bilateral services surplus with Ireland, and an (admittedly small) deficit with Germany (a world renowned center of service excellence obviously!). The U.S. runs a massive surplus with the UK Caribbean (primarily in financial services) and to my surprise, a massive deficit with Bermuda (it is all due to reinsurance). It also runs a surplus with places like Switzerland and Singapore. That is why I suspect the bilateral services trade data is even more distorted by tax considerations than the bilateral goods data. (country numbers are from the U.S. services trade data, table 2.3)

*** I would guess in part for tax reasons. Singapore is a hub for petrol refining, pharmaceutical manufacturing, and semiconductor manufacturing and testing. And well, the import and and re-export of Australian iron, which clearly is tax-driven.

**** In some countries, like Japan, the finance ministry manages the bulk of the country’s formal reserves. But even in these cases there are ways of shifting foreign asset accumulation to less scrutinized institutions.

***** Since 2011, “private” holdings of portfolio debt—according to Taiwan’s net international investment position data—have increased from 35 to about 80 percent of Taiwan’s GDP. That’s a lot of foreign exchange risk for domestic institutions to hold.