$500 Billion in Dividends out of the Double Irish with a Dutch twist (with a bit of Help from Bermuda)

Tax is often the biggest factor in the balance of payments. U.S. firms operating in Bermuda paid $229 billion in dividends back to their U.S. parents in 2018. That’s more than the United States earned from exporting to China before the trade war, and more than Boeing and GE generated by exporting aircraft and their engines even before the new 737 was grounded.

Of the various questions raised by the international provisions of the Tax Cuts and Jobs Act, the amount of money that came home is probably the least important.

The notion that these funds were “trapped” abroad was always a bit of a myth. The funds themselves weren’t actually abroad. They might be legally held by the offshore subsidiary of a U.S. firm—but the funds themselves were almost entirely in dollars and almost entirely invested in a portfolio of U.S. assets (often a mix of Treasury and corporate bonds).

And any firm that wanted to make use of the funds onshore—whether to fund new investment or more likely a buyback—could do so without much difficulty. Financial markets were quite happy to lend Apple (Cupertino) dollars against the cash and cash equivalents held (notionally) in Apple (Ireland) or Apple (Jersey). Oh, and if a firm really wanted to invest more at home it could also rejigger its tax arrangements so it was earning a bit less abroad—if it actually had large investment needs, with accelerated depreciation its marginal tax rate would have been well below the headline rate.

No matter, the size of the offshore cash stash was impressive—and proponents of the reform made a big deal about how getting rid of global taxation and moving toward a territorial system would unlock the funds that were trapped abroad so that they could be invested in the United States.

Trillions were going to return to the United States.

And, well, a lot did return—it just all poured out of tax havens.

The offshore profits of a lot of U.S. companies were, so to speak, summering in Ireland and wintering in Bermuda.*

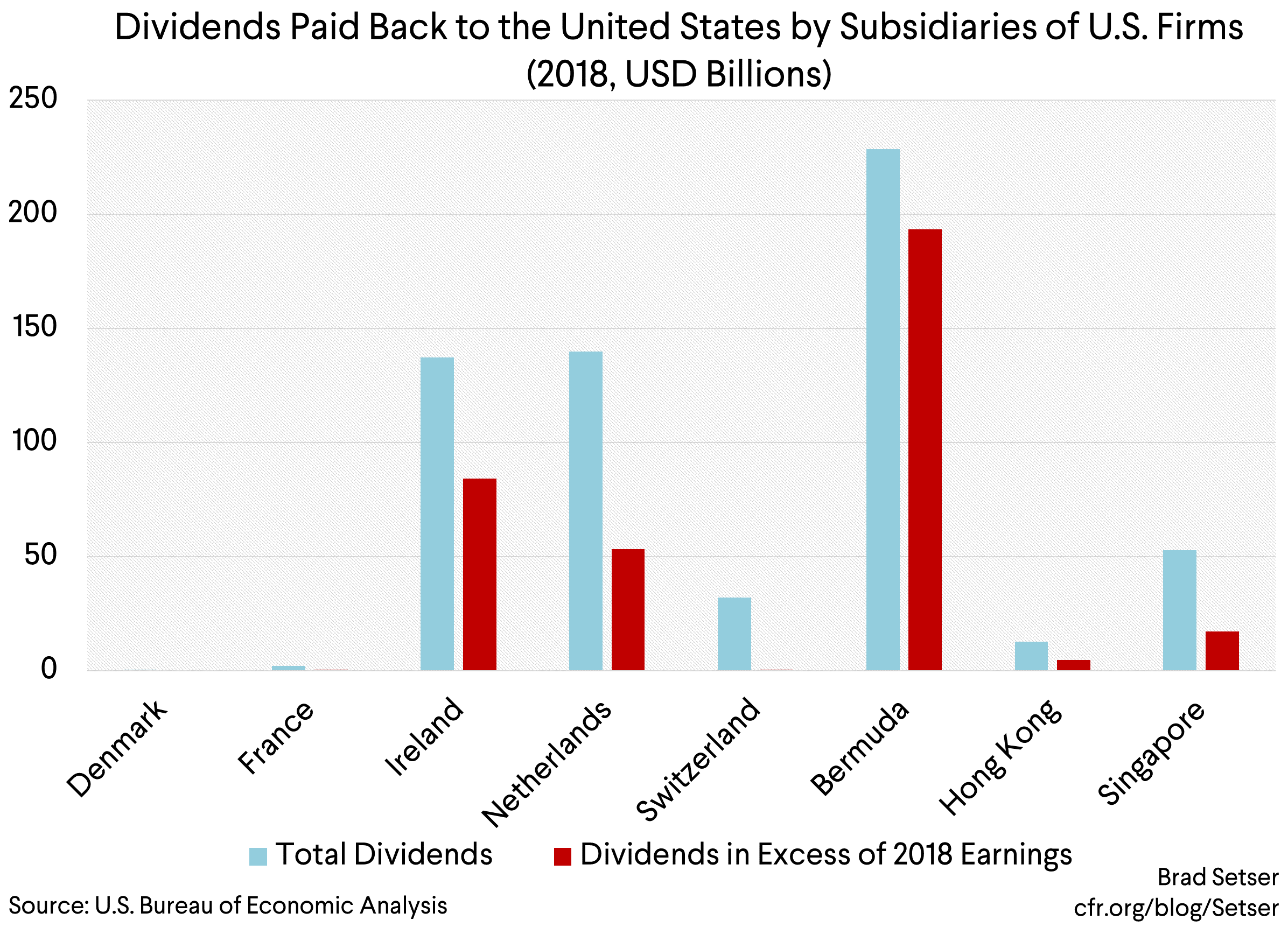

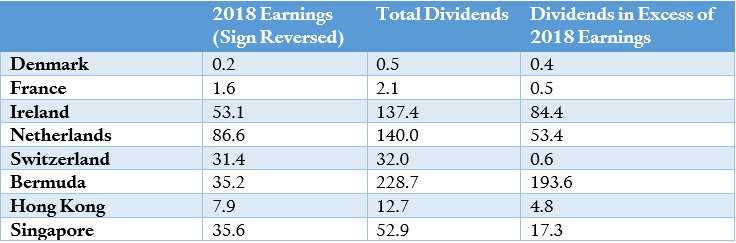

The offshore subsidiaries of American firms paid $775 billion or so in dividends back to their U.S. parents in 2018, up from $150 billion in 2017. Best I can tell, over $500 billion of that came from just three jurisdictions: Bermuda, the Netherlands, and Ireland.

Aficionados of multinational tax strategies will recognize these three countries immediately—they all figure prominently in the Double Irish with a Dutch Twist tax strategy (the goal of which was to legally move a firm’s profit out of Ireland and its 12.5 percent corporate tax rate to Bermuda and its zero corporate tax rate, with an intermediate stop in the Netherlands. Jim Stewart, a senior lecturer in finance at Trinity College’s school of business in Dublin, observed back in 2010: “You accumulate profits within Ireland, but then you get them out of the country relatively easily [.] And you do it by using Bermuda.”.**

Figuring this out took a bit of sleuthing.

The BEA transparently reports the dividends paid by the subsidiaries of U.S. firms in Bermuda and the Netherlands. Bermuda somehow managed to pay $229 billion—yep, $229 billion, 3600 percent of Bermuda’s GDP in 2017 [p.7]—in dividends back to the United States in 2018. The Netherlands paid another $140 billion.

Ireland took a bit more work, as the BEA suppressed the data on dividend payments from Ireland (see table 3) to protect the confidential tax information of a U.S. firm (likely Apple, but perhaps one of the pharma companies).*** However, the total dividends the Irish subsidiaries of U.S. firms paid to the United States can be inferred from other parts of the BEA’s foreign direct investment data. Take the total profit U.S. firms reported they earned in Ireland in 2018. That’s about $50 billion (around 15 percent of Ireland’s GDP). Add in the “negative” number that firms reported they “reinvested” in Ireland. Reinvested earnings in a tax haven used to be the funds that firms squirreled away in their subsidiaries‘ Treasury accounts so they didn’t legally have to pay U.S. tax on those earnings. A negative number on reinvested earnings thus is the cash drawn out of the firms offshore subsidiaries above and beyond what they reported to earn in that location. For Ireland, the negative number on reinvested earnings was about $85 billion (see “Reinvestment of earnings without current-cost adjustment”). Sum those numbers up and you have a plausible estimate for the dividend paid by the Irish subsidiaries of U.S. firms back to their parents (just over $135 billion).

That’s insane when you step back and think of it. Three small countries accounted for almost two thirds of the $775 billion in dividends U.S. firms paid back to their U.S. parents in 2018. It goes to show that you really cannot understand the U.S. balance of payments these days without understanding how deeply its details are distorted by the tax strategies of U.S. multinational companies.

This data also helps answer a second question: how much cash has actually returned in the first year of the tax law?

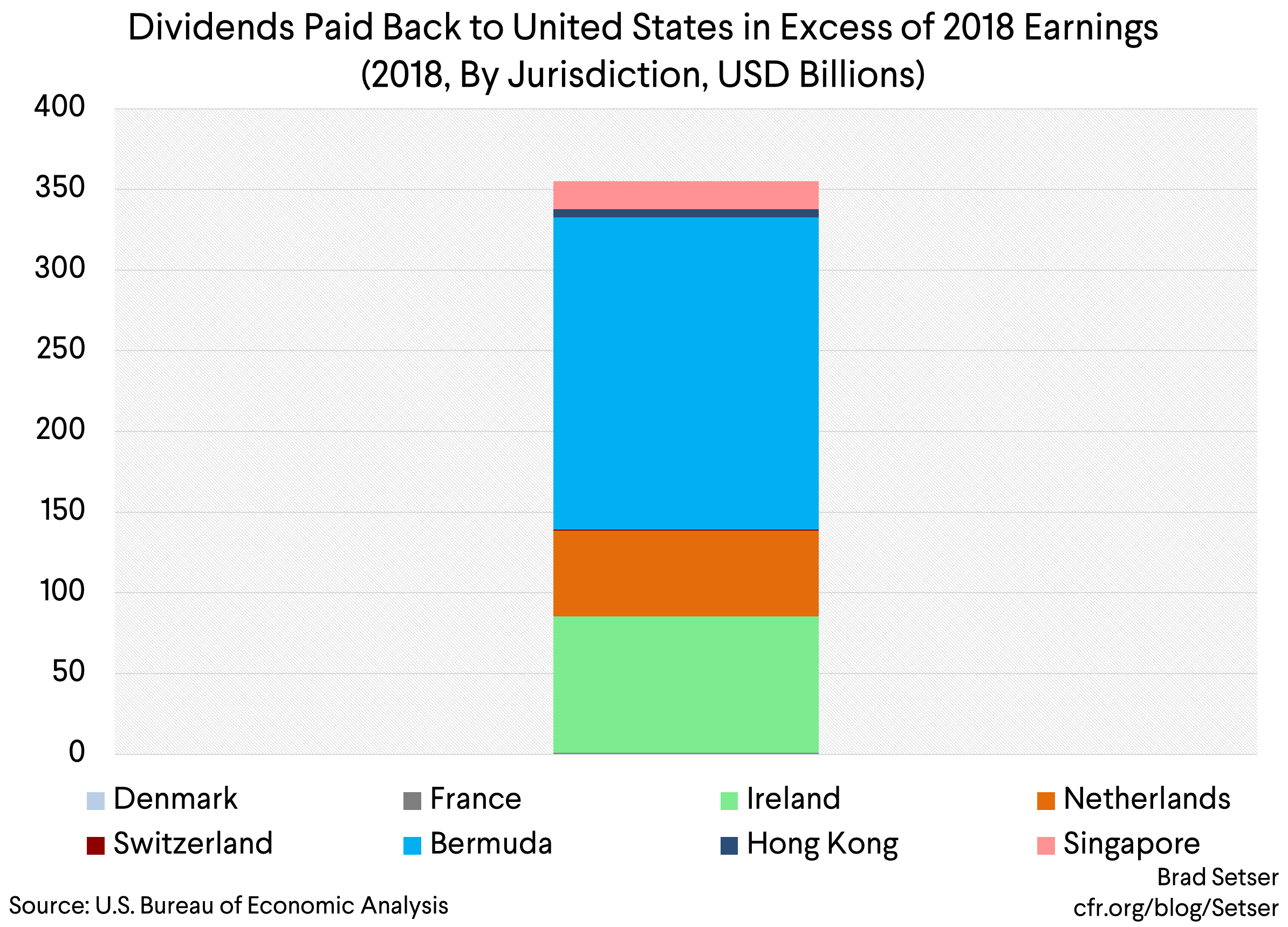

The answer I think, is about $350 billion ($355b).**** That is the “extra” dividend paid back to the United States from the offshore subsidiaries of U.S. firms. To get that number, I took the dividends paid by U.S. firm’s offshore subsidiaries in excess of the subsidiaries’ 2018 earnings in that jurisdiction. For example, the subsidiaries of U.S. firms in Bermuda paid $228 billion in dividends in 2018, while earning $35 billion there. That implies a $193 billion reduction in their cash balances.

Yep, Bermuda alone accounted for the majority of the cash returned to the United States in 2018. And all of the cash returned, more or less, appears to have come from five jurisdictions: Bermuda, the Netherlands, Ireland, Switzerland, and Singapore.*****

If you thought that funds were going to pour out of China or Germany to invest in the United States now that it has a more “competitive” tax rate, well, that just isn’t what is in the data.

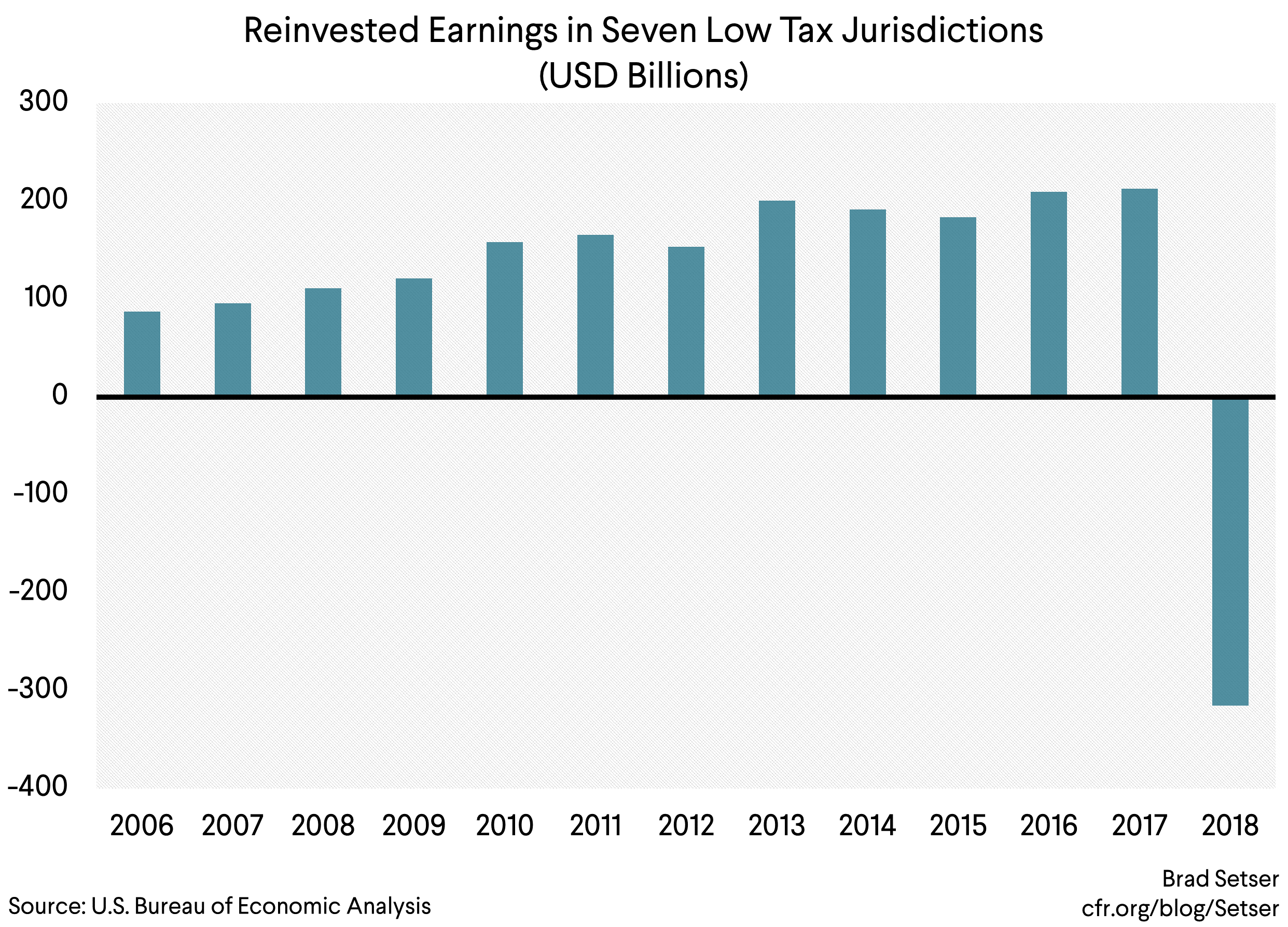

I used data from the reinvested earnings and income lines of the BEA’s interactive tables. But a similar number can be found if you look at the numbers for 2018 financial transactions by non-bank holding companies (column R in the spreadsheet on financial transactions). The $320 billion reduction in the financial assets of the “holding companies” U.S. firms have set up abroad also entirely explains the $90 billion overall fall in U.S. FDI abroad. U.S. firms continue to invest in real assets abroad.

There is one additional if somewhat very plodding result that emerges from this work.

After the tax reform, it looks like U.S. firms returned about $400 billion of the $530 billion they earned abroad in 2018 as dividends (almost 80 percent of the total) in addition to running down their existing cash balances by about $350 billion. This is a ball park figure, as some firms may be running down their cash balances in say France while others are adding to their real assets in France—generating offsetting entries in the aggregated data. But there is no question that the tax law did reduce the incentive to continue to accumulate large sums of cash in the offshore subsidiaries of U.S. firms. It just doesn’t seem to have changed the incentives that led firms to want to shift a large share of their “intangible” profits offshore. ******

Note: Edited slightly after posting for clarity, and to add a link to a 2010 Bloomberg article laying out Google’s tax strategy.

* The phrase was I think first used by the great Ann Richards, a former Texas Governor with a way with words.

** This is, for example, the tax strategy that Google has traditionally used, according to reporting by Jesse Drucker of Bloomberg back in 2010 and work by Gabriel Zucman and his colleagues. The Independent laid out the basics of this tax strategy clearly:

“Google Ireland collects most of the company’s international advertising revenue and then passes this money on to Dutch subsidiary Google Netherlands. A Google subsidiary in Singapore that collects most of the company’s revenue in the Asia-Pacific region does the same. The Dutch company then transfers this money on to Google Ireland, which has the right to license the search giant’s intellectual property outside the US. That company is based in Bermuda, which has no corporate income tax. The use of the two Irish entities is what gives the structure its “Double Irish” moniker and the use of the Netherlands subsidiary as a conduit between the two Irish companies is the “Dutch Sandwich.”

*** This sum could be more than just Apple. Apple only reports its total cash position now, not how much is offshore. I think Apple’s total cash position fell by 14 percent in 2018, from $285 billion to $245 billion. It though is possible that Apple shifted some of its legacy offshore profit back onshore (legally speaking) while continuing to hold it in cash or cash equivalents, which would produce a larger number.

**** U.S. firms earned around $530 billion abroad in 2018 while paying $775 billion in dividends. That implies a minimum reduction in their offshore assets of $245 billion. But that understates in my view the size of the funds that came home in 2018. American firms are still adding to their assets abroad in some jurisdictions, even as they reduce their assets in others. To estimate the reduction in the cash balance, it consequently makes sense to look at the fall in assets in those jurisdictions—typically the big tax havens—where we know American firms paid big dividends back to headquarters out of their accumulated past profits.

***** France and the Denmark technically added to the total, but that was basically a fluke, and the sums involved are trivial (less than a billion dollars).

****** Jesse Drucker (now at the New York Times) nailed it early last year: “Income earned abroad will be subject to federal income taxes at half that [21 percent] rate — 10.5 percent — and potentially even less. As a result, companies are likely to shift even more profits into tax havens — even if they want to use that money in the United States.”