Abenomics and the Long Legacy of the Consumption Tax Hike

Abe’s consumption tax hike stalled what until then had been a demand led recovery, leading to a three year period with no growth in domestic demand.

Both Noah Smith for Bloomberg and Matt O’Brien for the Washington Post —prompted I assume by the recent electoral victory of Prime Minister Abe as well as Trump’s trip to Japan—have written relatively positive assessments of Abe’s economic record:

Japan is certainly growing rapidly right now. And Japan also seems ready to experiment with running its economy a bit hot, with the goal of pulling more workers into the labor force (see Jay Shambaugh’s recent work on Japan’s success in raising their female labor force participation rate) and generating a bit more nominal wage growth.

But Smith and O’Brien still grade Abe’s most recent two terms a bit more generously than I would.

Abenomics undoubtedly has meant aggressive monetary easing—a massive expansion of the Bank of Japan’s balance sheet, and now an explicit targeting of long-term rates. There is some real innovation there.

But it in some key ways Abenomics also has been fairly orthodox.

Abe shifted the tax burden away from firms and toward households, cutting corporate taxes and raising the consumption tax. (This has some parallels with the Republicans‘ current tax proposals, as they provide larger tax cuts for firms than for individuals.)

Abe did this at a time when corporate profits were rising and corporate saving was high: while Japan has suffered from a “structural deficiency in consumer income,” Japanese firms were not cash constrained in any way.*

And, thanks in part to the consumption tax hike, Abe has done a significant fiscal consolidation over the last five years. Japan’s three plus percentage points of GDP in fiscal tightening between 2012 and 2016 is more than in either the U.S. or the eurozone over the same period. Abenomics consequently shouldn’t be synonymous with using all policy tools to stimulate the economy and spur growth; it has in a lot of ways been a fairly conventional effort to offset tight fiscal policy with monetary easing.

And a mix of tight fiscal/loose monetary policy has had the contractionary effect on internal demand that I would have expected in an economy where policy interest rates were already at zero when the fiscal consolidation started, and thus the scope for monetary policy to offset fiscal tightening was more limited.

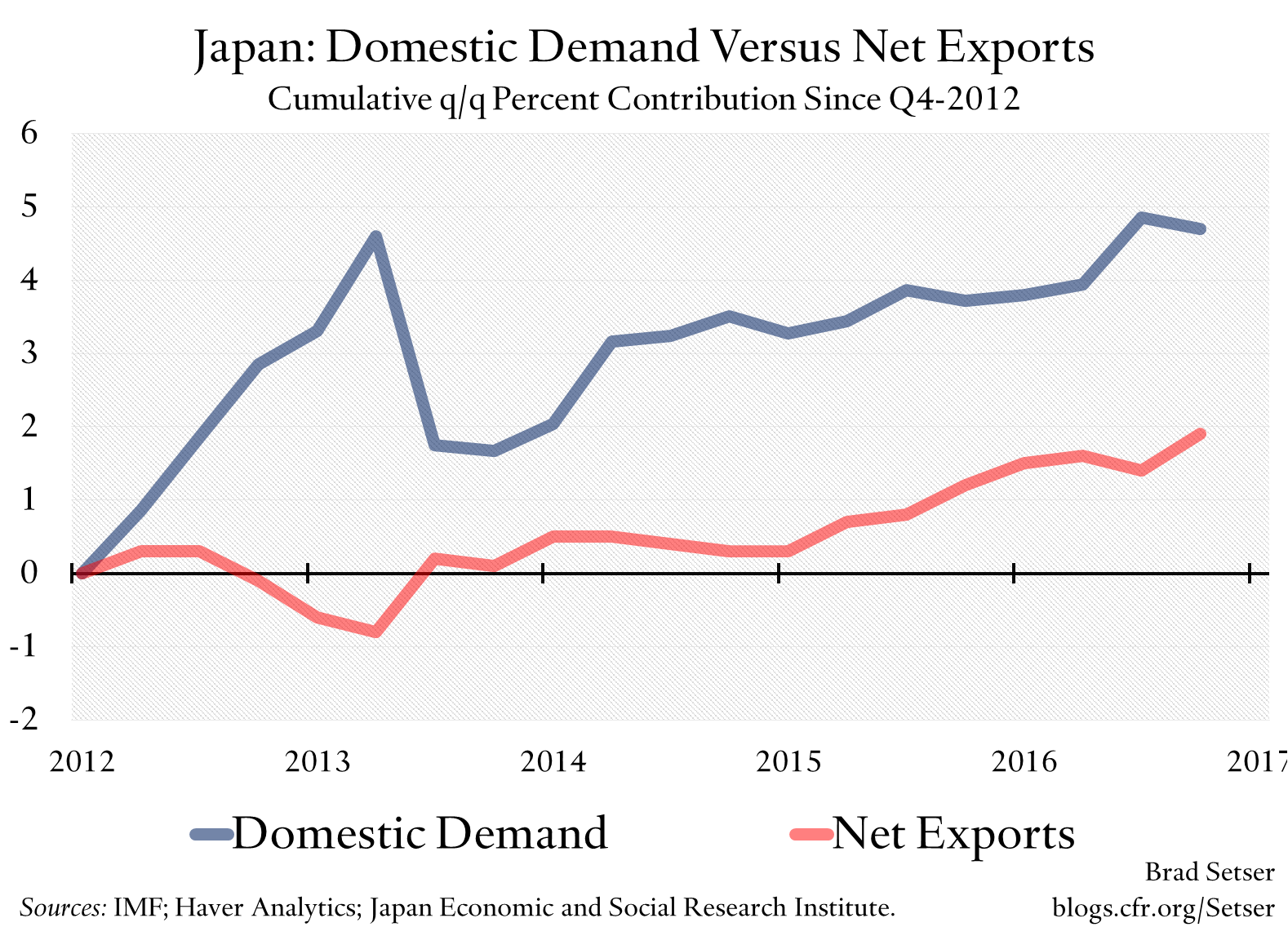

For three years—2014, 2015 and 2016—domestic demand contributed very little to Japan’s growth. Only the support of net exports kept Japan out of a three-year stall before this year. With much of the world economy operating below potential during this period, there was a strong case that Abenomics meant that Japan was exporting its secular stagnation—largely through the yen’s weakness—rather than helping to lead the world out of a liquidity trap through aggressive policy stimulus.

There was a perception that Japan’s economy was stagnant prior to Abe’s program of reform—a perception, I suspect, that is heavily influenced by the stagnation in the Nikkei.

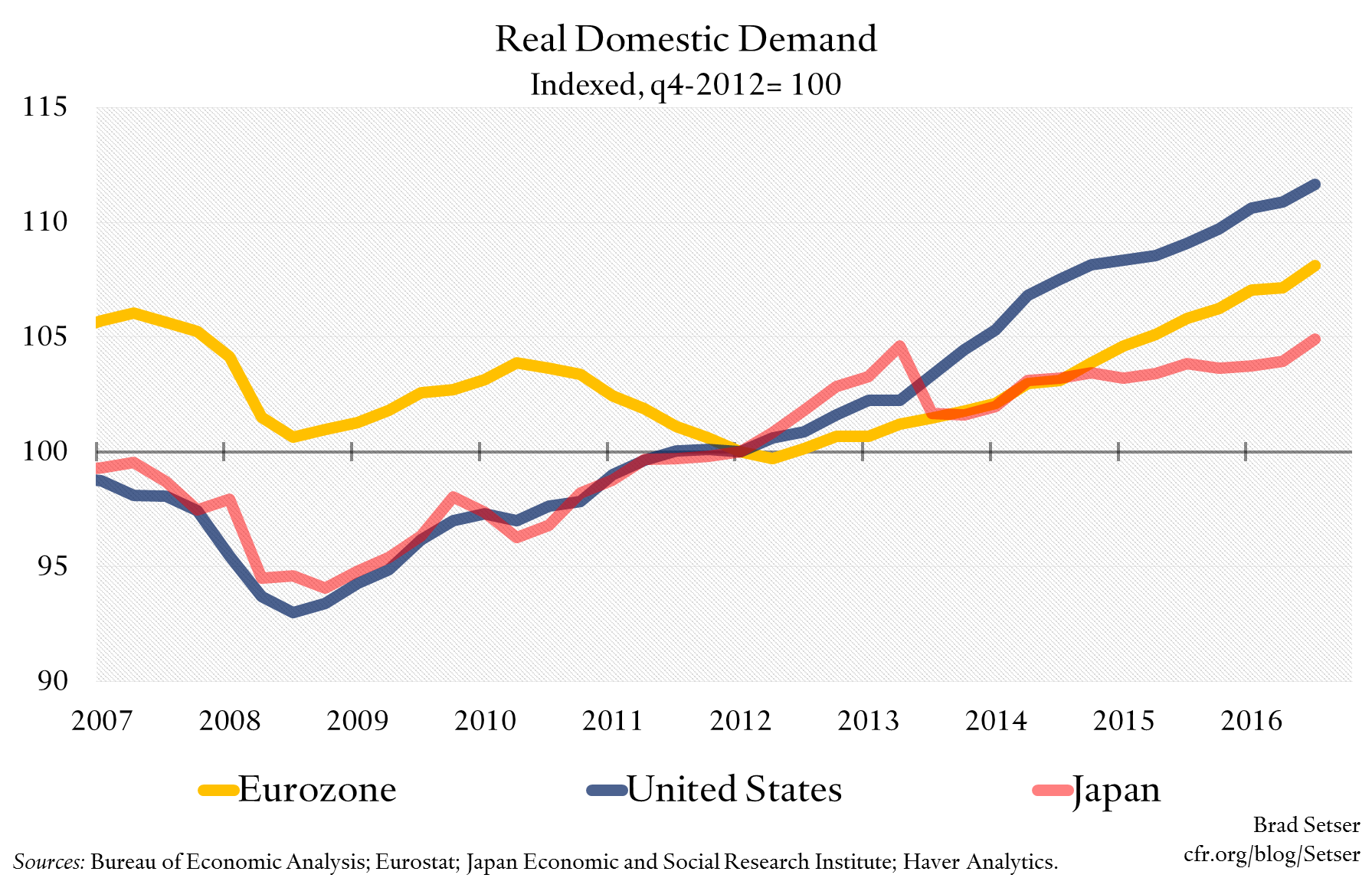

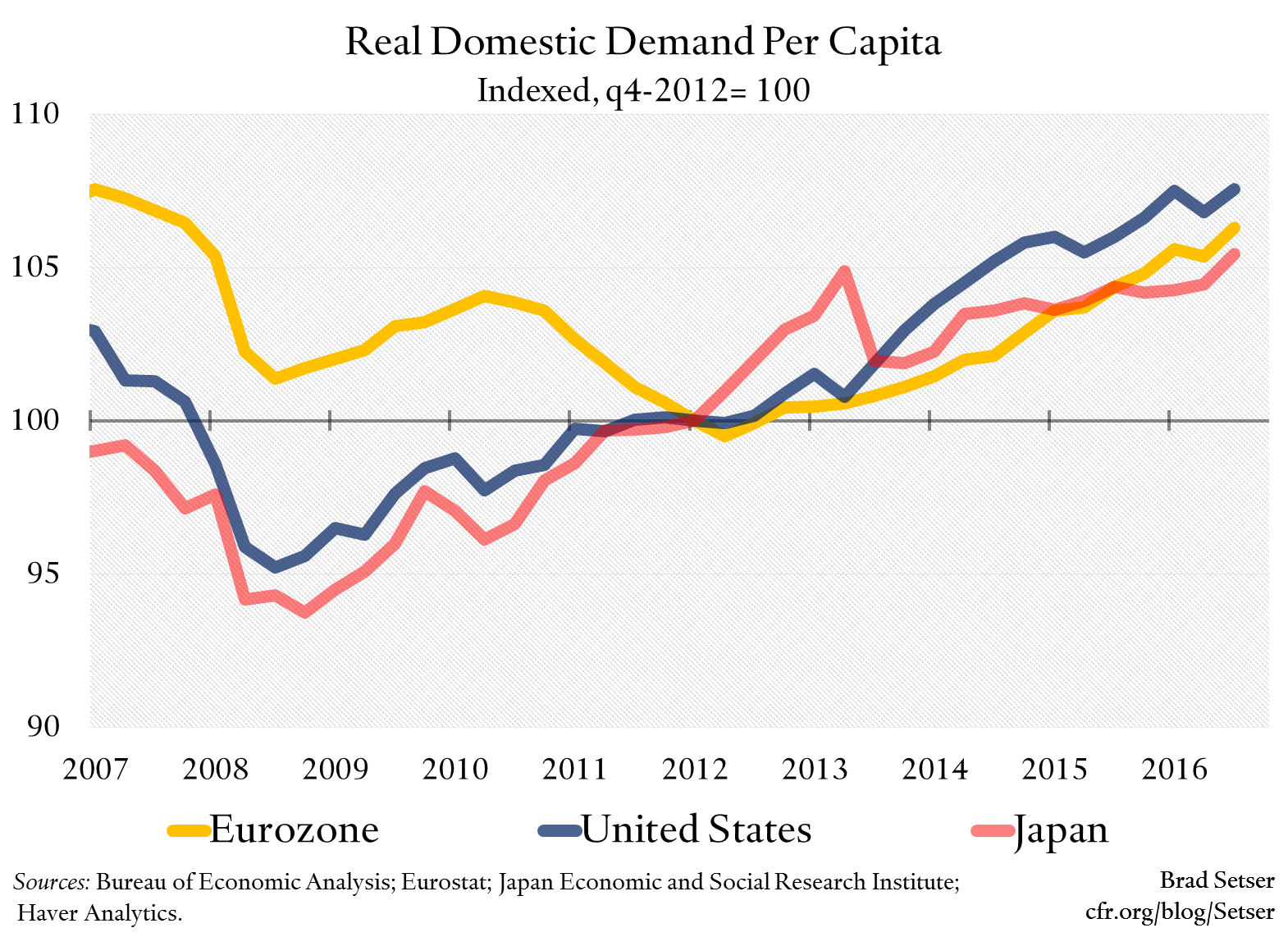

But it isn’t really true. After the global crisis, Japan’s demand recovery—on a per capital basis—kept up with the demand recovery in the United States. Europe was the real laggard. And, from the point of view of the world at large, Japan’s pre-Abe policy mix of loose fiscal and (comparatively) tight money was actually quite helpful. Unlike its neighbor Korea, which never really did any stimulus and instead relied on the weak won to support its growth, Japan clearly helped support the global recovery.

Japan’s recovery in internal demand did slow a bit in 2012—in part because Japan started to consolidate in 2012—before rebounding in 2013. But to me the real break comes in 2014—when the consumption tax hike broke the momentum of what until then had been a demand-led recovery

There is an argument to be made that Japan’s recovery before Abe relied on an unsustainable fiscal deficit, and that the growth in demand before the consumption tax hike was in some sense an unsustainable sugar high. I certainly think that Japan should have combined its post-crisis fiscal stimulus with a more creative monetary policy; there is no good reason why the BoJ didn’t join the Fed in balance sheet expansion (“QE”) back in 2010. But I also think pre-Abe Japan should get a bit more credit for making full use of fiscal policy to support a demand led recovery at a time when the global economy was short demand and the scope for monetary policy on its own to generate demand was limited. (One of the recommendations emerging out of the effort to “rethink” macro-economics is to rely more heavily on fiscal policy at the zero bound: Japan did so after the global crisis).

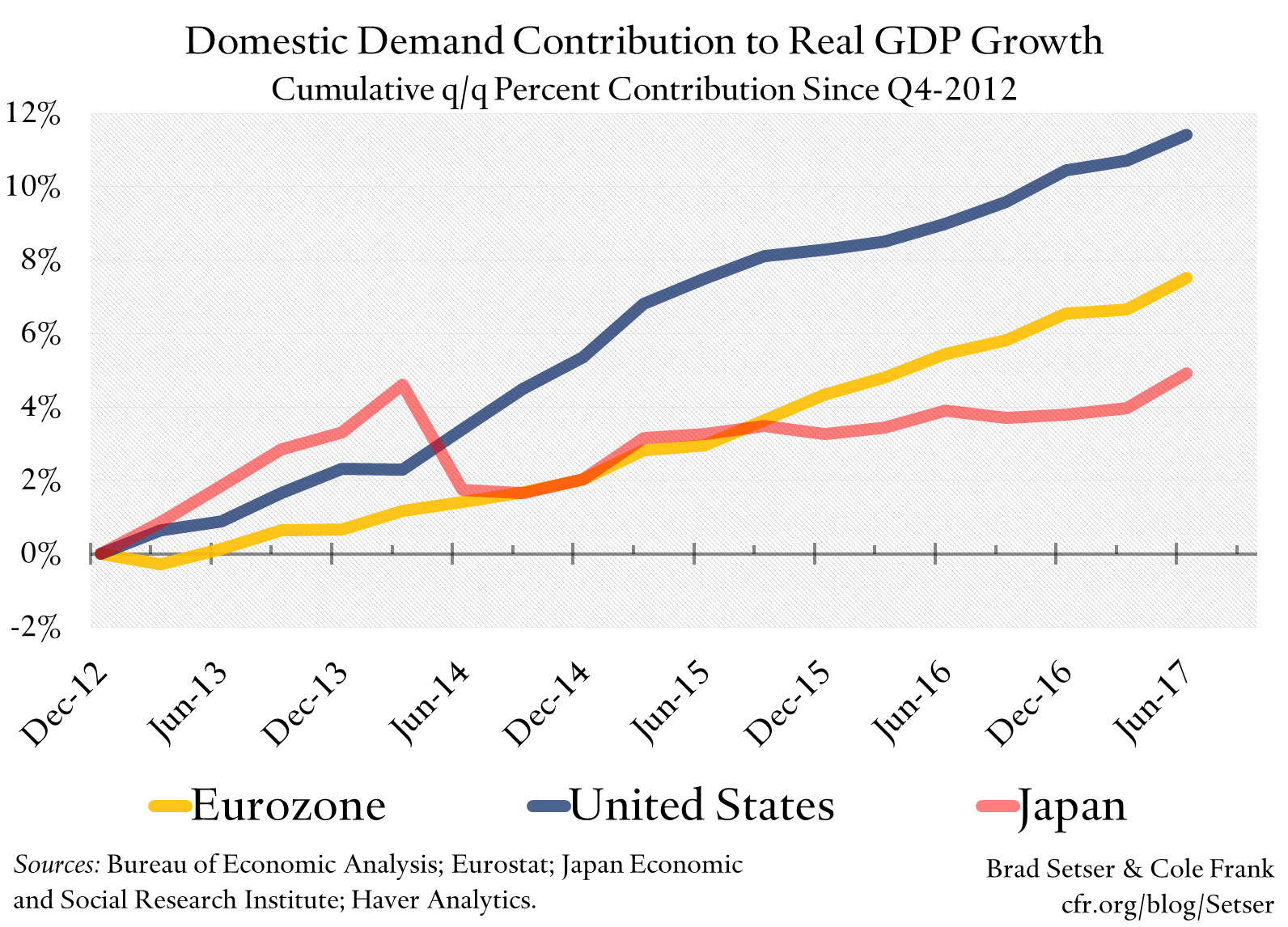

Matt O’Brien—citing Simon Cox of the Economist—notes that over Abe’s nearly five years in charge, domestic demand has accounted for over half of Japan’s growth.

That is true. But it also should not be a surprise. Over most periods of time, net exports tend to contribute—in a mechanical, growth accounting sense—very little to growth, as both imports and exports tend to rise symmetrically. A large, sustained contribution from net exports requires an ever-rising trade surplus, and that doesn’t happen all that often.**

All of the eurozone’s growth in the last five years has come from domestic demand, and, thanks to a one percentage point drag from next exports, overall U.S. growth has slightly lagged U.S. demand growth.

And, well, the bulk of Abe’s demand growth came way back in 2013—domestic demand contributed 3.7 percentage points to Japan’s growth in the four quarters that preceded the consumption tax hike, and 0.3 percentage points in the 13 quarters since.

Abe deserves some credit for strong demand growth in 2013. He did a small stimulus, which—at least in 2013—kept fiscal policy broadly neutral (Japan had stimulated demand through a series of temporary stimulus packages, which meant that new stimulus was needed to avoid a negative fiscal impulse) and monetary easing juiced the stock market and triggered a spike in luxury goods consumption.

But Abe also bears responsibility for deciding to go ahead with the planned consumption tax hike in 2014, and failing to effectively offset its negative impact on demand.*** The fall in demand was larger and more sustained than Japan’s cabinet office (or, for that matter, the IMF) forecast at the time. And after the consumption tax hike demand growth lagged most reasonable estimates of Japan’s potential growth until this year. Japan’s demand growth since 2012 now lags that of the eurozone by a considerable margin, even with the head-start from 2013.

As a result, Japan has gotten far more of its growth from net exports and less from domestic demand over the last five years than its G-3 peers.

Abe does deserve credit on one point: he doesn’t seem keen to repeat the same mistake twice. He hasn’t shown any real enthusiasm for a second consumption tax hike and now seems willing to give monetary expansion a bit more time to take hold and start to push up wages before moving forward with more consolidation.

*The consumption tax was always expected to pull demand from q2-2014 forward to q1, so the q1 spike in demand was pretty clearly “fake”: proponents of the tax hike though expected a rebound in consumption starting in q3-2014, which didn’t happen. Relative to pre-tax hike expectations Japan consistently under-performed. There is also an argument that some of Japan’s 2013 demand growth reflects anticipation of the 2014 consumption tax hike. I am a bit skeptical—in part because I don’t think it was clear for most of 2013 that Abe would go through with the consumption tax hike and in part because if looks like the surge in q1-14 was large enough to account for a significant share of the expected bump.

** For a sense of scale, the much-discussed China shock corresponds with a rise in the U.S. trade deficit with Asia of around a percentage point of GDP, and maybe a slightly bigger swing in real net exports. And conversely, during this period, domestic demand accounted for the bulk of China’s growth—the two to three percentage point contribution from net exports was absolutely large, but never accounted for more than a quarter of China’s growth.

*** There was an expectation that the shock of the consumption tax hike would be offset by more stimulus elsewhere, so the aggregate consolidation would be less than the 1.5 percent of GDP implied by a 3 percentage point increase in the consumption tax. Judging from the numbers in the national accounts on public investment and public consumption spending, that offset never materialized. The IMF’s total structural consolidation in calendar 2014 is 1.8 percentage points of GDP.