April U.S. Trade Data

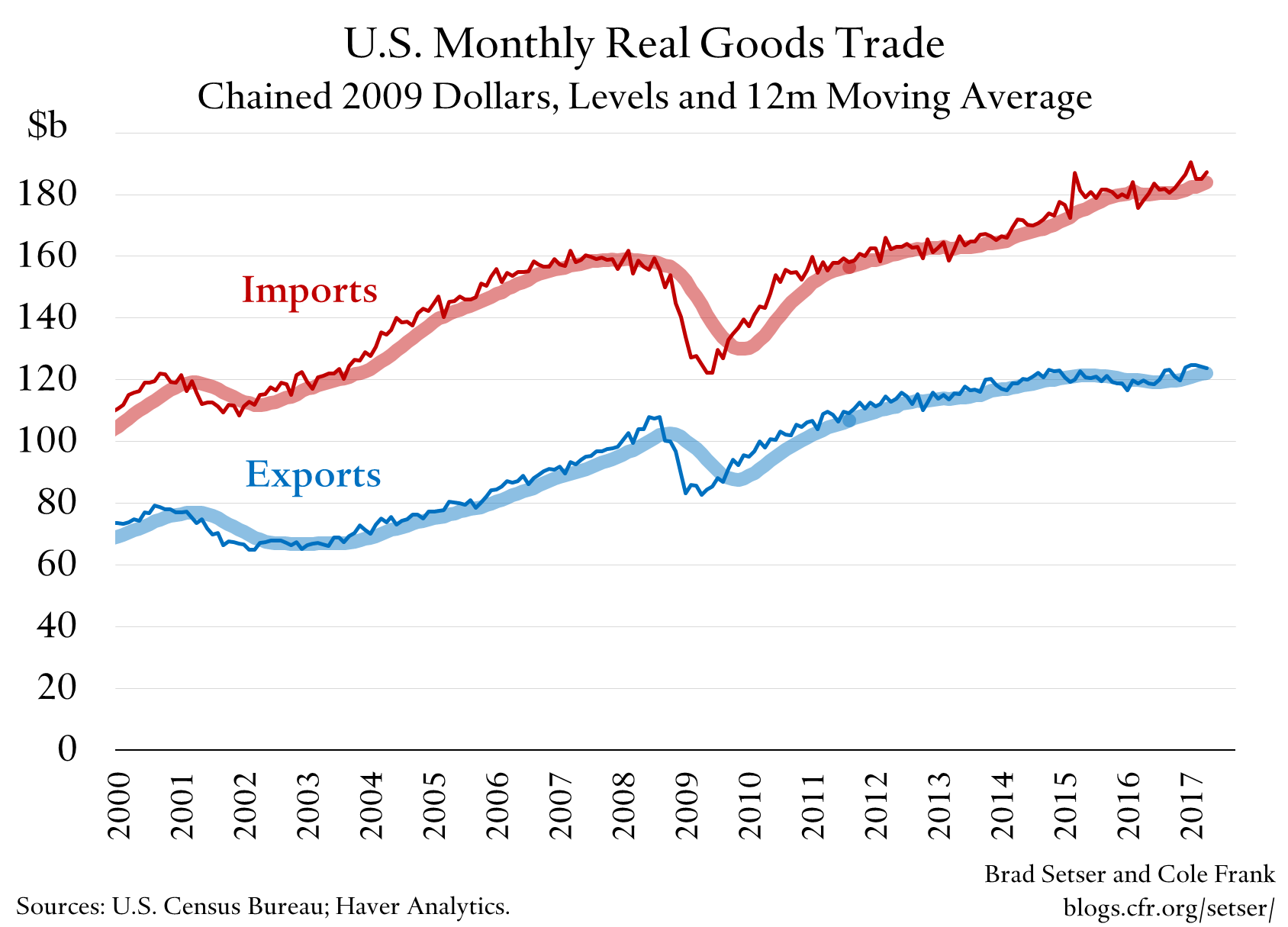

The U.S. trade deficit jumped in April—after staying roughly flat in the first quarter.

Real goods exports in April were just below their q1 average.

Real goods imports were a bit higher than their q1 average.

Given the volatility in the monthly data it is too soon to say much about how trade will impact q2 growth—but if both imports and exports stay at their April level, the drag will be noticeable.

I have a strong prior here—I expect the lagged impact of dollar appreciation in 2014 and 2015 to have an impact on the trade balance this year. The lags on exchange rate moves are long, and, well, I expect that weakness in investment and an inventory correction shifted some of the adjustment in imports that one normally would expect after a large currency move from 2016 to 2017.

A quick reminder: exports have responded more or less as expected to the dollar’s 2014-15 appreciation, imports have responded by less than would be normally be expected.

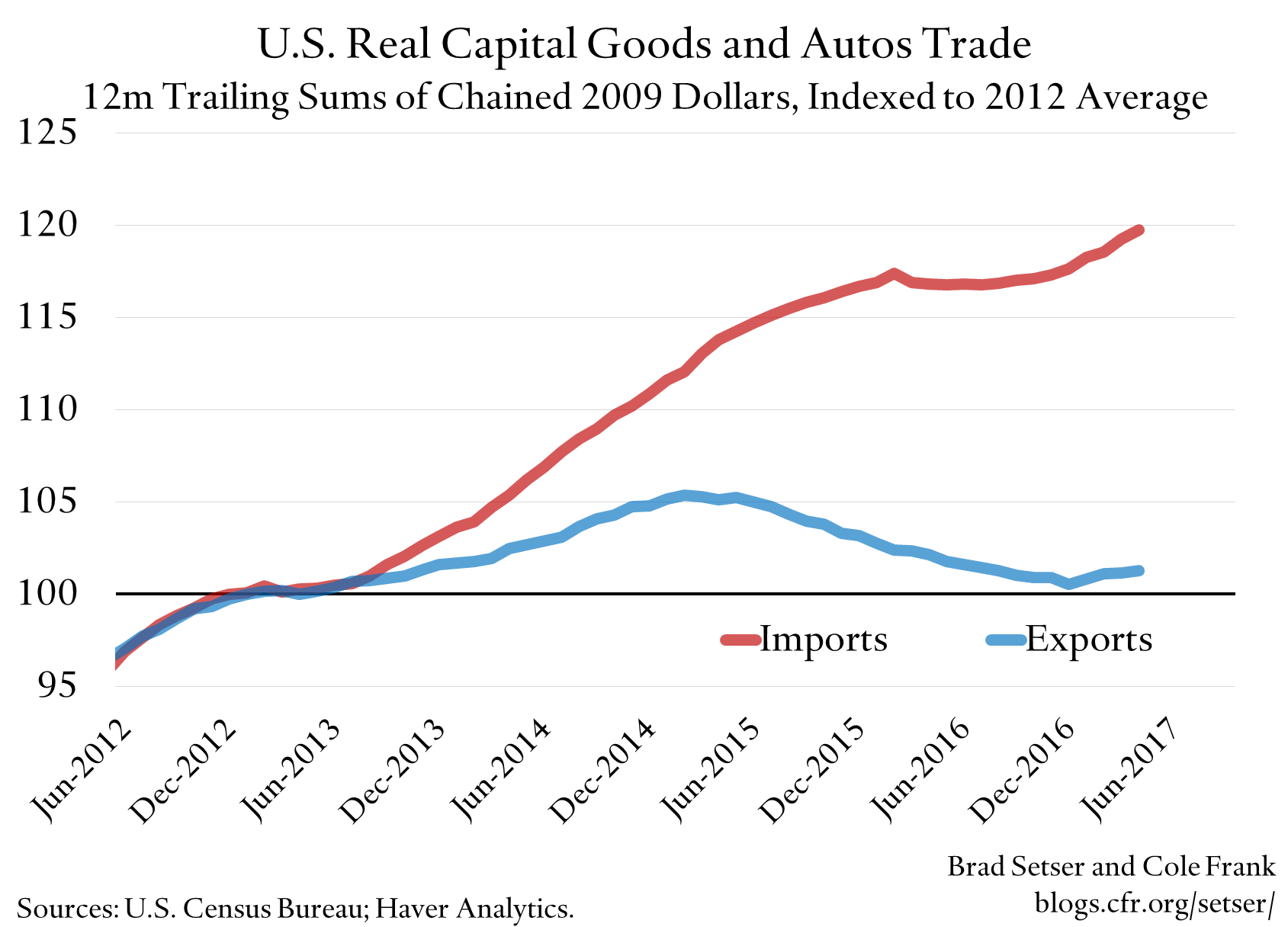

Imports though are growing at a decent clip now. Imports of capital goods are up (the graph shows the sum of capital goods and auto imports, but the dynamic is stronger in capital goods).

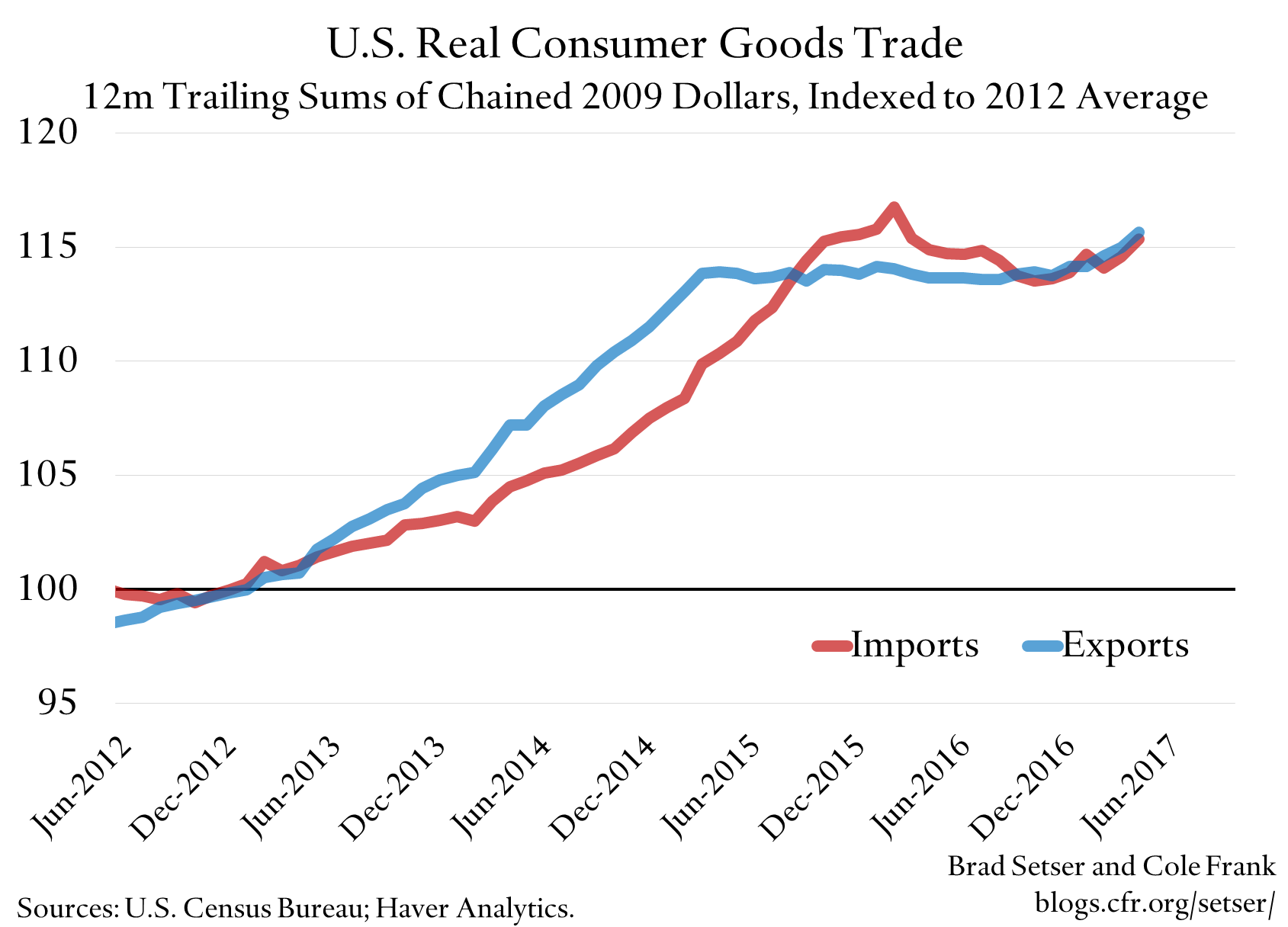

And consumer goods imports are growing again.

Given that the U.S. imports far more goods than it exports (especially if you look only at manufactures), similar rates of growth imply an expanding deficit. (The monthly data on services, apart from the tourism numbers, is based on a lot of estimates and tends to be revised; it thus lacks the information content of the goods data).

Looking at the bilateral data now almost feels like a political statement.

I confess that I find the bilateral numbers useful—though I certainly do not think the bilateral balance should be the target of policy (the “port” effect on the bilateral is real—look at the U.S. surplus with Singapore and Hong Kong and the Netherlands. I generally combine U.S. exports to China and Hong Kong for just this reason). The bilateral data can help confirm broader themes.

For example, the rise in the U.S. bilateral deficit with China—even with nominal export growing at a decent year-over-year clip—is an illustration of the broader pickup in U.S. goods imports.

Nominal U.S. imports from China are up 7 percent by the way (year to date 2017/ year to date 2016), and they appear to be once again rising faster than the overall growth in capital and consumer goods imports. Evidence, perhaps, of a lagged response to the 2015-16 depreciation of the yuan?

The U.S. numbers on imports from China are consistent with the overall strength in China’s exports in the Chinese data: Chinese monthly export volume growth this year has averaged 8 percent, and real goods exports were up 7 percent (y/y) in April. This is a bit faster than April growth in Chinese import volumes (import volumes though were up enormously in q1). I will be interested to see if May confirms this as a trend.

U.S. exports across Asia are also growing strongly, pulling the headline U.S. bilateral deficit with countries like Korea and Japan down. That tells a couple of stories. Nothing much looks to be happening on U.S. exports of manufactures. But commodity exports are way up, both in nominal and real terms. Exports of agricultural products to Korea are up something like 50 percent (more for oilseeds), exports of ores are up something like 100 percent and exports of petroleum and natural gas are up even more. The pattern with Japan is similar.

The fall in the bilateral balance with Japan and Korea is thus a reminder that that the U.S. is a major exporter of commodities, especially to Asia—and that exports of petroleum and natural gas now can have a significant impact on bilateral balances (even as the U.S. continues to be a net importer of oil and gas and thus the overall trade balance is hurt by a rise in the price of oil).

U.S. exports to China and Hong Kong are also growing at a decent clip, for much the same reasons — and gold exports to Hong Kong also seem to be up. Two cautions though. Aircraft exports to China in q1 were weak. That didn’t have much of an effect on the year over year comparison because aircraft exports to U.S. China in q1 of last year were also weak. I don’t know what Boeing’s delivery schedule looks like for the rest of the year, but if aircraft exports do not quickly return to their levels of late last year, aircraft will start to pull the year over year numbers down. And, well, the soybean harvest in Brazil has been good. Prices are running a bit below their levels during the U.S. harvest last year as well ...