Are Asian Insurers the New European Banks?

It is hard to understand the global flow of funds without understanding the risks now being taken by Japanese, Taiwanese, and Korean life insurers.

Asia’s insurers have become big buyers of U.S. bonds.

That makes sense. Insurers are classically patient investors—life insurers in particular need assets that pay off over a long horizon to meet their promises.

But in a low rate world where Asian insurers cannot make money at home, they are increasingly taking on the same kind of risks that banks do. Rather than borrowing short and lending long they hedge short and invest in long-term bonds. Their hedging strategy in turn makes the insurers sensitive to the shape of the U.S. yield curve—the cost of hedging is closely linked to the cost of short-term borrowing. With a flat curve, Asian investors either need to take on more credit risk to make money on their foreign currency books—or to stop hedging and take “naked” currency risks.

There consequently should be new concern about the potential buildup of financial risk in their portfolios.

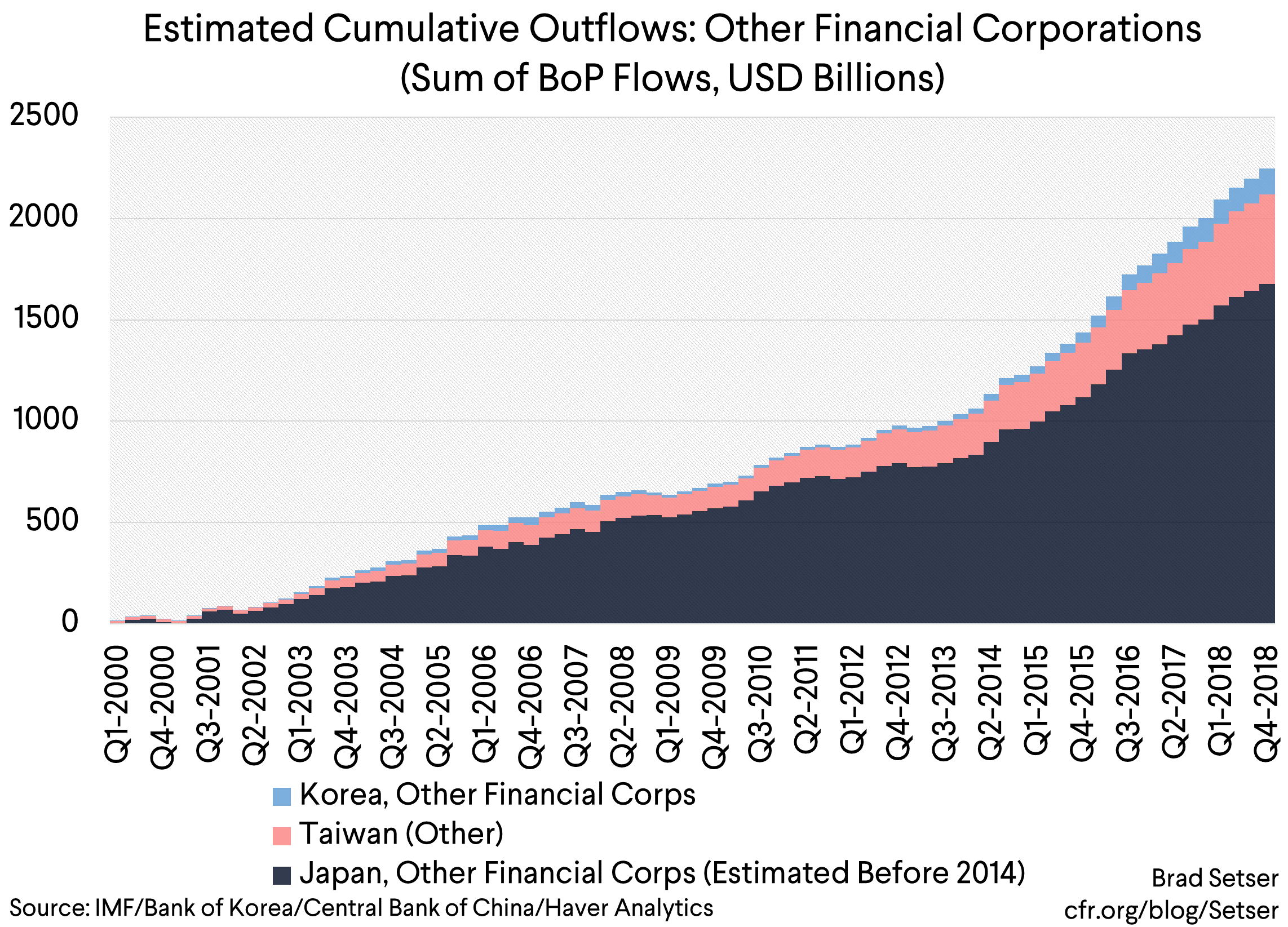

Especially in a world where Asian insurers—and other non-bank financial institutions—keep adding to their holdings of foreign assets. Asian insurers and a few other financial institutions have bought over $2 trillion in foreign bonds over the last twenty years, with a rapid run up in total holdings over the last five or six years.*

And relative to the size of their “home” economies, the exposure is starting to become significant—nowhere more so than Taiwan, where the life insurance industry holds an estimated $550 billion in foreign assets, a sum that is approaching 100 percent of Taiwan’s GDP. For Japan, the data above shows a broader set of institutions—but the life insurers hold around $1.6 trillion, a sum that is around a third of GDP.

How Insurers Started Taking on “Banking” Risk

Banks, classically, borrow short and lend long. They make money by taking a credit spread, but also benefit from the “typical” upward slope of the yield curve.

European banks—before the crisis that is—ran big wholesale funded dollar books, borrowing dollars from money market funds and big reserve managers, and swapping euros for dollars through the swap market. And they put those funds into risky U.S. asset backed securities—private label securitizations (which repackaged subprime mortgages and home equity lines of credit and the like), and the infamous “synthetic CDOs” (derivatives written on securitized subprime). That created a tremendous vulnerability when doubts about the quality of their dollar assets led the “wholesale” market for short-term dollar funding to dry up (See Brender and Pisani).

Insurance companies aren’t typically thought to run the same type of risk—as they don’t typically borrow short-term funds in the same way as banks (setting the Anbang’s of the world aside). Classically, insurers only need to worry about the absolute yield they can get on long-term assets, not their access to short-term financing.

But that changes when insurers cannot get the returns they want (or need) at home, and they start investing abroad in a quest for yield. Japanese life insurers (and for that matter Post Bank and Nochu) have looked abroad because yields at home are zero, and Japanese firms (in aggregate) don’t need to borrow. Taiwanese and Korean insurers have looked abroad because rates at home are relatively low—and there simply aren’t that many Taiwanese or Korean long-term government bonds to buy.

When life insurers invest abroad, they often “hedge”—and generally they hedge their foreign currency risk with short-term contracts. Those contracts in effect create a form of rollover risk, as the life insurance company is counting that their short-term “hedges” can always be renewed. As a result, life insurers who invest a large share of their assets abroad end up engaging in a form of maturity transformation, as they manage their foreign currency risk with short-term contracts while investing in long-term and often illiquid bonds abroad.

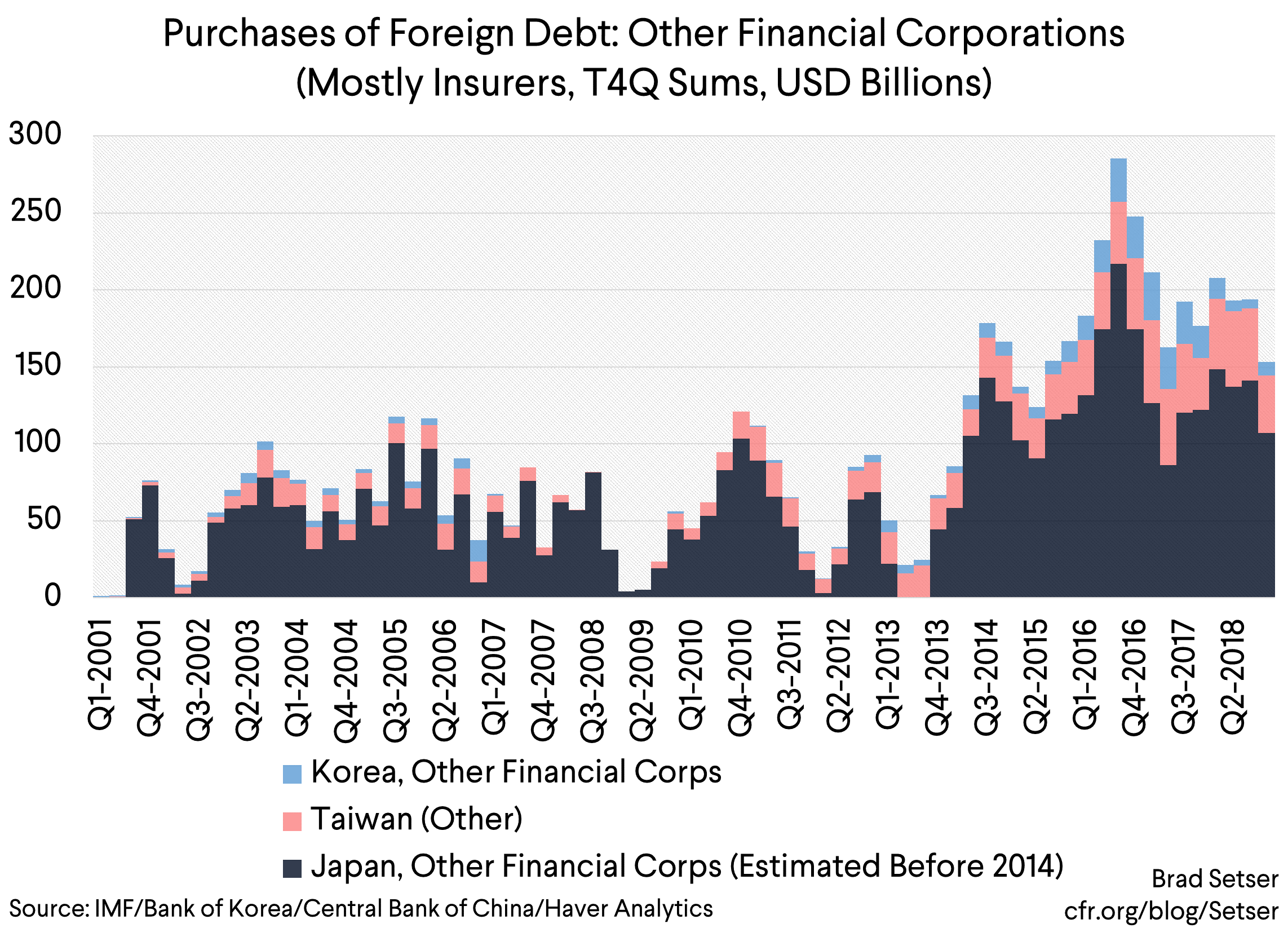

Asian insurers were certainly dabbling in foreign currency assets prior to the global crisis. But their purchases really picked up in the last five or so years—going from $50 to $100 billion a year to $150 to $250 billion a year.

There are a host of reasons for this rise. Taiwan loosened up some regulatory limits on foreign currency exposure. Japanese lifers reacted to Kuroda’s asset purchases (which reduced the supply of JGBs in the market) and yield curve control. And Korea joined the party in 2015, when Korean regulators allowed insurers to hedge with contracts under a year (previously the hedges needed to be longer-term for the assets to be considered long-term).

Total foreign purchased bonds by Asia’s “other financial institutions” have topped $1 trillion over the last 5 years. That kind of flow is big enough to impact the market, especially as it has often been directed toward less liquid parts of the bond market.

There is also a macroeconomic story that goes with these flows—Japan and the Asian NIEs run a large combined current account surplus. That current account surplus by definition means these countries are building up financial claims on the rest of the world. In the past almost all of the resulting financial outflow would come through the buildup of reserve assets and on the balance sheet of various sovereign funds—Japan’s GPIF, Korea’s National Pension System, and Singapore’s GIC. Right now though official outflows fall short of the region’s current account surplus—and consequently we know from the balance of payments that there should be a private outflow from Asia.

And it used to make financial sense too, in a way.

Japanese yields have been zero across the yield curve, which created an incentive for life insurers to reach for yield abroad. Particularly back when the hedged yield on dollar bonds used to exceeded the yield on Japanese government bonds.

Taiwanese yields are too low for the Taiwanese lifers who have promised a relatively high return to their domestic savers, pushing Taiwanese insurers abroad (there also just aren’t that many Taiwanese bonds out there).

Korean insurers needed long-term bonds to better match their long-term promises, and they could find those long-term assets more easily abroad (at least so long as the regulators didn’t focus too much on the fact that these bonds were hedged with short-term contracts, and thus long-term yields weren’t really locked in; see box 3 of Korea’s June 2018 Financial Stability Report).

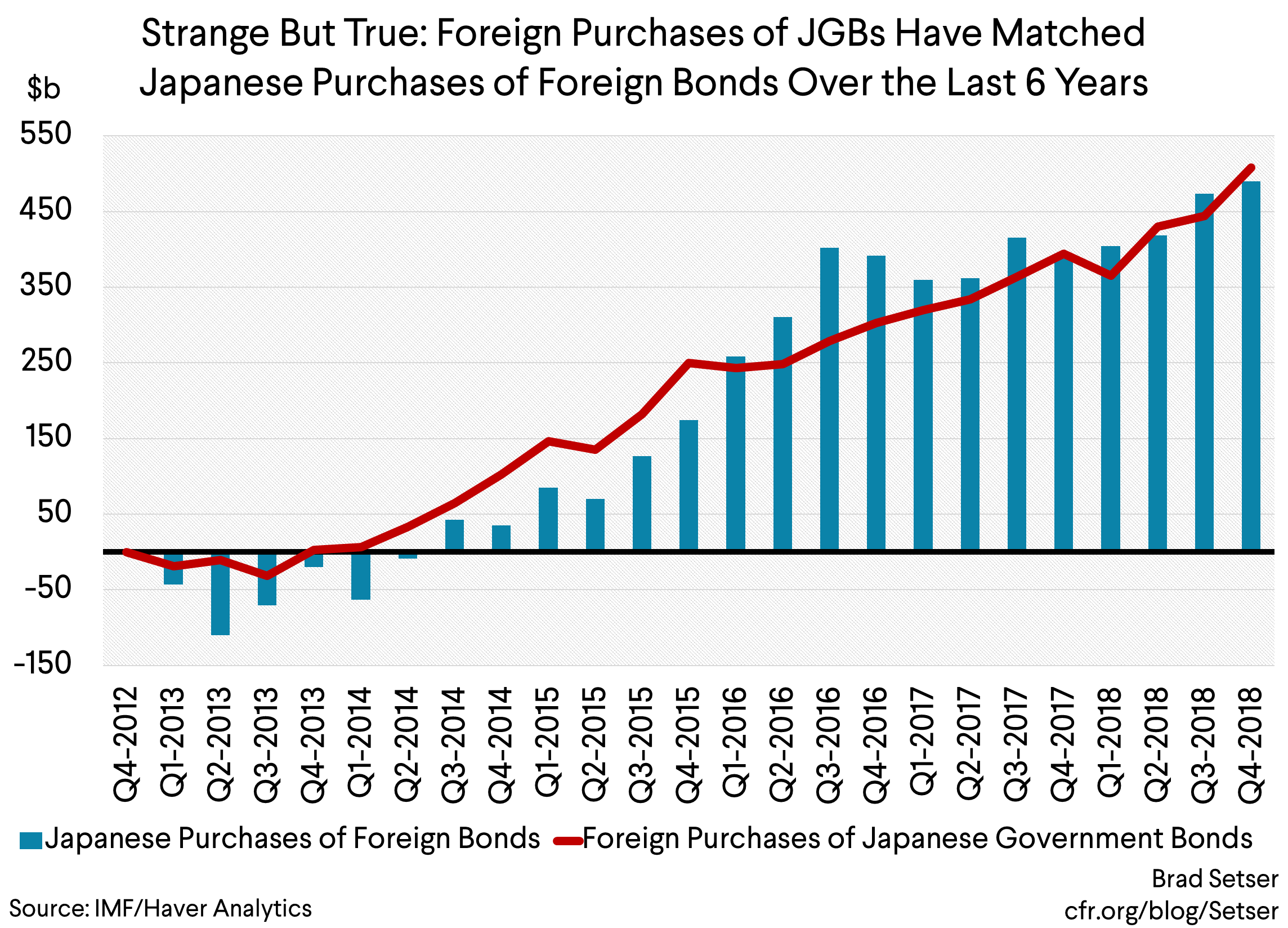

That all combined has made Asian insurers big users of cross currency swaps (see Chart III-2-3 and especially chart IV-3-6 in Japan’s April 2018 Financial System Report; Chart IV-3-6 shows that “institutional investors” – a category that includes Post Bank and Norinchukin as well as the lifers, had a trillion dollars in FX swaps and other hedges in 2017). Such swaps essentially allow the insurer to borrow dollars short-term (they get the dollars by swapping yen, won, or Taiwanese dollars for U.S. dollars). The insurer then buys long-term bonds, and collects the difference between its cost of dollar funding (swap/ hedge) and its long-term assets.

But this all also means that many insurers suddenly starts to look a bit like a bank. Or even a bank engaged in rather extreme levels of maturity transformation. Relatively few banks use 3 month deposits to “fund” a portfolio of 30 year bonds, but some insurers do use 3 month cross currency swaps to hedge very long-term bond portfolios.

And one strange result of these cross-currency swaps has been that investors who provide dollars to Japanese financial institutions end up with yen, and they in turn have been been big buyers of zero-rate Japanese bonds (they get paid to do the swap), a point that was first brought to my attention by the blogger Concentrated Ambiguity.

How Fed Tightening and the Flattening of the Curve Upset the Asian Apple Cart

The Asian insurers’ strategy hinged in large part on an upward sloping U.S. curve—it was part of a global search for “steepness.” Borrowing (hedging) short and lending (or investing) long only works if there is a term premium.

And, well, there isn’t anymore.

That poses a problem for the Asian insurers.

Some have responded by buying U.S. bonds unhedged.

Others have scaled back their hedging as it became difficult to make a return (at least a large return) on a fully hedged book. Taiwan’s insurers and Nippon life for example.

And others have been taking more credit risk, emulating, in a sense, the strategy of “Nochu”—a Japanese cooperative bank for fishers and farmers that has become the world’s largest source of demand for collateralized loan obligations (which have a floating interest rate). Nochu generally buys on a hedged basis, and with floating rate obligations, it isn’t taking on a duration mismatch—it is just taking on credit risk, and the risk that it might face a state of the world where it cannot rollover its hedges.**

That all feels similar to what European banks were doing prior to the global financial crisis. Back then European banks were running up their holdings of dollar securities. Those holdings were “funded” by taking in short-term dollars—whether by collecting dollar deposits from the world’s big central banks, selling short-term paper to U.S. money market funds, or swapping euros for dollars in the cross-currency swap market. And they kept buying even as the curve flattened.

The banks were then left doubly exposed when conditions turned. They needed short-term funding, which they couldn’t get. And the value of the long-term assets that they had bought with their short-term funds was plummeting, so they also needed capital. Especially as the market for complex mortgage backed securities dried up, so the banks really couldn’t sell their assets into the market easily. They needed to be able to ride out the worst of the crisis…something that they could do only through a combination of central bank dollar funding (direct from the Fed, and through the famous swap lines) and the willingness (at the time) of European governments to inject capital into their banking system.*

Asian insurers are actually now taking on those risks plus a certain amount of outright currency risk—those insurers that have reduced their hedge ratio would take losses if their home currencies ever were to appreciate against the dollar. They consequently would need to rollover the hedged part of their book even as they were taking losses on their unhedged book that reduces their capital.

The Financial Stability Risks Are Fairly Obvious

It isn’t that hard to figure out that Asia’s insurers are taking on a new set of risks as the size of their foreign bond portfolio rises. But domestic regulators in the “source” country are conflicted. Their insurers would face an immediate problem with their income if they were not able to buy foreign bonds. In fact, in Taiwan, it is a bit worse than this—the regulators have allowed the insurers to hedge less as the cost of hedging increased to help the insurers keep their income up. And in Taiwan’s case, the “equilibrium” is one where the insurers need to keep adding to their risk to keep the game going, as the Taiwan dollar likely would appreciate without the unhedged outflow from the insurers. At least absent of intervention by the Central Bank of the Republic of China (Taipei).

So I hope the global regulators in the countries that are the destination for these flows are also taking notice.

* That said, in one sense, the Asian insurers aren’t analogous to European banks. Europe didn’t hold that many reserves going into the crisis, while most Asian countries aren’t short reserves. That means their central bank could be the dollar lender of last resort (or hedge counterparty of last resort) to their insurers even without the help of the Fed and its famous swaps lines.

** Concentrated Ambiguity provided an excellent, highly detailed overview of Asian institutional demand for U.S. bonds in a post last summer.