Can Korea Provide a New (Fiscal) Model for North Europe’s Twin Surplus Countries?

Korea looks to be doing a real stimulus. Other “twin surplus” countries should too.

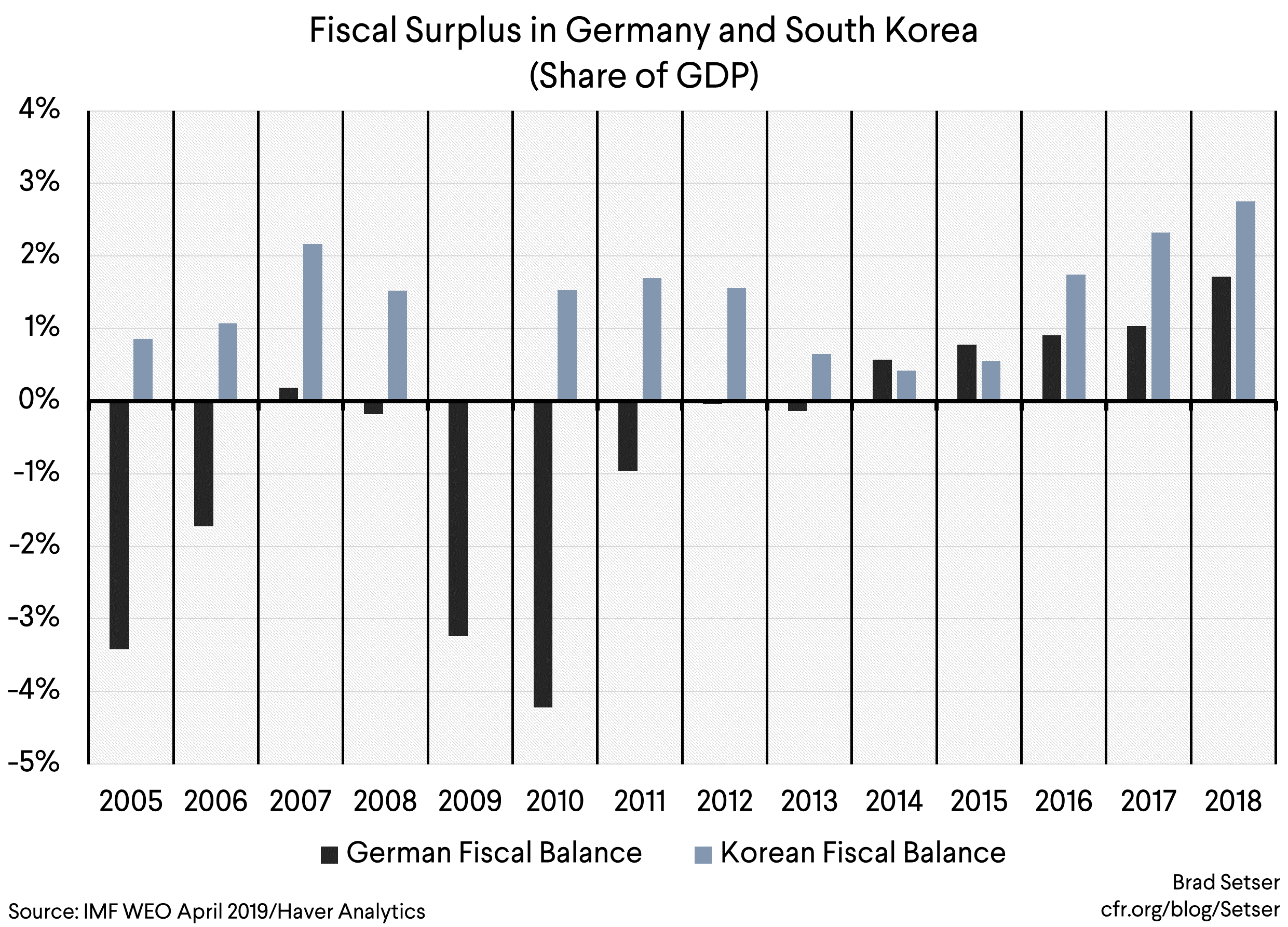

Korea has long been the “Germany” of northeast Asia.

China and Japan responded to the global financial crisis of 2008 with significant fiscal stimulus. Japan withdrew that stimulus a bit too fast, but it was hardly alone there.

Korea? Not so much…

Its general government fiscal balance never went into deficit.

And it was very quick to withdraw the roughly 1 percent of GDP fiscal stimulus it did in 2009.

It was also intervening heavily in the foreign exchange market to keep the won weak immediately after the crisis, so its crisis recovery plan basically consisted of growing on the back of exports—something that I have long thought should have attracted more criticism. And more recently it has adopted a policy of diversifying the assets of the National Pension Service away from Korea, a policy that has helped keep the won weak.*

Korea also has a long record of announcing “fake” fiscal stimulus. The government would propose a temporary increase in budget spending—but if you read the fine print, there was no net increase in borrowing, as the extra spending just offset the roll-off of last year’s temporary stimulus.

The most recent budget though looks to be different. Korea is proposing an increase in spending at a time when revenue growth hasn’t been buoyant. There (reportedly) is an actual increase in the government’s borrowing need. The government is planning to issue 60 trillion won of Treasury bonds next year, a good sign.

The deficit of the central government doesn’t assure a general government deficit, as the general government balance is the sum of the structural surplus in the National Pension Service and the “headline” or on-budget deficit of the central government. But some investment banks are projecting that the general government might move into a small deficit next year, which would be quite a swing from Korea’s general government surplus of over two percent of GDP in 2018.**

Korea certainly has the fiscal space to respond aggressively to the global manufacturing downturn. Net debt has been falling rapidly. The “general” government has been running up its external assets rapidly. That’s what happens if your $600 billion government pension fund is investing heavily abroad while you continue to hold over $400 billion in reserves (counting forwards).

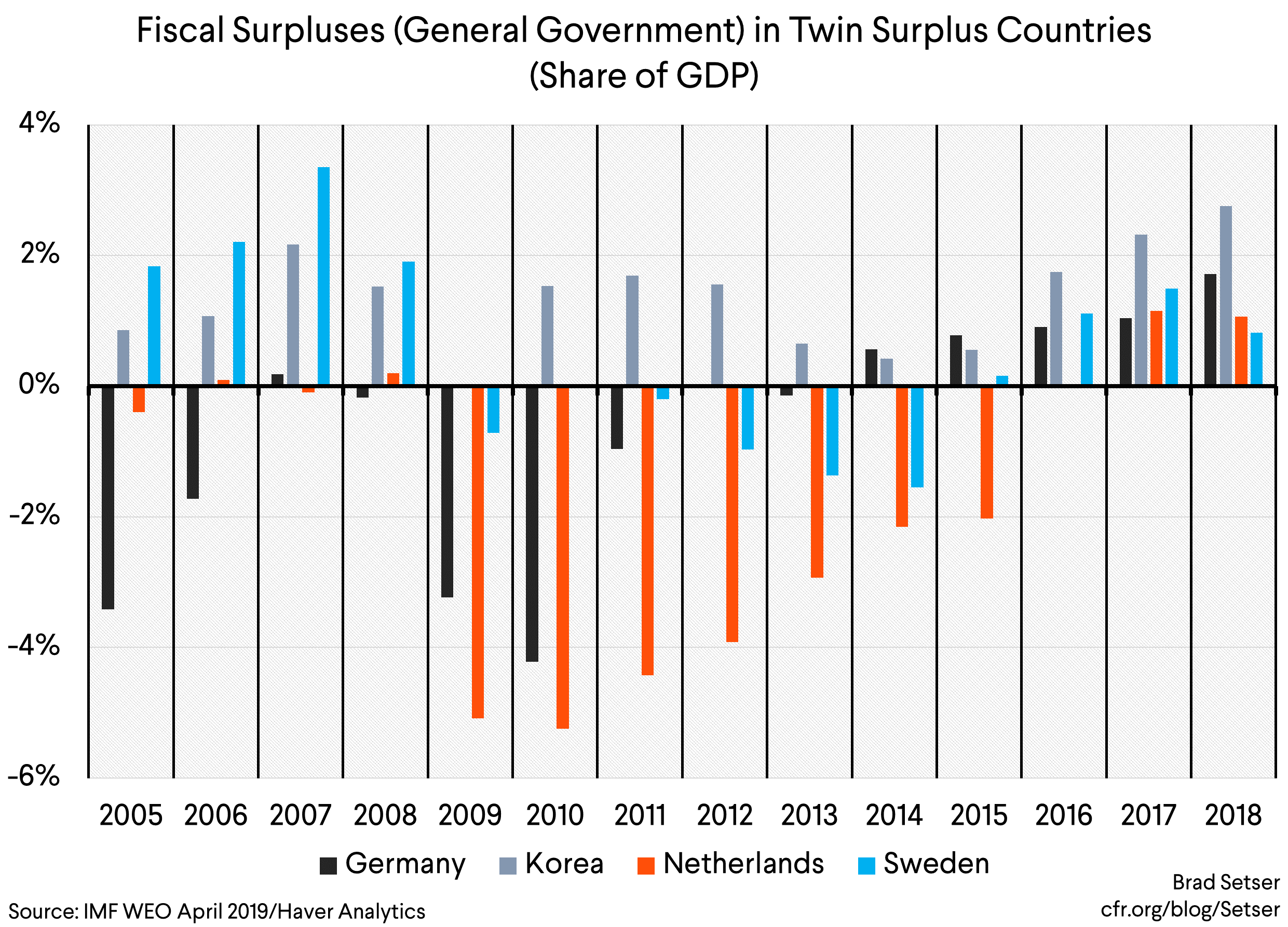

One can only hope that the export dependent economies of northern Europe that are now experiencing a slowdown take notice.

There is no economic reason why Germany, the Netherlands, and Sweden—all countries with falling gross (and net) debt to GDP ratios and fiscal surpluses need to avoid fiscal deficits right now. They obviously have fiscal space, and should use it to counter the current downturn.

Tight fiscal stances are putting extreme pressure on monetary policy.

They are depriving investors around the world of safe euro denominated assets, and effectively pushing them into the dollar (and Treasuries) to get a bit of default risk free yield.

And they are holding back the economies of the countries running them, which now need to rely on domestic demand—not exports to the United States, or for that matter the United Kingdom.

President Trump and Prime Minister Johnson have in their own ways both made that clear…

* The U.S. analogue would be a social security trust fund that was running a far larger surplus than the social security system ever actually ran, with the U.S. government then investing a very large share of the surplus in the social security system in foreign assets. Come to think of it, no one should give the Trump administration any ideas…as the social security trust fund still has some assets, and diversifying them globally would be a way of solving the Exchange Stabilization Fund’s “firepower” problem…

** I have criticized the IMF for advocating a global fiscal consolidation at a time when nominal and real rates globally are low. But on Korea, the IMF recently has been on the side of more spending and more stimulus, not less. Its most recent Article IV report helped make the case for a more aggressive loosening of fiscal policy. This is what the IMF said in May: “The authorities should provide more fiscal stimulus this year through a supplementary budget of more than 0.5 percent of GDP, while paying attention to fiscal efficiency. Additional measures should include higher spending on targeted safety nets, childcare, training and employment services ... Fiscal policy should remain expansionary in the medium-term, focusing on increasing social protection, boosting female labor force participation, and supporting growth enhancing structural reforms.” Bravo.