Can an Emerging Economy Get Into Financial Trouble by Holding Too Many Foreign Assets?

The strange case of Taiwan and its life insurance industry.

Emerging economies historically have gotten into trouble by borrowing too much in a foreign currency.

They borrow in foreign currencies typically because foreign currency debt appears cheaper—with a lower interest rate than domestic currency debt.

And then they face “balance sheet” risk if their currency depreciates. A depreciation raises the real value of their foreign currency debts, and the resulting financial distress means that depreciation—at least in the short-run—is contractionary.

Over time emerging economies learned this lesson the hard way. Emerging market governments shifted to borrowing in local currencies, and started building up foreign reserves. The strength of emerging market sovereign balance sheets is a big reason why the 2013 taper tantrum and the 2014 oil price shock didn’t result in any major distress. Prices adjusted—emerging market currencies fell significantly—but no one (big) defaulted, or had to turn to the IMF. The governments of countries like Russia and Brazil are technically “long” foreign currency—with more foreign exchange reserves (at the central bank) than foreign currency debt (at the Treasury), their solvency improves as their currency depreciates.*

But does the risk work the other way too? Can an emerging economy get into trouble not because of foreign currency denominated debts, but rather because of foreign currency denominated assets?

This isn’t just a theoretical risk.

Consider Taiwan.

Taiwan has a huge life insurance industry. And its life insurers have promised fairly high returns—returns that are far higher than the life insurers can obtain holding a portfolio of “safe” Taiwan dollar bonds. Ten year Taiwanese government bonds have yielded between 1 and 1.5 percent since the crisis. Taiwan’s firms also aren’t huge borrowers.

So what did the life insurance industry do?

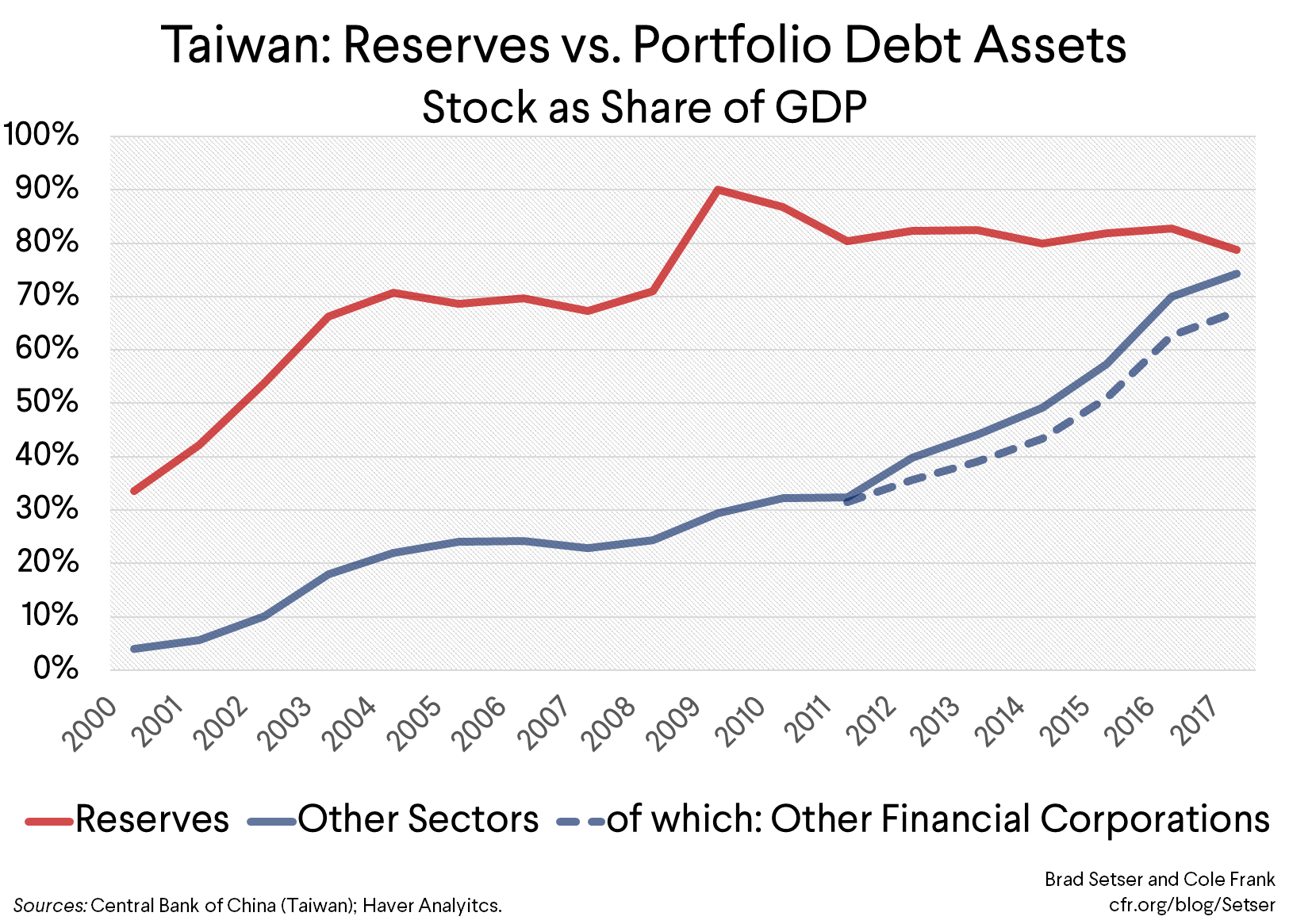

It—with an assist from the local regulators (Formosa bonds!)—reached for yield abroad. “Other financial corporations” is balance-of-payments speak for life insurers (at least in Asia).

Foreign bond holdings have soared as a share of Taiwan’s GDP, and as a share of the life insurance industry’s portfolio. Moody’s last year:

“As of the end of July, overseas investment accounted for 64 percent of insurers’ invested assets, up from 43 percent at the end of 2013 .... in particular, investments in international bonds have increased markedly since the asset class was exempted from life insurers’ cap on overseas investments in 2014.”

And the rise in foreign bond holdings in turn has created an intrinsic currency mismatch on the insurance industries‘ books that is the opposite of the standard emerging economy vulnerability.

The insurers have sold policies that offer the promise of future payment in Taiwanese dollars, but they increasingly hold as assets a portfolio of foreign bonds (often corporate bonds it seems, and now some taxable municipal bonds) and locally issued foreign currency denominated bonds (the Formosa bonds, which are considered “local” for regulatory purchases even though they are denominated in foreign currency and issued by non-residents).

If they don’t hedge, they “win” if the Taiwan dollar depreciates, but stand to lose if the Taiwan dollar appreciates.

And, well, they don’t fully hedge.

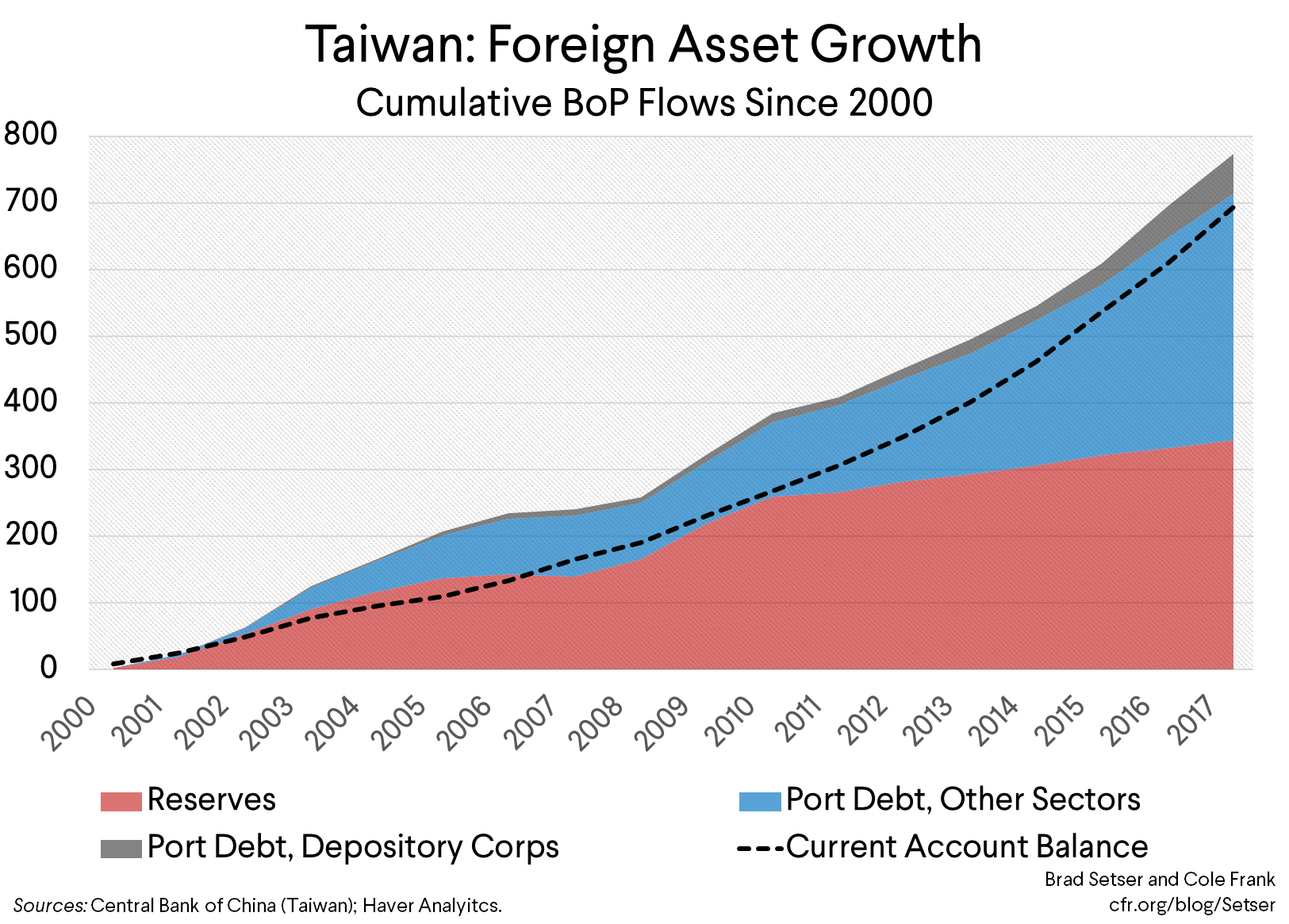

As the scale of the Taiwanese life insurers’ foreign portfolios increased—and we are talking about an eight year run of buying close to $50 billion a year in foreign bonds, leading to an estimated foreign bond portfolio of $400 billion—the lifers did start to sell policies denominated in dollars (or another foreign currency). That pushes the foreign currency risk to the household sector, as households would effectively be saving in dollars (and stand to lose in the event of an appreciation).

But domestic dollar policies only offset a portion of the life insurers’ foreign portfolio. A portion of the remainder is hedged through onshore swaps (or offshore non-deliverable forwards), and a portion is simply unhedged. Moody’s noted in 2017:

“Taiwan life insurers normally do not fully hedge their foreign-currency exposure and instead maintain 20 to 30 percent of total overseas exposure open to reduce overall hedging costs. This unhedged currency risk will grow as companies’ overseas investment portfolios expand”

The hedges have also gotten a bit complicated, or at least pricy, recently. The insurers—like most institutional investors—typically hedge their foreign currency risk through short-term swaps even though the underlying asset is long-term. Think of rolling over 3 month hedges against a 10 year bond. Swaps are—to the first approximation—priced off of interest rate differentials. So the hedge didn’t cost much when there wasn’t a big gap between short-term interest rates in Taiwan dollars and short-term U.S. dollar rates. But with dollar rates rising, the hedges are getting costly. The hedged yield pickup on “safe” U.S. assets isn’t great—which pushes the life insurers to buy riskier products.

It also isn’t totally clear who is on the other side of the life insurers’ swap books. Taiwan’s exporters also need to swap dollars into Taiwan dollars to hedge, so they aren’t a natural counterparty. Taiwan’s importers would want to swap Taiwan dollars for U.S. dollars, but, well, there are a lot more exporters than importers. Foreign investors in Taiwan’s stock market might want to hedge (and lock in a dollar return). But Taiwanese portfolio investment abroad is much larger in aggregate than foreign portfolio investment in Taiwan ($635 billion v $325 billion at the end of 2016, and the stock of investment abroad rose over the course of 2017). It isn’t immediately obvious to me how the market clears even if the life insurance industry only hedges 75 percent of its total foreign currency risk.

Of course the central bank could be on the other side—otherwise the banking system would need to borrow dollars and sell them for Taiwan dollars (putting upward pressure on the spot market) to hedge its swap book. The IMF had a nice paper on the market dynamics created by the large FX hedging need of Korea’s exporters (the shipbuilders in particular) prior to the global crisis.

We don’t know though, as the Central Bank of China (Taiwan) has never disclosed its derivatives book (the central bank claims that there is nothing it needs to disclose).**

No matter—it is clear that the life insurers are only partially hedged. They in effect have relied on the assumption that the central bank will cap any Taiwan dollar appreciation to protect their portfolio. They would be in trouble if the new Taiwan dollar’s move exceeded the funds set aside in their foreign exchange volatility reserves.

Yet Taiwan needs to generate ongoing, large outflows for the new Taiwan dollar to stand still given its massive (around 15 percent of GDP) current account surplus. Before 2010, most of that surplus showed up in reserves. After 2010, most of the surplus has shown up in a net buildup of foreign assets in the financial sector (the banks have joined in recently too, but presumably are hedged).

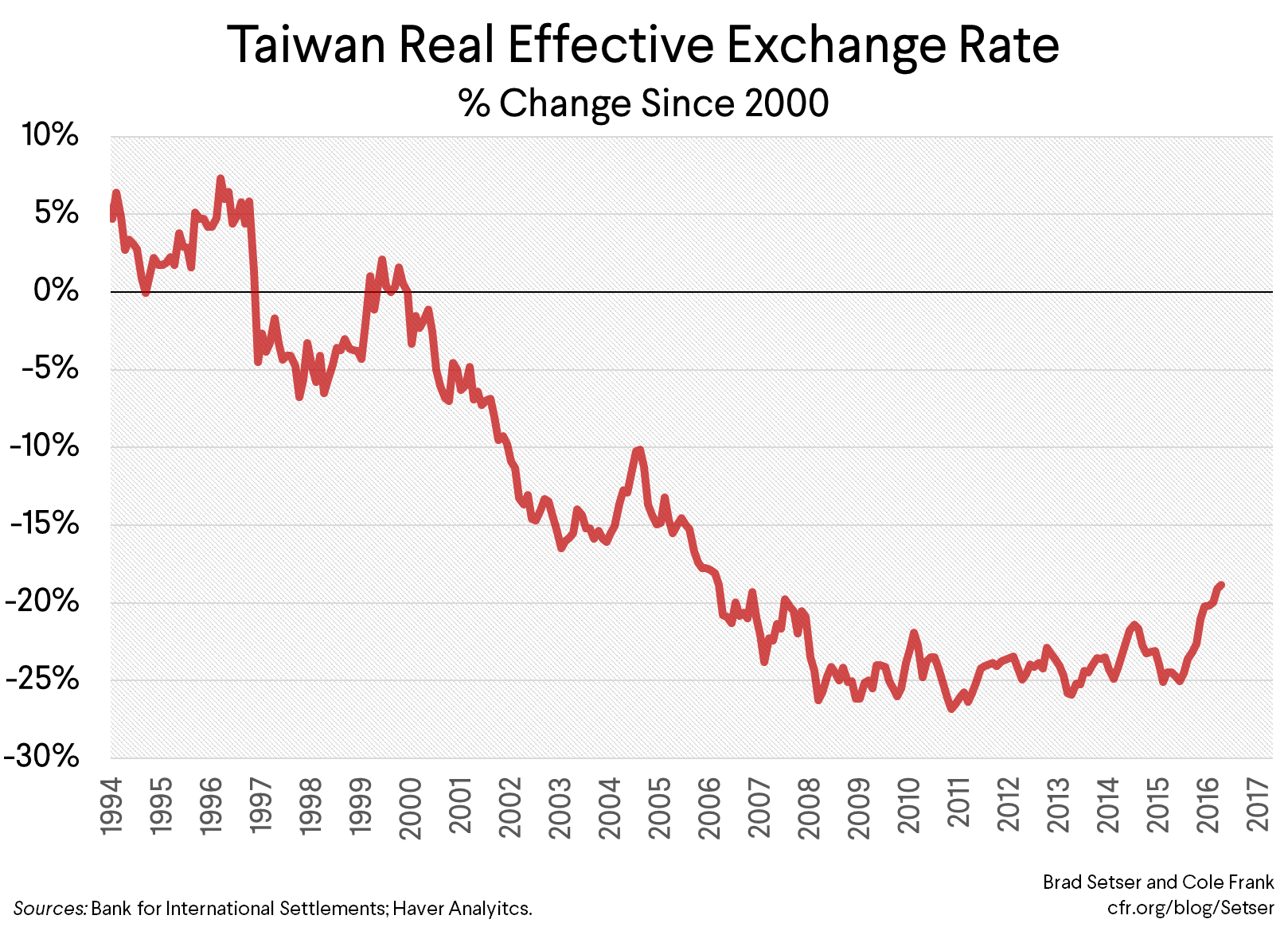

It isn’t hard to see why Taiwan’s external surplus has gotten bigger over time. The Taiwan dollar in real terms is quite weak—it is down something like 20 percent from its 2000 level, and while it did appreciate a bit in 2016, it is still low versus its level in the early to mid-aughts.

So a fall off in demand for foreign bonds would pose a dilemma for Taiwan’s central bank, as the structural outflow from the insurance industry and the associated bid for dollars has been the key to the post-crisis weakness of Taiwan’s currency.

The central bank could step into the market in a visible way, and return to large-scale purchases and buildup its reserves. Taiwan’s new central bank government has indicated that keeping the currency “steady” is a key priority.

That though would carry the risk that Taiwan would be put back on the Treasury Department’s watch list, and perhaps even get dinged for manipulation. (Even if it triggered the reserve accumulation threshold by purchasing over 2% of its GDP in foreign currency, Taiwan would only meet two of the three Bennet criteria as its measured bilateral surplus with the U.S. is under $20 billion. However, the 1988 manipulation statute is still on the book, and Taiwan could be dinged under the 1988 law for impeding effective balance of payments adjustment).

Or it could let the Taiwan dollar appreciate even if this generated large losses among the life insurers.

The insurance industry in turn could be bailed out from large currency losses. Bailing out a domestic insurer can be done by giving the firm government bonds; technically it isn’t that hard. Taiwan’s government isn’t heavily indebted, it can absorb the cost (though any bailout might come at a price—diluting shareholder equity and/or risk-sharing on legacy high-return life insurance products).

This all could make for an interesting set of choices, as it isn’t clear that the equilibrium of the last ten years (limited intervention, massive foreign bond purchases by he financial sector, a growing open FX position in the life insurance sector, etc.) can be sustained forever (even if pressure on the new Taiwan dollar fell a bit in April as the dollar rallied).

* This is true even if the foreign currency debts of the large state-owned Russian and Brazilian companies are added to the explicit foreign currency debt of the finance ministry.

** Taiwan’s central bank has already criticized my analysis of their currency management in the second half of 2017, and I do not expect this “blog” to increase my popularity.