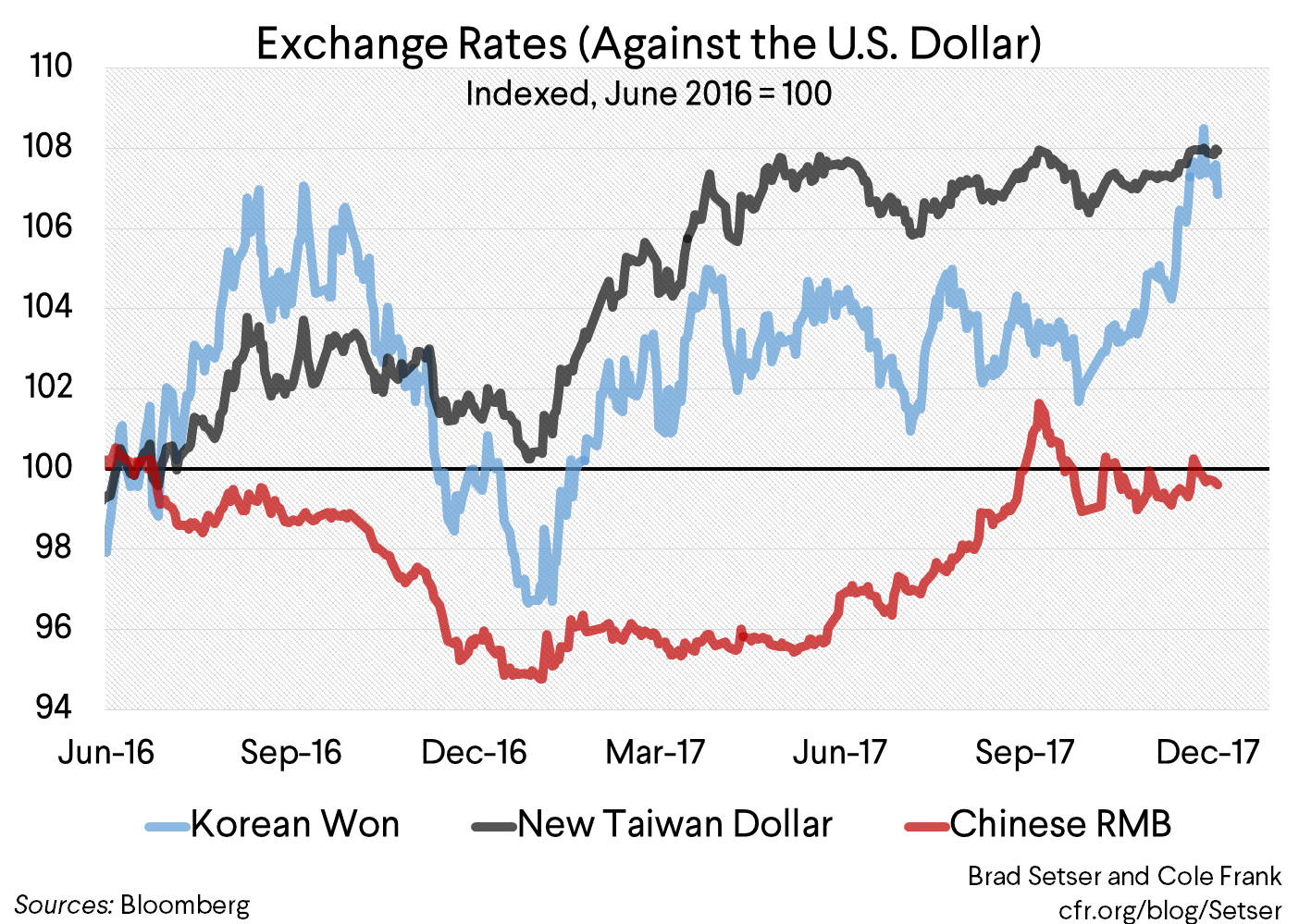

Korean Won Up, New Taiwan Dollar Flat: An Update on Asian Intervention

Korea didn’t stop the won from appreciating through 1090 (its intervention level in 2016); Taiwan seems to be blocking any move through 30.

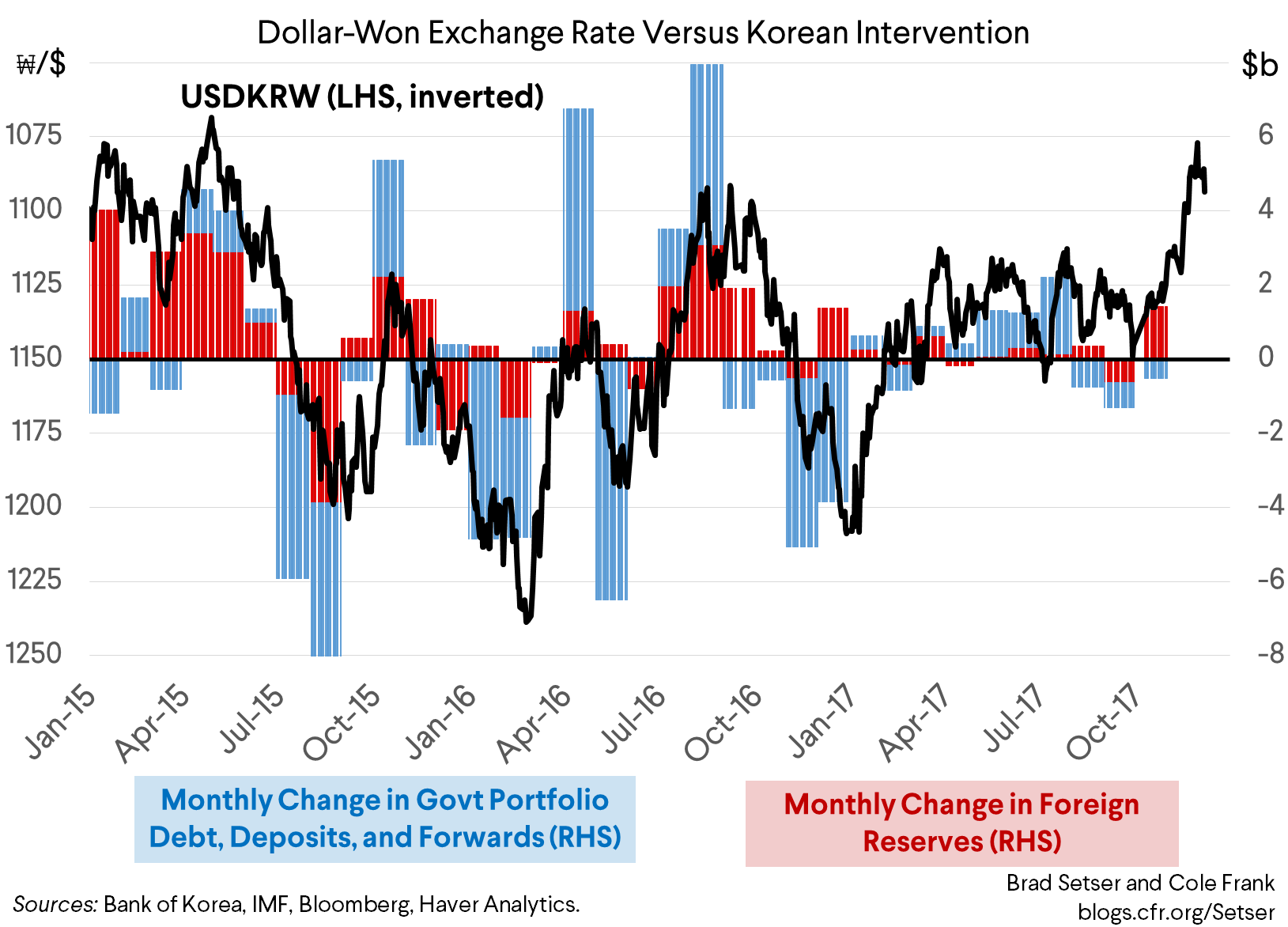

In the past I have criticized Korea for intervening to keep the won from appreciating. In the summer of 2016, Korea intervened at 1090. Earlier this year, it seems to have intervened at 1110 or so.

So Korea’s decision not to intervene as the won rose to 1080 (or at least not intervene much, there isn’t yet real data for November) is noteworthy.

Back in the spring of 2014, before the dollar’s rise, Korea (very briefly) allowed the won to rise to 1010 before intervening. And from 2011 to 2014 Korea generally intervened at 1050. So there is some chance Korea’s intervention policy is changing a bit.

Though the won sold off a bit at the end of the weak on the “dovish” rate hike by the Bank of Korea, so we don’t yet know just how significantly Korean policy has shifted (before the global crisis the won was allowed to rise to 900 before Korea intervened, so there is potentially a lot of room for the won to rise if Korea really is shifting its intervention policy).

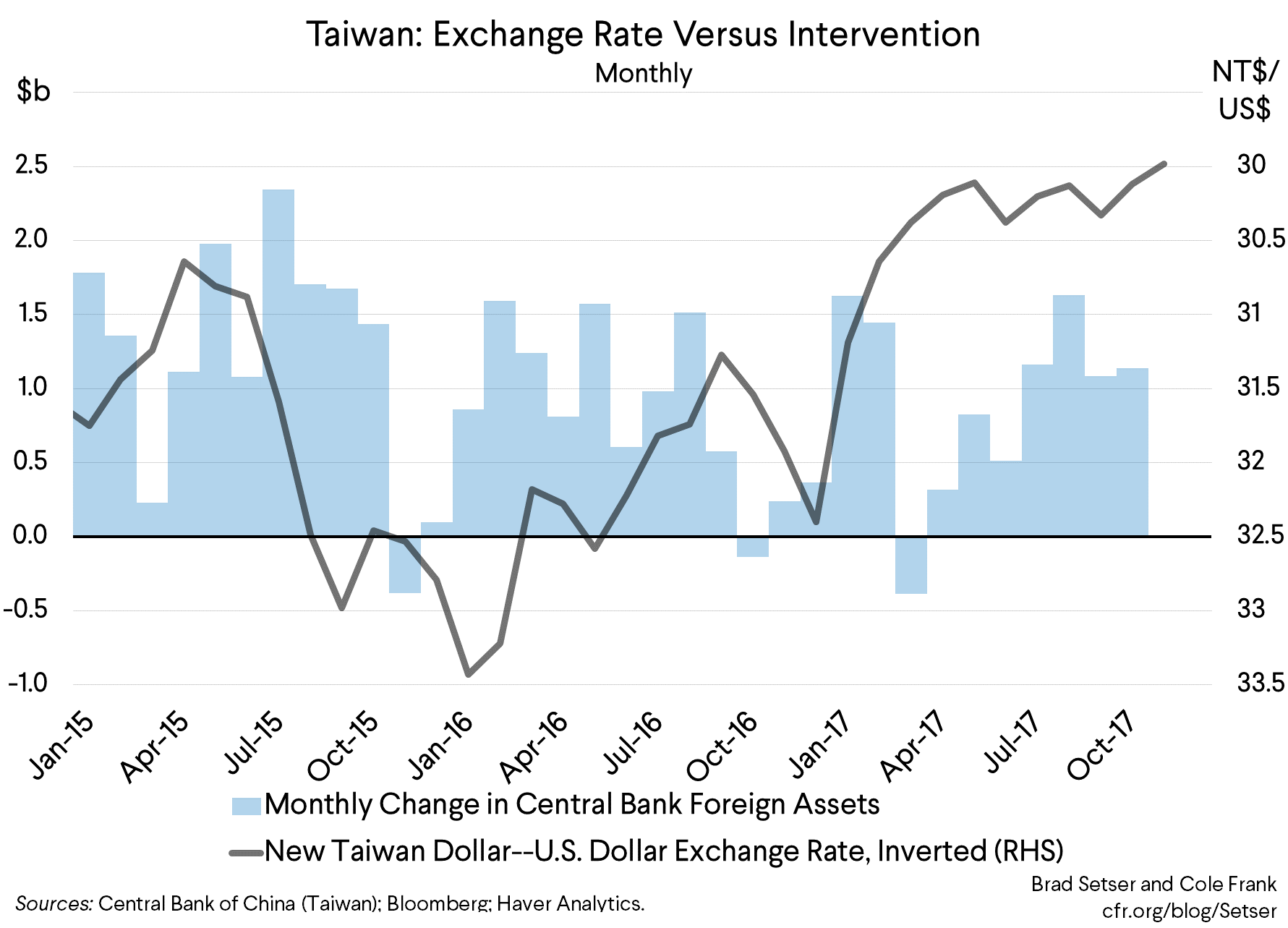

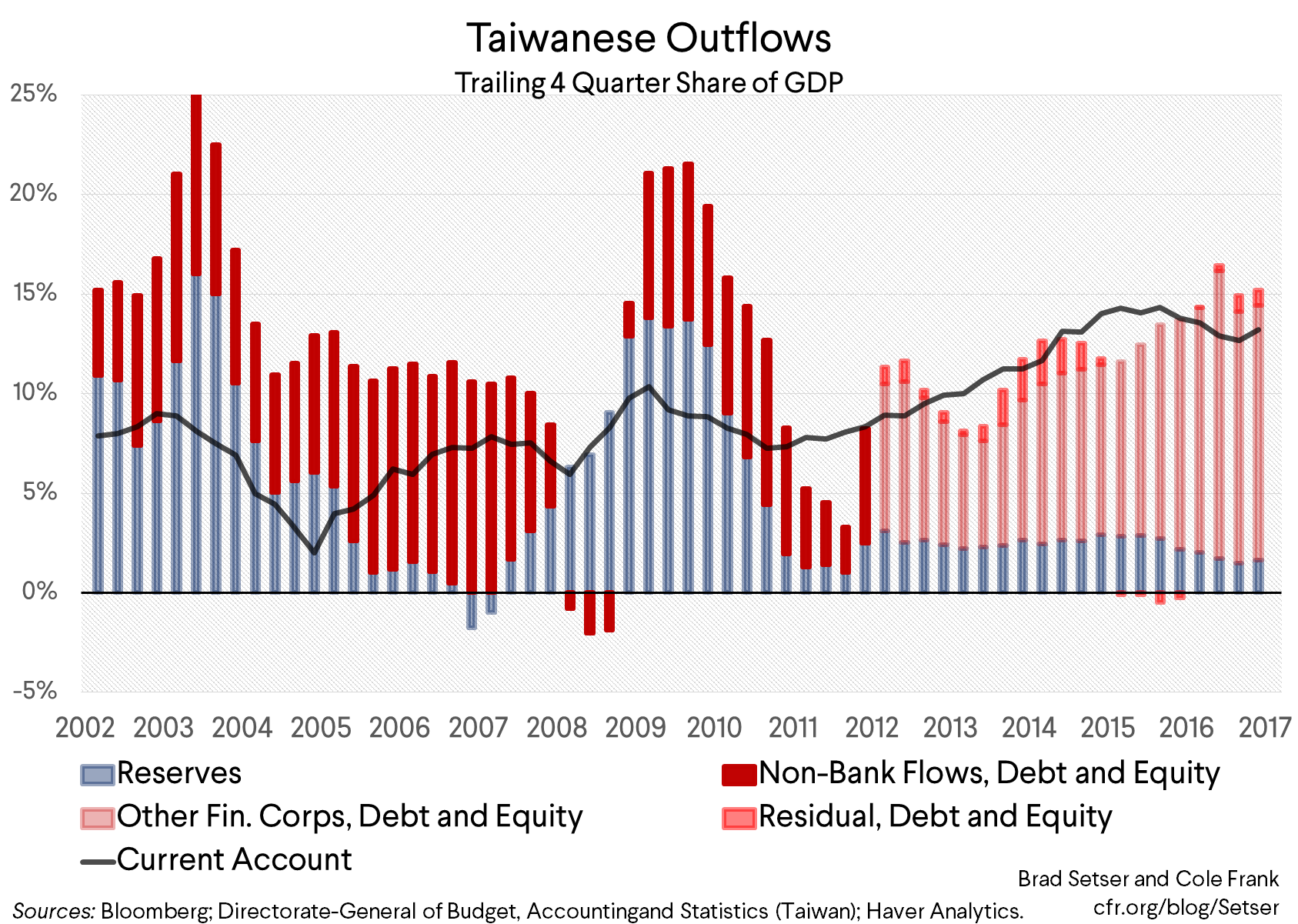

Taiwan by contrast has continued to hold the line at 30 Taiwanese dollars to the U.S. dollar throughout the fall. Reported reserve growth in q3 was right at the Treasury threshold of 2 percent of Taiwan’s GDP. And my guess is that Taiwan intervened heavily in November. It certainly hasn’t responded to being taken off the Treasury’s watch list by reducing its intervention and allowing further New Taiwan Dollar appreciation.*

Taiwan was a (relatively) good actor back in q1. But its willingness to allow the New Taiwan Dollar to appreciate then didn’t augur any broader change in policy. It looks to have reverted to its old intervene-to-hold-the-dollar-below-a-certain-level-at-the-end-of-the-trading-day ways.

That’s why, much as I welcome Korea’s decision to let the won reach 1080, I am not ready to conclude that Korea’s policy fundamentally has shifted. It may simply be looking to set a new ceiling (1075, 1050) on the won.

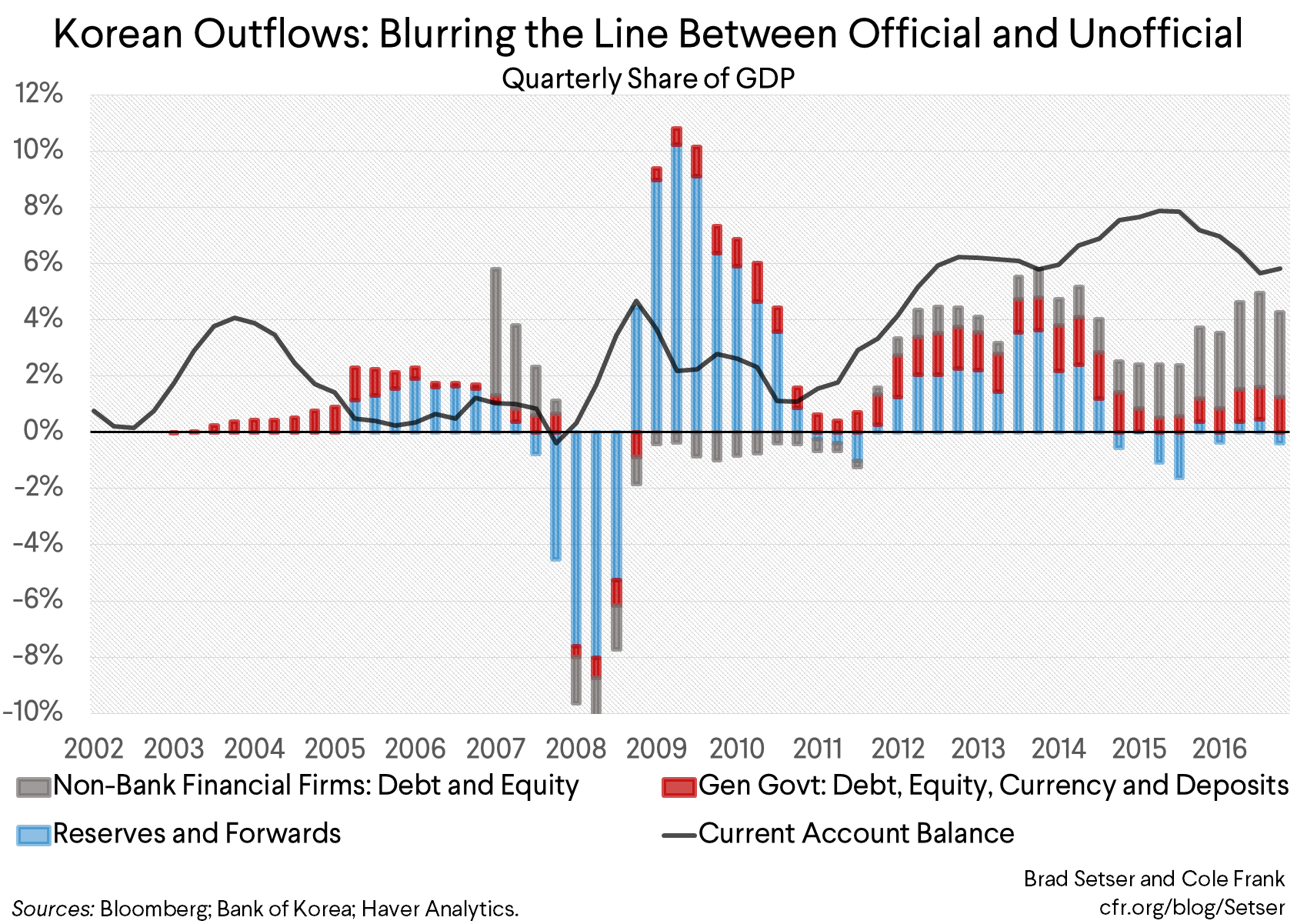

And in other ways Korea continues to use government policy to encourage capital outflows in its ongoing effort to make a large current account surplus consistent with the limited central bank intervention needed to stay out of the U.S. Treasury’s sights.

In the past I have noted that Korea’s social security fund—the National Pension Service (NPS)—has increased its purchase of foreign assets. That’s a policy choice. The U.S. social security trust fund is entirely invested at home in Treasuries. And Goldman Sachs (in a research report by Danny Suwanapruti and Andrew Tilton) has reported that the NPS reduced its hedging in the past couple of years, which effectively increases the market impact of its ongoing purchases of foreign assets.

And it increasingly seems that Korea has taken a page from Taiwan’s playbook and is encouraging its life insurers to invest more abroad. Notably, prudential limits have been lifted.

So it is no surprise that the balance of payments shows a big surge in purchases of foreign debt by Korean’s private sector, and that “other financial institutions”, e.g. financial institutions that are not banks, account for the bulk of the flows. The outflows here aren’t quite on Taiwan’s crazy scale but they have become significant fast.

Over the last four quarters, outflows from the government pension fund (government portfolio asset purchases in the BoP) and the life insurers (who account for most of the flow in the other financial institutions category) have been almost as large Korea’s current account surplus. The rise in these institutional flows, encouraged by the government, in turn has helped Korea reduce the amount of its formal intervention.

Korea, in a sense, has emulated Taiwan—which started encouraging large outflows by its life insurers back in 2012, and doubled down by loosening a set of regulations back in 2014.

The downside of this of course is that if the life insurers don’t hedge, they are exposed to won or Taiwan dollar appreciation. And if they do, well, market stability requires an offsetting source of demand to hedge won and Taiwan dollar exposure back into dollars or euros.** That’s why, from a financial stability point of view, it is a lot safer if the foreign asset purchases needed to sustain an undervalued exchange rate come from the central bank, or another government actor that doesn’t hedge.

* Treasury deducts Taiwan’s estimated interest income from its reserve growth. I personally think that interest income earned abroad by a central bank on its excess reserves should be remitted to the Treasury and thus converted to domestic currency, not stockpiled abroad. And, well, Taiwan still doesn’t report its forward book, so in my view we don’t really know if Taiwan is respecting the Treasury’s criteria. If it has nothing to hide, why not disclose using the IMF’s Special Data Dissemination Standard (SDDS) template, with enough back data to make the disclosure credible?

** The obvious source of such demand would be foreign investors holding won-denominated equites, such as foreign investors in Samsung and Hyundai’s stock (Korea makes it hard to invest in its bond market, so foreign holders of won-denominated bonds don’t have that much to hedge—and well they may like the won risk). Right now foreign holdings of Korean portfolio equity are $510 billion, relative to $390 billion in Korean holdings of foreign portfolio equity. But outflows from Korea (thanks to the NPS) exceed inflows to Korea, so any gap should eventually close. And then who hedges the lifers growing holdings of portfolio debt? The other potential sources of hedging demand would be Korean exporters who want to sell future dollar export proceeds for won. See this Ree, Yoon, and Park IMF paper for details of the market for won hedging, and the difficulties imbalances in the market created in the global financial crisis. It is quite good.