China, Credit, and the Current Account

Arguing China’s credit growth is too high in effect is arguing that the post-crisis fall in China’s external surplus isn’t sustainable.

The Financial Times—in a leader arguing that China should continue to try to wean itself off shadow credit—argues that credit led growth has lost efficiency, as it takes much more credit to generate growth today than it did ten years ago:

“Non-financial sector debt has gone from $6 trillion in 2007 to nearly $29 trillion today, according to data from the Bank of International Settlements. The debt, equivalent to 260 percent of gross domestic product, has brought with it dramatic declines in credit efficiency. The International Monetary Fund points out that in 2016 it took four units of credit to raise GDP by one unit. A decade ago the ratio was 1.3 to one.”

The FT and the IMF are far from alone in making this argument.

And I don’t doubt for a second that the rise in banks and shadow bank credit to Chinese firms continues to generate hidden losses. Rapid rises in credit are a reliable indicator of future banking trouble. It would take a brave man or woman to argue that China’s financial system has successfully intermediated roughly 200 percent of GDP in credit to firms and households.

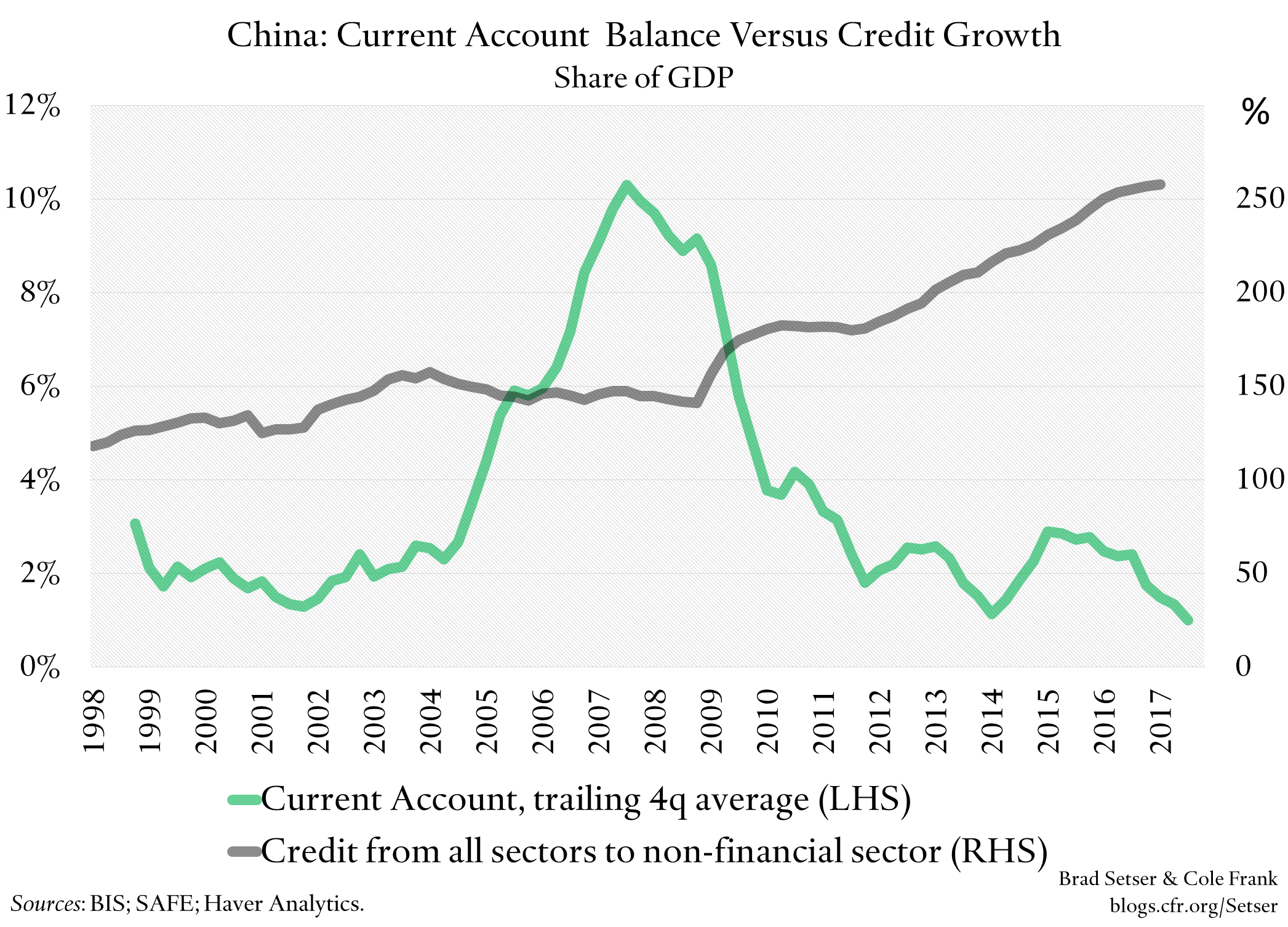

But the standard calculation that China’s credit growth has lost efficiency relative to 2007 still bothers me for one reason: it leaves out net exports.

Back in 2007 China was juicing its growth with a (still) quite undervalued exchange rate. Net exports added 2.5 percentage points to China’s (very rapid) 2007 growth, pushing China’s external surplus above 9 percent of its GDP. And with net exports adding so much to China’s growth (net exports on average added about 2 pp to China’s annual growth from 2005 to 2008, see table 1), China was holding down—through regulation and outright quotas—domestic bank lending to avoid overheating.

That all had the effect of making the credit that China did provide appear more efficient, in the sense that it generated more growth. But the apparent efficiency of credit back then is a bit artificial: credit was being held down in order to make it easier to hold the exchange rate down and allow China to grow based on exports.

And that reflects that I think is a fundamental problem with the simple credit-efficiency calculation.

If China’s banks intermediate China’s high level of savings domestically by lending to domestic firms, local government funding vehicles. and the like, domestic credit will rise. That’s what has happened, generally speaking, since China loosened curbs on domestic credit and allowed a rise in its (shadow) fiscal deficit to finance a wave of infrastructure investment back in 2009.

If China’s banks are forced to put large sums on deposit at the PBOC—as was the case in 2007, when the reserve requirement was jacked up—and in the process sterilize a massive increase in China’s foreign exchange reserves, China’s high savings is still being used to provide credit. It is just credit to the rest of the world, and that credit is considered an asset—a foreign asset—not a domestic liability.

And the savings that China exported prior to the crisis also weren’t used all that efficiently it turns out—through a complex chain of financial intermediation, those savings indirectly helped finance excessive borrowing by American and Spanish households (see Brender and Pisani for more on how it took both Asian savings and leveraged U.S. and EU intermediaries to sustain pre-crisis imbalances; their “Globalized finance and its collapse” is in my view an unappreciated classic).

Arguing that the pace of credit growth needs to come down to bring China’s credit-to-GDP ratio down implies, I think, that the post-crisis fall in China’s current account surplus isn’t sustainable. Too much of the adjustment came through an unhealthy credit-fueled rise in investment (and an unsustainable increase in the augmented fiscal deficit, which funded a portion of the rise in investment), and too little has come from a reduction in China’s high level of national savings.

I agree with that by the way.

And it also implies that curbing China’s domestic credit—both credit to inefficient firms, and credit to local SoEs that the IMF believes is really backdoor fiscal spending—isn’t enough to generate a healthy equilibrium on its own. China also needs policies that would help bring down its high level of savings, policies that I at least don’t yet see in the pipeline.

One last, somewhat unrelated point.

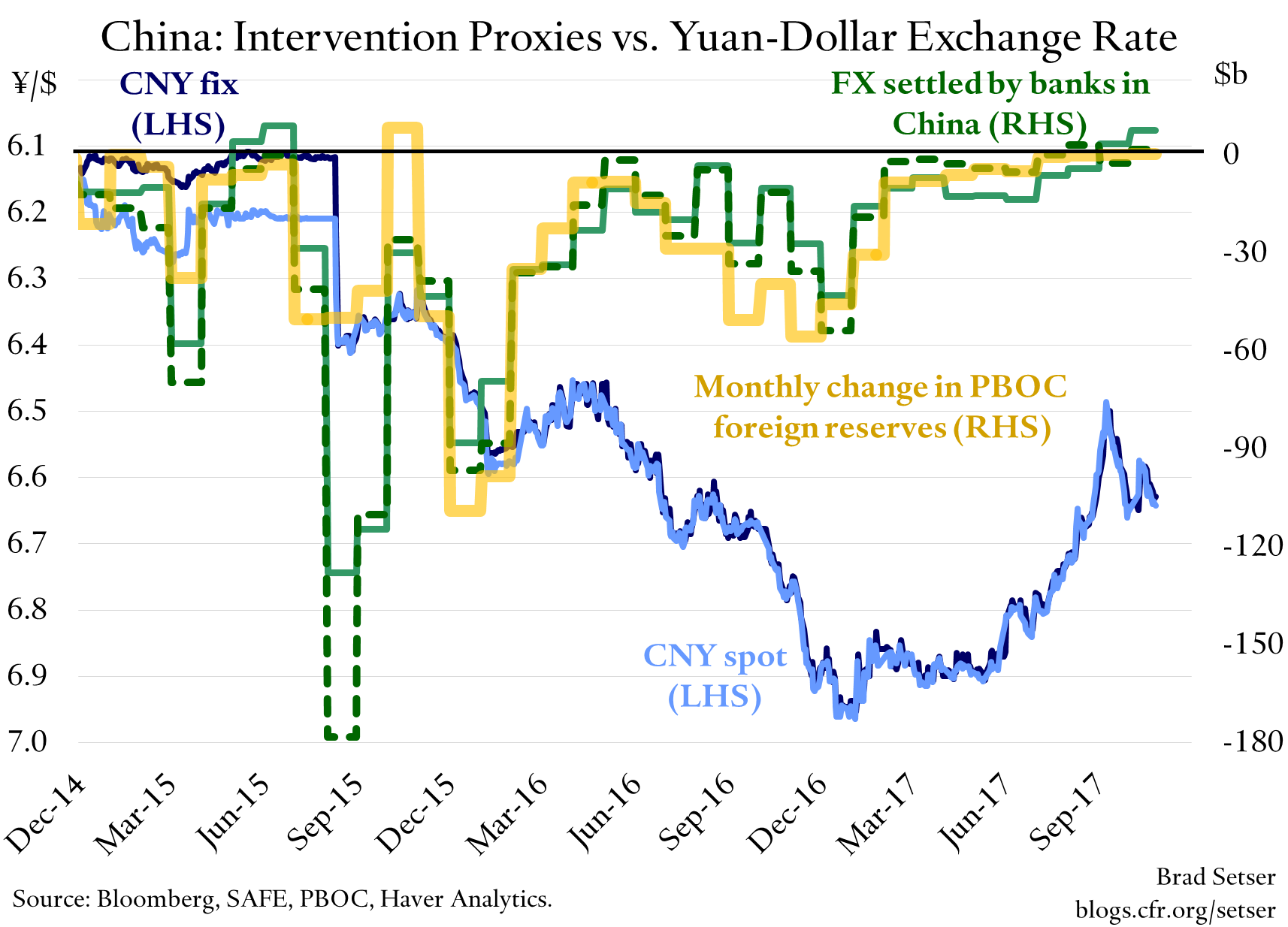

China has hardly sold any reserves at all over the past 9 months. The October numbers for foreign exchange settlement point to modest purchases (though the scale of the purchases falls after adjusting for the settlement of past forwards), while PBOC balance sheet reserves were flat (and the broader measure of the PBOC’s foreign assets fell ever so slightly). The balance of payments data indicates that China added around $30 billion to its reserves in both q2 and q3, putting China on track to maybe add $100 billion to its reserves this year if q4 follows trend.* Flows in both directions remain heavily managed, but the notion that China is still intervening heavily to prop up its currency is now a bit dated.

And, more generally, I think the evidence suggests that China’s 2016 stimulus helped take pressure off the yuan, by ginning up China’s growth and thus allowing China to be in a position where domestic interest rates could follow the Fed. Basically, a looser fiscal and somewhat tighter monetary policy mix proved good for the world, despite all the criticism it has attracted. (Also see Gavyn Davies for an argument that the Fed and China tacitly cooperated back in 2016 to limit the risk of an uncontrolled depreciation of the yuan; I also suspect their combined actions likely played some role in the pick-up in global growth over the course of 2016).

* There is a gap between the PBoC balance sheet data and the BoP data that I don’t fully understand. The balance sheet data—which shows reserves in yuan at their historical purchase price—suggests that reserves have basically been flat. The BoP data shows reserves rising at a $120 billion (1 percent of GDP) annualized pace in the last two quarters. It isn’t a huge difference, but it is big enough that I would like to understand it better.