American Asian Security Allies, Alas, Contribute More to Global Trade Imbalances Than China

One possible U.S. international economic policy towards Asia, broadly speaking, would be to seek to align with Asia’s other economies to put more pressure on China.

Xi’s rhetorical commitment to globalization seems motivated by a desire to keep global markets open to Chinese products, not by a new willingness to allow foreign products—especially manufactures—easy access to China. As a share of China’s GDP, China’s imports of manufactures for its own use are low—and China’s industrial policy seems directed at further reducing China’s imports of many high-end goods: aircraft and semiconductors most prominently.

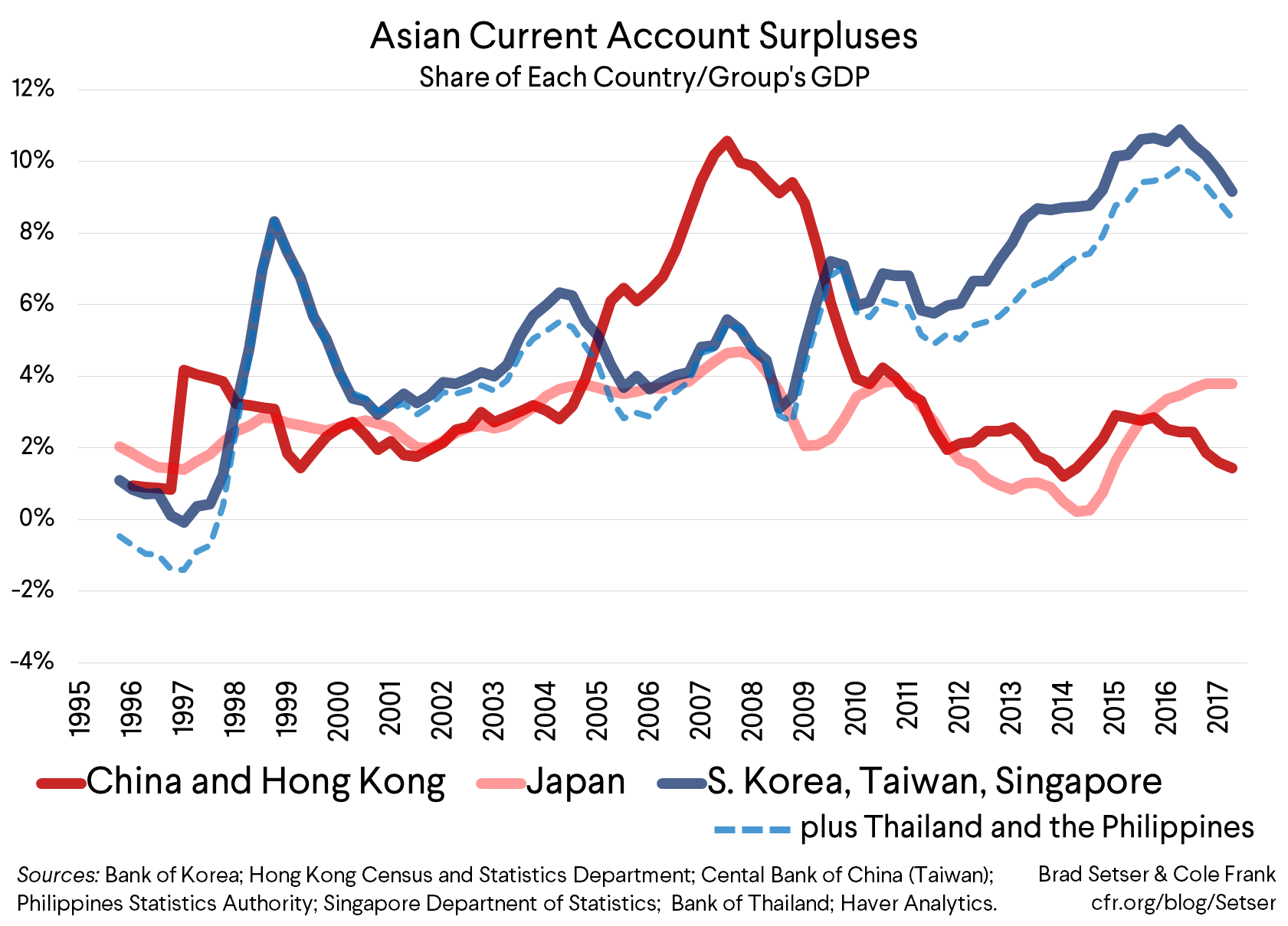

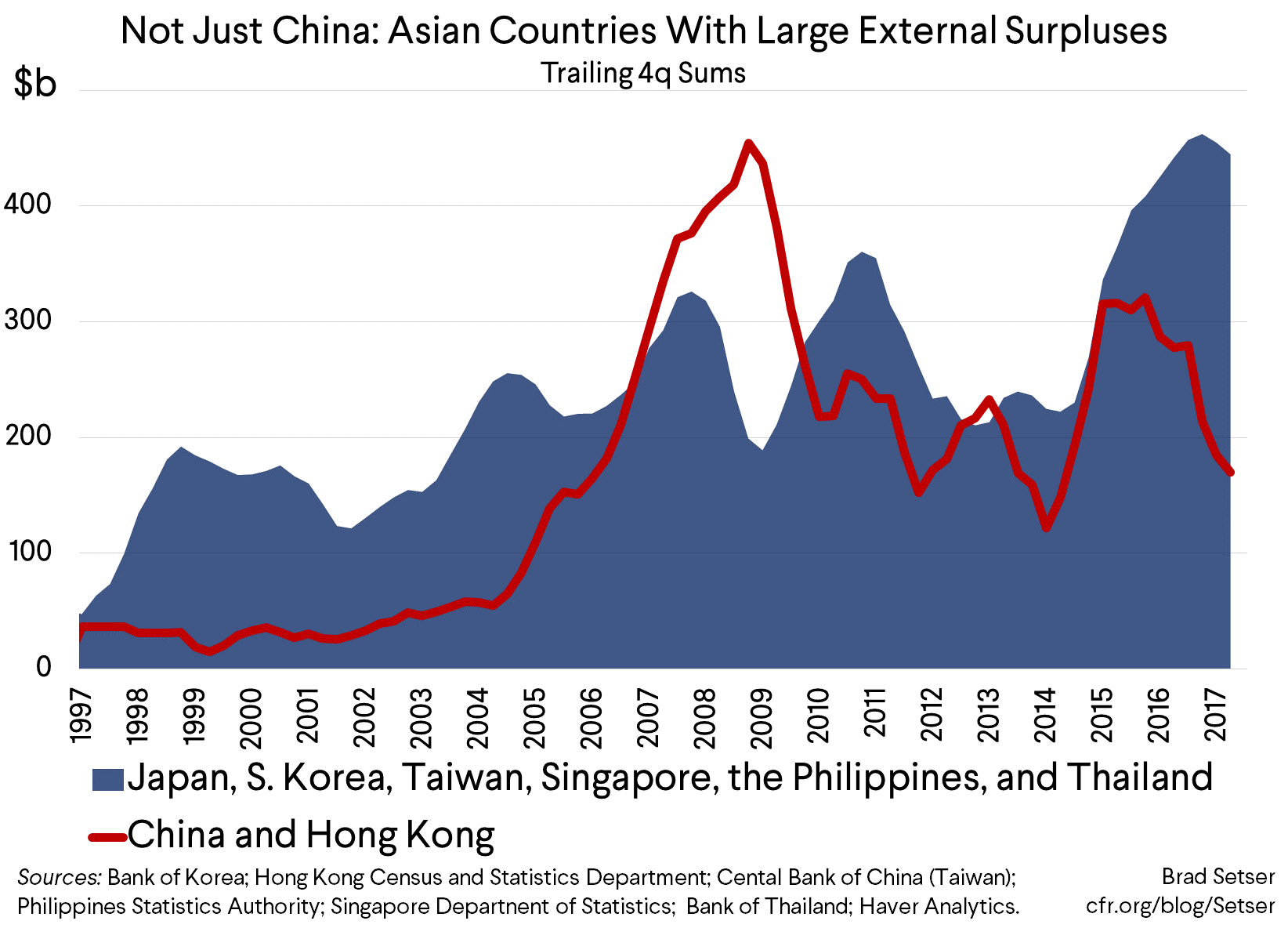

Yet there is one major obstacle to this approach: if you worry about overall trade imbalances, as opposed to headline bilateral balances*, America’s traditional Asian allies are now a bigger problem than China.

The surpluses of Korea, Taiwan, Singapore, and Thailand are all exceptionally large relative to their own economies. As a share of their combined GDP, their external surplus is as large as China’s surplus was—relative to its own economy—before the global crisis.

Japan’s surplus has also inched above its pre-crisis levels. Not a surprise really, given the yen’s weakness.**

The combined surplus of these economies, in dollar terms, now easily tops that of China.

I have no doubt that China’s internal market is rigged (see Mark Wu, among others). China imposes significant barriers on many products at the border, generally doesn’t make it easy to invest in China without a joint venture partner, and doesn’t always maintain a level playing field once a firm has set up shop in China.

But thanks to a loose fiscal policy (the IMF says far too loose a fiscal policy) and a big rise in domestic credit, China has kept its external surplus down for most of the post-crisis period—with a high level of investment absorbing the bulk of China’s huge mass of domestic savings. China’s true external surplus is a bit bigger than its reported surplus—but even with an adjustment for China’s overstated tourism imports, China’s external surplus is currently far smaller than that of many of its neighbors.

Other Asian countries generally do less than China to tilt their domestic markets away from imports. But they have limited their own demand and thus their imports with tight fiscal policies and, in some cases, with underfunded social safety nets. And they keep their exports high in part by actively working to keep their exchange rates weak—in Korea’s case, much weaker than it was prior to the crisis—through a mix of overt foreign exchange intervention, the channeling of public pensions into foreign assets, and more subtle efforts to encourage “private” capital outflows.

Such policies almost certainly do more to maintain an unbalanced overall pattern of trade globally—and, across the Pacific—than China’s sectoral trade barriers.

And they are an important reason why the trade gains from past agreements to liberalize trade between the U.S. and Asia are, in my view, a little hard to see. At least on the export side.***

KORUS certainly did not create Korea’s current account surplus. But it also didn’t do anything significant to bring it down. Neither KORUS nor any of Korea’s other free trade agreements led Korea to change its tight fiscal policy or put an end to Korea’s tendency to intervene in the foreign exchange market when the won gets too strong for the taste of Korea’s influential export sector.

Korea stands out because its free trade agreements with the U.S. and Europe are relatively recent but the point applies more generally: trade barriers don’t typically drive the trade balance nearly as much as macroeconomic and foreign exchange policies.

In an ideal world, America’s Asian security allies would become better economic allies, and adopt the kind of policies needed to bring down their surpluses—and to do their part to solidify the economic side of the security partnership. But in the absence of some real changes in America’s trading partners, it will remain hard to generate more balanced trade across the Pacific—no matter what China does.

I don’t share President Trump’s focus on the bilateral trade balance—and certainly don’t think the U.S. can credibly criticize others for large surpluses while pursuing a tax policy that would raise the United States’ overall external deficit. But I also think that countries with macroeconomic and foreign exchange policies that produce large external surpluses do not necessarily make the best trading partners. And I am little surprised that Trump and his team haven’t made those policies more of a focus.

* If the bilateral balances were done on a value-added basis, I suspect the overall total with Asia wouldn’t change much. What would change is the attribution of the U.S. bilateral deficit across countries. The deficit with China would fall, while the deficits with Taiwan, Korea, and Japan would rise. Korea and Taiwan export a ton of semiconductors. But they almost all go to China in the first instance not the U.S., and then many are re-exported as computers and cellphones. I should also note that the amount of Chinese content in China’s exports is rising, as more components are now produced in China—and China clearly wants that trend to continue. But that doesn’t change the basic reallocation now needed. At least for goods. Bilateral services trade is horribly measured and is often so distorted by tax concerns (see Torslov, Weir, and Zucman, or spend some time with the BEA’s geographic breakdown for services trade) that I am not confident that it adds all that much. The real action seems to be in the income balance.

** Since the end of 2013, net exports have contributed 2.5 percentage points to Japan’s GDP growth and domestic demand only 1.4 percentage points. Trump wasn’t all wrong when he encouraged Japanese auto manufactures to raise their U.S. production, though at the current value of the yen, I suspect Japanese firms have an economic incentive to do the opposite. Japanese marks currently produce about 4 million cars in the United States. They also produce about 1.7 million cars in Japan for export to the United States (see the JAMA data, pp. 17). That works out to be roughly 1 out of every 10 cars and light trucks sold in the United States. In many ways, I think it is surprising just how reliant the Japanese economy still is on auto exports to the United States. The U.S. accounts for over 1 in 3 of all Japanese auto exports—and Japanese marks produce far more cars in Japan for sale to the U.S. (1.7 million) than they produce in Japan for the sale to the rest of Asia (0.6 million, with China accounting for only 0.2 million). Japanese auto exports to U.S. alone are larger, as a share of Japan’s economy, than U.S. aircraft and aircraft engine exports to the world are as a share of the U.S. economy.

*** A couple of caveats. A significant share of U.S. exports to Asia are bulk commodities. As a result, fluctuations in the price of commodities can play an important role in the headline export numbers and the headline trade balance. Such fluctuations are, fairly obviously, not the result of any trade agreement. Tariffs on most bulk commodities are generally low in Asia; countries usually want to import needed inputs at the lowest possible price. That said, in some agricultural markets tariff and non-tariff barriers are high, and preferential trade agreements can make a difference.