China, More Than Trump, Has Been Driving the Slowdown in Global Trade

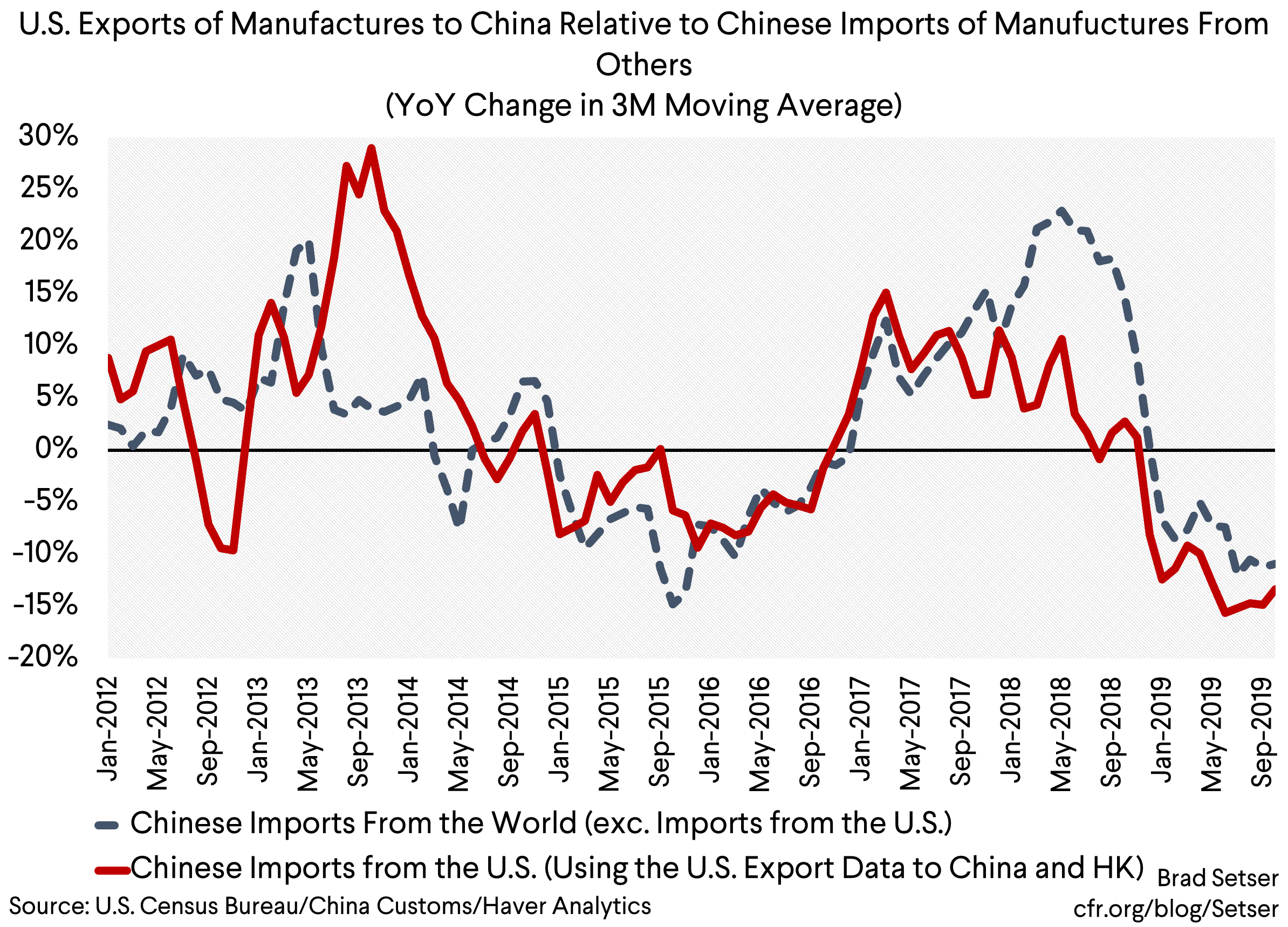

U.S. imports from China are down.

China’s imports from everyone are down.

One central question facing the global economy is how much of the slowdown in global trade can be attributed to Trump’s tariffs, and how much, well, is a function of a global economy that doesn’t always revolve around Trump—

And my guess is that the slowdown in trade stems more from China than Trump.

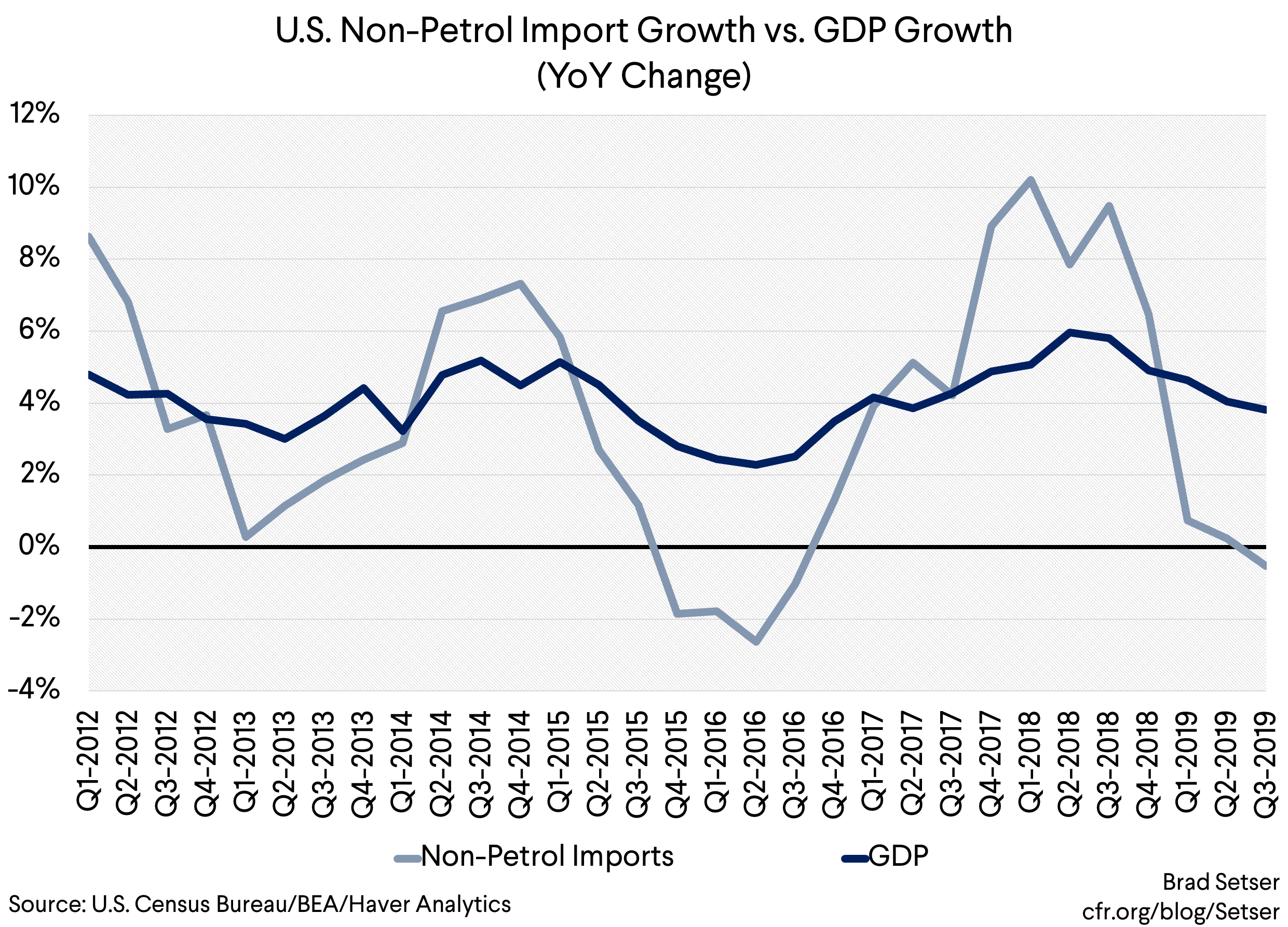

Let’s start with the United States.

U.S. imports this year will be a bit below U.S. growth. In part that’s a function of rising U.S. oil production, which naturally has displaced some imports. In part, though, that’s clearly a function of the tariffs—imports from China are way down and imports from the rest of the world are growing more or less in line with U.S. growth, that has pulled down overall import growth relative to GDP growth (data is nominal terms for comparison with the Chinese data).

Even with weak import growth, the U.S. non-petrol deficit is up modestly thanks to weak exports (at least for the full year, the overall deficit has dipped a bit in the last couple of months). The fall in the bilateral deficit with China has been offset, in dollar terms, by a rise in the bilateral deficit with the rest of the world.

That said, Trump’s tariff’s have had a much larger impact on transpacific trade than on transatlantic trade. There is’t much evidence that general uncertainty around trade—or the targeted tariffs introduced in the long-running Boeing-Airbus dispute—has significantly impeded U.S. trade withe Europe. European exports toward the United States are growing at a reasonable pace and U.S. exports toward Europe are also up year over year. The U.S. isn’t the reason for the slowdown in Germany’s exports.

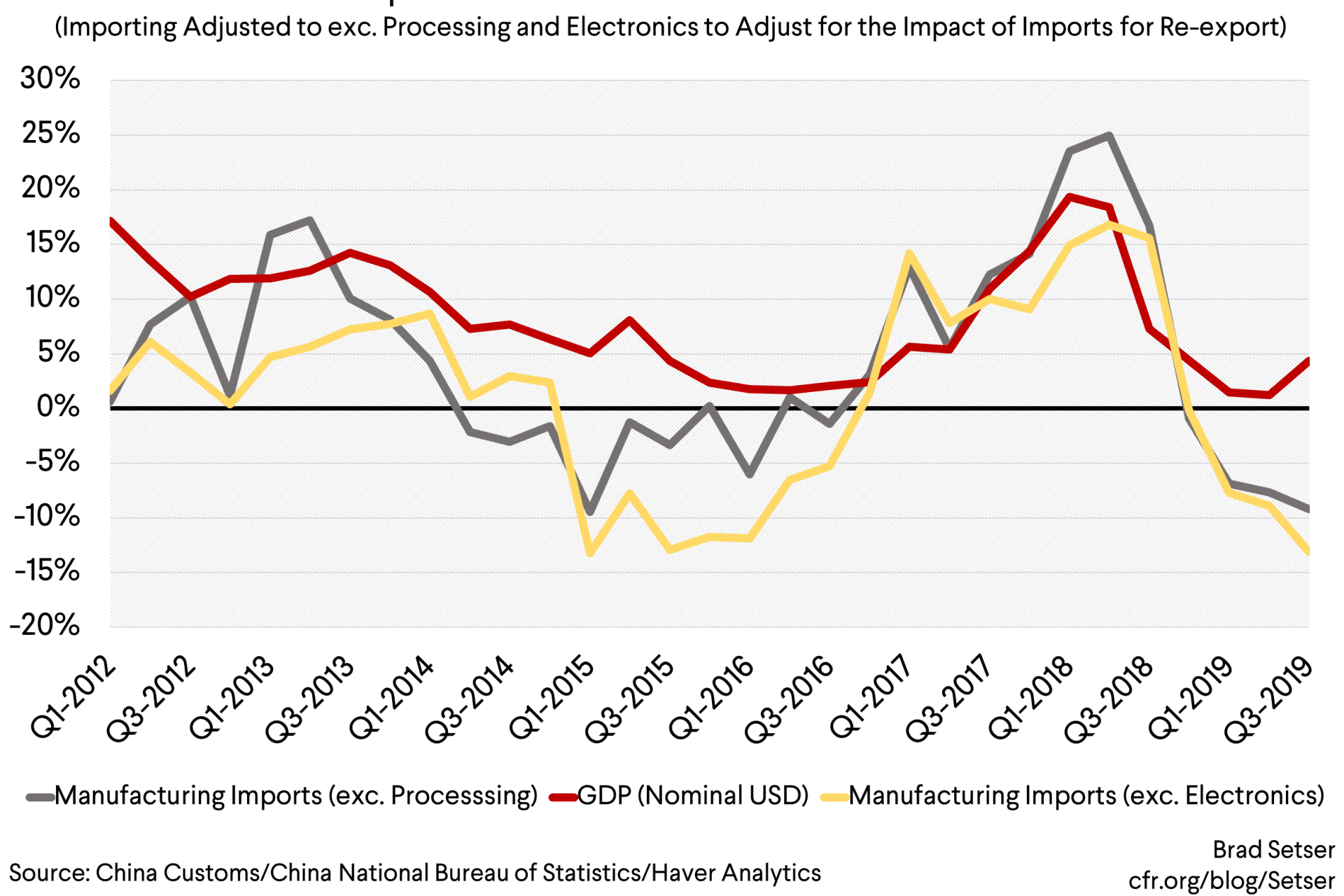

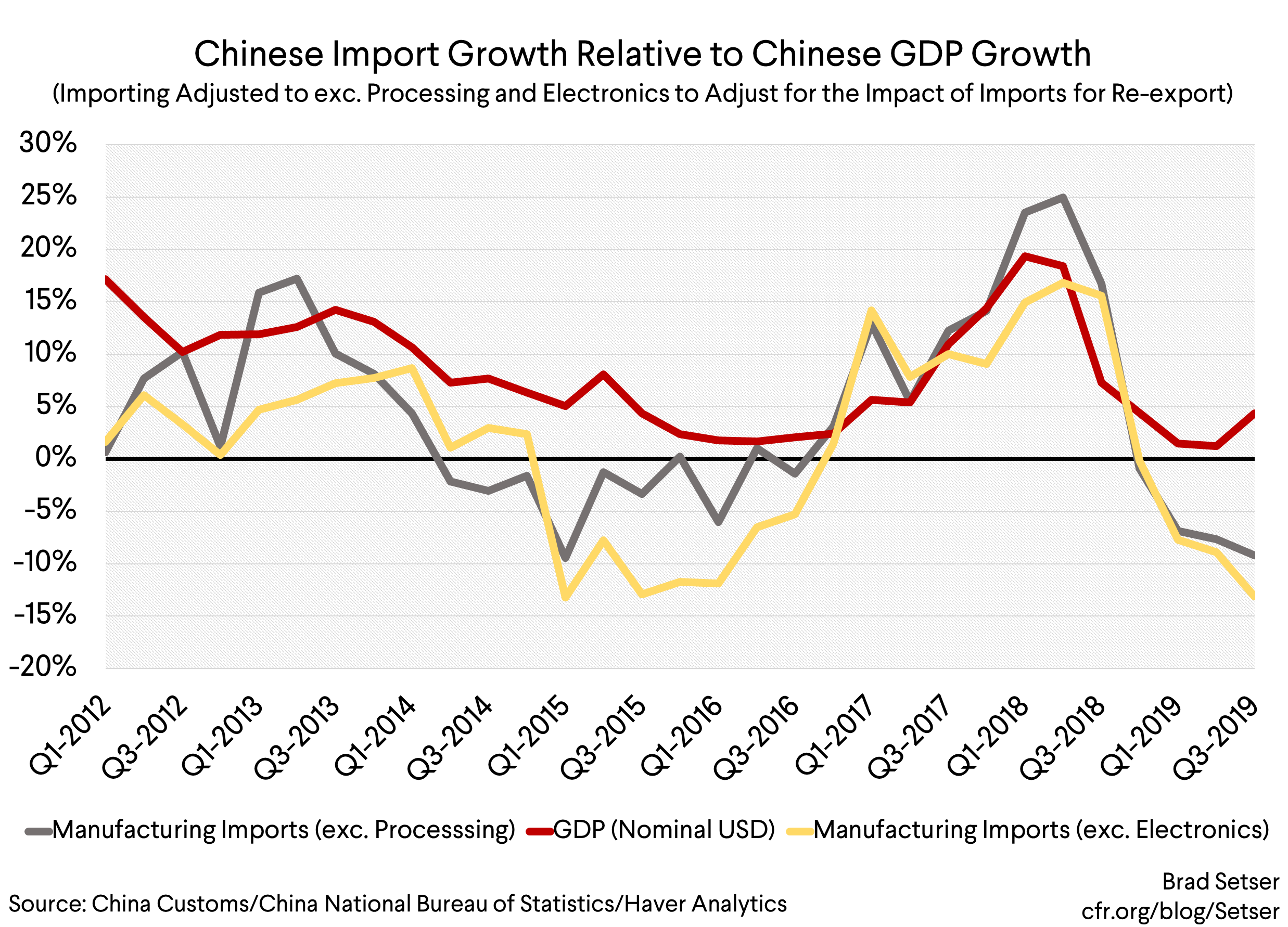

Now look at China.

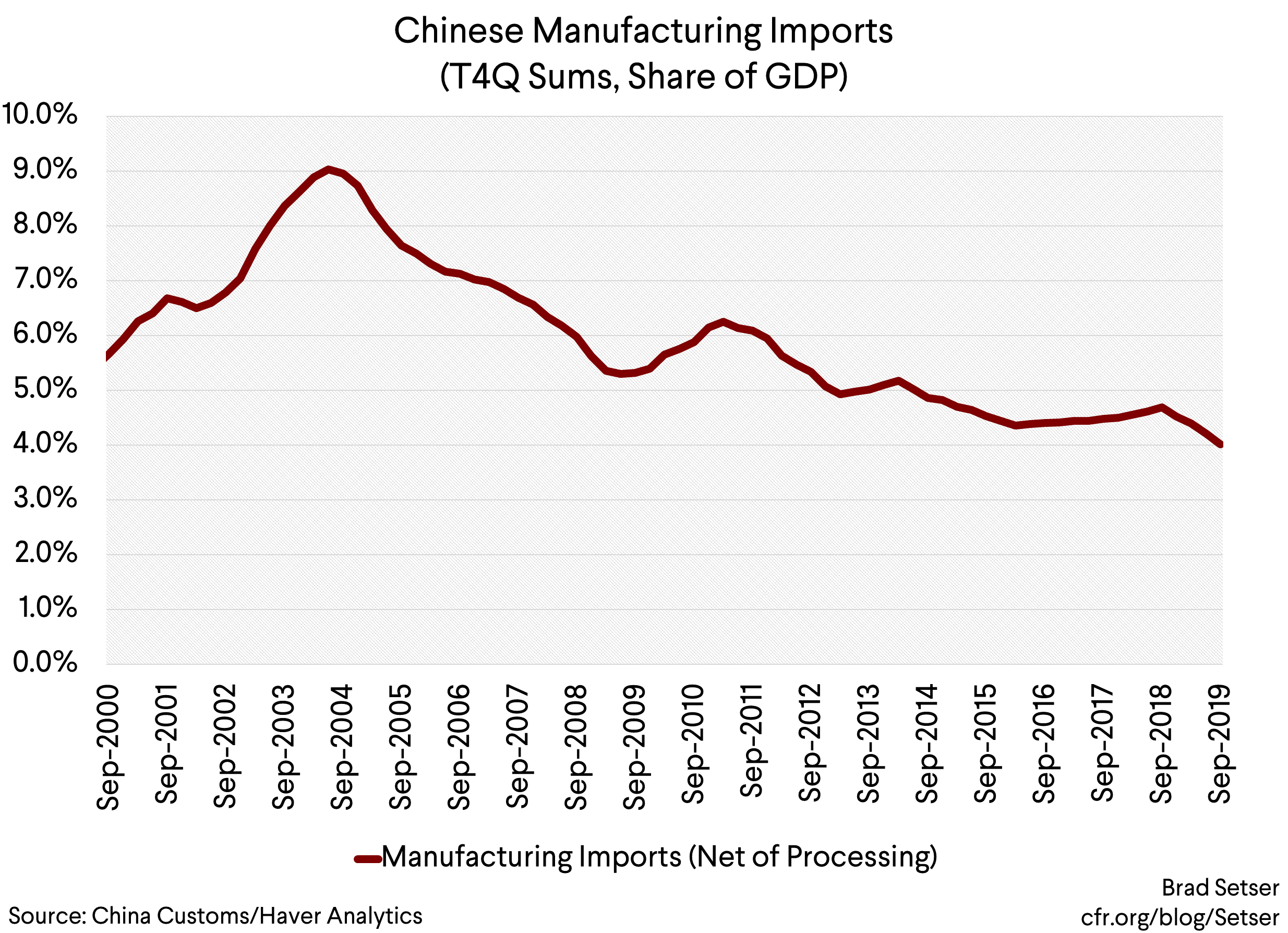

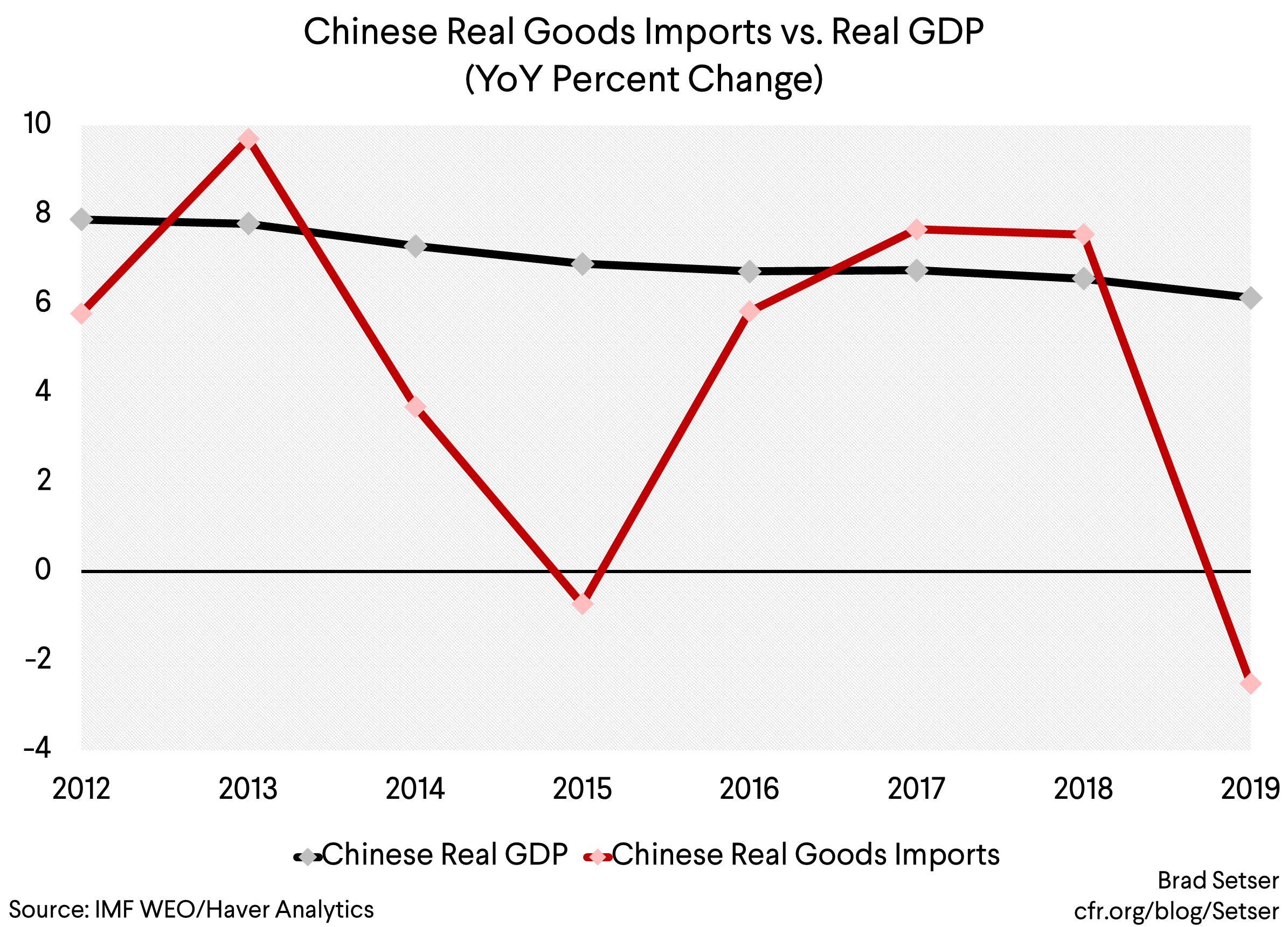

China’s import growth this year is running well below Chinese growth. The IMF puts China’s real growth at around 6 percent and real import growth at negative 2 percent. That’s an enormous gap. That gap also shows up in the nominal data—China’s imports of manufactures (excluding imports for re-export) are down around 10 percent y/y.

China’s imports of manufactures from the U.S. are down 15 percent. But even if you take out trade with the United States, imports of manufactures are also down.

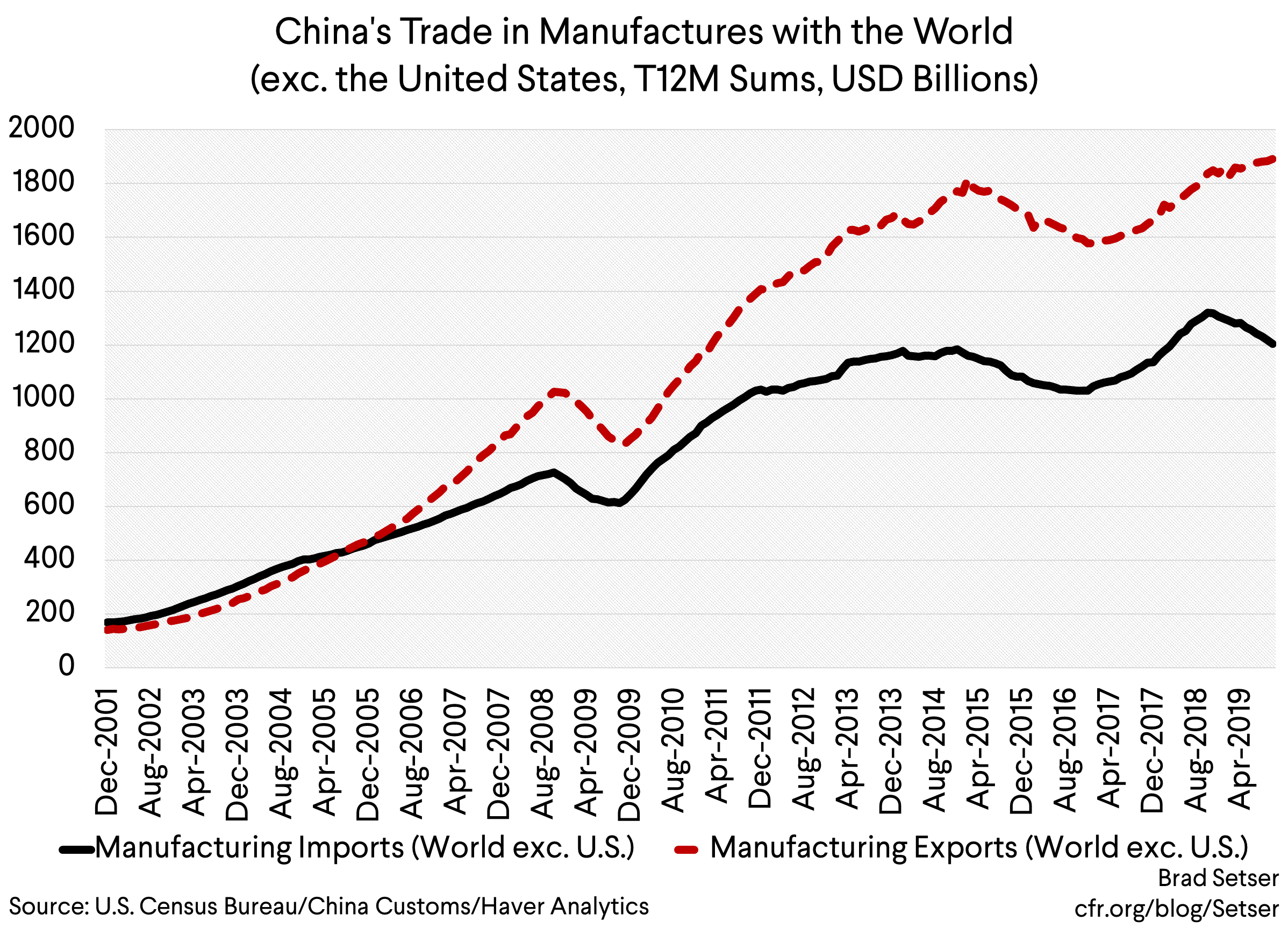

Weakness in China’s imports in turn is driving a major increase in China’s trade surplus. China’s surplus with the United States is down, but its surplus with its other trading partners is way up…

There isn’t any real doubt about this one.

One of the key stylized facts about the global economy in 2019 is that everyone should know China’s trade surplus in manufactures has increased by just under a percentage point of China’s GDP on the back of falling imports (the overall surplus is also up, but by a bit less). Even with the fall in trade with the United States.

Yet it is something that a lot of people haven’t quite internalized. The IMF’s 2019 assessment of China was built around the assumption that the 2018 fall in China’s trade surplus would be sustained. And most of the financial press—the Wall Street Journal, the Economist—and many investment banks were forecasting that 2019 would be the year when China’s current account moved into deficit. Yet China’s current account surplus is on track to top $200 billion this year on the back of a rising trade surplus…

The question is why.

Is it a function of the direct effect of Trump’s tariffs and China’s retaliation on trade with the United States, and the indirect effects of tariff uncertainty on investment in China’s tradables sector?

Is it a function of Yi Gang’s apparently successful effort to limit China’s stimulus to the minimum necessary—and China’s broader decision not to sacrifice deleveraging to the exigencies of the trade war?

Is it a function of China’s version of peak “autos”?

Is it a function of Xi’s campaign to “localize” production in China—a push symbolized by import substitution goals embedded in “Made in China 2025”?

Or is it something else?

There isn’t any definitive answer here.

It isn’t just a direct function of the trade war. China’s exports to the United States are on pace to fall by about 75 billion this year. That automatically would reduce China’s imports by say $25 billion (fewer exports mean fewer imported inputs). China’s tariffs will reduce imports from the United States by something like $20 billion. That isn’t enough to explain the broader fall in China’s imports.

But it is hard to differentiate between the impact of domestic weakness on investment—weak auto demand and auto oversupply should be combining to reduce investment in new Chinese capacity—with the impact of trade uncertainty, which also would deter investment in new manufacturing in China.

We do though know that China’s investment has been weak and investment tends to have a disproportionate impact on trade, as the imported content of investment is higher than the imported content of consumption.**

One thing is clear—even though China lowered its overall tariffs (by just a bit) even as it raised tariffs on U.S. exports, other countries aren’t really benefiting from trade diversion away from the United States.

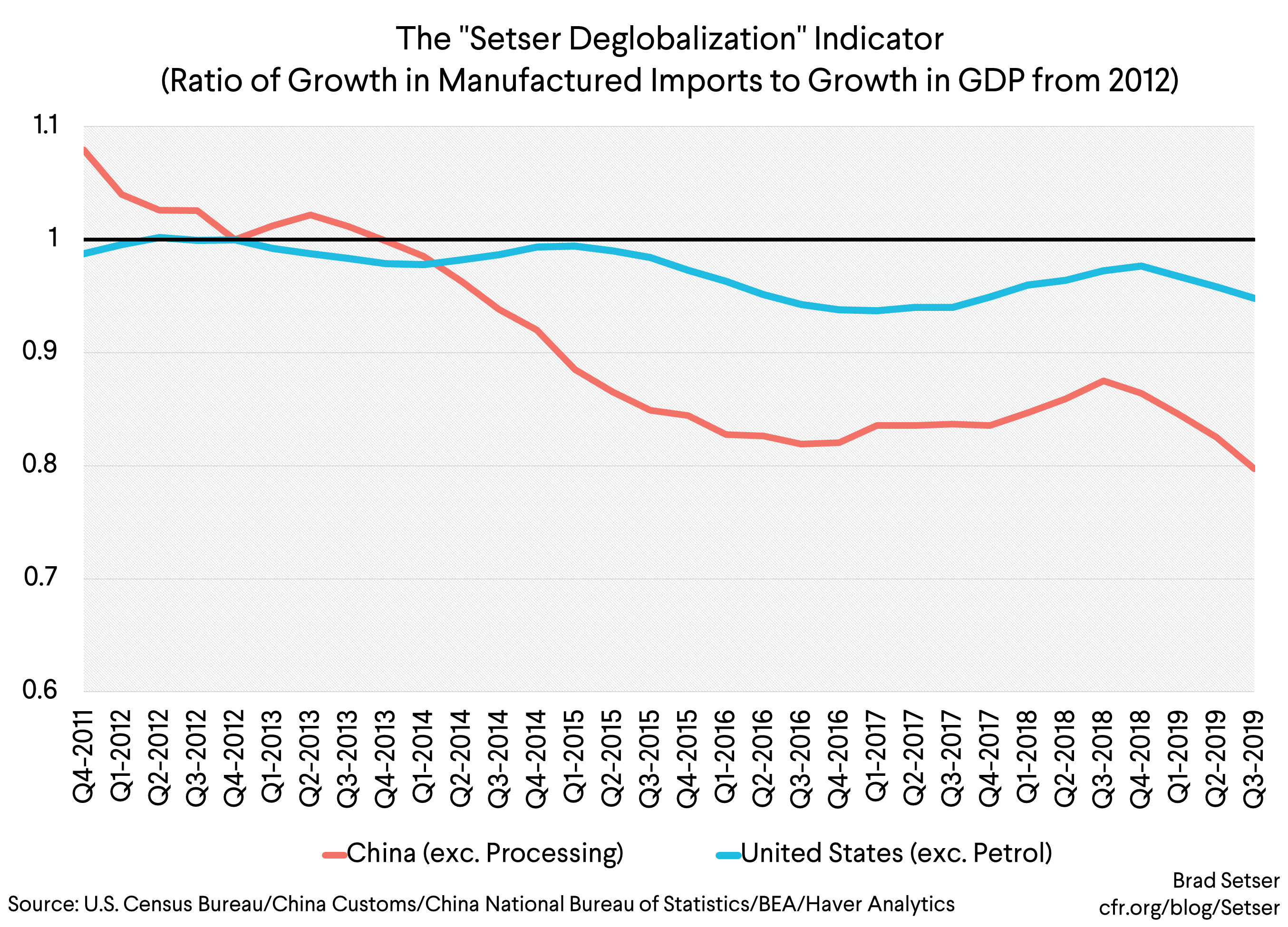

There is one more thing—the gap between China’s headline growth and its real import growth this year is unusually large. But the presence of a gap between China’s growth and China’s import growth isn’t unique. Over the last 6 years, China’s real import growth (using the goods data to avoid the problematic travel numbers that drive the services trade data) has been roughly half the growth rate in China’s overall economy. (Since 2012 the economy has increased by around 60 percentage points and real goods imports are up 35 percentage points. I have left out services because of a large data discontinuity in 2014, and ongoing evidence that they are poorly measured.)

Imports of manufactures for China’s own use (that is, excluding processing imports) have been sliding relative to China’s economy for quite some time.

This isn’t just something that I have noticed.

The ECB and the IMF both were on the case back in 2016. As was the Banque de France, which was somewhat more direct than either the ECB or the IMF (“the recent trade deceleration is closely linked to the shift of China’s production towards domestic demand,” updated graphs here).

It increasingly looks like China’s post global crisis import income elasticity is well below 1. That’s the internalization of supply chains—with more parts for electronics exports produced in China. And, perhaps, that’s China’s industrial policy in action.

Made in China 2025 aspires to reduce China’s dependence on imports in key sectors—and, well, in sectors ranging from medical equipment to electrical transmission to (now) memory chips, China is making progress. China’s current policy ambitions (in memory chips, logic chips, and civil aviation) in a sense imply a deglobalized China, one that imports less, and, barring a sustained raise in China’s trade surplus, that in turn implies a China that exports less.

* The real trade data—for goods—is in these charts.

** A consumption oriented stimulus would lower the trade surplus through a different mechanism. It would result in an appreciation of the real exchange rate, as a rise in Chinese consumption initially raises demand for Chinese goods, and that in turn would lead to tighter PBOC policy. The stronger real exchange rate then would slow exports, as the stimulus leads Chinese demand to crowd out production for exports.