Asia Still Lags When It Comes to FX Market Transparency...

Quarterly disclosure with a quarter lag doesn’t add much to the numbers already provided in the balance of payments (especially if it isn’t clear what is being disclosed). Semi-annual disclosure provides less information than what’s already available in the balance of payments.

The Economist—echoing the U.S. Treasury—argues that some Asian economies are becoming more transparent in their intervention in the currency markets. Korea and Singapore are in particular said to have increased their transparency by disclosing their intervention in the market (with a lag) not just the level of their reserves.

“Some countries have also taken steps to make their role in currency markets more transparent. America’s Treasury has welcomed decisions by South Korea and Singapore to start publishing regular data about their interventions.”

I will happily take the other side of this argument. The numbers that South Korea and Singapore have agreed to publish are extremely lagged, and add little to what they already publish in the balance of payments. And it isn’t actually clear if South Korea will publish numbers that correspond to its actual intervention, or something else.

Moreover, the disclosure of formal intervention has coincided with broader policy shifts that have made the disclosed intervention of the central bank less important than it used to be to understanding the broad impact of Korea’s government on the market.

Let’s start with what Korea and Singapore should be disclosing if the Treasury had insisted that they live up to global best practices. The most transparent emerging markets disclose actual intervention monthly, with a one month lag (India, Brazil, and Russia all meet this standard).

And I personally think disclosure of formal intervention should be paired with disclosure of the growth in foreign assets of sovereign funds, along with the sovereign wealth fund’s hedge ratio. The norm here though could be quarterly disclosure with a quarter lag (Norway’s sovereign funds, Norges Bank Investment Management, exceeds this standard)

What has Korea agreed to do?

Quarterly disclosure with a quarter lag (perhaps).

We don’t actually know what Korea is disclosing, as Korea’s disclosed numbers don’t really line up with the numbers in the balance of payments (combined with changes in the Bank of Korea’s forward position).* The Koreans have long argued foreign exchange swaps shouldn’t count as intervention, so perhaps they aren’t disclosing them?

The Koreans are right that the swaps themselves are not intervention. But the swap also should reduce on balance sheet reserves. In the past, spot intervention has been paired by swaps that have both “sterilized” the actual purchase in the market, and obscured the scale of Korea’s actual intervention. For more on the impact of swaps on reported reserves, see this post on Taiwan.

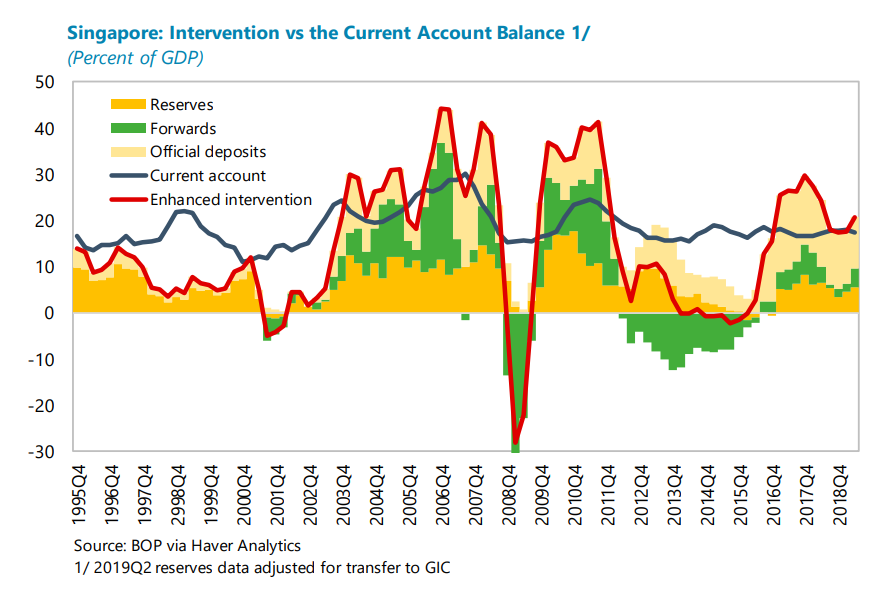

What has Singapore agreed to? Semi-annual disclosure with a half year’s lag. That’s just lame. Intervention in say January won’t be disclosed until the end of December.

And neither Korea nor Singapore has agreed to any substantive disclosure of the activities of their sovereign funds. Korea’s National Pension Service is big and fairly transparent.** Singapore’s Government Investment Corporation is big and not at all transparent. It for example has never disclosed its size.

Frankly, it isn’t clear that the new disclosure will tell us much more than what is already in the quarterly balance of payments and the monthly release of each countries reserves according to the IMF’s standard template.

In Singapore’s case, the trumpeted new disclosure is actually less than what’s in the quarterly balance of payments (admittedly, you have to know where to look in the balance of payments, as a lot of the activity doesn’t take place in the “reserves” line item).

To be fair, if you didn’t pay attention to all the line items in the balance of payments that Singapore has used to move a portion of its reserves over to its sovereign wealth fund in the past and instead just watch the “reserves” line there may be a bit of additional information. And Singapore’s disclosure that it shifted a large sum of its reserves over to the GIC this spring was helpful.

But to get credit for more transparency, you really need to start disclosing information that impresses the professional reserve watchers, not just the amateurs.

What would be a big increase in transparency?

Monthly disclosure by all the major Asian economies using the template provided by the Reserve Bank of India (Table 4).

Consistent disclosure by the GPIF in Japan—the Treasury cannot ignore this flow much longer given its size.

And a commitment by Taiwan to disclose its true intervention, including its forward book. Even quarterly data would be a big improvement over what we have now.

* The disclosed number should roughly match BoP reserves (quarterly or semiannually) net of interest income (something like 2 percent—or less—or $400b or so) plus the change reported forwards in the SDDS reserve template. It doesn’t quite line up though.

** Right now the government of Korea is rapidly building up its unhedged foreign assets. It does so by putting around 50 percent of the funds coming into the national social security fund into foreign assets. Korea is pretty transparent about this. We know it doesn’t hedge this large flow. Whether it is called intervention or not, these kinds of unhedged flows unambiguously have an impact on the market. Private institutional investors—like life insurers—typically would hedge.

*** The transfer also showed up in the balance of payments (it is hard to hide something that big), but the balance of payments comes out with a quarter lag.