China’s Non-Reserve Official Assets, and How They Might Help Us Understand China’s Forward Book

China’s headline reserves fell by around $45 billion in October, dropping to $3.12 trillion. Many China reserve watchers expected a bigger fall. Moves in the foreign exchange (FX) market knocked around $30 billion off China’s roughly $1 trillion portfolio of euros, pounds, and yen assets in October. After adjusting for these valuation changes, China might only have sold a bit over $15 billion or so in October. That is less than my estimates of the true pace of sales in September.

But it bears repeating that the changes in headline reserves often do not provide as good an estimate of China’s actual activities in the market as the PBOC’s balance sheet data and the FX settlement data. Neither is yet available for October. I at least do not yet have confidence that the pace of underlying sales really slowed.*

China’s October reserves, though, aren’t the real subject of this post.

Rather, I want to make two arguments about the non-reserve foreign assets held by Chinese state institutions. The second is a bit speculative. It is meant to encourage more work, not to provide a definitive answer.

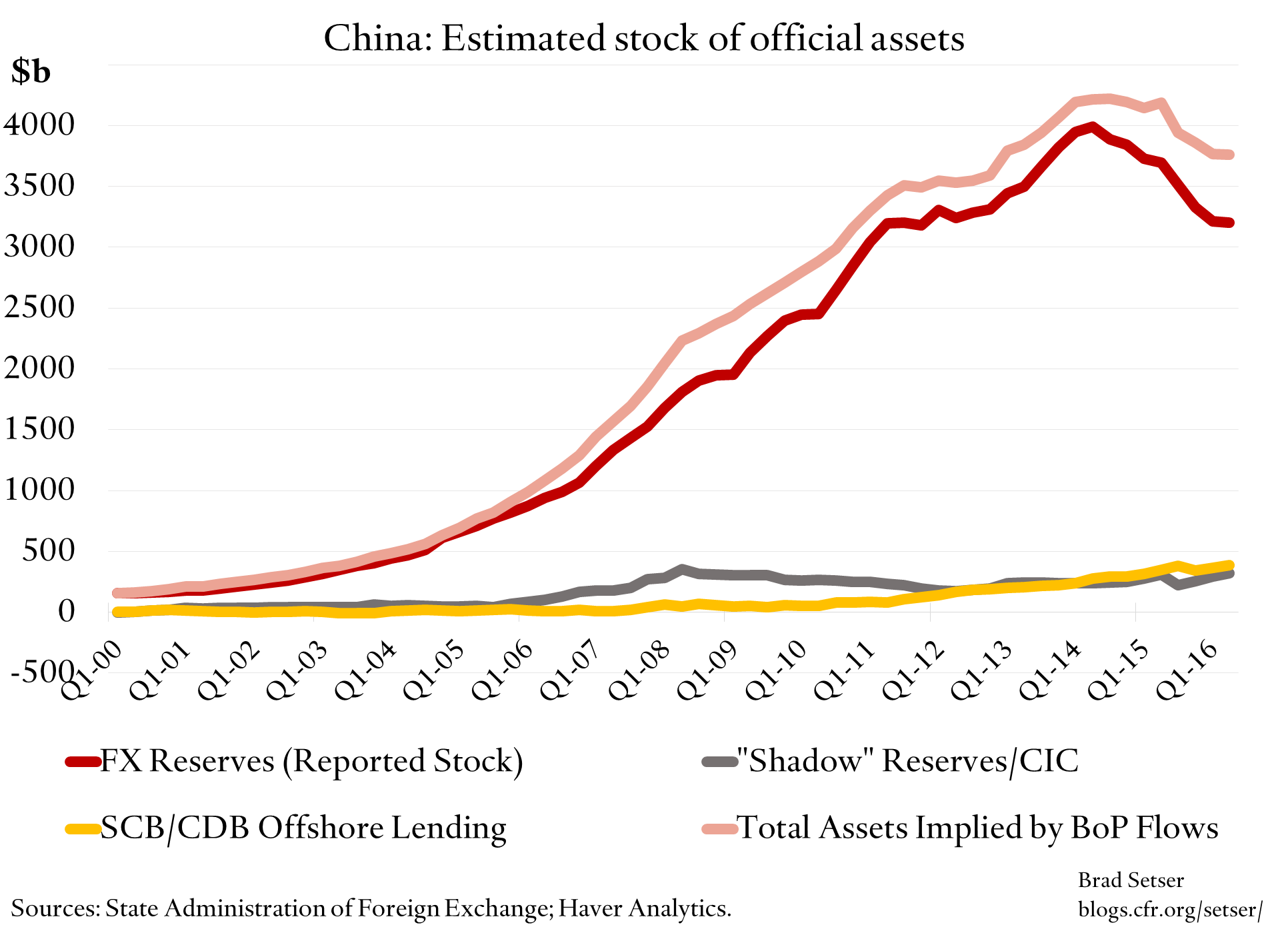

One, China’s state sector still has a lot of foreign assets, assets that are not formally counted as FX reserves. The state banks hold foreign exchange as part of their capital, thanks to past recapitalizations. The state banks hold foreign exchange as part of their regulatory reserve requirement (the banks have to set aside a large portion of every deposit at the PBOC). This pool of foreign exchange is not counted as part of China’s formal reserves. The China Investment Corporation (CIC—China’s sovereign wealth fund) holds some foreign assets in its portfolio, and financed the purchase of those assets with domestic borrowing. The China Development Bank (CDB) and the China Export-Import Bank have also made significant loans to the rest of the world. There is room to debate just how big the state’s non-reserve portfolio is, but the balance of payments indicates something like $200 billion in cumulative outflows through the banks and China Investment Corporation, and well over $300 billion or so in offshore loans—mostly, I assume, from the CDB.

Two, those foreign assets have created a set of state actors that have an underlying currency mismatch on their balance sheet, and thus, a set of institutions that are naturally exposed to changes in the yuan’s value.

There are a lot of emerging economies where big firms raise funds by borrowing in foreign currency, and take on a “balance sheet” mismatch as a result. They lose out in a depreciation. A portion of China’s balance sheet risk though is the other way around. The state banks and the CIC have raised funds in yuan and are holding foreign currency-denominated assets. As a result of this mismatch the banks and the CIC appear to gain if the yuan depreciates against the dollar. But they also stand to lose if the yuan rises against the dollar.

In the past, this was not just an academic risk. In fact, for many years, the state banks had trouble finding a market actor that would allow them to hedge (the banks would in effect enter into a trade where they would give up the gains from a fall in the yuan, in return for protection against the losses that would come with a rise in the yuan). It is possible that they hedged this risk in the past with the central bank (this would imply that in the past the PBOC had more foreign currency exposure than implied by its formal reserve holdings).

So I wonder if some of the unusual activity that many have observed in the FX market over the past year comes as a result of the state banks and the CIC moving from hedging their unmatched foreign currency book with the central bank (or not hedging it at all) to hedging it with the market. By taking on the risk that the yuan would appreciate (which the state banks need to move off their books to be FX matched), the foreign exchange market would get the gains from yuan depreciation.

I have a lot more confidence in the first argument than in the second argument, which is at this stage just a hunch.

That is a critical caveat.

Let me start with a bit of history.

Back in 2003, the PBOC provided $45 billion in foreign exchange reserves to the Bank of China and China Construction Bank. China could have done the recapitalization in other ways—most bank recapitalizations are done by giving the banks domestic bonds (with the government getting bank equity in exchange). But it had plenty of foreign exchange reserves, and it did the recapitalization with its reserves.

At 2003 exchange rates, these foreign assets had a value of 372 billion yuan ($45 billion times 8.28 yuan/dollar).

Once the yuan started to appreciate in 2005, though, the bank capital was shrinking in yuan terms. By 2008, at 6.83 yuan to the dollar, the same foreign assets were worth just over 300 billion yuan. The banks’ capital from this part of the 2003 and 2005 recapitalization, in yuan terms, had shrunk by a bit more than 15 percent.

Some people suspect—based in part on the data China used to release as part of its disclosure of the foreign exchange balance sheet of the state banks—that the banks could hedge this risk with China’s authorities in one way or another (see my 2009 working paper). The banks, after all, were doing the PBOC a favor by holding their capital foreign exchange, rather than selling the foreign exchange (back to the PBOC) and adding to China’s fast growing reserves.

And over time the pool of foreign assets held by the state commercial banking system increased, and rose well beyond those that stemmed directly from the use of foreign exchange reserves in the recapitalization of the state banks.

Specifically, starting in 2007, the PBOC forced the banks to meet a portion of their regulatory reserve requirement in foreign exchange. Back in 2011, Guonan Ma, Yan Xiandong, and Liu Xi wrote: “on several occasions, Chinese commercial banks reportedly were asked to deposit foreign currency with the PBOC to meet the reserve requirements on their local currency deposits.” This was a way of keeping the foreign exchange off the PBOC’s balance sheet. China’s problem back then was that its reserves were growing too fast. Between mid-2007 and mid-2008, the banks were encouraged to hold $200 billion of foreign reserves to meet the reserve requirement on their domestic deposits (and likely were allowed to hedge the FX risk at the central bank, as foreign exchange was being held against domestic currency deposits). The PBOC didn’t want the world to know just how much it was in effect intervening in the market at the time; it also wanted to keep its reserves from rising through $2 trillion.

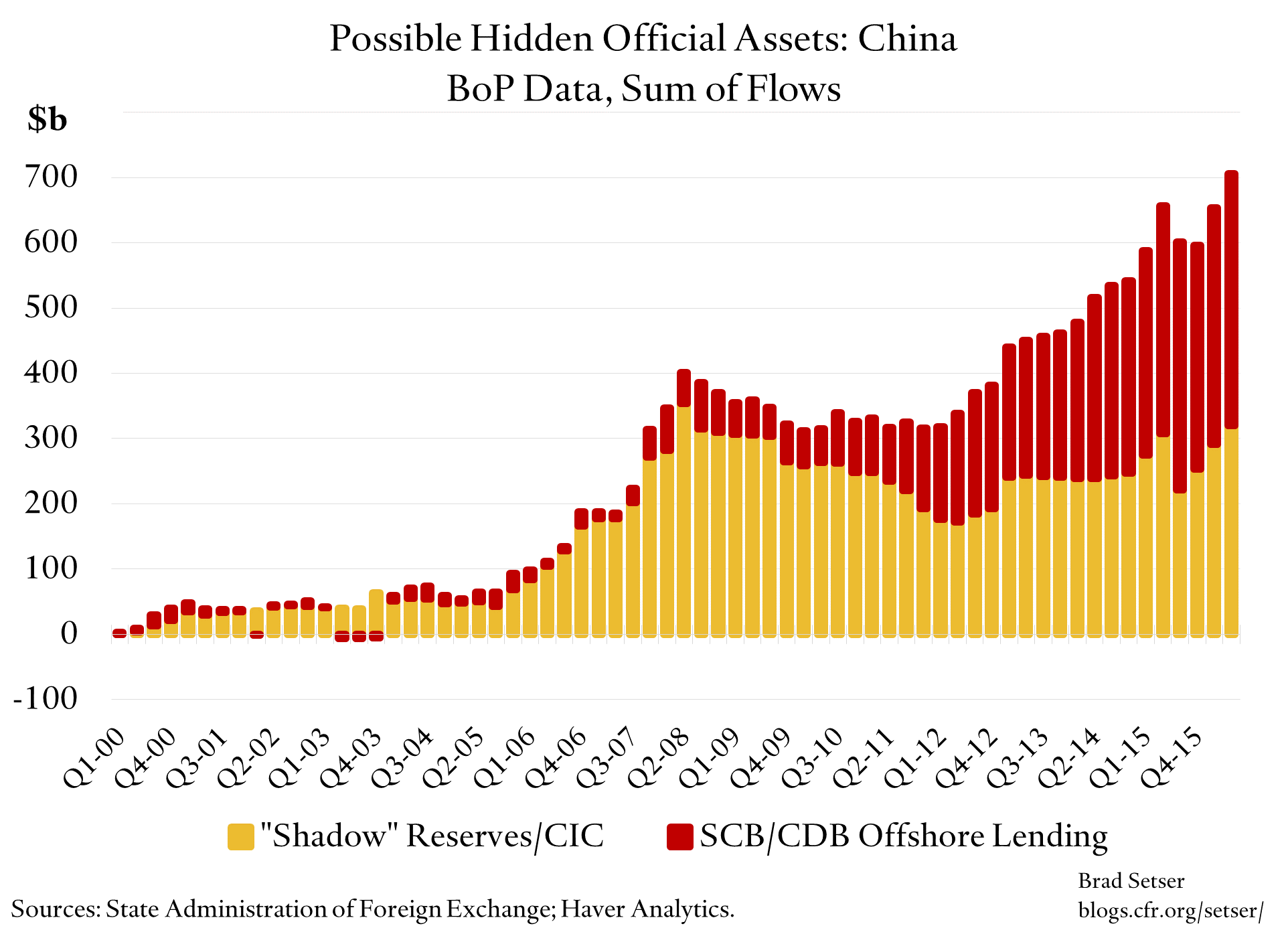

The foreign exchange hidden in the state banks during this period explains most of what I labelled “shadow” reserves in the chart (needed data is only available through q2 2016).

At various other points in time, other Chinese state institutions—the “national team” to use a term popularized during China’s stock market intervention—also issued bonds domestically to finance the purchase of foreign assets. The China Investment Corporation for example.

And after the crisis, the nature of the buildup of non-reserve foreign assets in the Chinese state system changed. The China Development Bank emerged as a critical source of outflows when it went on a global lending spree. Such lending substituted for further reserve growth. State-backed institutions remained fairly active in the foreign exchange market, but China started to recycle more of the foreign exchange it was building up by making loans to a range of riskier borrowers—and put a bit less into U.S. bonds.

The CDB finances itself primarily by selling domestic, yuan-denominated bonds. The CDB also now has, according to the balance sheet data in its 2015 annual report, $260 billion in foreign currency loans (and a total of around $295 billion in foreign currency denominated assets) on its balance sheet and only $135 billion in on-balance-sheet foreign currency liabilities. It thus has an explicit funding gap—more visible foreign currency assets than visible foreign currency liabilities, and it fills the gap in part through around $80 billion in swaps (p. 196 of the 2015 annual report, thanks to a friend for pointing this out). (One small note: the CDB’s total overseas loans seem bigger than foreign currency loans).

The buildup of these foreign assets can be tracked, indirectly and imperfectly, through China’s balance of payments data (with a bit of help from the PBOC’s balance sheet data). There is a line item in the balance of payments that maps relatively well to the portion of the banks reserve requirement that was held in foreign currency (also reported on the PBOC’s balance sheet, as “other foreign assets”). China reports its portfolio investment abroad—and while some of that is private, a lot clearly comes from the China Investment Corporation. And it reports the foreign loans of the banking system. It is reasonable to think that a lot of these loans are from the China Development Bank.

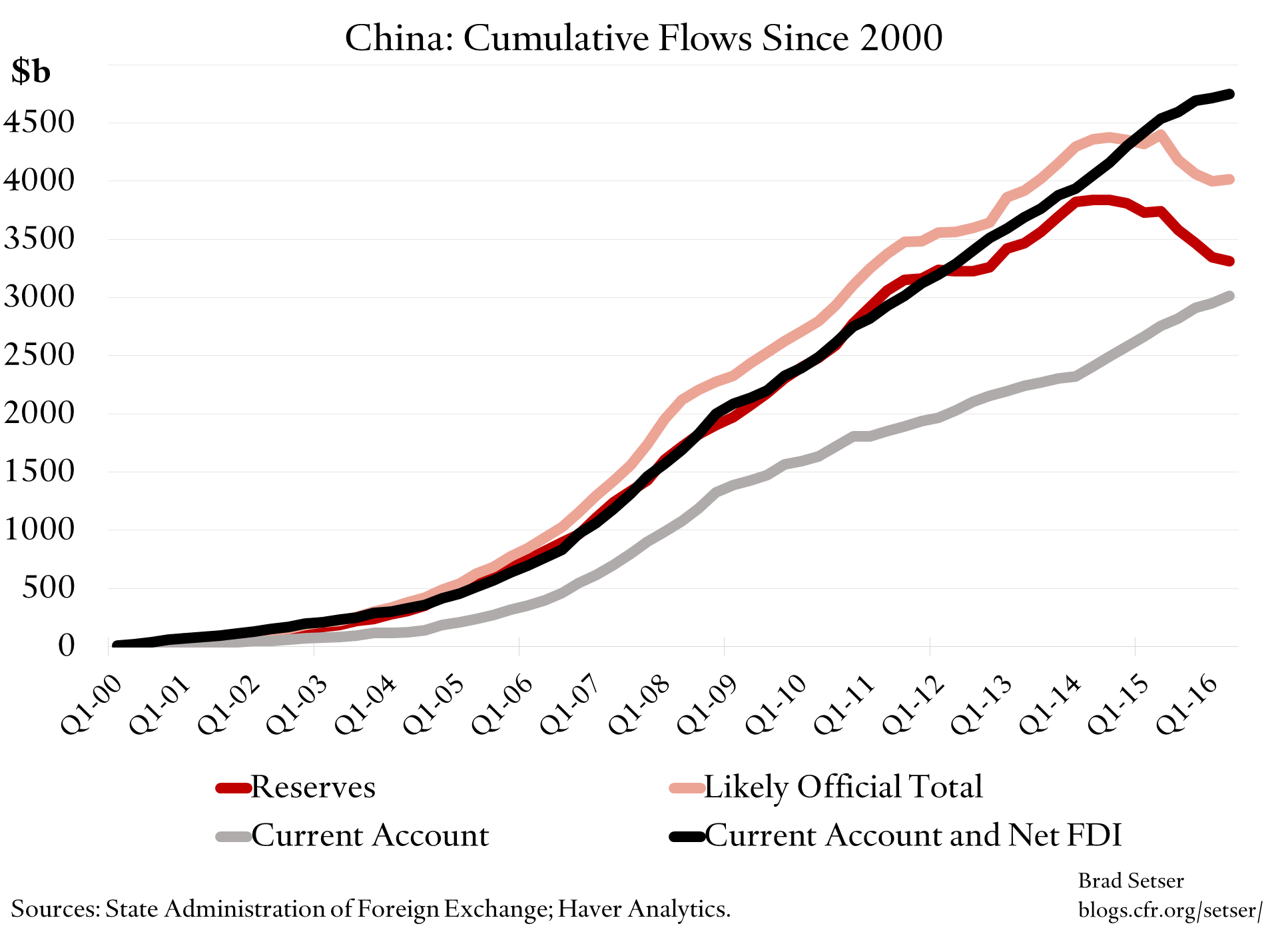

Sum up the outflows through all these channels in the balance of payments over time, and you can estimate the total non-reserve holdings of China’s “official” sector—foreign assets that aren’t part of reserves. I get a total of almost $700 billion, roughly split between shadow reserves held in the banks and in the CIC, and the overseas lending of the state banks (mostly the CDB). My chart treated all the outflows in certain categories of the balance of payments as official, which is likely an overstatement—there are about $90 billion in outflows from the qualified domestic institutional investor program, and some of those are private. Yet even if not all of the accumulated assets offshore are from the state banks, the CIC, and the CDB, it is reasonable to think most are.**

So how might this relate to China’s rumored forward book?

For those who need background (beyond this primer on modern intervention techniques from the BIS), there is an argument in parts of the foreign exchange market that China doesn’t really have $3.12 trillion in foreign exchange reserves, because it has sold some of its reserves forward. Those rumored forward sales allowed some in the market to place bets that the yuan would depreciate, and depreciate by more than what was “priced” in the forward market.

The PBOC now discloses a $45 billion short position (up from $29 billion earlier this year), but many in the market believe the real position is larger.

It though seems to me possible that a number of big state institutions might be the ones who have sold dollars forward.

We know that the state banks, the CIC and the CDB all have significant foreign currency assets—and since thy finance those foreign currency assets in part with yuan borrowing, their balance sheets have an underlying foreign currency mismatch. Specifically, they need to protect themselves against the risk the yuan rises (and they gain if the yuan falls). That makes them natural buyers of protection against yuan appreciation, and natural suppliers of protection against yuan (and offshore CNH) weakness.

Take an overly simple example. Suppose the CDB has raised funds by selling a one year bond denominated in yuan. And it has made a one year dollar-denominated loan. It loses if the dollar depreciates relative to the yuan (the yuan appreciates) over the next year. And it can protect itself against the risk that the yuan will appreciate by selling the dollar it expects to get back from the loan forward for an agreed sum of yuan, effectively locking in the yuan’s future price today. (A swap does the same thing, while providing the bank with actual dollars to lend out)

My guess is that the state banks hedged against the risks of yuan appreciation with the PBOC in one way or another, back during the period of yuan appreciation. Or got regulatory approval not to hedge. That would imply that the PBOC took on some of the foreign currency risk associated with what might be called China’s shadow reserves; the foreign currency risk wasn’t all being held on the books of the state banks and the CDB.

And maybe now some state institutions that previously hedged against yuan appreciation with the PBOC hedge in the offshore market? Back when the yuan was rising, the private market wanted to bet on the yuan’s appreciation, which wasn’t much use to banks that themselves needed to hedge against appreciation—but the story changes if the market wants to bet on yuan depreciation.

There is a tiny bit of hard data to support this theory, notably the indications in the CDB’s annual report that it has a large swaps book—that though doesn’t tell us who the CDB swaps with (and if the CDB does swaps with the State Commercial Banks, who the state banks then swap with).

And I have long wondered how the state banks hedged the foreign currency risk associated with the requirement that they hold a portion of their regulatory reserve requirement in foreign currency, which added to the risks that they took on by holding foreign exchange as part of their regulatory capital.***

Fundamentally though this is a hypothesis to be tested with more financial sleuthing. It is not something the available data proves.

And of course it is something that the Chinese could clarify with a bit more transparency about just how the foreign currency risk associated with China’s non-reserve official assets has been managed over time. Right now there are only hints.

If this all is even roughly right, China’s central bank isn’t failing to report its forward book to the IMF. The PBOC isn’t the one that is selling its foreign exchange reserves forward. The state banks are.

At the same time, one of China’s hidden buffers—the underlying foreign currency position of the large state institutions that had been building up what might be called China’s shadow reserve portfolio—is now being used in a new way to help stabilize the offshore market.

To be technical, a hidden long—the FX risk that the state institutions either didn’t hedge or hedged with the PBOC—is being reduced. To be more colloquial, China has used up a lot of ammunition in the market over the last year, but it also likely started with a bigger stockpile than most realized.

* The $135 billion reserve outflow in the q3 balance of payments has attracted a bit of attention. That suggests an underlying monthly pace of reserve sales in q3 of about $40 billion a month. Some bank analysts have noted that there is a big gap between the balance of payments data and the change in headline reserves. That is true. But it also isn’t significant. The PBOC’s own balance sheet data for q3 suggested close to $110 billion in reserve sales (see this), and that is a better indicator. Other “proxies” that include the state banks show somewhat smaller sales, suggesting that the banks bought some foreign exchange off the books of the PBOC.

** My estimate of the growth in China’s state portfolio tracks closely to the cumulative current account surplus—or actually the cumulative surplus in the current account and the FDI balance—until the recent period. The balance of payments data clearly implies that a lot of actors, not just the central bank, built up a reasonably sized foreign portfolio from 2005 to 2014, and that overtime the nature of this portfolio shifted, with the CDB assuming a bigger role. I count other foreign assets, all portfolio outflows, and all bank “loans” to the world in the balance of payments (other, loans, assets) in my measure. Some of the portfolio outflows in particularly clearly come from the qualified domestic institutional investor program; that would reduce the total by $90 billion or so. I avoided this adjustment because of the added complexity—and because many of the portfolio outflows really map to periods when either the banks or the CIC were known to be buying external assets.

*** The PBOC’s data on the foreign currency balance sheet of the state banks used to report a line item, under funding sources, called “purchases and sales of foreign exchange.” Back in 2009, I thought this line item was explained by swaps the banks conducted with the PBOC, where they essentially swapped yuan for dollars. This was the funding source the banks used for the ill-fated foray in the global bond market in 2005 and 2006 for example. China stopped publishing this line item at the end of 2015. One way of understanding my thesis is more or less as follows: the state banks (and the CDB) previously were selling dollars forward to the central bank, and rolling that position—and the PBOC was in effect holding foreign currency risk off its balance sheet. That explains the growth over time in foreign currency funding from “purchases and sales” on the state banks balance sheet. And the PBOC no longer needs to take the other side of the trade, as the state banks can easily find other actors who want to take on the risk of yuan appreciation in return for the gains from yuan depreciation. (And the banks themselves do not want to make an outright bet on the yuan; they need to try to match their books). Incidentally, the China Development Bank appears to be part of the state commercial banks’ foreign currency balance sheet data set.The CDB has at times been viewed as a commercial bank and at times as a policy bank, but in the data, it is a commercial bank—hence the steady growth in overseas loans from 2010 on in the aggregate foreign currency balance sheet (link).