Shadow FX Intervention in Taiwan: Solving a 100+ billion dollar enigma (Part 3)

By experts and staff

- Published

Brad W. SetserCFR ExpertWhitney Shepardson Senior Fellow

Brad W. SetserCFR ExpertWhitney Shepardson Senior Fellow- Guest Blogger for Brad Setser

This is the third post in a series* on Taiwan’s life insurers and their private & sovereign FX hedging counterparties. It’s the product of a collaboration with S.T.W**, a market participant and friend of the blog. Printable versions of entries in this series will be available in pdf format on his site (Concentrated Ambiguity).

Part Three: A Quick Primer on FX Hedging

This blog is intended to give a brief overview of the derivative instruments institutional investors have at their disposal when hedging FX exposures. It is far from exhaustive regarding the exact factors involved in pricing the instruments[1], but should provide the big picture intuition as well as highlight the fungibility of the various hedging methods.

A. Initial Situation

Staying with the topic of this series of blogs, the issue will be framed from the perspective of a Taiwanese life insurer selling a TWD-denominated policy to a domestic customer and, due to lack of alternatives, decides to allocate all of the received premiums to overseas fixed income instruments. The FX risk of these are then hedged via a variety of methods.

B. Physical Hedging

Going back in time to before the advent of liquid FX derivative markets, the only way for an insurer to balance FX exposures would be by creating FX-offsetting on-balance sheet positions. In an initial step, the insurer would take TWD deposits it received, convert these into USD in the FX spot market and subsequently acquire a USD-denominated bond. Following this transaction, the insurer is exposed to an obvious FX mismatch: the asset it owns is denominated in USD, while its corresponding liability is TWD-denominated. It can neutralize this risk by borrowing USD funds (in a size equal to the policy written) from an overseas bank, convert these into TWD in the FX spot market and keep them either on deposit with banks in Taiwan or acquire a TWD-denominated safe asset. Now, the insurer holds a USD bond and a TWD deposit, which are matched by equally-sized liabilities, a TWD insurance policy and a USD bank loan.

Since matching FX risks purely on-balance sheet is a cumbersome process, practically all end users today rely on the derivative solutions that follow.

C. FX Forwards I

Forward FX markets developed as a natural add-on to the spot market. Instead of exchanging currencies now, participants agree today to exchange a fixed amount at a designated exchange rate on a future date. Given that forwards are priced off the prevailing values in FX spot, they (assuming regular market conditions) exhibit extremely high correlations with FX spot markets, especially at short tenors. Thus, an insurer which has built up the initial FX imbalance as in the prior example, simply enters into a long TWD, short USD position in the forward market, which at trade initiation has a zero market value. This position, due to its high correlation with FX spot, will balance any FX profits or losses generated by the on-balance sheet FX mismatch, insulating the insurer from FX swings at the aggregate level.

D. Cross-Currency Swaps (CCS)

Cross-currency swaps are the modern incarnation of the physical hedging previously analyzed and are best approached as collateralized lending with foreign currency collateral. Upon receiving TWD funds as a result of selling a TWD- denominated policy, the insurer, instead of exchanging TWD for USD in the spot market, searches for a lender willing to provide USD by pledging its TWD deposits as collateral. Once a counterparty is found, currencies are swapped in a symmetrically-collateralized process, after which the insurer acquires the desired USD-denominated bond. During the contract, the insurer will—in a cross-currency basis swap, the most commonly traded variant—have to pay its counterparty USD Libor rates, while it will receive TWD interbank rates in return. At termination, the exact amount of funds swapped initially is handed back. Since the insurer only borrowed USD, which it will hand back at termination after it sells the USD- denominated bond, it was at no time exposed to FX risk.

E. FX Forwards II: FX Swaps

Hedging via FX forwards can also be approached through the collateralized lending lens. To do so, spot and forward transactions are paired[2] and conducted with a single counterparty. In such a case, the transaction is referred to as an FX swap. As in a CCS, funds are exchanged at initiation, however no interest payments are affected during the contract. Instead, the closeout of the trade is set (at the time the trade is established) based on (primarily) interest rate differentials in the two currencies, usually leading to a different exchange rate at close out.

F. Dealer Intermediation and Fungibility

All of the above instruments are traded over-the-counter (OTC), requiring end users to enter them with dealer banks. These will intermediate supply and demand across their client base, match orders via the interbank market or utilize their own balance sheets to facilitate clients’ hedging demands. From the dealer’s view, the products are fungible, as the smallest decomposable fragment of each are linear exposures to FX risk and interest rate risk (in both currencies). As seen, an FX swap can easily be decomposed into a forward and spot transaction; decomposition of a CCS is similar but requires an additional position in interest rate swaps. Lastly, it should be noted that FX forwards/swaps are largely used by institutions hedging risk on the asset side of their balance sheet (usually at relatively short tenors rolled over indefinitely), while CCS are longer-term and preferably used by institutions hedging the risk of foreign currency debt issuance.

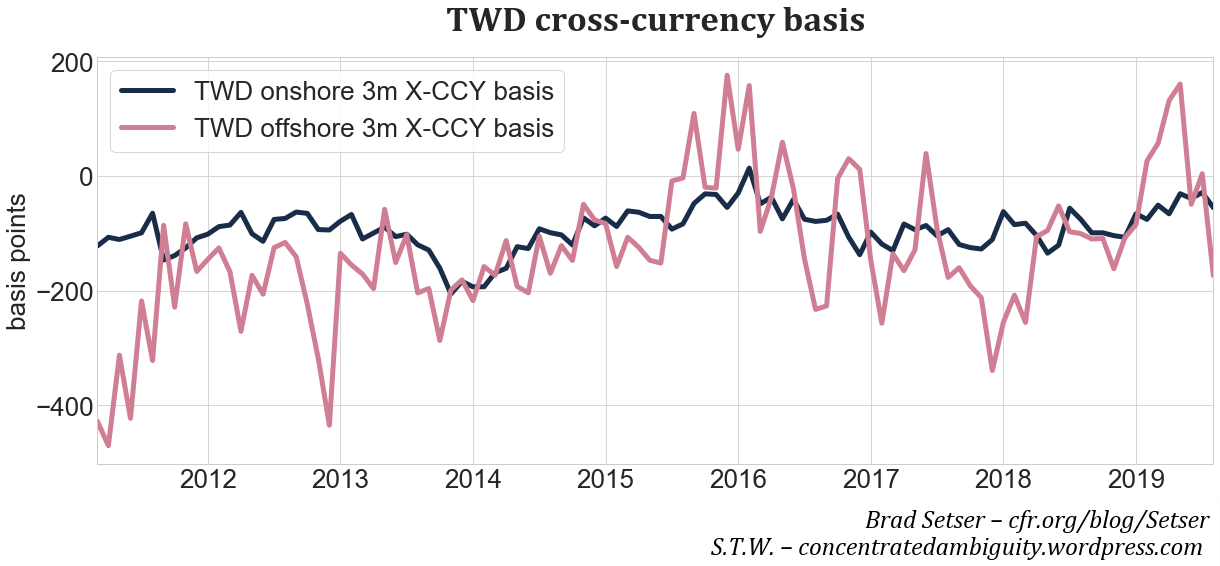

Taiwan’s onshore derivative market allows the trading of all of the above products, of which lifers show a clear preference for FX swaps. In addition, Non-Deliverable Forward (NDF) USD/TWD contracts are traded in offshore markets, which lifers tend to access opportunistically[3], when favorable pricing conditions arise.

* The Council on Foreign Relations takes no institutional positions on policy issues and has no affiliation with the U.S. government. All views expressed on its website are the sole responsibility of the author or authors.The Council on Foreign Relations takes no institutional positions on policy issues and has no affiliation with the U.S. government. All views expressed on its website are the sole responsibility of the author or authors.

** Contact at [email protected]

[1] This blog is loosely based on a (slightly) longer treatment of the same subject in the following post, ’FX-hedged yields, misunderstood term premia and $1tn of negative carry investments’. For a more exhaustive treatment, see any markets focused finance textbook.

[2] When not paired officially, the contract is not referred to as an FX swap, but the collateralized lending angle still holds, even if executed with different counterparties.

[3] In 2014, the CBC deregulated access to global NDF markets by overseas branches of Taiwanese banks. Given these are frequently owned by a common holding company as the life insurers and facilitate their trading, the ease of accessing NDFs by lifers for hedging purposes has increased substantially. Nonetheless, the offshore market remains less liquid than its onshore equivalent, featuring higher bid-ask spreads as well as higher volatility, thus situating it as an opportunistic outlet rather than a mainstay in lifers’ FX hedging.