Devaluation Risk Makes China’s Balance of Payments Interesting (Again)

A deep dive into the details of China’s balance of payments over the last few quarters of data. During the dollar’s depreciation in 2017 and the first quarter of 2018, it looks like China was adding to its official assets once again—though the growth largely came from the state banks.

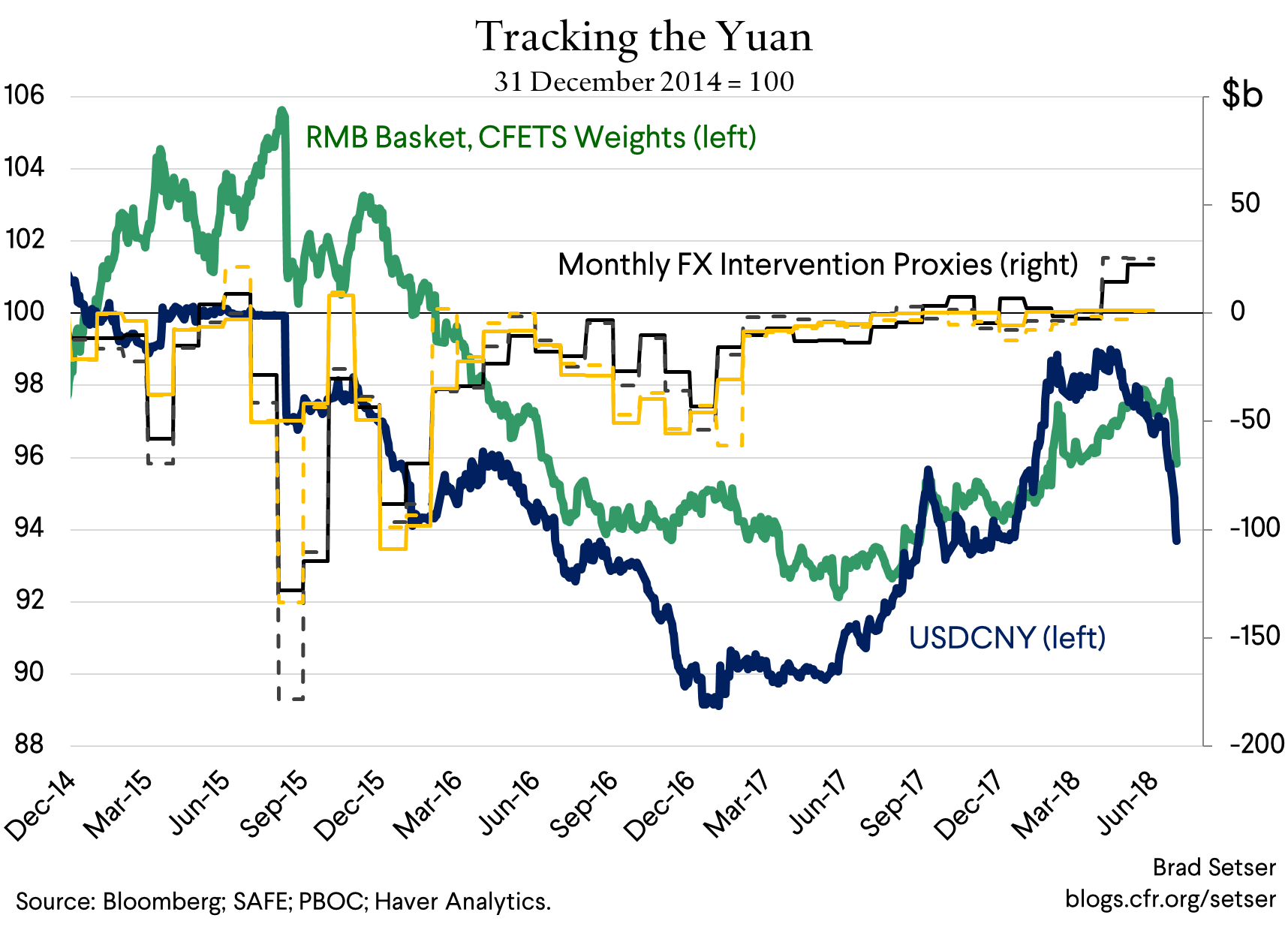

China allowed the yuan to strengthen a bit against a basket of the currencies of its trading partners in the first five months of this year.

When the dollar was weak in the first part of the year, the yuan strengthened against the dollar by more than was needed to hold the yuan constant against a basket. And when the dollar shot back up in April and May, the yuan didn’t depreciate by as much as would be implied to hold the yuan constant versus the basket. Going into June, the yuan was up nearly 2 percent against the basket.

Obviously that changed recently. The yuan gave up its appreciation versus the dollar—and against the basket.

And with trade pressure building and the possibility that Trump might escalate and put tariffs on $250 billion or even $450 billion of U.S. imports if China responds to the first wave of “301” tariffs with tariffs of its own (as it certainly will do), the risk of a significant devaluation has returned. China has almost “used” up the space it bought by guiding the yuan up against the basket earlier—continued movement will raise questions about whether China’s authorities want a weaker yuan.

We often speak of intervention pushing a currency down, as sustained intervention is a sign of an undervalued currency. But in practice, on a day to day basis, China usually buys to slow the pace of appreciation (when the market wants to push the currency up), and sells to limit the pace of depreciation (when the market wants to push the currency down). Its intervention tends to block faster moves in both directions more than anything else.

And since capital flows (think of Chinese exporters choosing whether to sell dollars or not, or Chinese firms choosing whether to borrow in dollars or not) tend to chase recent currency moves, China tends to buy foreign exchange when the yuan is appreciating and sell foreign exchange when the yuan is depreciating.

That is why it isn’t all that surprising that,China—by my count—added close to $100 billion to “state” assets abroad in the first quarter. China’s currency would likely have appreciated more “but for” the rise in the foreign lending by the Chinese states banks and ongoing purchases of foreign debt and equity by Chinese state institutions. Their buildup of foreign assets substituted, in a flow sense, for outright PBOC intervention.

And the high frequency data for April and May shows if anything signs of faster asset accumulation. The FX settlement data showed net purchases by the state banks for the first time in a long-time. Settlement includes the activity of the state banks as well as the PBOC; it tends to be the most robust proxy of Chinese activity in the foreign exchange market.

June, of course, will be different. Record monthly depreciation and all. The Wall Street Journal reported that China’s state banks were selling foreign currency to limit the pace of yuan depreciation last week.

I want to step back a bit though—with the whiff of depreciation in the air, it is worth laying out what China’s balance of payments looks like on the eve of the initial round of what may escalate into a real trade war.

The Economist has focused on China’s current account, and has argued that it shows some signs of weakness.

I though think that the real focus should be on China’s financial account, which, in my view, has shown signs of strength over the last year.

That cuts both ways now.

On one hand, China has stockpiled a bit of ammunition that it could use if it wants to turn a trade war into a currency war, especially if it wants to try to pull off another managed depreciation. I assume that China wouldn’t want to let its currency enter into an uncontrolled float down, though that conceptually is another option: it is the managed fall down, not the depreciation per se, that tends to burn through reserves.

On the other hand, the strength of China’s balance of payments position over the last few quarters suggests that China also has the option to hold its currency relatively stable, whether against the dollar or against the basket, if it wants to. Even with the modest recent erosion in China’s current account surplus. Stability against the basket—and to a degree against the dollar—has led to a large reduction in the pace of capital outflows from China. Or at least created an environment where inflows balanced outflows.

Enough with the throat clearing. Time for some numbers.

China releases its detailed balance of payments data with a quarter lag. A quarter lag doesn’t sound like much, but in the era of Trump, a quarter is a long time—in q1-2018 the market was talking about the puzzle of dollar weakness amidst rising U.S. rates and relatively little trade action against China. That’s not the case now. In the second quarter, the dollar appreciated against most currencies, and the threat of a trade war became a lot more tangible.

The first quarter data though is still interesting.

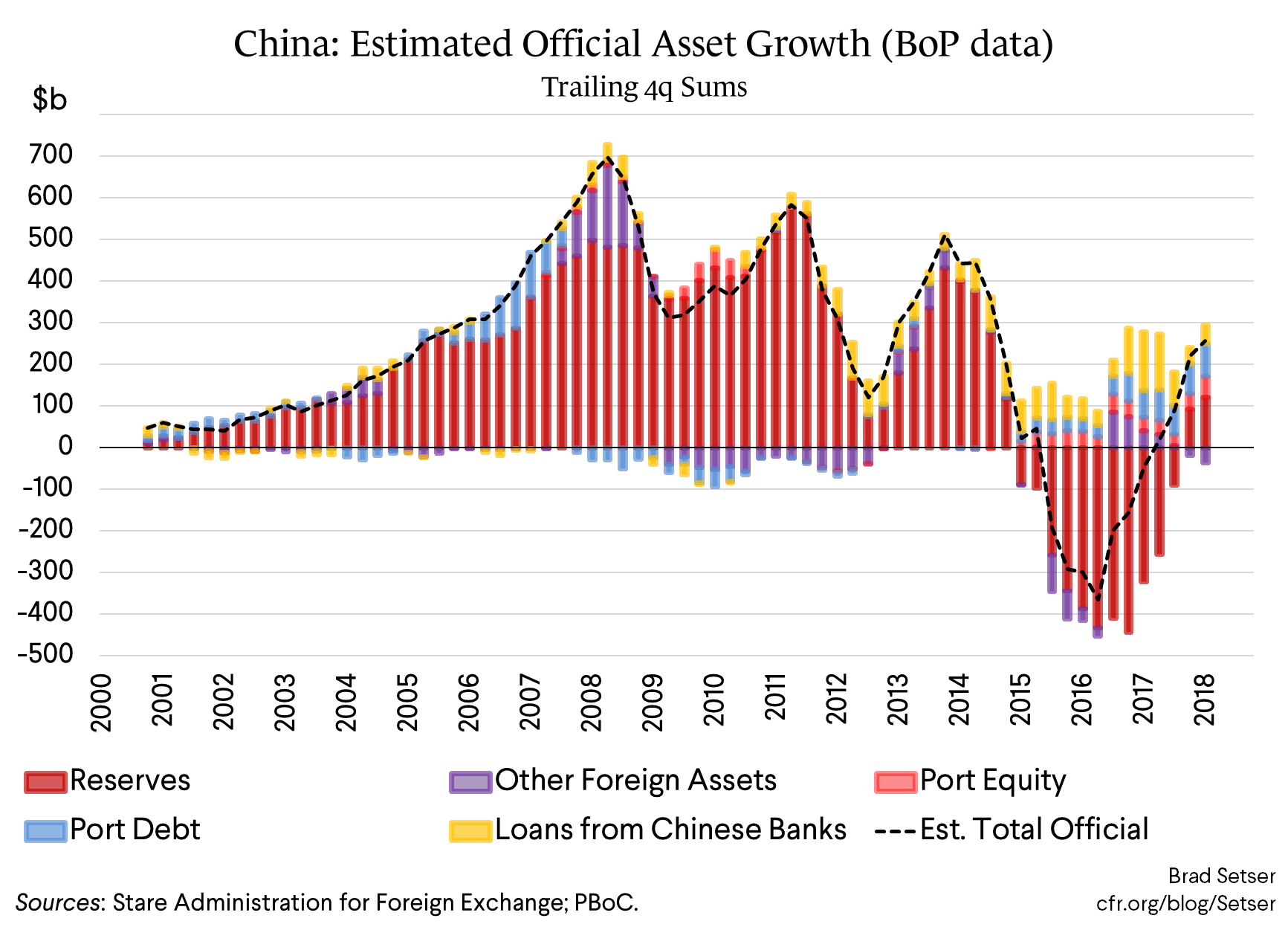

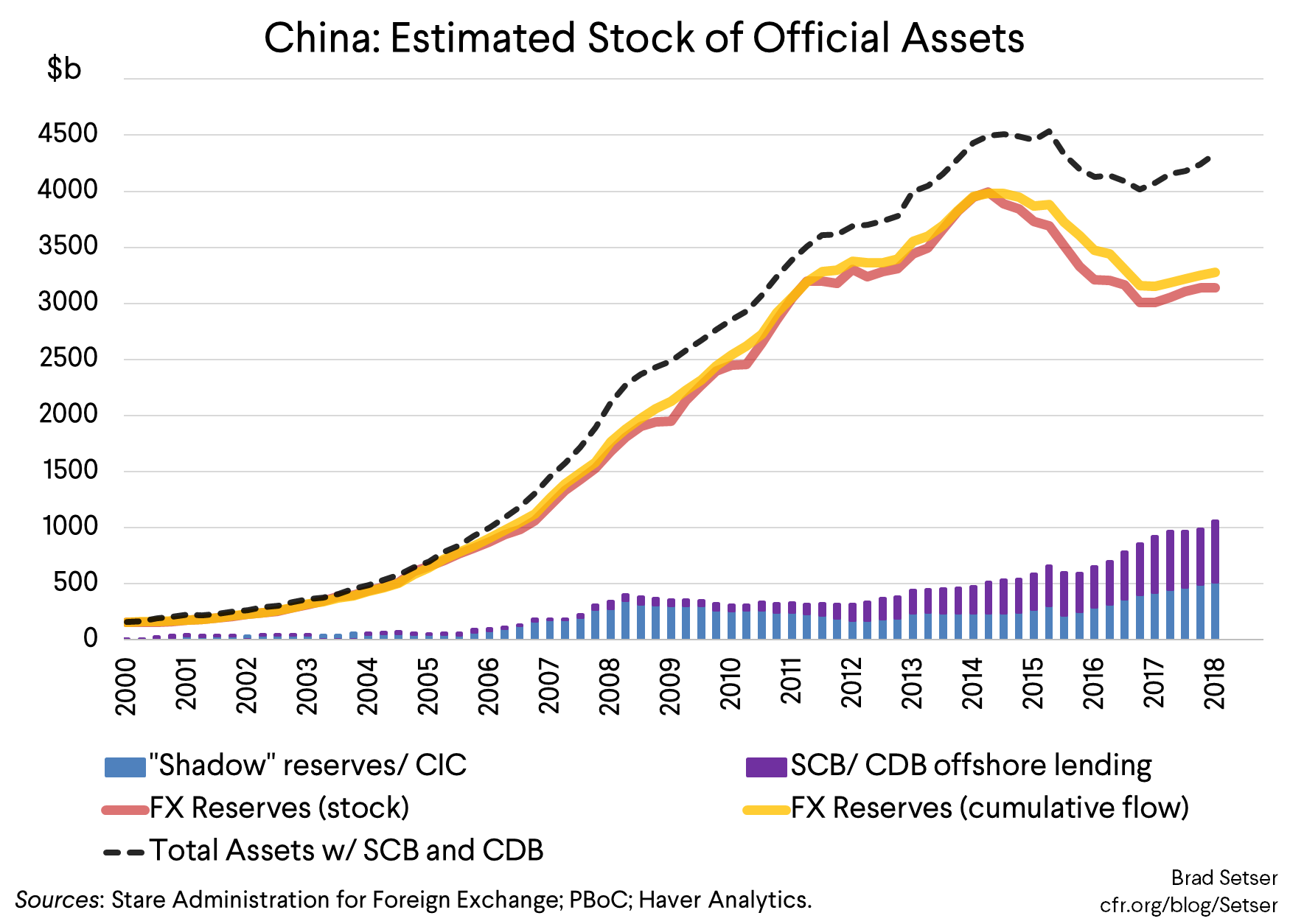

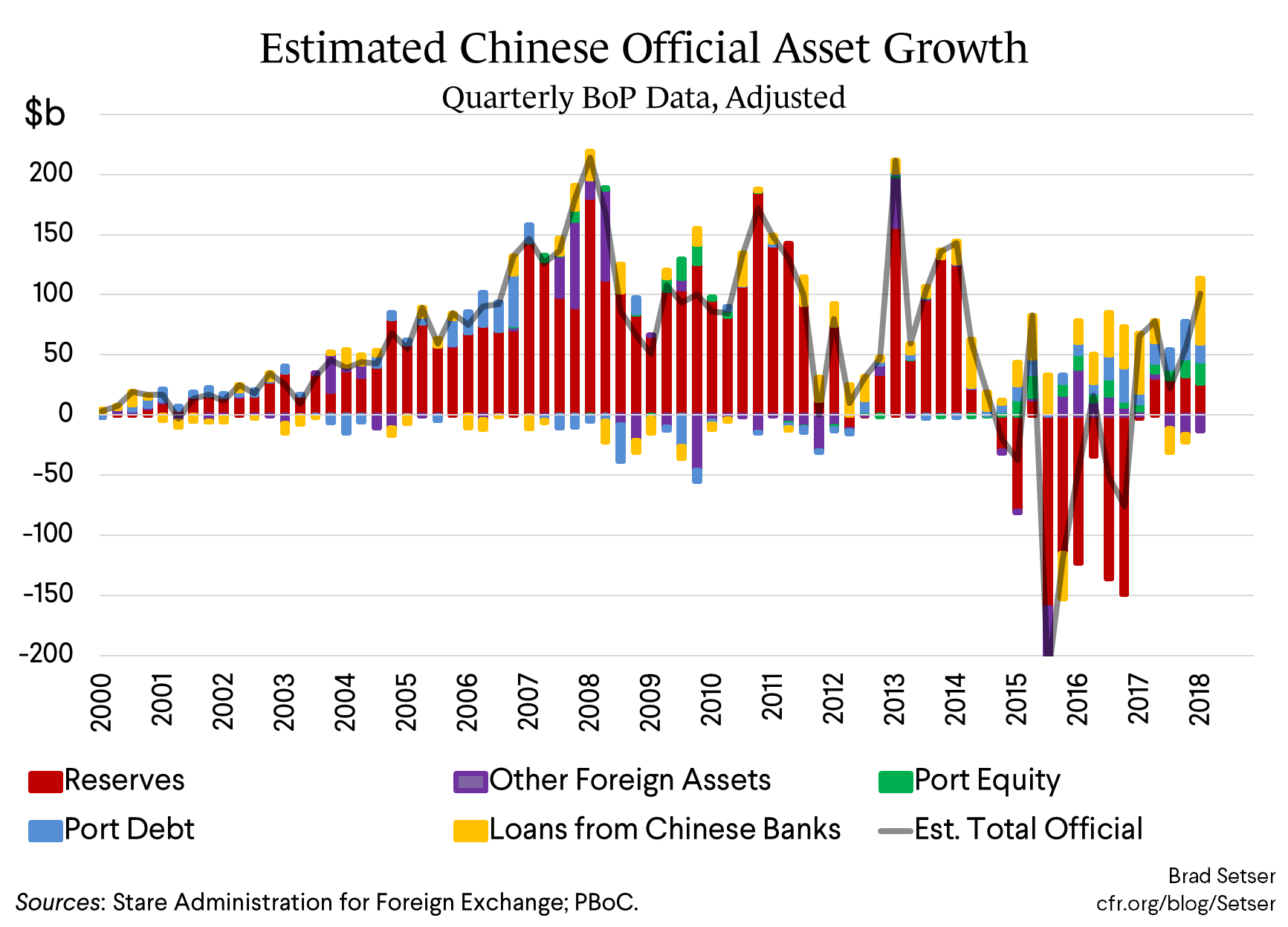

I watch several line items in the balance of payments closely to estimate the increase not just in China’s reserves, but in the broader set of assets held by China’s state: China’s shadow reserves.

And in the first quarter, by my count, China’s state added close to $100 billion to its foreign assets.*

There was a $25 billion or so increase in reserves.

The state banks increased their lending abroad by about $55 billion.

And Chinese financial institutions—mostly the state banks, but also some big state controlled equity investors (I suspect)—bought about $30 billion in foreign bonds and equity.

And the foreign exchange the state banks hold at the PBOC as part of their reserve requirement fell by between $10 and $15 billion.

The result—the fastest growth in my estimate of China’s official asset growth since early 2014—back when the dollar was still weak.

I watch the size of these flows because they correspond with the activities of a small number of big state institutions, institutions that in a pinch I believe China’s government could control.

The rise in offshore lending for example dates back to a decision made back in 2010 or 2011—lending started to rise rapidly from early 2012 on. And for reasons that I don’t yet understand fully, Chinese portfolio investment abroad—which had been flat from 2007 to 2014, picked up strongly in 2015. That too reflects a policy choice: the relevant institutions adding to their foreign books are clearly state controlled.

As a result China’s state holds significantly more assets abroad than show up in its reported reserves. About a trillion more. By my broad measure, China added about $300 billion to its foreign portfolio over the last 5 quarters.

Not all of these non-reserve assets are liquid to be sure. But some likely are (the bonds bought by the state banks in the last few years? A portion of the CIC’s equity portfolio?) and, in a pinch, China could certainly slow the pace of outflows to take a bit of pressure off the PBOC.

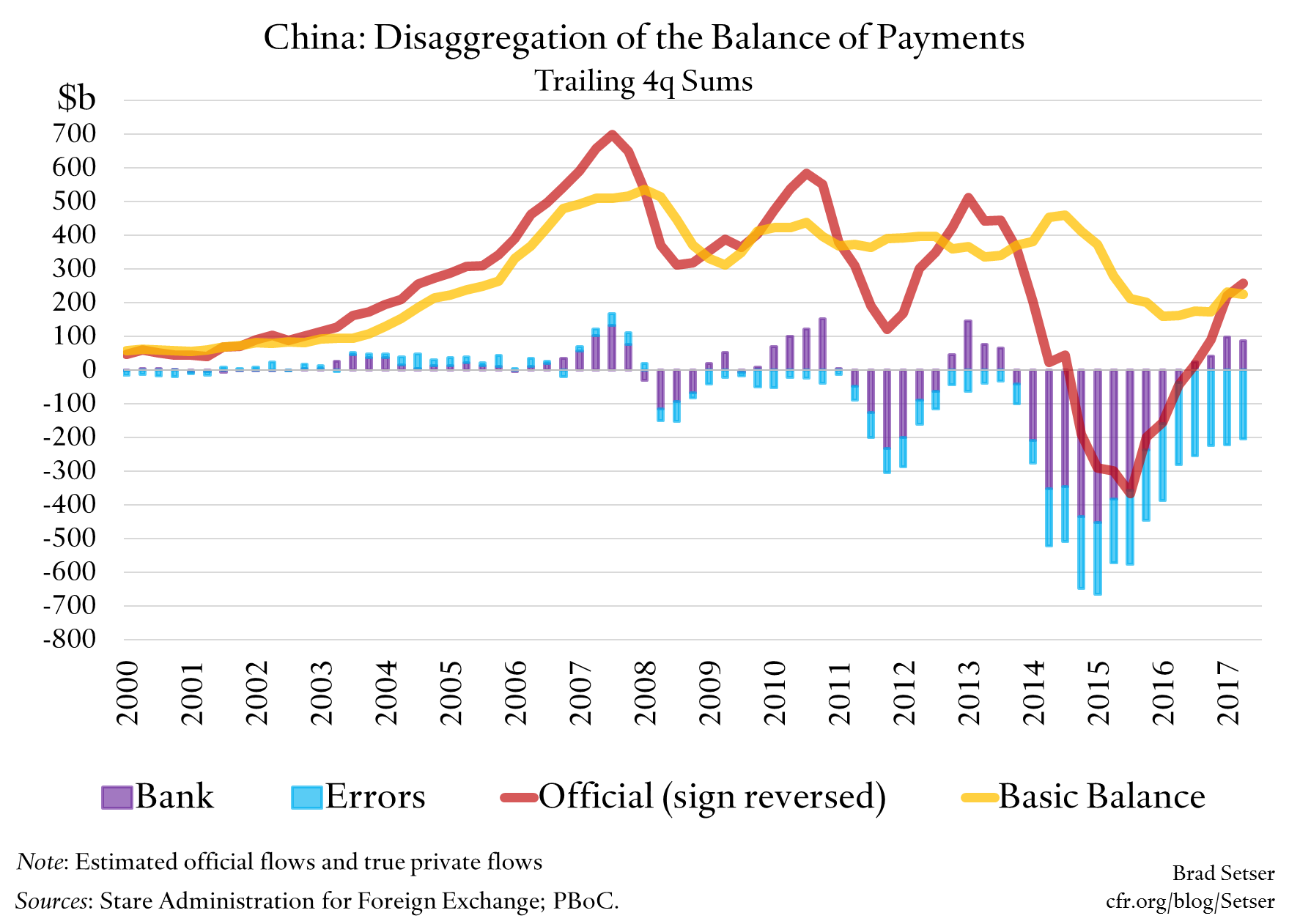

Tracking “true” official asset growth has another advantage—it lets me estimate true “private” flows in the financial account.

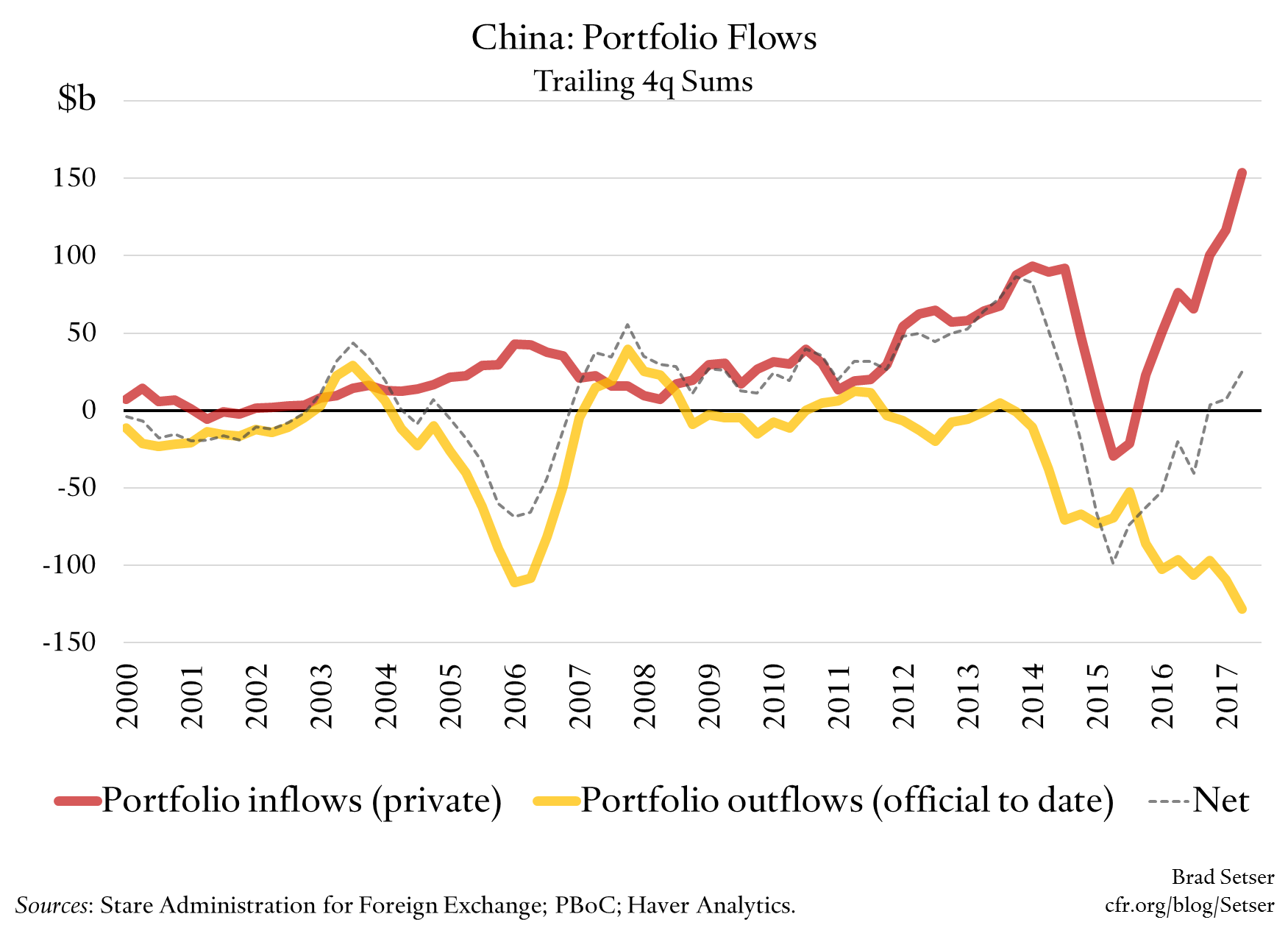

And those have turned around in the last four quarters of data. Consider the following chart, which packs a lot into its four lines.

First, note that the basic balance—the current account plus net FDI—has improved over the last few quarters. That is because the controls on FDI outflows had an impact, so FDI on net is flowing into China.

Second, note that official asset growth—with all of my adjustments to capture the “shadow” reserves hidden in the state banks and the CIC—tracked the basic balance until 2013, with the exception of the “peak euro crisis” quarters. And it is once again tracking the basic balance.

Third, “true” private inflows and outflows look pretty balanced right now. Note the swing in bank flows since 2015. This reflects the return of foreign lending to China’s banks over the past few quarters, after external “deleveraging” during the “Chinese yuan crisis” of 15/16.

Finally, note that errors and omissions—true “flight” capital—has stayed relatively high. The net bank inflows (adjusted for the state banks long-term lending abroad) aren’t enough to offset this outflow. To get balanced private inflows—as is implied by a pace of increase in state assets that exceeds the current account + net FDI inflows—there needs to be a flow that offsets the ongoing leakage of over $200 billion annually from errors.

And in fact there is.

Portfolio flows have come back to China, in a big way—with portfolio inflows over the last four quarters of data in excess of $150 billion, including over a $100 billion in purchases of Chinese bonds by foreign investors**…

Why does this matter?

Well, it helps highlight what might change if a trade war turned into a currency war…

Compared to 2015, there is a bit less short-term external lending that could run—cross border claims on China’s banks have crept up from a post-depreciation low of $600 billion to over $900 billion, but they remain below the pre-depreciation peak of $1.2 trillion or so.

And, well, I have always thought China could offset some outflows from the banks without dipping into its official foreign exchange reserves by slowing the pace of Chinese bank lending abroad if it really wanted too, for whatever set of reasons ...

But compared to 2015, there is more risk from portfolio investment—the new bond inflows— could stop, or even reverse. Again, China could offset this in part by slowing the pace of its own institutions’ purchase of portfolio assets abroad. Chinese state banks don’t need to keep adding to their foreign portfolio. By allowing those outflows to continue last time China effectively added to the draw on its reserves, as the state’s foreign holdings away from reserves and toward shadow reserves.

And finally there is the real leakage from “errors”—flows that cannot be accounted for, and thus cannot be controlled or managed. China can fund a portion of that leakage from its ongoing current account surplus (well over $100 billion even now in my view) and the interest income/other gains that led to over a $100 billion increase in reserve growth (according to the balance of payments, which shows more reserve growth than the PBOC’s CNY balance sheet) over the last year. And it could finance a temporary spike by dipping into its reserve stash—China still has far more than it needs.

But China would eventually lose its ability to control its currency if portfolio inflows dried up and errors structurally marched higher, and consistently topped the current account …

That to me is the risk China faces if it decides to make a weaker currency—through a controlled depreciation—a part of its response to Trump’s trade war. The hard part is weakening the currency by a bit without leading the market to expect a big depreciation. It is, in my judgement, doable given the state of China’s balance of payments—but that doesn’t mean it wouldn’t be risky. To China. A weaker currency helps China directly, but the net gain depends on avoiding a broader loss of confidence in a lot of implicit state guarantees that permeate China’s financial markets.

There of course is a much broader, more important risk too—namely that if China’s economy slows the PBOC won’t want to follow the Fed up and China will exit from its basket regime through a float down to gain full monetary independence. Fiscal policy divergences (tightening in China, loosening in the U.S. could drive monetary policy divergences that make a basket peg untenable). But that’s a topic for another post.

*/ My adjustment is simple and easy to replicate using the detailed financial account numbers. I add four lines from the balance of payments to reserves to estimate “official” assets, and thus remove them from the “private” side of the ledger. The most straightforward adjustment is adding in the line item that corresponds with the state banks‘ required foreign exchange reserves (other, other, assets), which aren’t consolidated into the PBOC’s reported reserves even though the funds appear to be held at the PBOC. The second is adding in the long-term loans reported in the balance of payments: this captures the activity of the CDB, China ExIm, and the big-four state commercial banks. Next, I add in all portfolio outflows. Purchases of portfolio debt (bonds) have historically come from the state banks. Back in 2005 these purchases were financed through swaps with the central bank. More recently they have been financed by spare domestic dollar deposits and foreign borrowing. Finally, I add in China’s purchases of portfolio equity, as historically this has largely come from the activity of the China Investment Corporation and a few other big state actors. I may slightly over-adjust, as I haven’t factored in China’s efforts at financial account liberalization significantly.

But I think the result provides a more accurate picture of underlying balance of payments pressures than looking at reserves alone. We know at times in the past China has shifted reserves over to other state institutions to lower its reported pace of reserve growth (that’s how the adjustments started), and that China’s reserves capture only a portion of the foreign assets of the Chinese state. And that over time, we know that over time there has been a shift toward foreign asset accumulation in the state banks. My quarterly estimates of the split are in the graph below.

**/ This excludes bonds issues in Hong Kong by the offshore subsidiaries of Chinese firms, which would register in Hong Kong’s balance of payments. However, if the funds raised by the Hong Kong subsidiary are then lent to the mainland that should register in the balance payments, probably as a loan (so in “other”).