The Global Cost of the Eurozone’s 2012 Fiscal Coordination Failure

The eurozone countries collectively did far too much fiscal adjustment in 2011, 2012, and 2013. Germany joined in the consolidation in 2012, hurting the eurozone—and the world.

The Banque de France has an interesting little article in its summer report. The Banque de France argues that the eurozone collectively did too much fiscal consolidation—e.g. austerity; budget cuts and tax increases—between 2011 and 2013.

And way too much fiscal consolidation in 2012:

“The consolidation observed between 2011 and 2013, based on the overall change in the primary structural balance of general government, is now estimated by the European Commission at almost 2.9% of potential GDP…the fiscal effort was 1.5 percentage points of GDP in 2012.”

Notably, the consolidation wasn’t just done by the “weak” countries thought to lack fiscal space (it isn’t clear if they really did, as “too much consolidation” lowers GDP and thus often doesn’t do much to help debt-to-GDP; see Auberbach and Gorodnichenko). The “strong countries” with obvious fiscal space, notably Germany, joined in:

“Efforts were extremely significant in 2012 and 2013 in Spain and Italy and noteworthy in Germany (one percentage point) and France (0.8 percentage point). Fiscal consolidation in 2012 probably triggered a downturn in demand at a time when the output gap was significant at -2.2%...“

In other words, the sum of national fiscal policies produced far too much overall fiscal tightening for the eurozone as a whole—much more tightening than the ECB could plausibly offset (and it is not clear the ECB did all that it could, as it couldn’t overcome the internal hurdles needed to start “QE” until 2014).

The Banque de France also identifies a plausible alternative scenario, one that would have avoided at least some of the excessive consolidation. It proposes, for 2012:

“a change in the structural balance of 0.8 percentage point in France, Italy and Spain as well as a modest fiscal expansion of 0.5 percentage point in Germany. These assumptions lead to a smaller aggregate consolidation in the four largest European countries by 1.1 percentage points of GDP.“

A slower pace of consolidation in France, Spain, and Italy and an offsetting fiscal expansion in Germany would have reduced the overall fiscal consolidation in 2012 from 1.5 percentage points of eurozone GDP to 0.4 percentage points of eurozone GDP, which translates into a much smaller drag on domestic demand.

And the Banque de France suggests a more modest consolidation in 2013—one limited to 0.2 percent of eurozone GDP—as well.

I personally think the Banque France’s alternative scenario is still too (fiscally) conservative. France could have delayed consolidation too, even if the Banque de France doesn’t want to so say so.*

But the key is that Germany consolidated when it clearly didn’t have to.

That consolidation pushed German output below potential and made the lives of its immediate neighbors more difficult.

And at a time when the rest of the eurozone was delivering a negative shock to world demand.

The FT‘s Martin Sandbu has noted—accurately—that Germany’s trade surplus with the world hasn’t changed much since about 2013. He further argues that a large but constant German surplus hasn’t been a drag on the rest of the world over this period. I wouldn’t go that far—an ongoing trade surplus means that other countries continually have to generate demand in excess of their output (and import more than they export) and that can be a bit of a challenge (or to be less diplomatic, it only tends to happen if other countries are running fiscal deficits or otherwise levering up, a constant deficit often implies a growing stock of debt). And, well, it would be nice if a fall in Germany’s surplus provided a positive shock to demand globally.

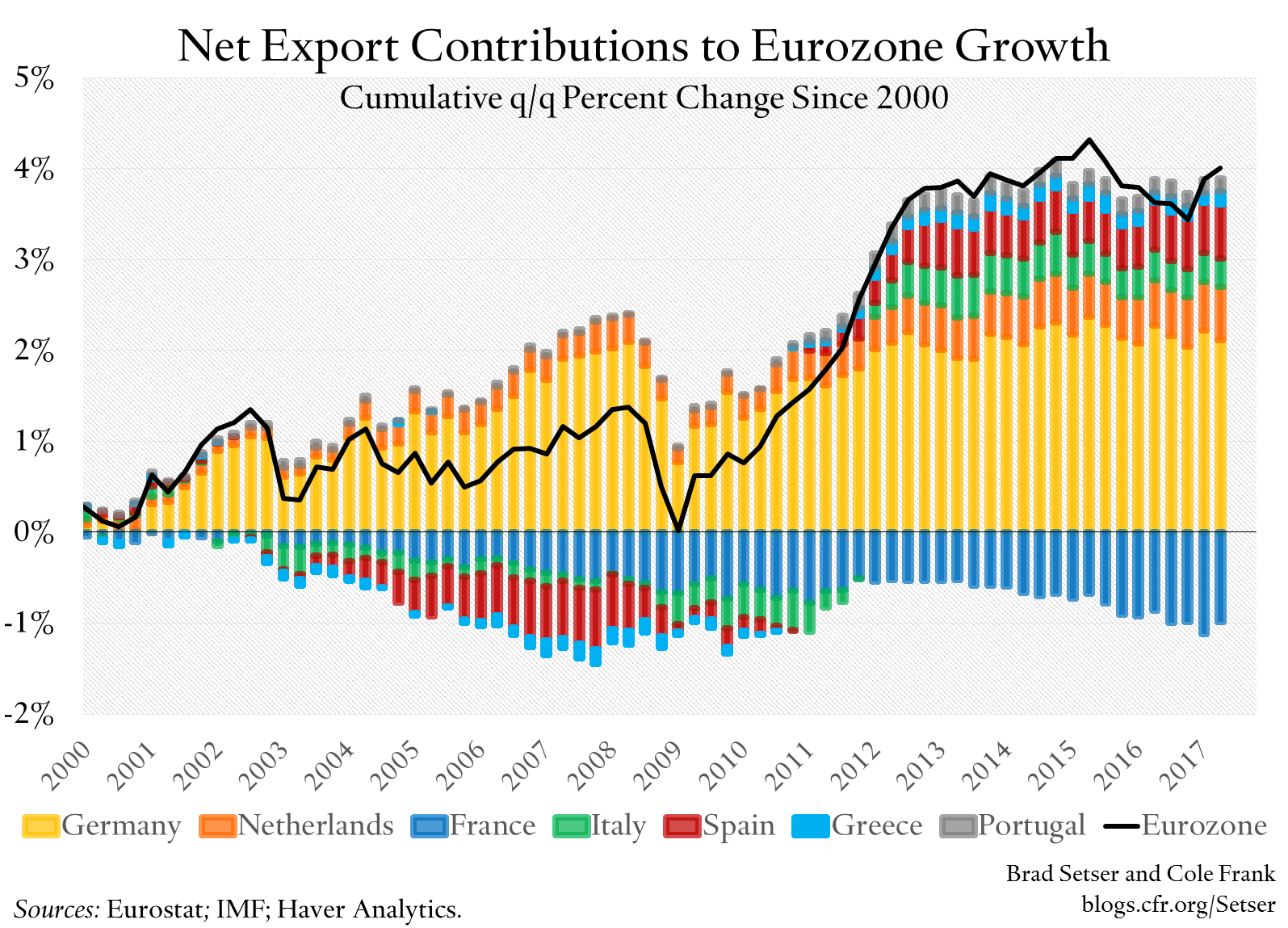

But the Sandbu defense (sounds like a chess move) doesn’t apply in 2012. Cole Frank and I disaggregated the contribution net exports made to overall eurozone growth by country—and Germany was drawing on net exports for growth then.

Mathematically, a contribution from net exports can come either from a fall in imports (the rest of the world shares the pain, so output falls by less than domestic demand) or a rise in exports. For most of the rest of the eurozone, the contribution from net exports came from a fall in imports. But for Germany, it was a rise in exports—as Germany offset the fall in internal eurozone demand by exporting more to the world.

In other words, an unneeded consolidation in Germany—and an excessive consolidation in the eurozone—didn’t just push the eurozone into a deeper recession, it also slowed the global economy. The rest of the world was demand constrained at the time—Germany’s rising surplus meant less growth elsewhere.

There is a second point here, one that is as relevant for today as for arguments about the past. For now, as Sandbu has emphasized, eurozone fiscal policy is the sum of the fiscal policies of its major member states. That could change, with a big eurozone budget and eurozone finance ministry that has real borrowing capacity. But odds are it won’t (see Martin Wolf, among others). So the key to getting eurozone fiscal policies right is coordinating different national fiscal policies—and making sure the sum of national fiscal policies makes sense for a region that shares a single monetary policy.

* I also think the multiplier the Banque de France applies to calculate the impact of its alternative scenario is probably too low—they used a multiplier of 1 to 1.2. The Obama Administration, in the 2009 American Recovery and Reinvestment Act, used a multiplier of 1.5, which seems about right. The Banque de France:

“Overall, a multiplier of 1 to 1.2 could be applied to a fiscal policy that targets public investment. Combined with a lesser consolidation effort...resulting from a more flexible coordinated fiscal stance as described above, the opportunity cost in terms of growth of deficiencies in fiscal policy coordination in the 2011-2013 period would amount to 0.8 and 1.9 percentage points of GDP.”