How Many Reserves Does a Country Like Argentina Need?

The IMF’s reserve metric tends to overstate the reserve needs of current account surplus countries with little external debt, and understates the reserve needs of current account deficit countries with lots of external debt.

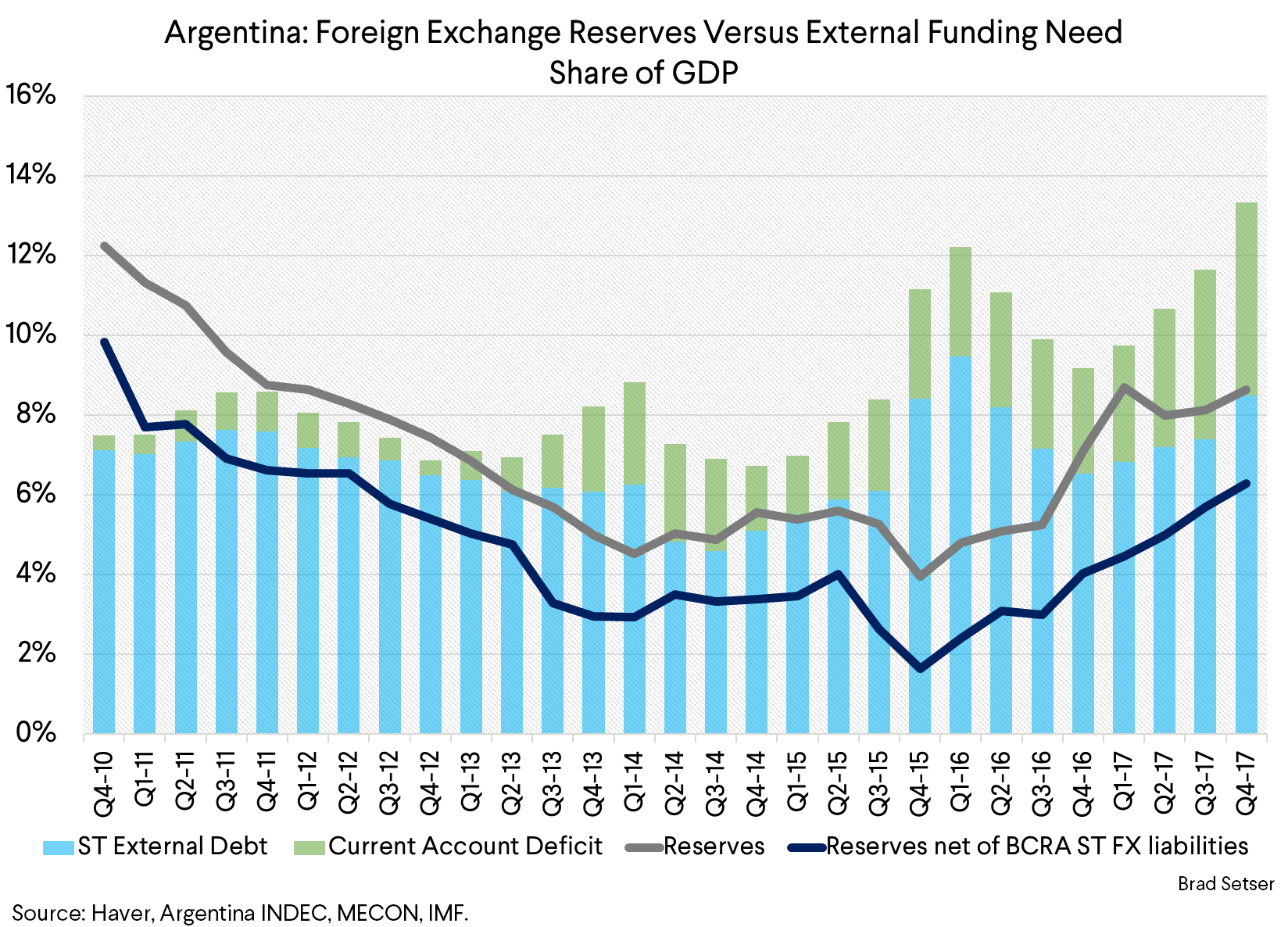

Argentina now has around $50 billion in foreign exchange reserves. A bit less if you net out reserves borrowed from the domestic banking system and other identified short-term drains (last data point is end-March).*

Is that enough?

The answer, I think, hinges on whether foreign exchange reserves should be assessed relative to the size of a country’s domestic banking system, or relative to the size of a country’s external debt and its external funding need.

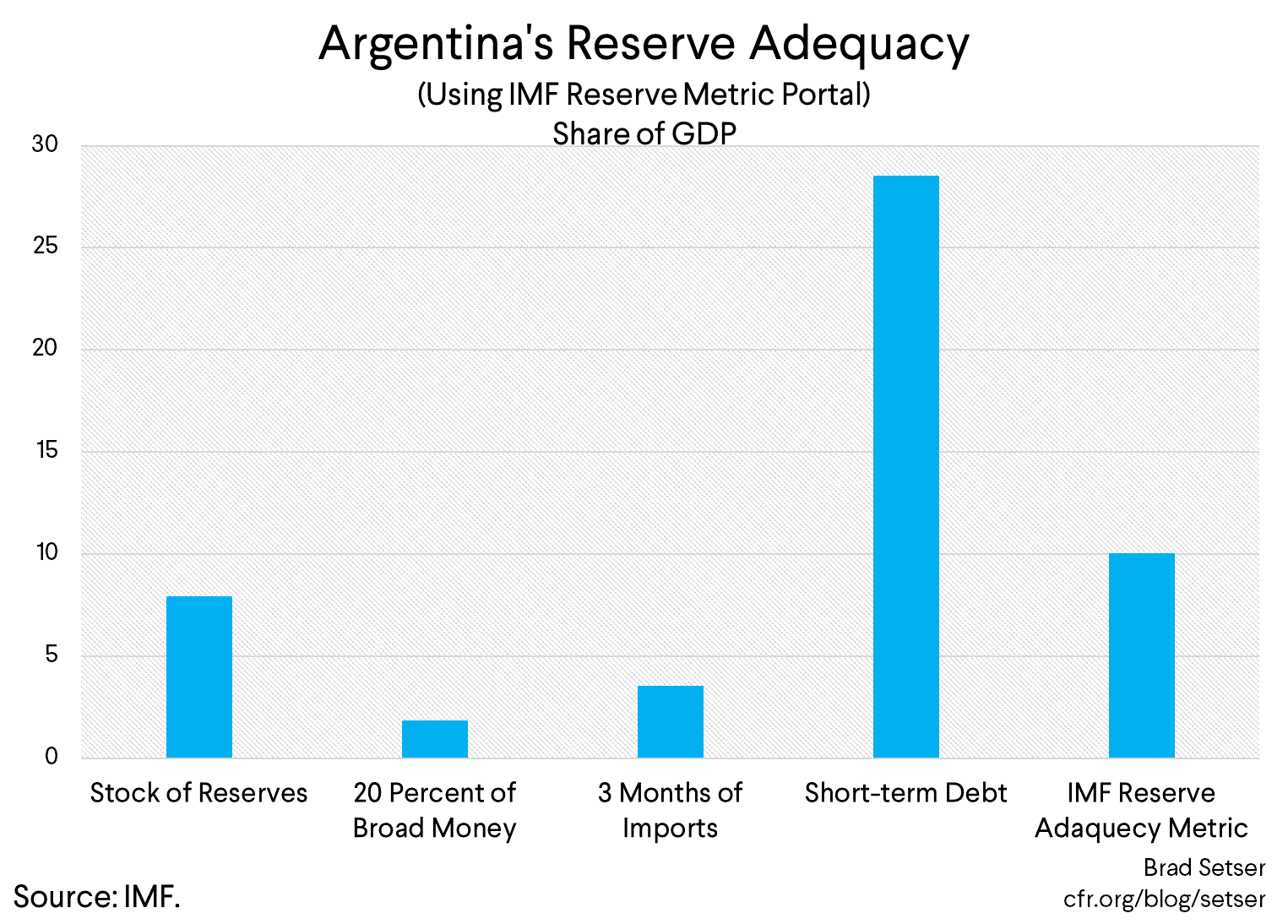

Argentina has a fairly small banking system. Deposits in all currencies are something like 25 percent of GDP. China it is not. So covering 20 percent of M2 doesn’t take much money. Argentina could get by with less than 5 percent of GDP in reserves. 2 percent of GDP to be exact.

But Argentina also has a sizeable current account deficit and a significant—and rapidly growing—stock of external debt. To cover its external funding need (short-term external debt plus the current account deficit) Argentina would need around $80 billion in reserves, or over 12 percent of pre-devaluation GDP.

Argentina is consequently a case (like China) where different measures of reserve adequacy generate wildly different estimates of reserve need. In other words, the choice of indicator matters.

And to be blunt, I don’t think the IMF’s indicator gets it right.

The IMF in December put Argentina’s reserves at 115 percent of its “need” (see paragraph 17 of the staff report)—leading the Wall Street Journal to suggest that Argentina’s recent troubles show the limits of the protection that reserves provide.

I disagree with the Journal.

Argentina got into trouble in part because it was not holding enough reserves, and thus lacked the kind of buffer available in countries like Russia and Brazil. With a current account deficit of close to 5 percent of GDP, reserves of around 8 percent of GDP simply aren’t enough (8 percent is absolutely low for a major emerging economy, and some of those reserve were some borrowed from the domestic banks and others were borrowed from China through a swap agreement).

The IMF’s measure is the combination of four indicators: imports, domestic base money (M2), short-term external debt, and all external liabilities (net of short-term external debt to avoid double counting). This more complicated metric means that the IMF can judge Argentina reserves to be adequate even if reserves don’t cover all maturing short-term external debt. That said, I am not sure quite where the short-term debt number in the reserve metric portal come from.** It does seem a bit high—but other measures put maturing debt at $50 billion or more.

Why does Argentina end up with a fairly modest reserve need in the IMF’s metric despite the high level of short-term debt?

First, Argentina’s banking system is relatively small.

And second, its economy isn’t very “open” (exports and imports aren’t that large relative to GDP).

Those two variables combine to pull down the amount of reserves that Argentina needs to hold to meet the IMF’s composite reserve metric.

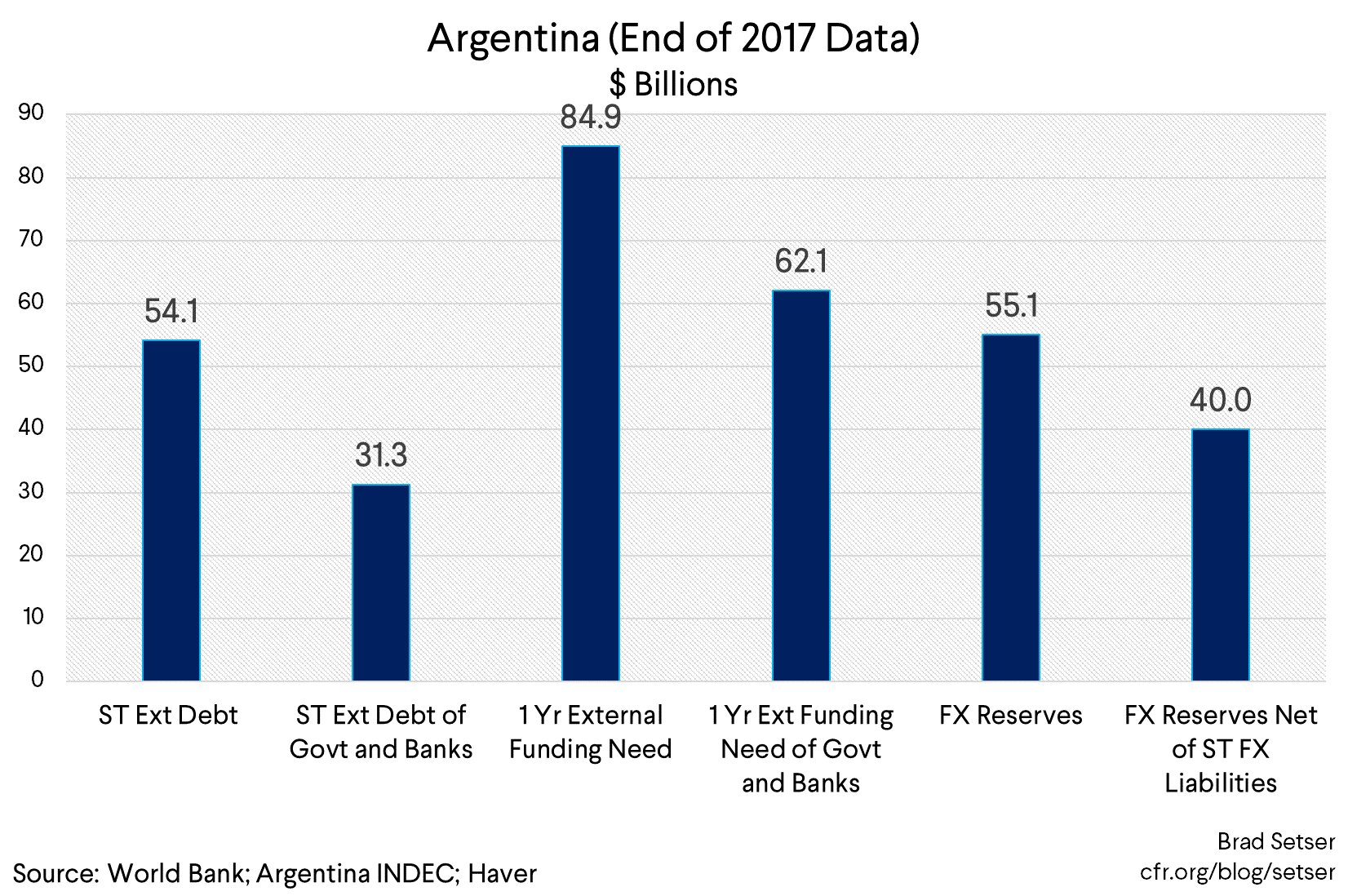

As a result, the composite measure ends up blurring what otherwise would be a clear signal from reserves to short-term debt or reserves relative to the Argentina’s external funding need.The following chart shows various measures of short-term debt (based on the Argentine debt data, not the number in the IMF reserve template data set)**** and different measures of foreign currency reserves at the end of 2017. $55 billion wasn’t enough.

One note: to the extent the short-term drains on reserves reported in Argentina’s detailed reserve disclosure come from domestic foreign currency deposits, the domestic banks have placed at the central bank, there is no double counting with the external debt data.

In fact, I think the problems with the IMF’s metric go well beyond its application to the particular case of Argentina.

Turkey also emerges relatively favorably from the IMF’s metric. It too needs to hold fewer reserves under the IMF’s metric than it would if it adopted the old rule of having at least full coverage of short-term external debt (let alone full coverage of short-term external debt and one year’s current account deficit).

Conversely, the IMF metric has at times been interpreted as signaling that China—which has a massive domestic banking system but far more reserves than external debt, let alone short-term external debt—is short on reserves.

There is an underlying economic reason for the metric’s sometimes strange results.

Most countries with a large domestic banking system (think China, Taiwan, Korea, Malaysia, Thailand) and a high M2 to GDP ratio tend to run current account surpluses, while countries with a small domestic banking system with a limited domestic deposit base often run a current account deficit (as either the banks or the government need to raise funds abroad).

The net result is that the IMF’s composite metric tends to push up the assessed reserve need in countries with external surpluses, and tends to push down the assessed reserve need of countries with external deficits. It consequently doesn’t always flash red when it should, and sometimes flashes red when it should not.*****

No matter. Argentina managed to get itself into a bit of a pickle.

Its problems go well beyond the reserve metric, and the fact that a certain portion of Argentina’s reserves are borrowed.

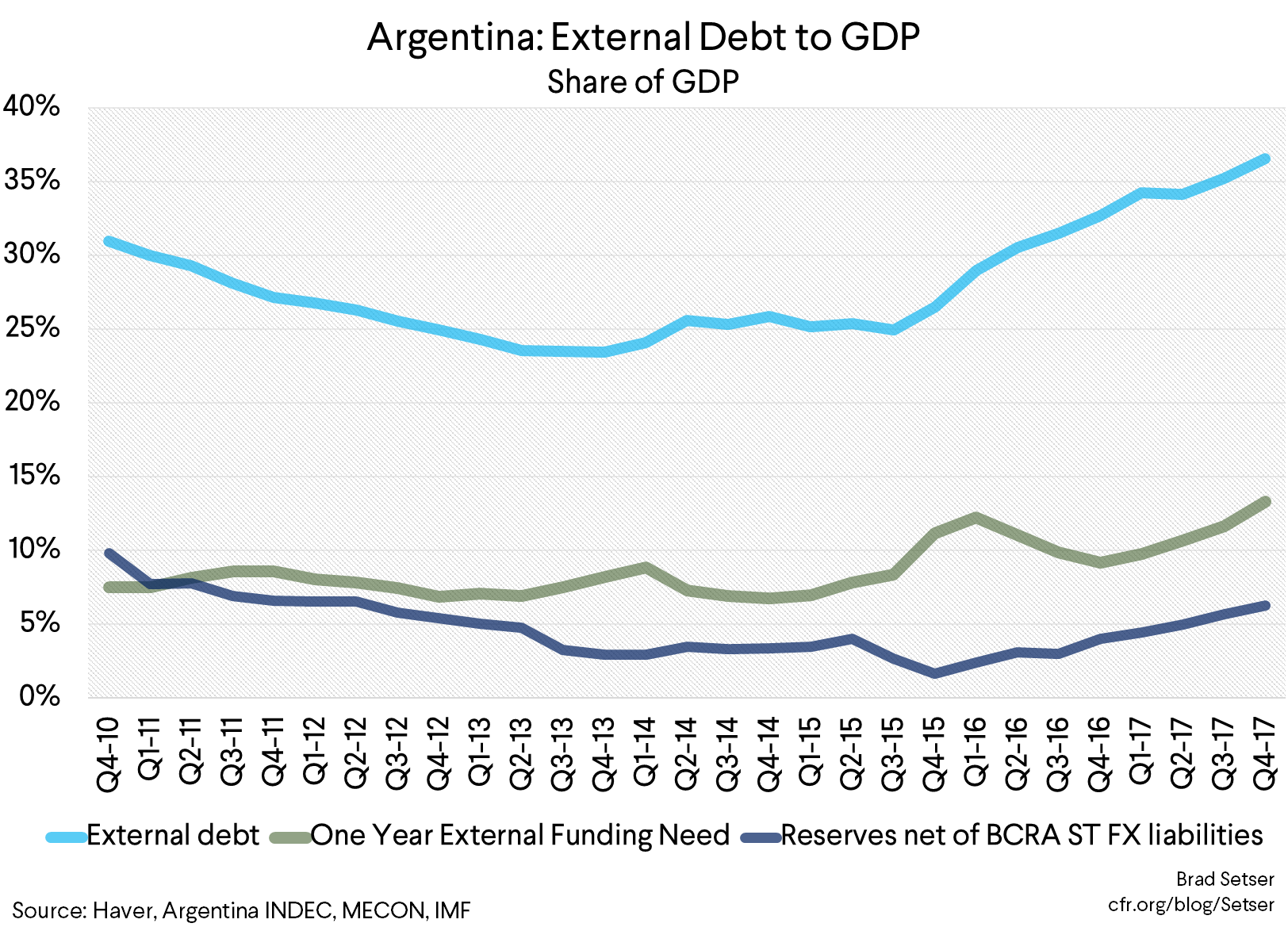

Argentina has more or less doubled its stock of hard currency bonds in two years (gulp) —and it isn’t clear, even with a bit of help from Franklin Templeton, that it can continue to fund ongoing fiscal deficits essentially by place large quantities of bonds abroad. While the bulk of the finance ministry’s dollar-denominated bonds are long-term, the Treasury also has been issuing short-term dollar denominated paper that it needs to roll (many of these “letes” are held domestically). The central bank also has issued a lot of short-term peso paper—and a portion of that paper now is held by flighty non-residents rather than captive domestic financial institutions. This week’s auction went relatively well, but the ongoing rollover need creates the potential for a run by non-residents that would quickly turn into pressure on the central bank’s non-borrowed reserves. Remember, the central bank sold reserves to stabilize the peso prior to Tuesday’s auction.

And, finally, external debt to exports—a rather old fashioned indicator I know, but I put more weight on old school balance of payments based measures of debt and reserves than most—is reaching levels that start to give me pause.******

* See Section 2 of the IMF SDDS reserve template for the disclosed short-term foreign currency liabilities of the central bank. There is also a fair amount of data on the general government’s foreign currency funding need.

** Since short-term debt is combined with other indicators in the IMF’s metric, it has a weight of less than 100, 30 percent to be exact. That implies that if a country borrows $10 billion in one-year money from the rest of the world, only $3 billion needs to be set aside in reserves—the other $7 billion can be used to fund a current account deficit. That balance seems off to me if the country is largely borrowing in a foreign currency. Hat tip to the General Theorist.

*** I cannot figure out how the Fund estimated Argentina’s short-term external debt to be close to $180 billion in the reserve metric data set. That seems far too high (it implies a majority of Argentina’s external debt is short-term, which I don’t think is the case). Table 7 of Article IV puts short-term external debt at $66 billion, which seems more reasonable.

**** Argentina’s external debt data shows around $55 billion of short-external debt (original maturity basis I think) at the end of 2017, and around $30 billion of that is the short-term debt of the government, the central bank, and the banks. The number on a residual maturity basis should be higher, but I haven’t found a number I trust (and I also wanted a time series). I should also note that a portion of the central bank’s external debt is denominated in pesos not dollars or another reserve currency, and a portion of the government’s domestic debt is denominated in dollars (it has a decent amount of short-term dollar debt that it needs to roll). Foreign currency debt and debt owed to non-residents are different concepts.

***** To be fair, the IMF’s staff assessment for Argentina makes it clear that the Fund thinks Argentina should build up its reserves—it highlighted that Argentina’s reserves to GDP ratio was low versus its peers. And the IMF also indicated in its assessment of China that China’s controls reduce its reserve need. However, the “metric” still matters as it is the default used for cross-country comparison. It just doesn’t seem to be working particularly well in what I think are the most important cases…

****** The IMF external debt forecast has gross external debt rising to about $400 billion/50 percent of GDP (table 7) by 2022—while exports of goods and services rise from under $75 billion to over $100 billion. I doubt though that Argentina’s nominal GDP will be around $800 billion in 2022 (nominal GDP in 2017 was inflated by an overvalued exchange rate). Even if Argentina adjusts a bit more quickly, gross external debt will rise above $300 billion—which is high relative to current exports in my book. See p.48 of the IMF staff report for the effect of a large real depreciation. It isn’t pretty.