Ireland Exports its Leprechaun

Irish tax distortions have a material impact on aggregate eurozone economic data.

The Irish leprechaun, of course, is Paul Krugman’s term for the 20 percent jump in Ireland’s GDP back in 2015. The leprechaun is almost certainly an apple (in bureaucratic terms, a large contract manufacturer).

For a long time, Apple International was, famously, neither a tax resident of the United States nor a tax resident of Ireland, and thus was able to defer payment of tax on almost all of its international profits. And in 2015, according to the New York Times, it seems to have become an Irish company, after a brief stopover in Jersey (the channel island that is, not the U.S. state)

To be sure, Apple is simply the biggest and most famous example. Other technology companies have an Irish presence, as do, I hear, a number of pharmaceutical and aircraft leasing companies.

Ireland’s GDP numbers haven’t been the same since.

And it increasingly seems that the distortions created by Ireland aren’t limited to the Irish data.

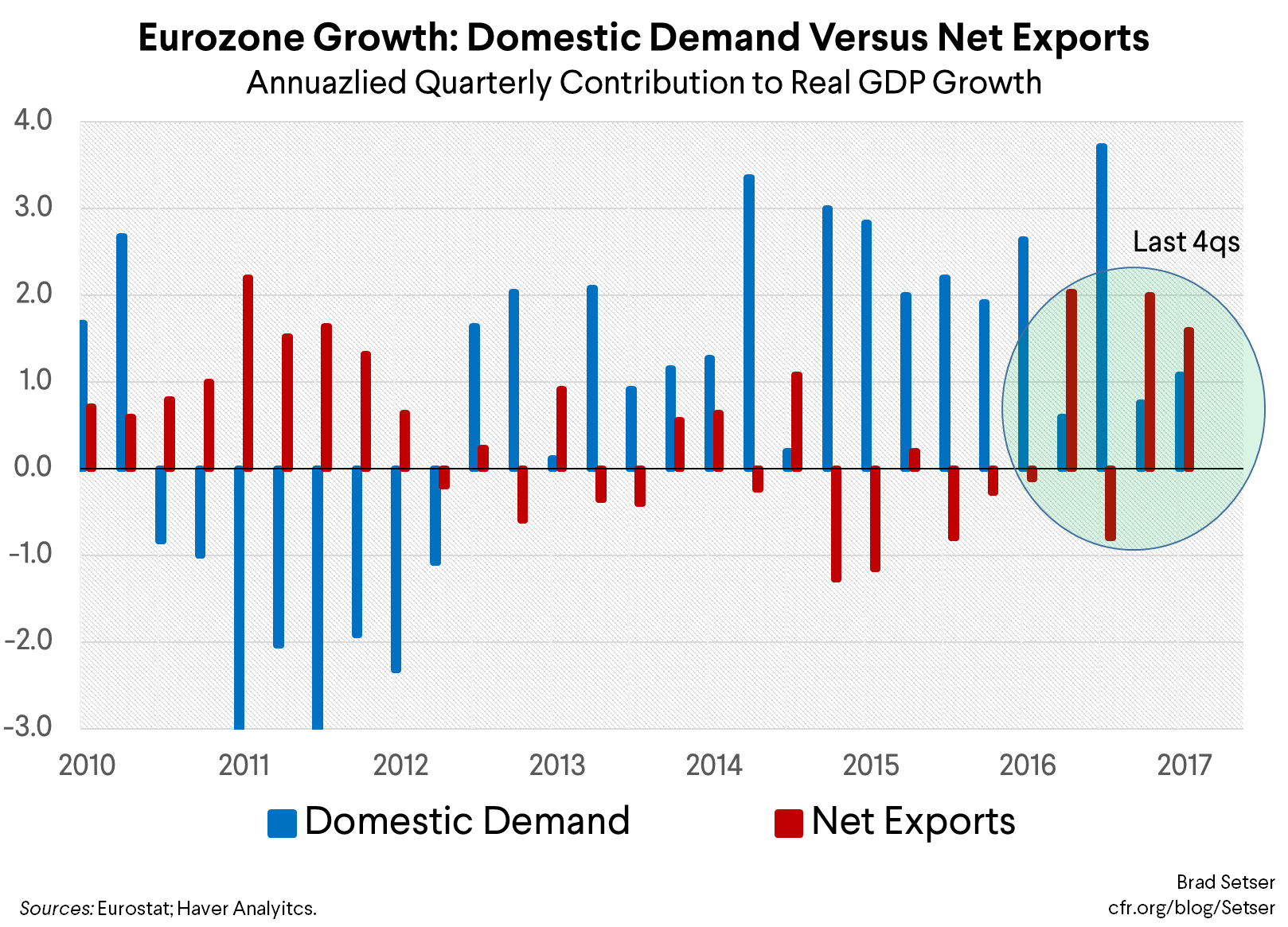

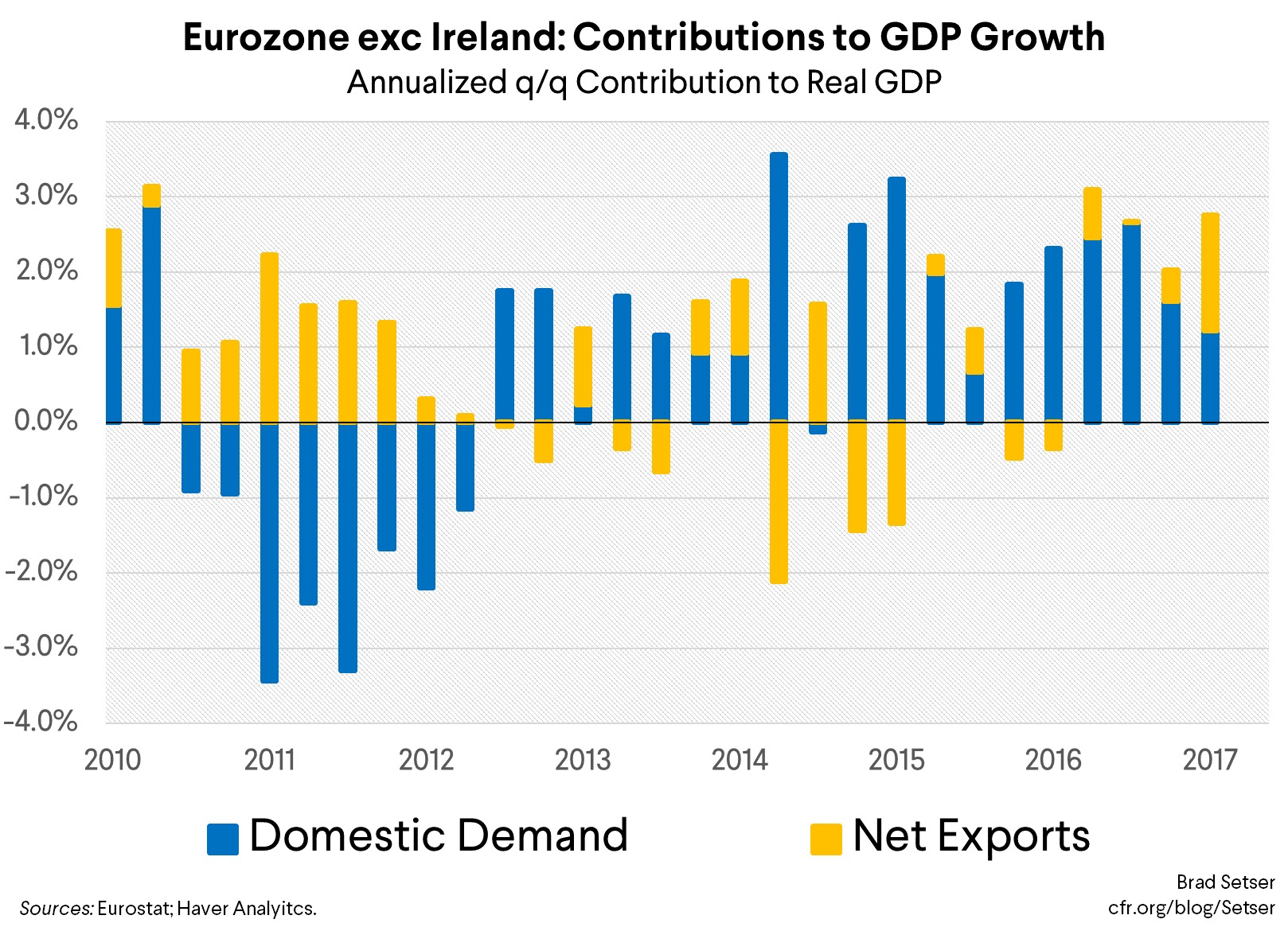

The eurozone’s aggregate GDP data doesn’t attract the same attention as the U.S. data—most focus on the underlying national data, which comes out earlier.

But, well, the aggregate data is interesting. I use it to help track the eurozone’s impact on the rest of the global economy, and specifically, to assess whether or not the eurozone has grown through domestic demand or net exports.

If you take the official numbers at face value, the eurozone has become increasingly reliant on net exports over the last year. The contribution of net exports topped the contribution of domestic demand in three quarters in 2017 (q2 is a major exception). And net exports contributed over a percentage point to eurozone growth.

That’s big.

During the eurozone crisis the peak contribution of net exports to European growth was about 1.6 percentage points (over four quarters) —largely because a sharp contraction in demand led to a sharp contraction in imports in the periphery which (somehow) had no impact on Germany’s current account surplus (there was no German leprechaun though: Germany offset reduced exports to its European partners with more exports to the rest of the world).*

But it seems like the Eurozone net exports number was touched by a leprechaun over the course of 2017.

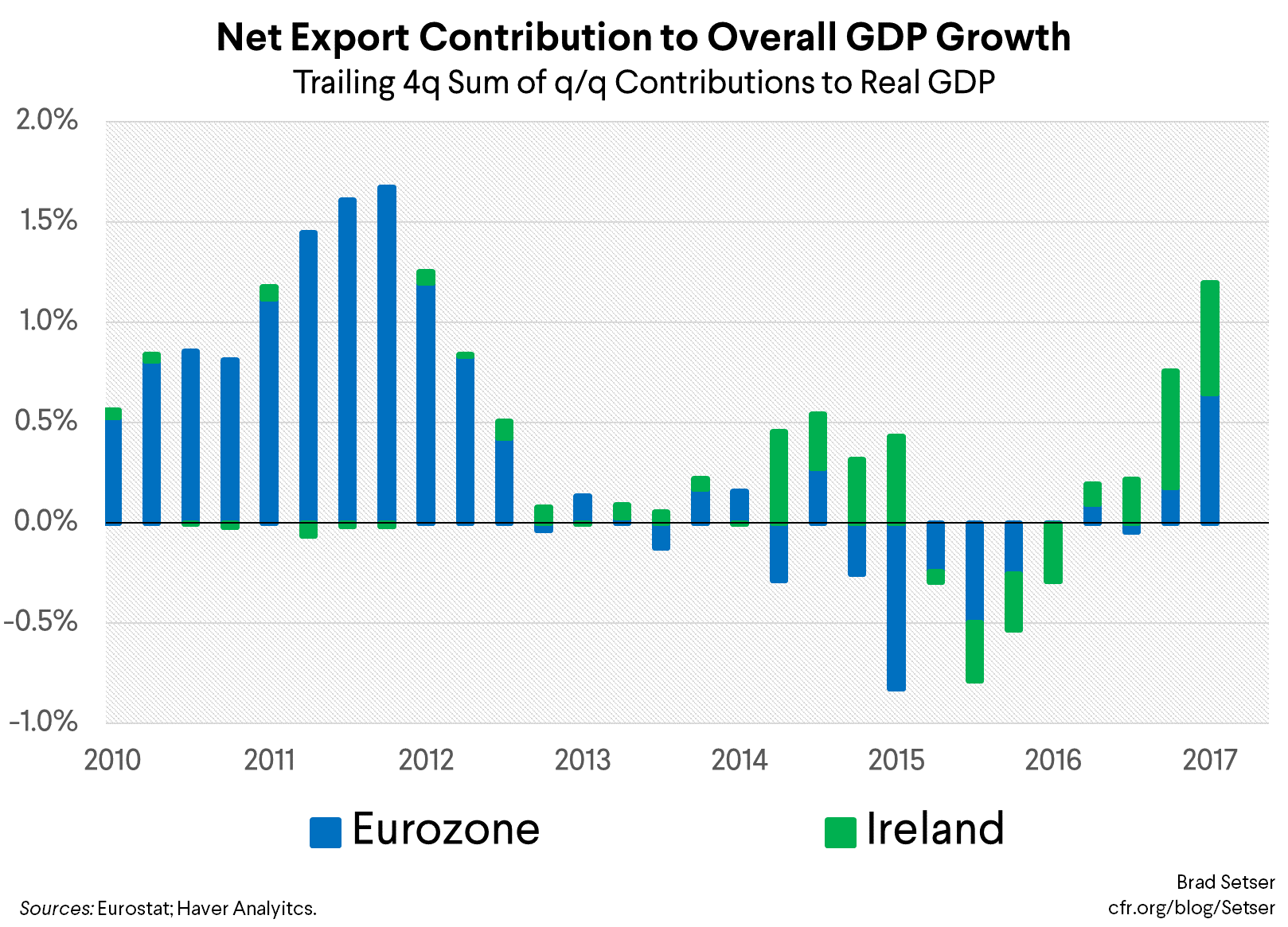

Ireland alone seems to account for about half of the 1.2 percentage point contribution of net exports to eurozone growth.

Irish net exports look to have added over a half point to eurozone growth. But Irish domestic demand (in the measured numbers) seems to have subtracted just under a half point from the overall growth rate (never mind all the on-the-ground signs of a boom). Depreciation of capital assets moved to Ireland or some such.

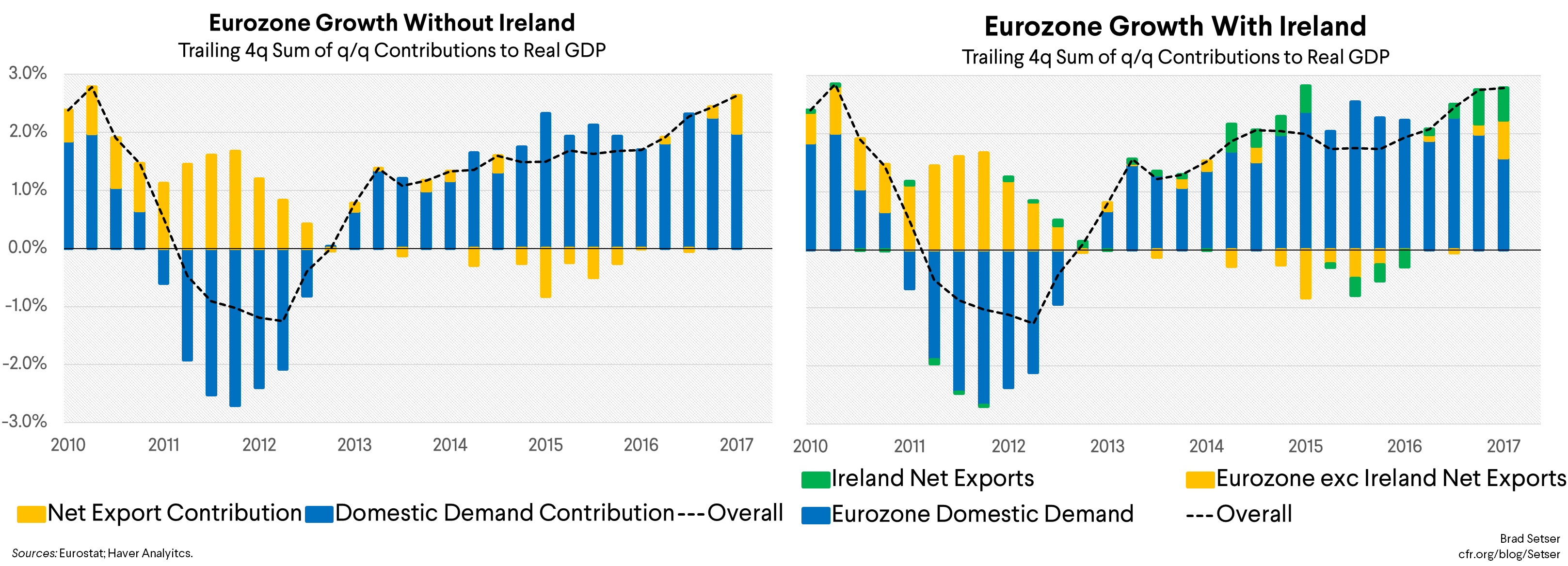

So if you net out Ireland, overall eurozone growth doesn’t change much. But the composition of growth does shift significantly. Rather than contributing 1.2 percentage points to growth, net exports “only” contributes 0.6 percentage points.

But that’s still a lot. The eurozone as a whole has grown more dependent on external demand. Germany too.

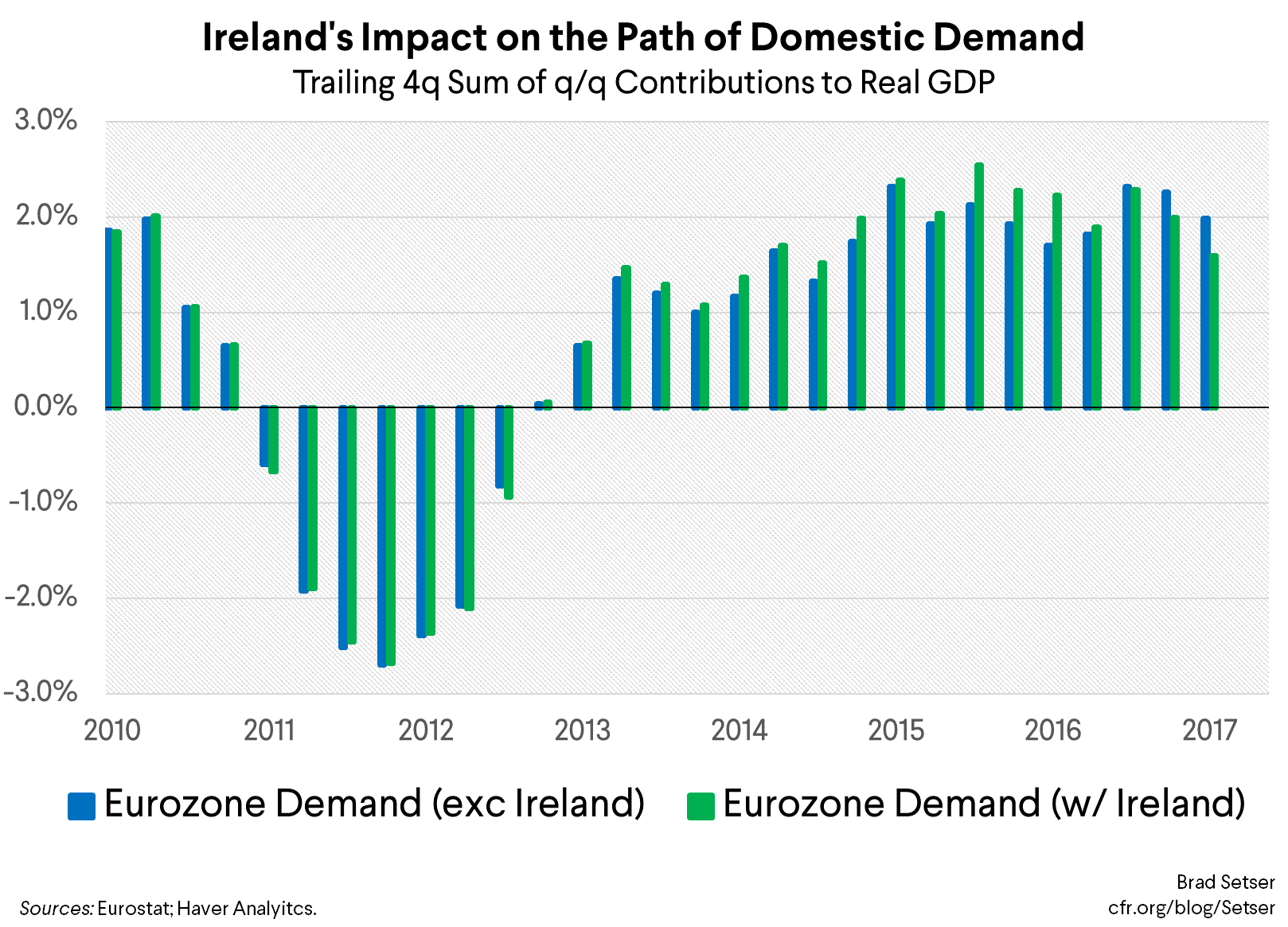

And eurozone policy makers shouldn’t take too much comfort from the fact that some of the deceleration in domestic demand growth in the overall European data seems to come from an Ireland-specific distortion: even if Ireland is taken out of the equation, European demand growth looks to have decelerated in q3 and q4 of 2017.

There isn’t a decomposition yet for q1 2018. But if I had to guess, the story will turn out to be simple. Demand growth remained modest for a region that still has a decent amount of slack, and net exports contributed a bit less.

And that makes the German decision to maintain an outsized fiscal surplus ** and the French decision to try to be German all the more mystifying. U.S. fiscal policy is too loose. But European fiscal policy is already too tight (given that the ECB is at the zero bound), and seems likely to get tighter (French and Spanish tightening will I think overwhelm any swing in Italy). Europe, and Germany, could do the world a favor by being a tad less fiscally virtuous, and importing a bit more…

Set the fiscal debate aside for a moment though. It is stunning that an economy as small as Ireland—it accounts for 2-3 percent of total Eurozone GDP—could end up having a material impact on the overall European data. The distortions created by tax-related leprechauns have gotten a tad too big for their own good.***

Many in Ireland know this. Ireland has, more or less, stopped using GDP to measure its own economy. And on current trends, the eurozone taken as a whole may need to consider something similar.

Note: I want to recognize the help of Matt Turner of Macquarie Group. He suggested that I look more closely at Ireland. I didn’t need all that much encouragement.

*/ The U.S. also got a contribution of around a percentage point to growth back in 2007, when domestic demand growth was sluggish, the dollar was weak and higher commodity prices juiced investment in oil and mining (capital equipment for the oil and mining sectors is a US specialty).

**/ the IMF puts Germany’s cyclically adjusted fiscal surplus at around 1 percent of its GDP. I am not sure though that I trust the cyclical adjustment. The actual surplus—general government surplus that is—is closer to 1.5 percent of Germany’s GDP. And there is no evidence it is poised to fall. In fact, the IMF now expects it to rise to 1.75 percentage points of Germany GDP. And tax revenues if anything seem likely to over-perform. The U.S., alas, isn’t likely to have that problem. The opposite, I fear, is more likely.

***/ A hint: a bold, rising economist with a bent toward disruption could take a close look at the geographic distribution of U.S. trade in services. My guess is that there are lots of leprechauns to be found. For a surprising number of major service sectors (setting tourism aside), the biggest single market for U.S. services exports is Ireland.