Leprechaun Adjusted Euro Area GDP…

The entire euro area’s economic statistics now need to be adjusted to remove the distortions created by the tax transactions of large multinationals operating in Ireland and the Netherlands. Headline GDP numbers aren’t too distorted, but the main components of GDP—net exports and domestic demand—have been contaminated by tax driven transactions that don’t reflect real economic activity.

It is by now generally recognized—not the least by the Irish themselves—that Ireland’s GDP data tells you more about Apple (and soon, perhaps Microsoft) than the actual Irish economy. I guess it is reassuring that being the tax home away from home of two of the world’s largest companies does have a measurable impact on Ireland’s economic data, and that tax related transactions don’t just disappear (as they often do in the Bermuda tax triangle).

Yet Apple, Microsoft and others mainly use Ireland as a tax hub—not as a real hub. Sure, they leave some crumbs behind (not the least tax payments to the Irish Treasury) but it would be a stretch to call the iPhone and Windows Irish exports. And when “Ireland” invests billions in a quarter to acquire the intellectual property of a non-resident company (think Apple Ireland buying Apple Jersey, or Microsoft Ireland buying Microsoft Singapore) nothing real is happening.

And to be sure this happens on a smaller scale too—it just isn’t as visible. Apple and Microsoft are now to the euro area data what China used to be to the U.S. international capital flow data—too big to hide, even in anonymous data.

Paul Krugman famously called the 26% surge in Ireland’s GDP back in 2015 “leprechaun” economics. That surge by the way has been revised up, not down, with time.

But the leprechaun is now so big that it isn’t just impacting Ireland’s own data. It has a profound and obvious impact on the euro area’s aggregate data. The OECD’s base erosion and profit shifting reforms have to date proved to be a boon to Ireland, as previously stateless income has had to find a tax home—and that is having a noticeable impact on the euro area data too.

The headline euro area GDP series is fine, more or less—

But the main components of euro area GDP? Not so much.

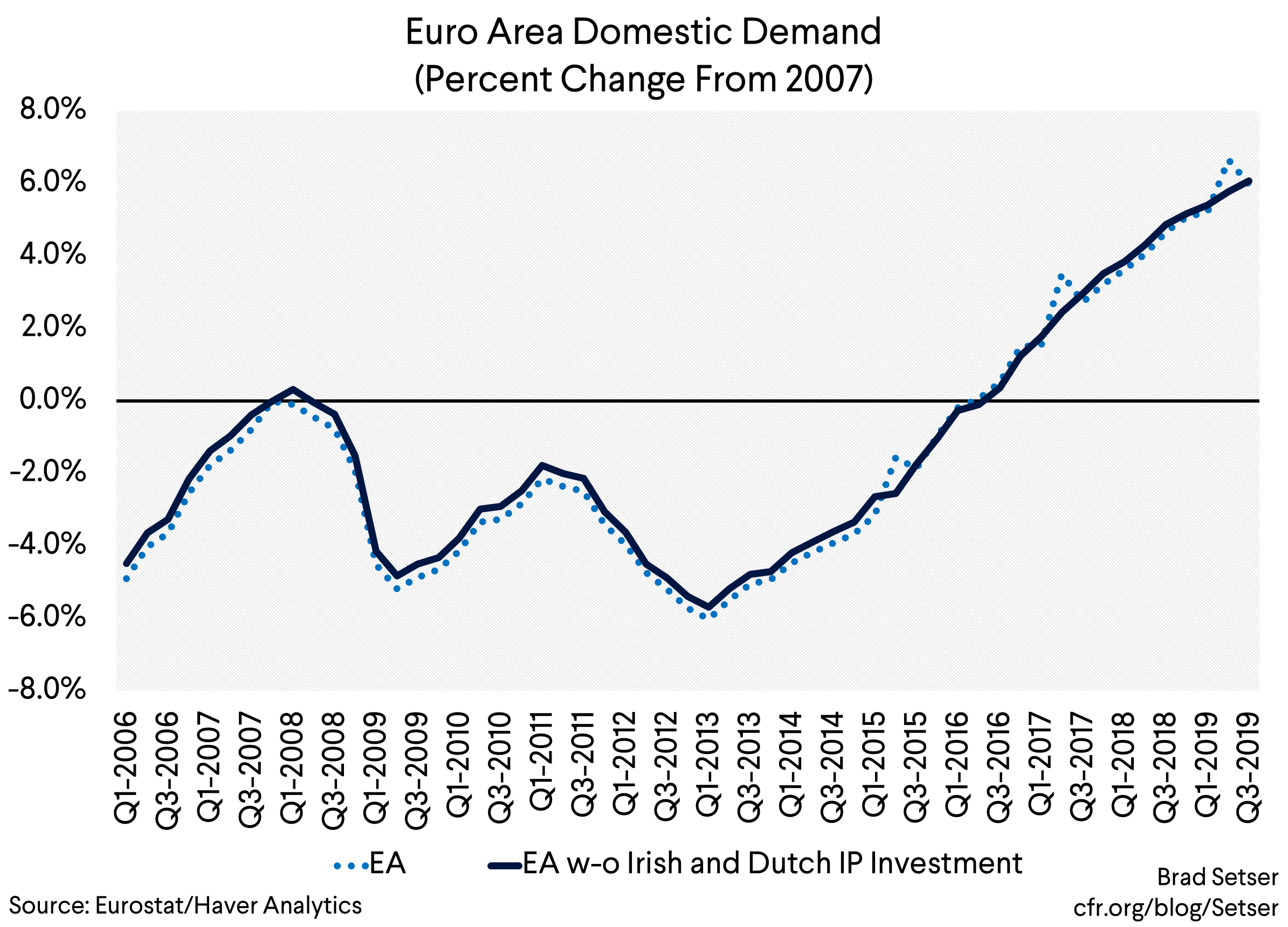

Domestic demand is the sum of consumption, investment, and government spending. It usually moves in line with GDP. But in the euro area, there are a set of obvious spikes—one in 2015, one in 2017, and another in 2019.

Those spikes can be traced back through the GDP data—and they all stem from big rises in investment in intellectual property, and corresponding rises in “service” imports. As a result, they have a far bigger impact on the composition of euro area growth than on the overall headline growth rate.

By now the impact of tax related transactions on Ireland’s GDP isn’t a secret (nothing like a Krugman tweet…) so the usual adjustment is to just net out Ireland’s GDP (and its subcomponents) from the euro area aggregate.

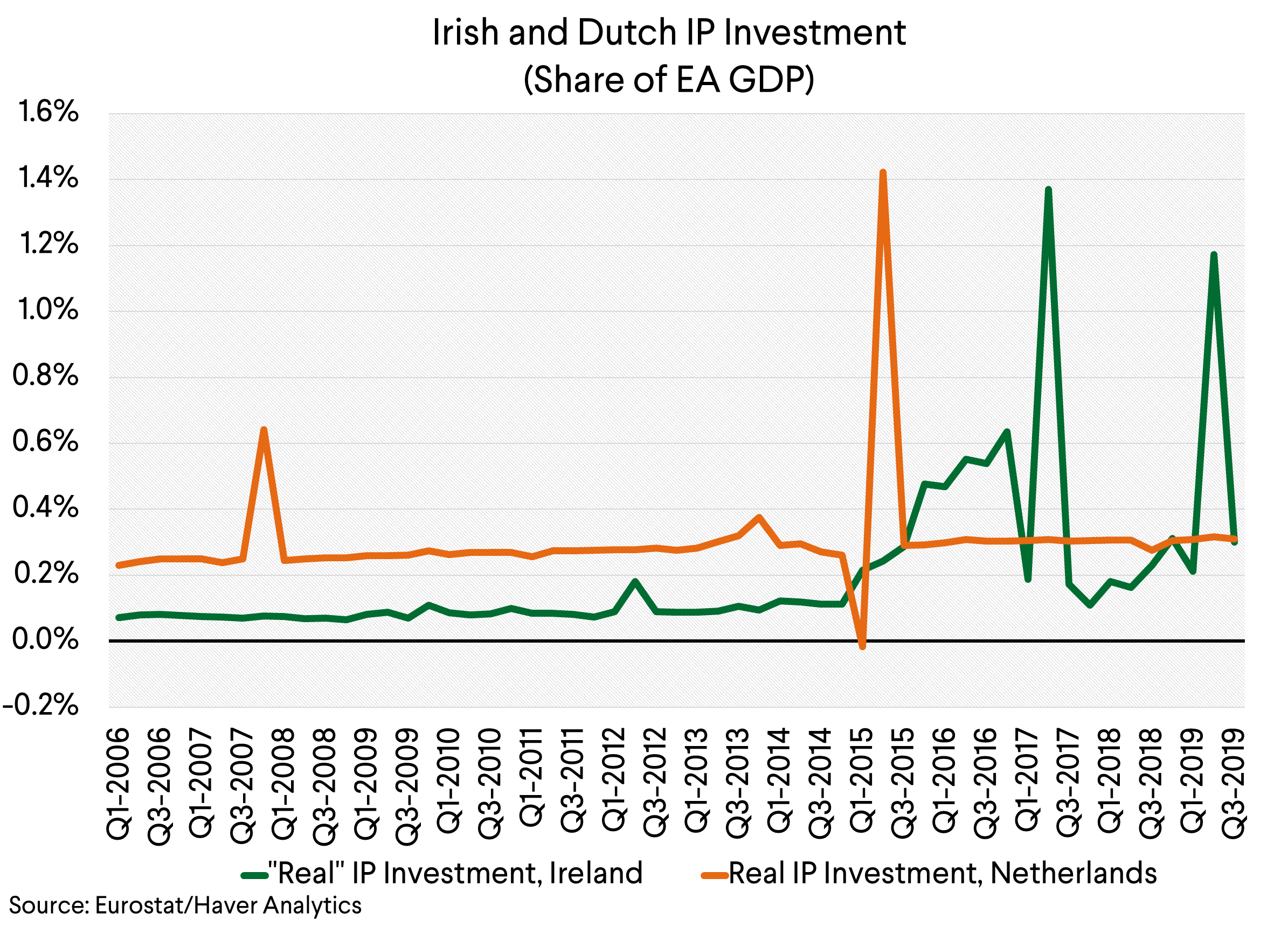

That though is a bit unfair—as the first spike, back in 2015, came not from Ireland but from the Netherlands (I am not sure which firm generated it though…Apple’s tax transactions seem to have impacted the Irish data over the course of 2016 so they didn’t “pop” quite like Dutch IP investment.)

Now it should go without saying that these kind of jumps are a bit mad.

The Netherlands is actually a substantial part of euro area GDP. But a euro 100 billion/1 percent of euro area GDP (annualized) quarterly swing out of the Netherlands is still a bit much. In the real (non-tax) world, Dutch IP investment should be about 25 basis points of euro area GDP, and Irish IP investment around 10 basis points of GDP—not enough to materially affect the overall trend.

The most parsimonious adjustment to the euro area data thus is simply to net out Irish and Dutch IP investment, not to drop the entire Irish economy from the euro area (Britain has left the EU, but Ireland is proudly a part of the euro area).

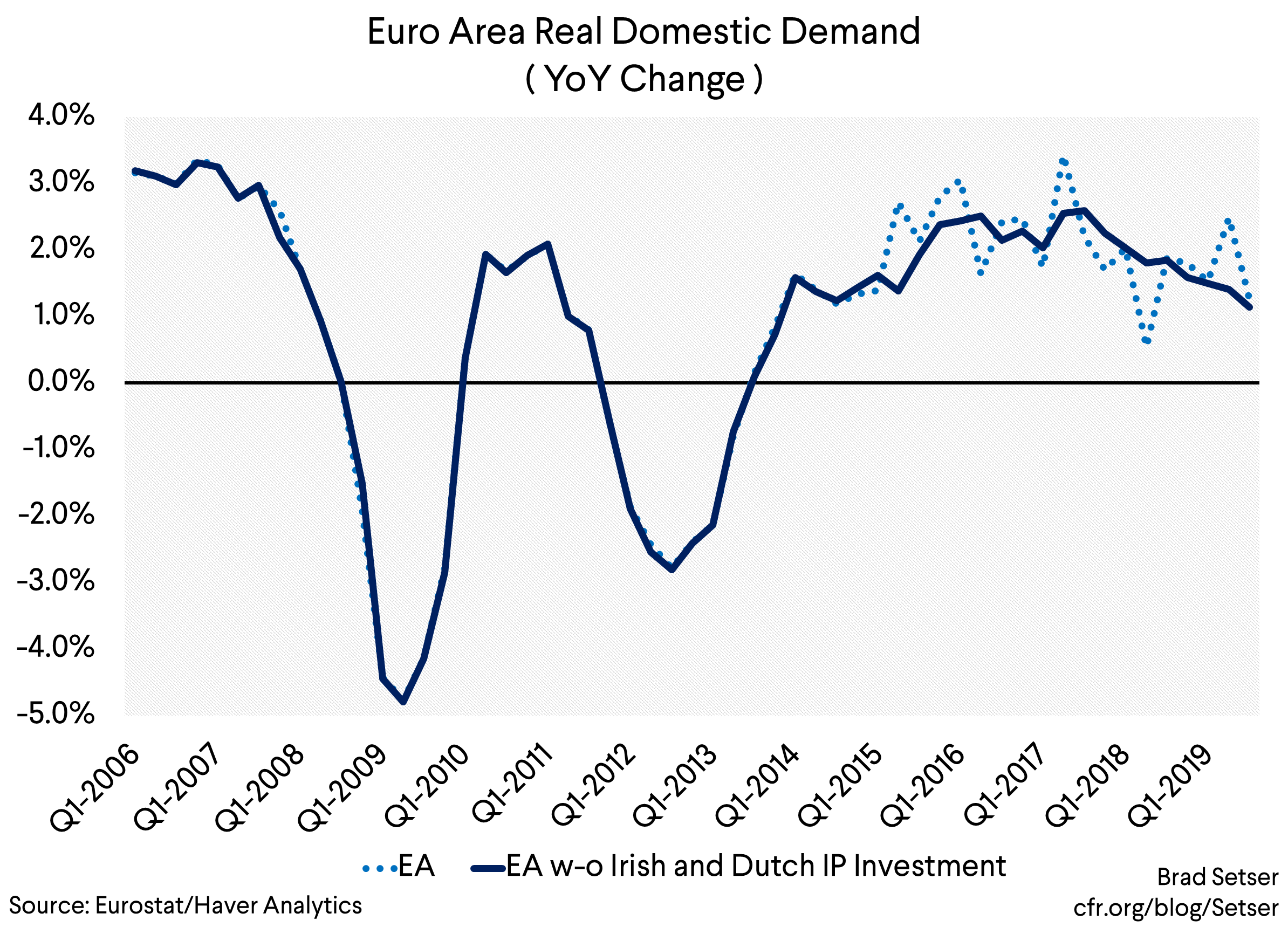

The year over year change in domestic demand (and q/q numbers) suddenly make a lot more sense.

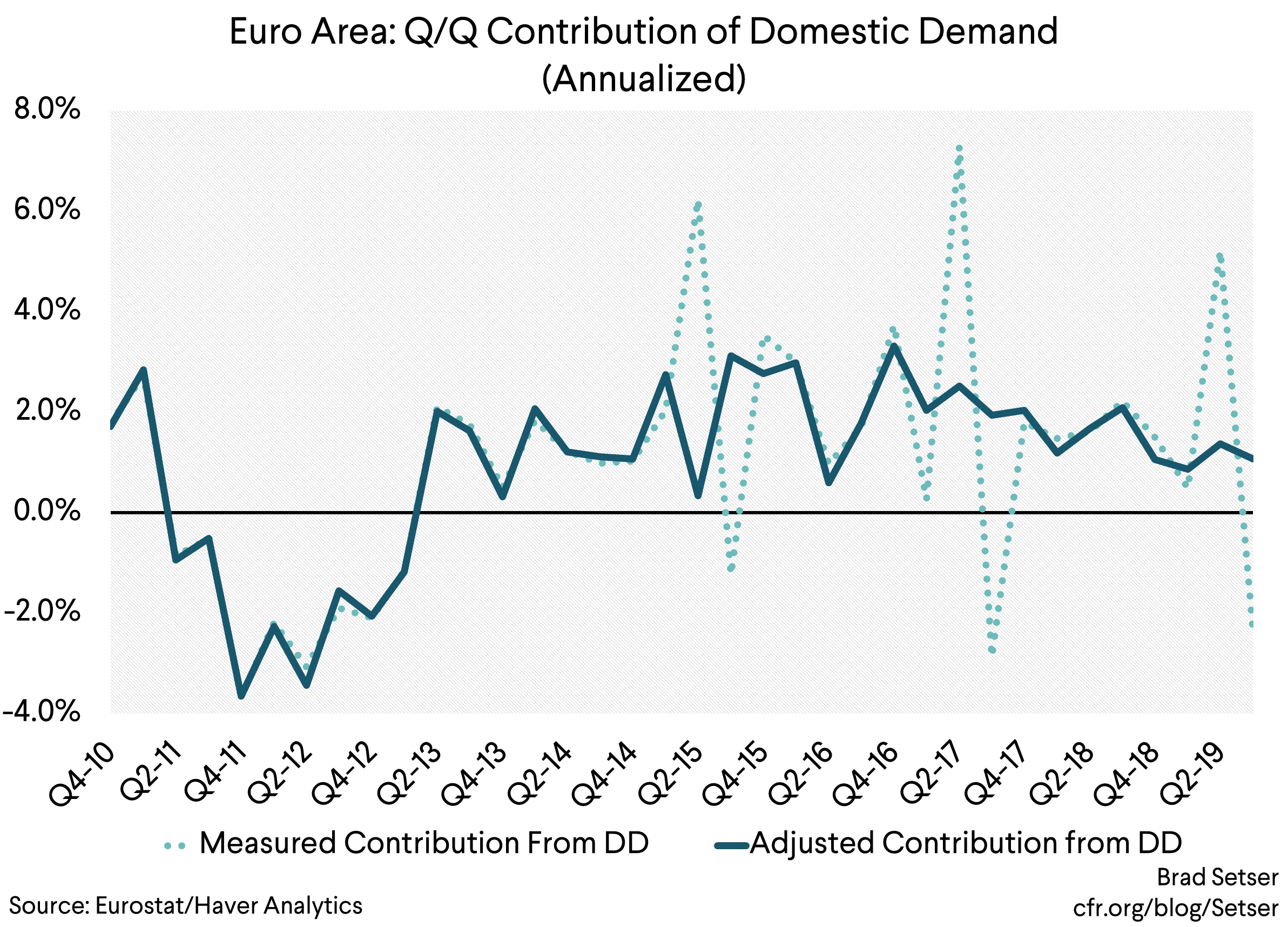

And the adjustment matters even more for the quarterly data

This isn’t just a technical matter.

The adjustment matters for policy too. It immediately becomes clear that the deceleration of overall euro area growth from the “euro boom” of 2017 has been driven in large part by a deceleration of domestic demand growth. Germany’s failure to stimulate (its fiscal surplus is likely to remain over 1.5 pp of GDP in 2019—larger than its 1 pp of GDP fiscal surplus in 2017) looms larger as a source of regional weakness.

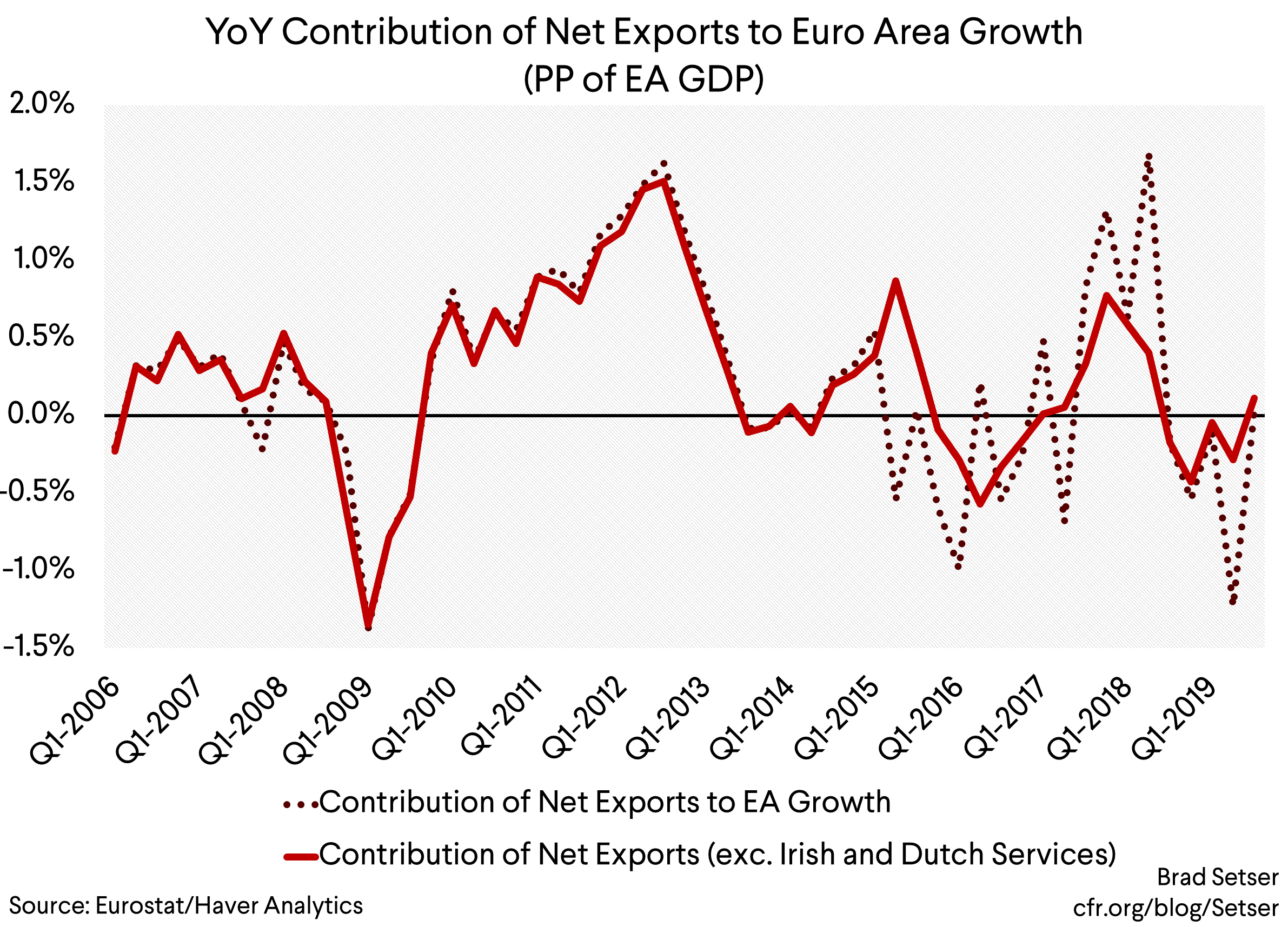

A similar adjustment is needed to the trade data. I know many people think that capturing the modern economy requires paying more not less attention to services trade. But the services trade data is heavily distorted by tax transactions (remember, for many categories of service exports, “Ireland” is the United States biggest export market). Removing Ireland and the Netherlands‘ services imports (and for completeness, exports) from the euro area data provides a cleaner picture of the underlying trend for euro area net exports.

The adjusted data changes the broader narrative around the 2017 “Euroboom”—and more importantly the narrative around the euro area’s subsequent slump. Net exports did help the euro area in 2017, but by substantially less than the headline data implies. And while net exports did contribute to the slowdown in 2018, they haven’t been a big factor in the euro area’s 2019 weakness. In fact, the high frequency data shows that the fall off in the contribution from net exports really came right at the start of 2018. That changes the narrative around the global impact of Trump’s trade war on China just a bit—that trade war really only impacted the global data in 2019 (with the 10 percent tariffs on $200 billion in December).

All this should matter to the ECB, to the Commission and I hope, to the more progressive parts of the German establishment. A slump in domestic demand in a region that has a tight overall fiscal policy (the euro area’s overall fiscal deficit is under a percent of its GDP) is something that conceptually isn’t hard for the euro area to address. And it doesn’t hinge on convincing Trump not to bring his trade war tactics to Europe in 2020.

But the profound impact that tax related distortions are having on the euro area’s aggregate data also should be a global wake up call about the scale of tax avoidance. The aggregate data for the world’s second largest economy shouldn’t be obviously distorted by the tax shenanigans of a few giant U.S. multinationals.

Leprechaun economics, it turns out, is real economics.