When the Services Trade Data Tells You More About Tax Avoidance Than About Actual Trade…

In theory, there is a strong case for trade in services—specialization raises the productivity of all.

Yet the actual data on U.S. trade in services tells a less appealing story. Far too much trade in high end services seems to be with low tax jurisdictions. I love the Irish, but there is something wrong when “Ireland“ is the United States’ leading export market for software services, business consulting services, and R&D services.

The United States, like the U.K., is a services driven economy. So it follows, at least to many, that the United States naturally should run a substantial surplus in services trade.

This simple argument though leaves a lot out.

To start, many—if not most—services are still hard to trade. A lot of services, as we are learning all too quickly, rely on personal contact. Others are hard to trade across linguistic borders and time zones. Once you set aside the portion of services trade linked to the movement of people, the bulk of actual trade remains in goods.

The United States does run a substantial surplus in tourism trade. But that surplus doesn’t come from especially large exports. The United States isn’t say Greece, which is a really big tourism exporter. The U.S. surplus in tourism trade instead comes from the United States‘ relatively modest tourism imports. Americans don’t travel all that much outside the United States.

I have long joked that the French should complain that American firms’ limited vacation time is a hidden barrier to trade in services.*

And, well, the United States’ surplus in high-end services (exports of intellectual property and the like) isn’t all that it seems.

It is real, no doubt. In fact, it almost certainly is understated on net, for reasons that I will explain later.

But the geography of service trade shows a clear pattern—namely, that, an awful lot of actual trade in services is currently with the world’s low tax jurisdictions.

In theory, services trade sounds great. In practice, it often doesn’t look so good.

Rather than exporting software and other high-end services to say China, or Germany, or France, U.S. firms prefer to export their services to Ireland, Switzerland, or the Caribbean. Their subsidiaries in these low tax jurisdictions in turn book the profits on their overseas sales, usually at a rate well below the headline U.S rate on corporate income (The lowest tax rate in the U.S. corporate tax code is the 10.5 percent rate on offshore intangible income, which is currently set at half the headline 21 percent rate).

The net result—enormous investment by U.S. and other firms in low tax jurisdictions, enormous profits for U.S. firms in the world’s low tax jurisdictions, and a very distorted geography of services trade.

My conclusion here is simple. We shouldn’t celebrate increased services trade so long as that trade reflects tax avoidance rather than efficient specialization and true trade in tasks.

And I would hope that discussion of global chains of tax avoidance becomes as commonplace as discussion of global supply chains now is.

When U.S. firms export intellectual property to their wholly owned subsidiaries in the Caribbean, who then license the right to use that intellectual property to another subsidiary in Ireland, and then the United States imports an Irish made good (at a substantial markup over production costs), the overall result is a lot of trade in goods and services—but not much, if any, gain in economic efficiency.

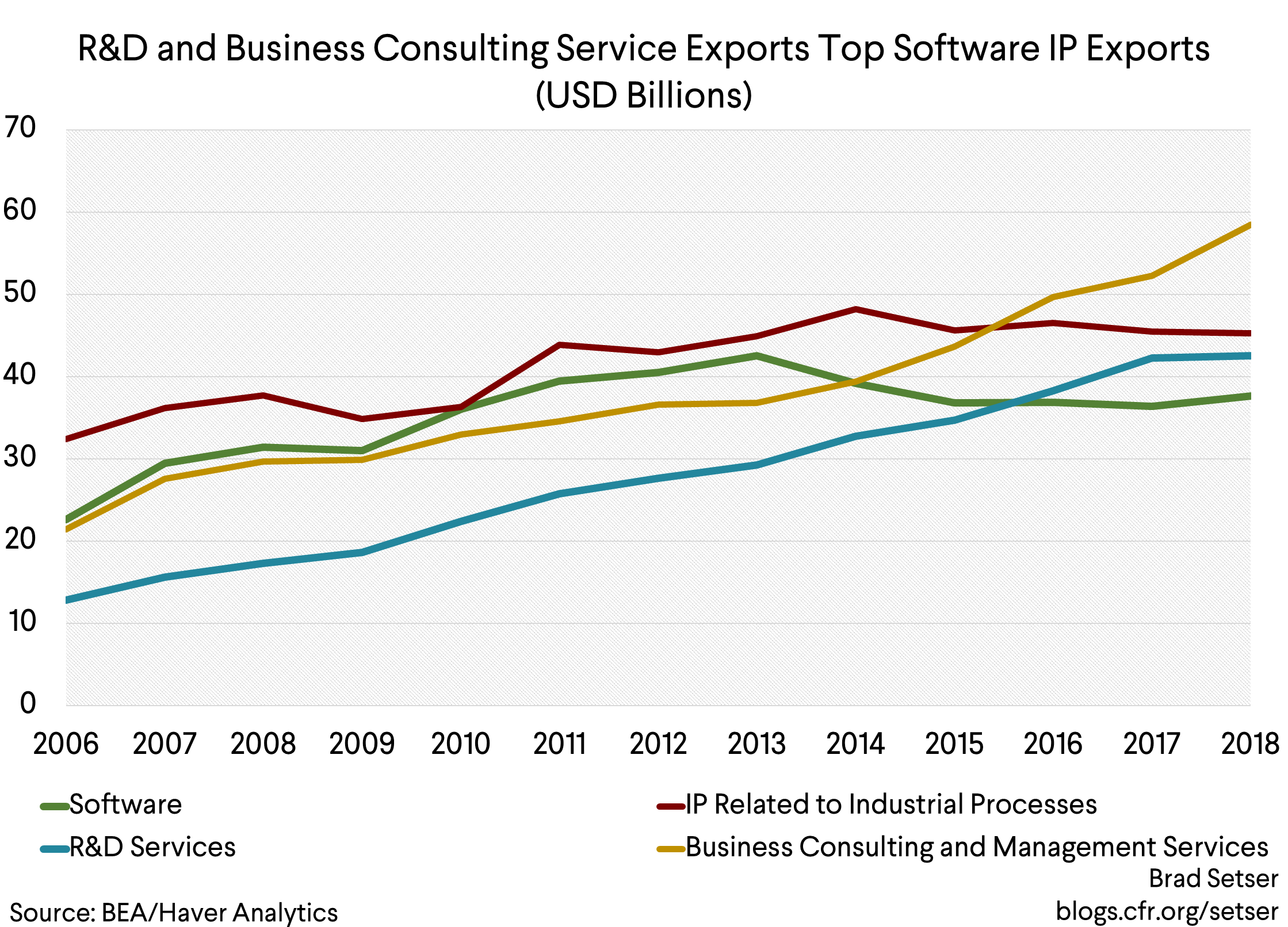

I want to build this case through a review of the numbers on U.S. trade in a number of key services categories. All categories that I will examine are categories where the United States runs a substantial surplus in the overall trade data. They collectively account for about $300 billion of total services exports.

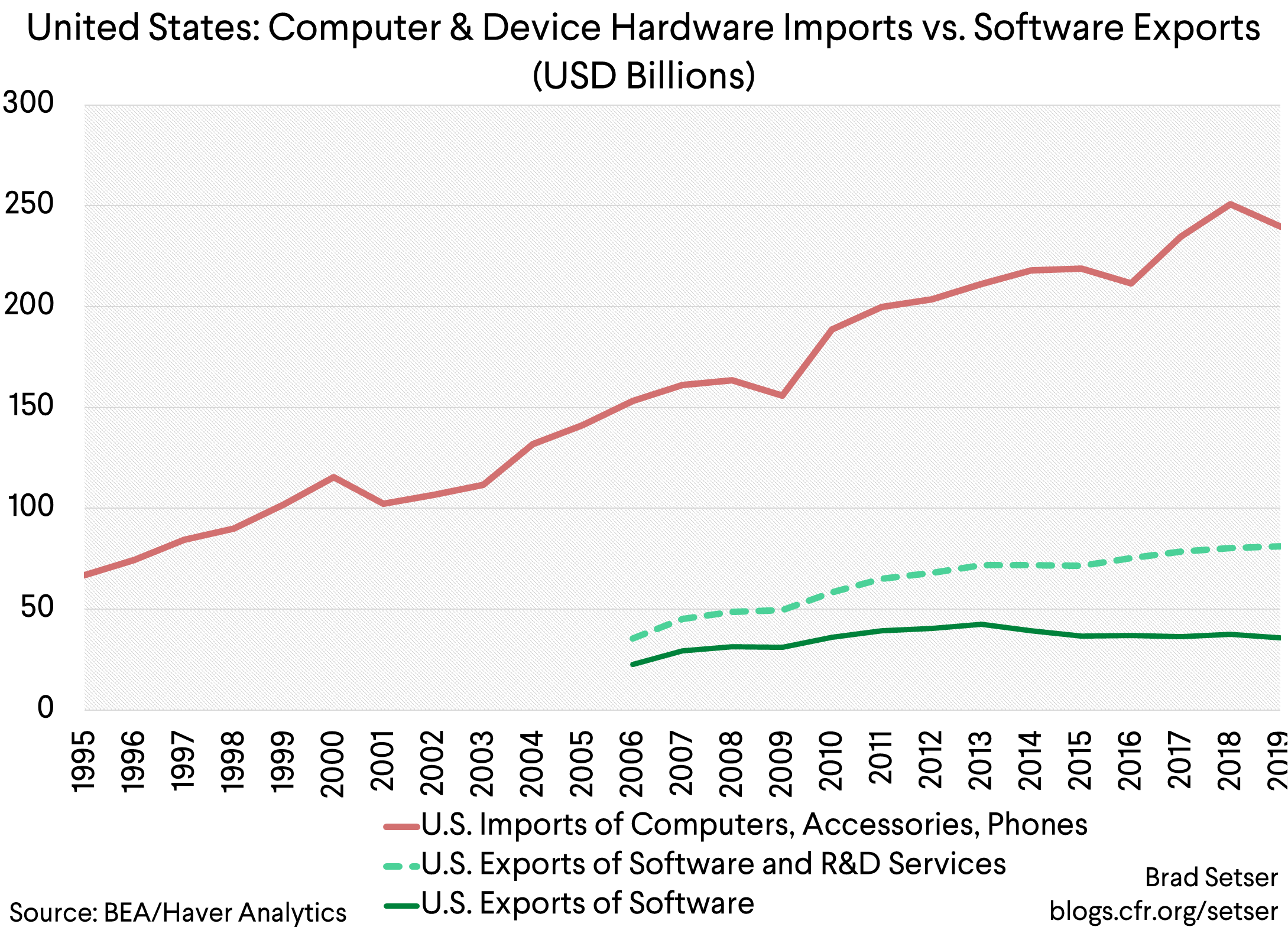

Let’s start with trade in software.

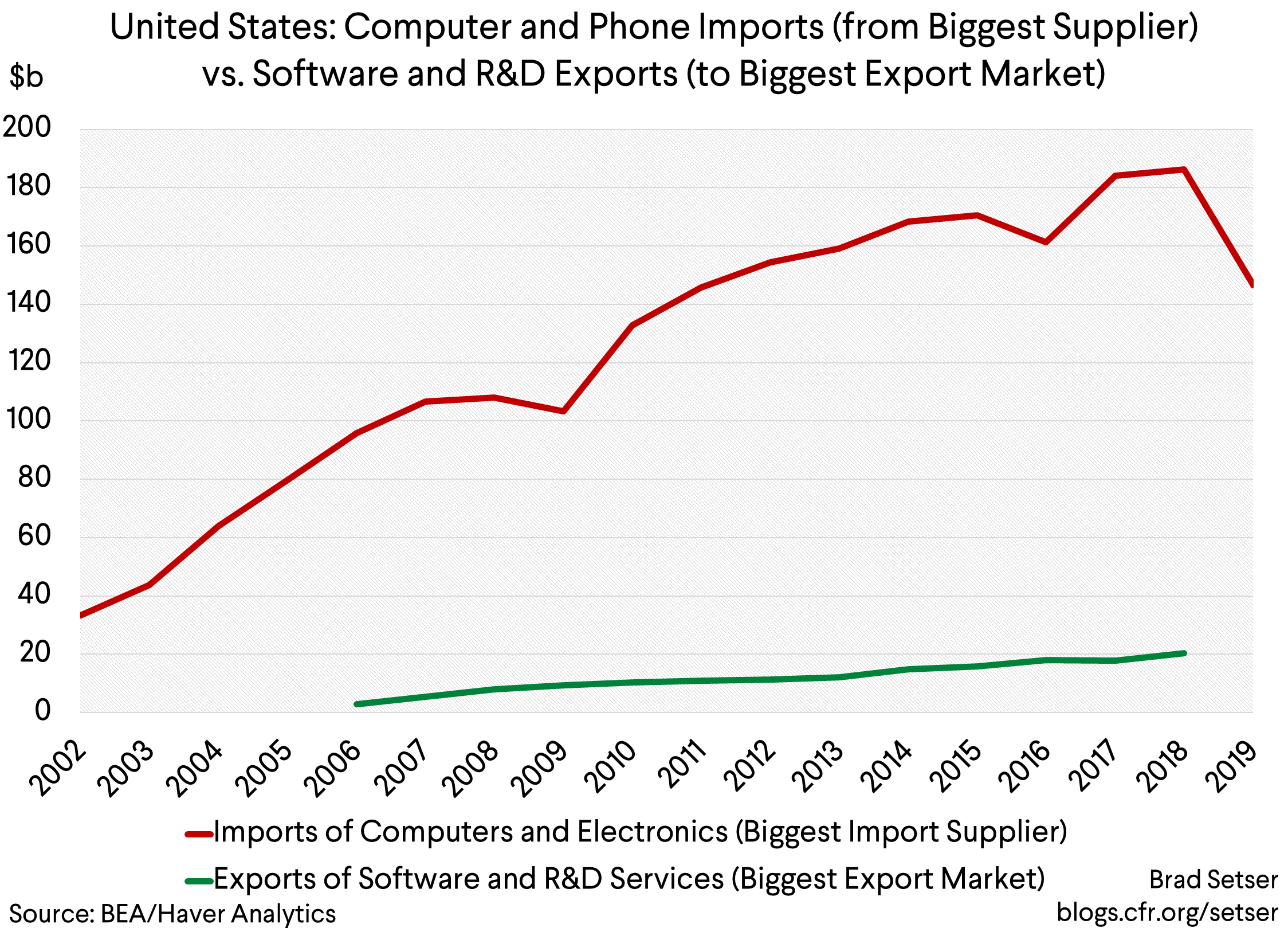

No surprise, the United States runs a substantial surplus in software services. That makes sense—the United States is the home of Microsoft and a number of other giant software firms. Apple for example sells phones, but the value of its phone derives significantly from Apple’s proprietary operating system. Google and Facebook are software companies of course, but they make their money—famously—by selling advertising not by selling software, so they shouldn’t enter the trade data here.

Many have argued—drawing on the Apple analogy (Apple gets all the profits off an Asian centric manufacturing supply chain)—that the United States need not worry about its trade deficit in electronic hardware because of its success in software. That it is just efficient specialization, with a U.S. owned company reaping the lion’s share of the profits from a global supply chain through service exports.

But, well, the numbers don’t quite bear that story out. At least not the trade numbers.

The biggest supplier of computer hardware to the United States is of course China, which draws on a bigger Asian electronics supply chain, but has also significantly increased its share of manufacturing value added in electronics over time (see Yuqing Xing; the widely cited “China gets only $8 for manufacturing an iPhone factoid is wildly out of date).

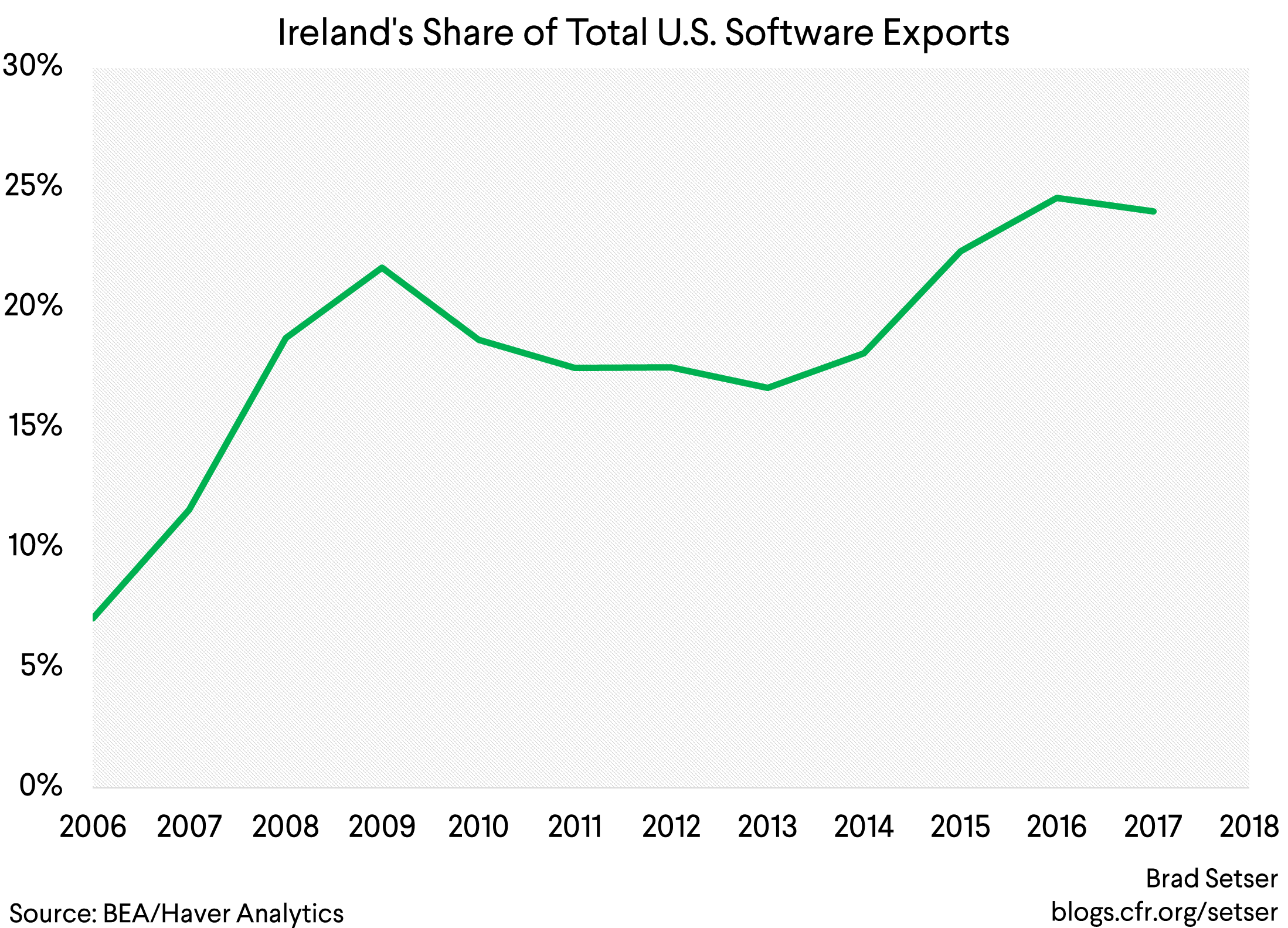

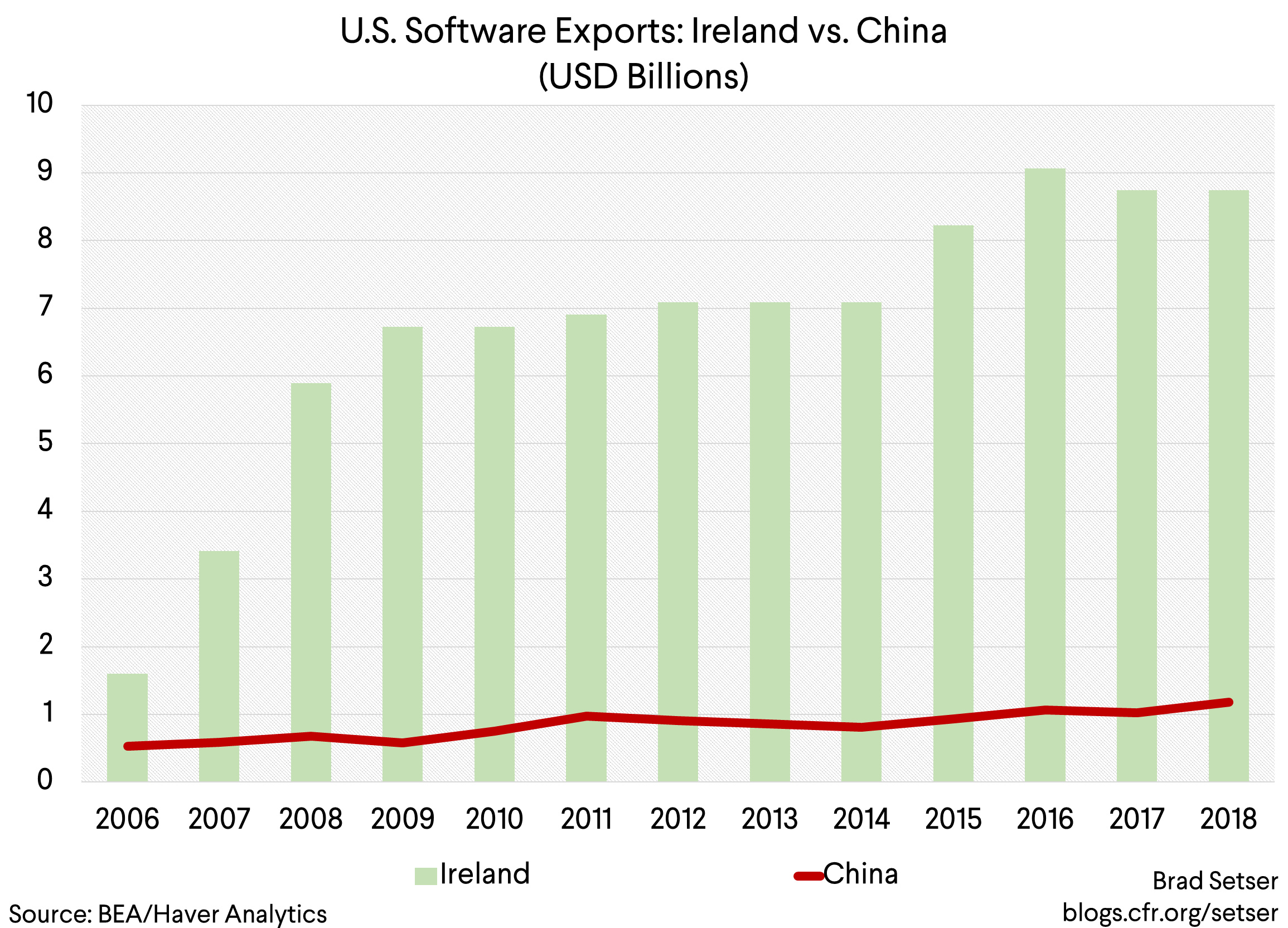

The biggest export market—judging from the trade data—for U.S. software though isn’t China. Or any other country with a large population. It is rather Ireland.

And by a significant margin—Ireland now accounts for 25 percent of U.S. global software exports (using the 2017 data -- the 2018 data was hidden to protect confidential firm information).

Software exports to Ireland are about 8 times software exports to China.

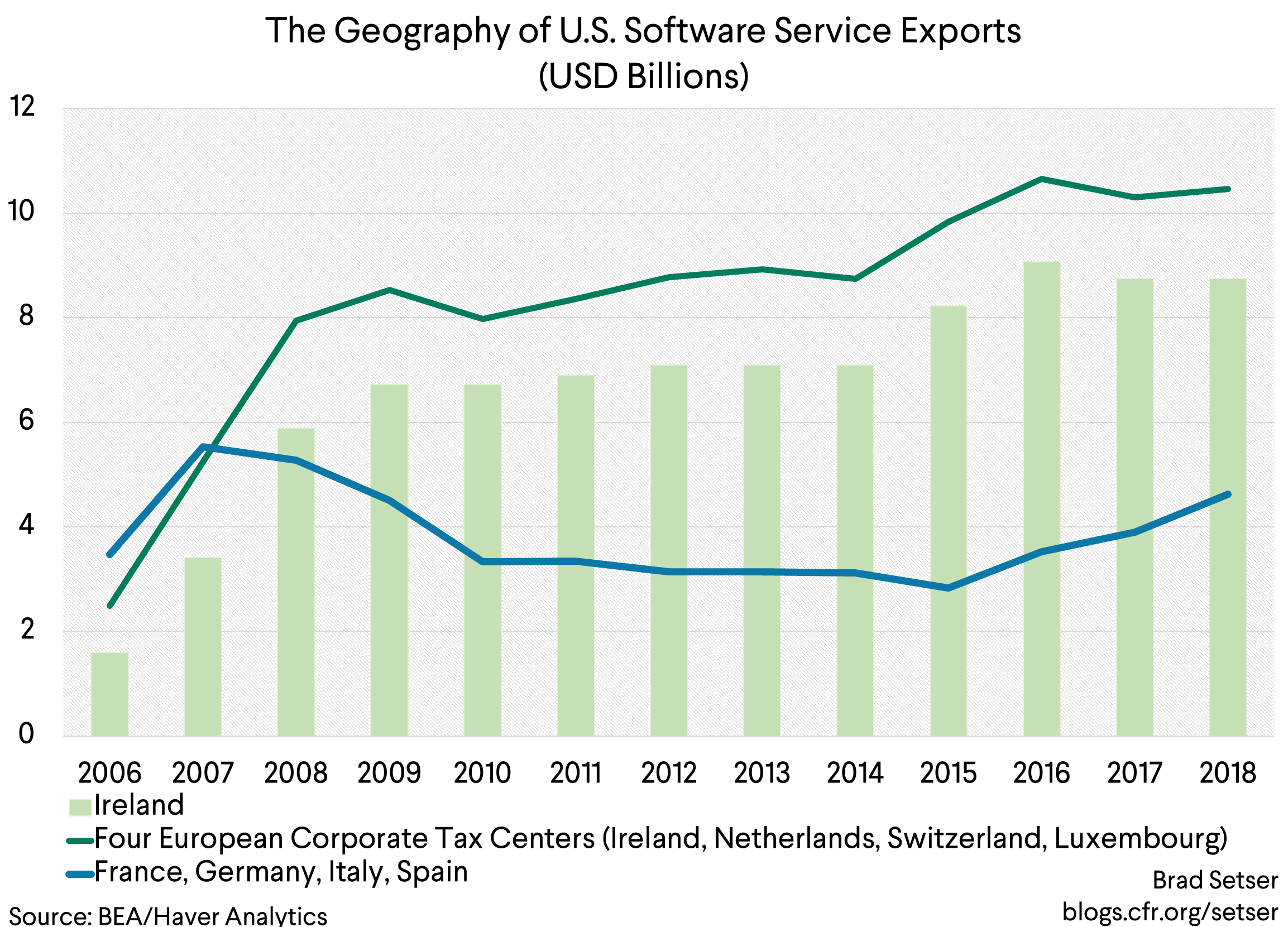

And if you think that this is because China doesn’t pay full freight on its imports of U.S. software, that’s only partially right. Software exports to Ireland are also far larger than software exports to France, Germany, Italy, and Spain combined (Ireland’s population is around 4.9 million, vs. ~ 250 million in the four biggest continental European markets).

So it isn’t a surprise really that recorded U.S. exports of software fall far short of covering the bill for U.S. imports of electronics hardware. Recorded software exports actually aren’t that impressive—$35 billion is roughly two times U.S. soybean exports, but only about half U.S. civil aviation exports. And it is tiny relative to the amount the United States spends on imported electronic hardware.

Now many would say that this analysis must be missing something. We know that Apple makes a ton of money on its phones and sells a lot of them around the world. And we know Microsoft makes a ton of money selling its software all around the world.

That’s actually right. But I haven’t missed something big in the software services trade data. Finding Apple in the trade data takes a bit more work. Apple’s tax strategy means that Apple’s profits on its global sales don’t primarily show up in the U.S. trade data as software or design exports. Rather they show up in the broader balance of payments data as a big part of the offshore profit of U.S. firms, and of course, Apple also now shows up in a big way in the post 2015 Irish GDP data.

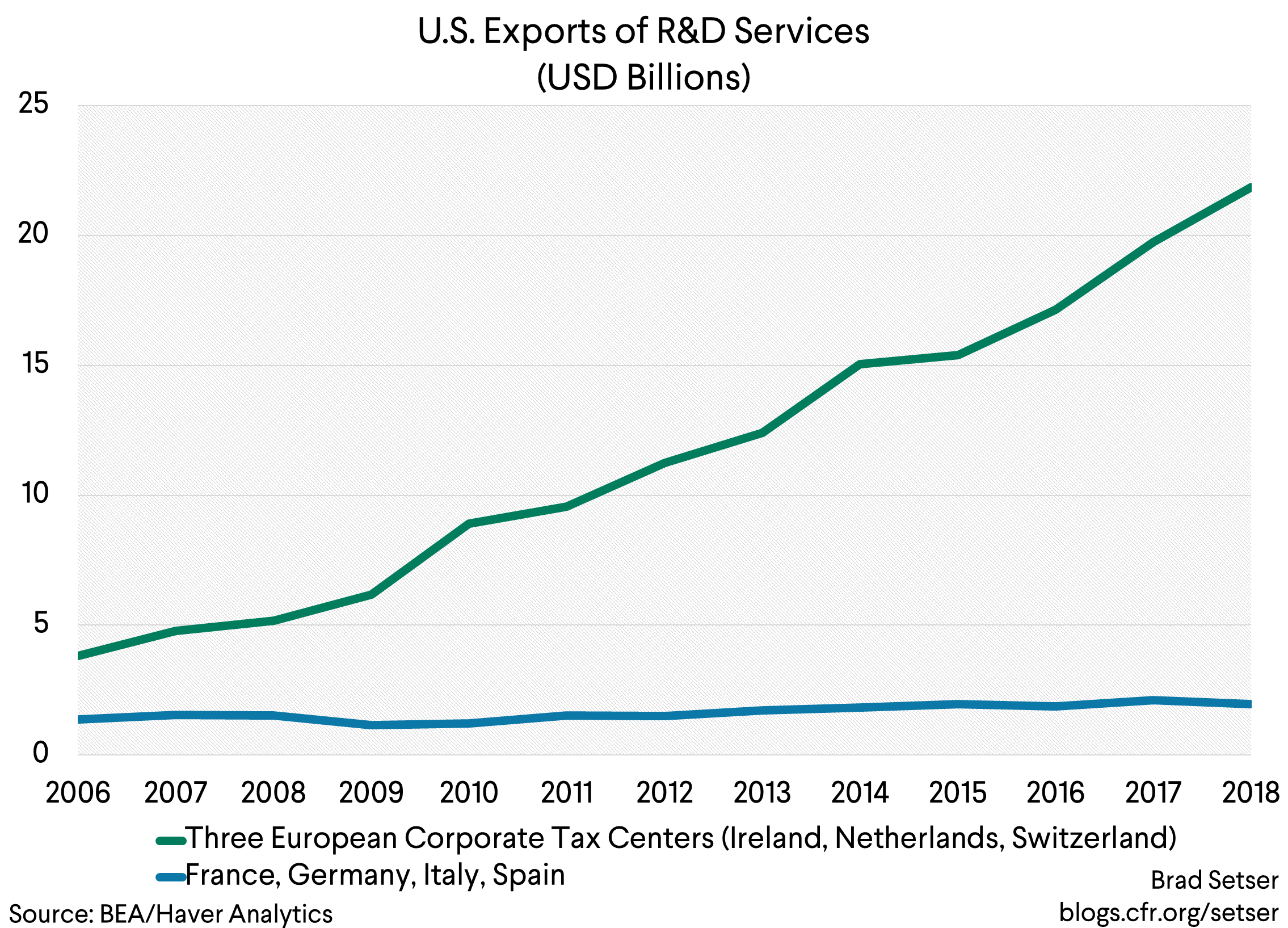

Now let’s turn to a bigger services export category—research and development services.

Note that I included R&D services in the graph above. That isn’t an accident. This is the services trade category Apple is now likely hiding in.

The key here is the work of Senator Levin’s Senate subcommittee on investigations. Because of their forensic sleuthing, we know that Apple has long had a research and development cost share arrangement with its Irish subsidiary. As part of this deal, Apple’s Irish subsidiary pays something like 60 percent of Apple’s R&D budget (something like 60 percent of $10 billion, based on disclosed information) and in turn gets the right to book the profits on Apple’s sales outside of the Americas (so Apple Ireland probably generates around $30 billion or so of Apple’s $55 billion in profits). That’s a pretty sweet deal—Apple’s Irish subsidiary is undoubtedly one of the world’s most profitable and most valuable companies.**

All this implies that Apple enters the U.S. services trade data as an exporter of “research and development services” rather than as an exporter of software. And that its measured exports will fall well short of its total global sales.

And lest anyone think I am singling out Apple unfairly, Apple’s tax structure is exceptionally common. I am using Apple as a stand in for many other companies with similar tax structures. The Levin committee documented how Microsoft uses a similar structure.

It thus shouldn’t be a surprise that exports of research and development services have been growing very rapidly over the last ten years. Nor should it be a surprise that the bulk of this growth has come from exports to countries with a reputation for offering multinational companies a favorable tax environment.

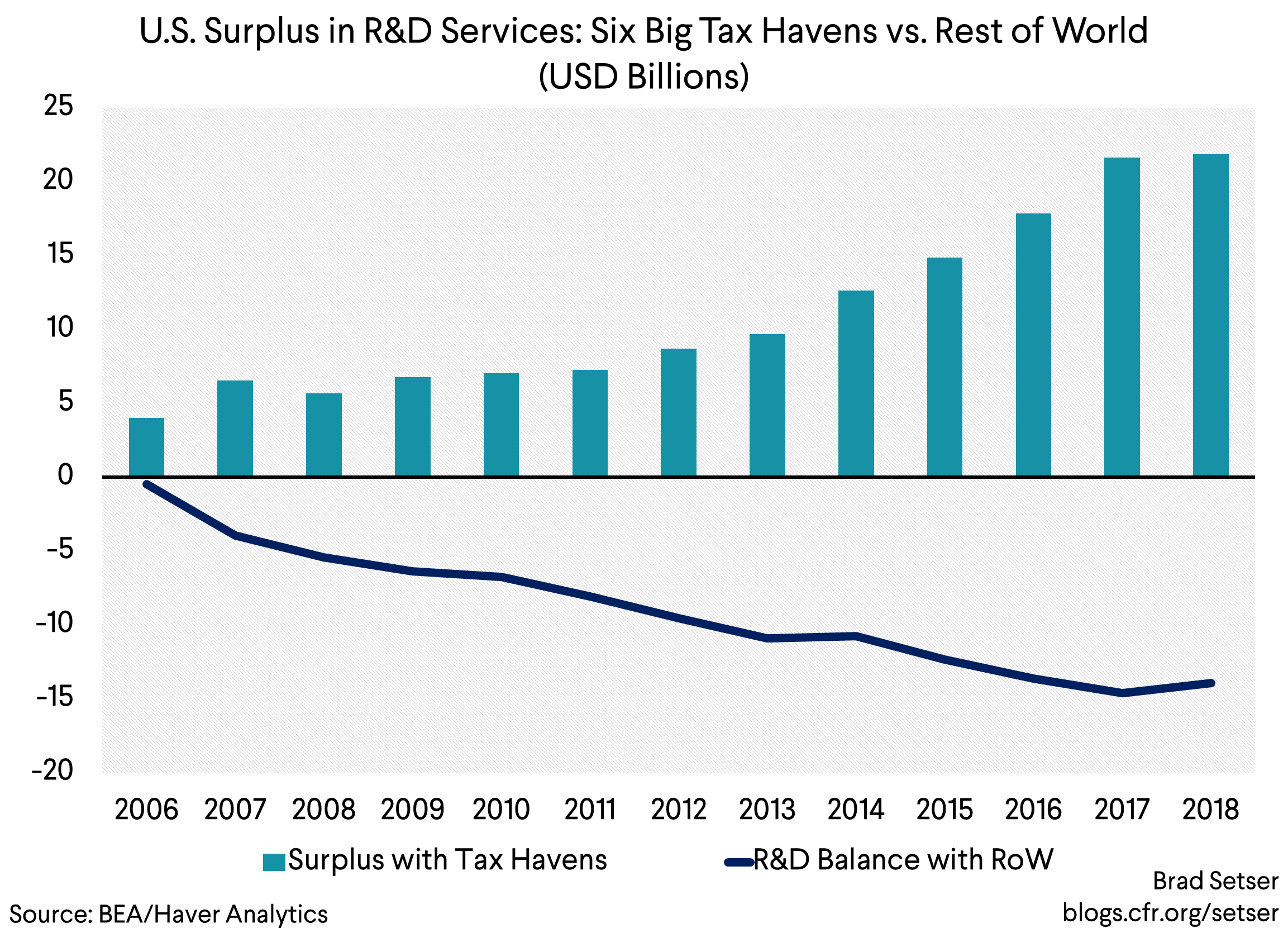

Ireland is the number one U.S. export market here. Switzerland is number two. In fact, about 70 percent of all U.S. exports of R&D are to low tax jurisdictions, and the surplus the United States runs with these countries accounts for the entire surplus that the United States runs in this particular category of services trade.

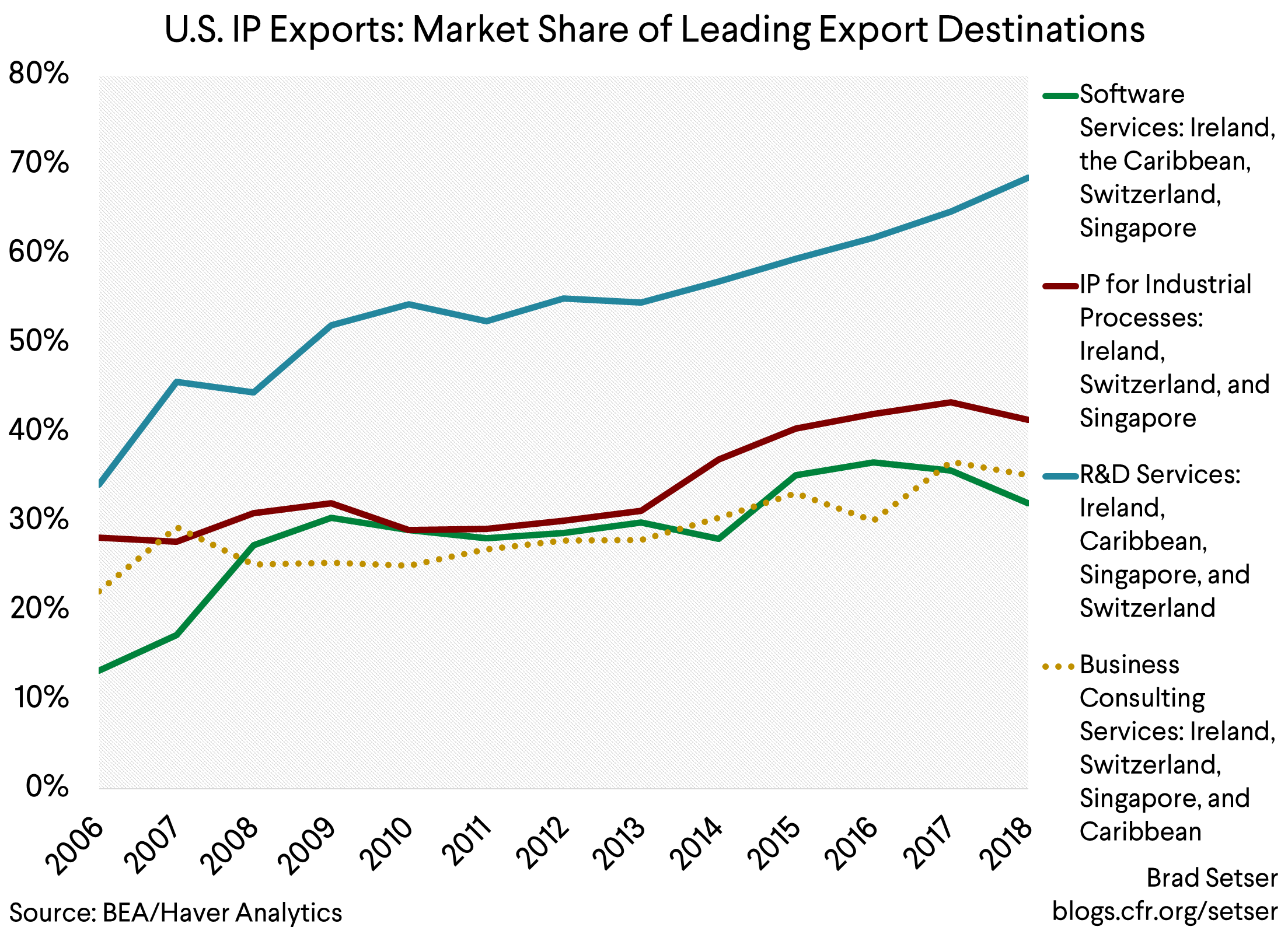

Trade in R&D services is an extreme case. But when you look at a range of high-end service export categories, the world’s main low tax jurisdictions account for between a third and two thirds of U.S. exports.

The biggest export market for U.S. business consulting services? No surprise: Ireland ($9 billion of a $60 billion total). The second biggest: Switzerland (at $6 billion). See the BEA data (table 2.2 in the interactive data).

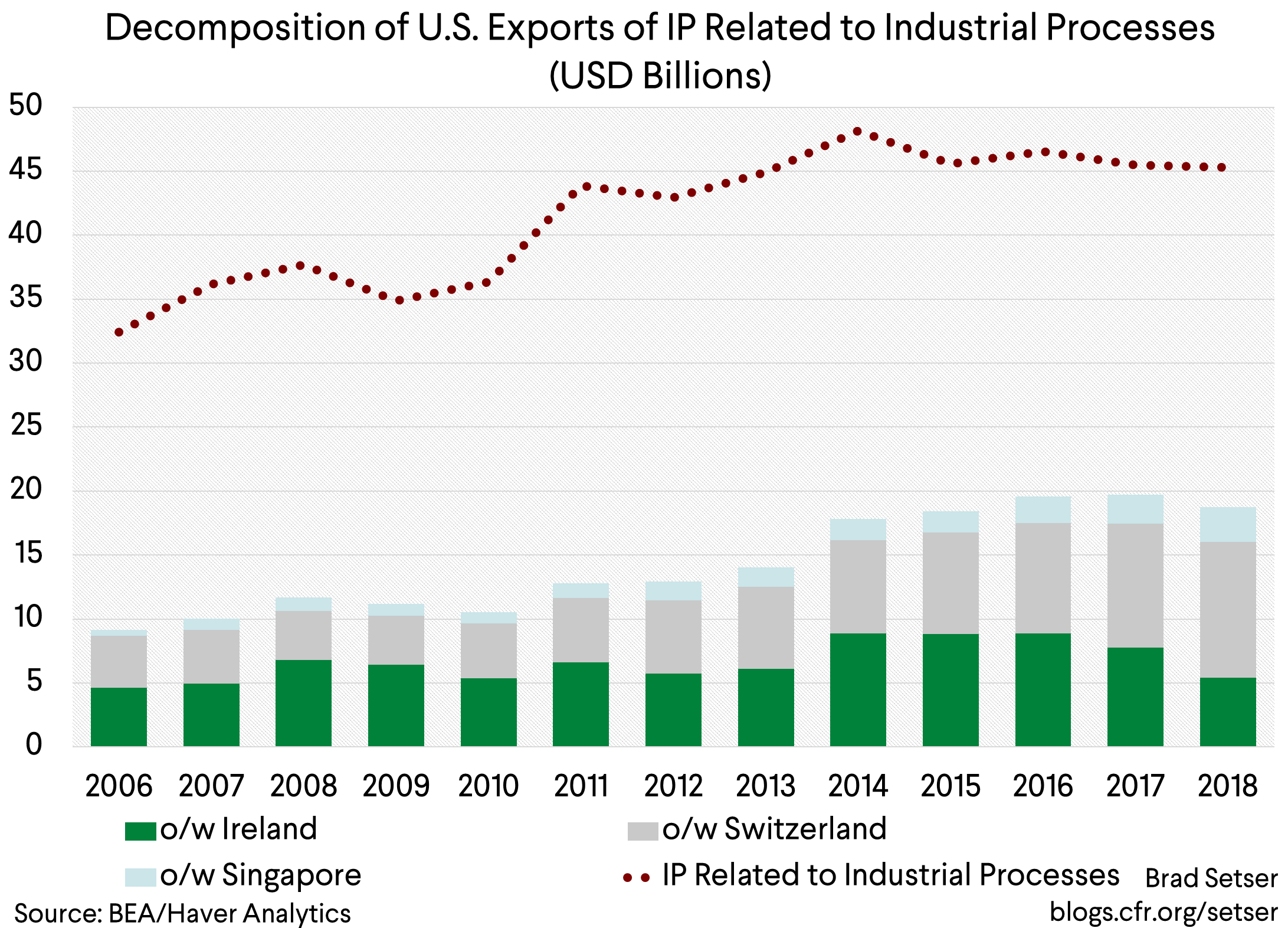

And the tilt toward low tax jurisdictions isn’t limited to the obvious categories. A big U.S. “IP” export is the export of “IP related to industrial processes.” This is, in fact, a bigger category of services exports than software—and for that matter, a bigger category than films, legal services, or architectural and engineering services.

One might reasonably expect that the biggest market for exports of intellectual property related to industrial processes would be Germany.

Or Japan.

Or perhaps China.

But no, the biggest market here is Switzerland.

It started to edge Ireland out in 2017, and now accounts for almost 25 percent of total U.S. exports in this services trade category.

My strong suspicion is that a lot a pharmaceutical intellectual property exports are showing up here. Ireland and Switzerland are also the two biggest suppliers, in dollar terms, of pharmaceutical goods to the U.S. market. Singapore also registers strongly in the data here, and it is also both a tax hub and a center for pharmaceutical manufacturing. Just a hunch.

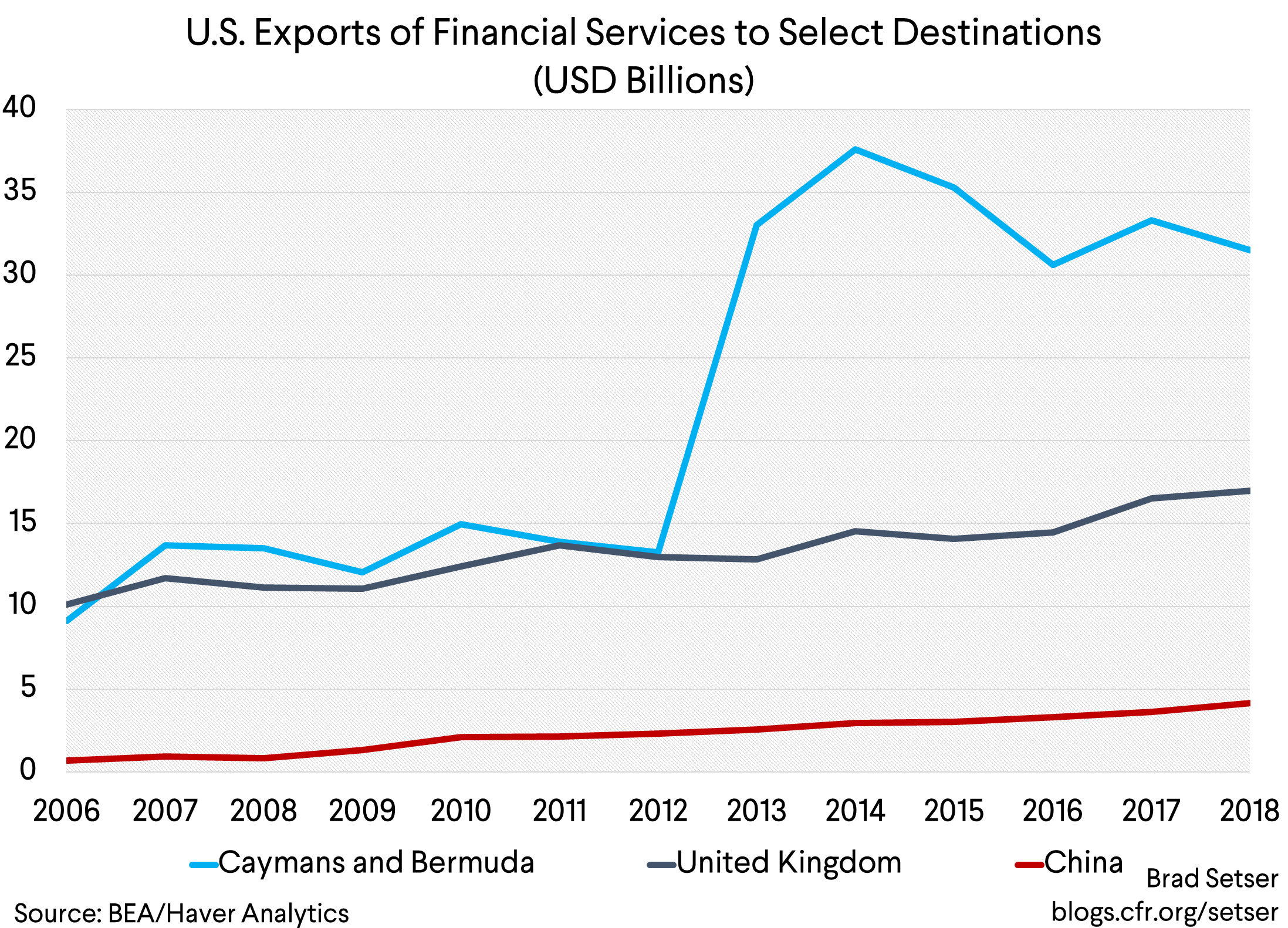

I have focused on the IP export categories most related to “tech” so far. But the U.S. is also a big exporter of financial services.

And guess who is the biggest U.S. export market?

The “UK Caribbean” of course (the Caymans and the Bahamas for all intents and purposes).

The “UK Caribbean” now buys twice as many U.S. financial services as the UK.

Based on this data, I would guess George Town (the Cayman’s capital) must be a bigger financial center than London, as the U.K. Caribbean islands account for a little over a quarter of all U.S. exports of financial services these days (exports jumped when the BEA started looking for hidden services trade in 2013).

I think the geography of trade here matters: in category after category, the United States exports more services to small islands known for their low tax rates than to the world’s biggest economies. This almost certainly isn’t an accident—a lot of this services trade is among the subsidiaries of the same company, and the bulk of U.S. foreign direct investment these days is also in the world’s low tax jurisdictions. Most of the services export categories I have laid out are the first step in a series of global tax chains that allow U.S. firms to report the bulk of their earnings abroad in a small number of low tax jurisdictions (see the graphics the New York Times produced to accompany my oped).

To be sure, the overall impact of these tax shenanigans on the U.S. trade balance is a bit ambiguous.

Exports of software services to Ireland rather than Germany give rise to enormous “Irish” profits from sales that are ultimately made in Germany. Take out the Irish middleman and the United States would be exporting more services—and U.S. firms would be paying a lot more corporate income tax than they are now.

But in other cases, the export of services results in higher goods imports. Think of the impact of exports of IP related to industrial processes to Switzerland, or the export of R&D to a Caribbean isle that then licenses the use of that IP by a factory in Ireland. The tax game here is for a U.S. firm to export underpriced IP to a low tax jurisdiction, and then to import an overpriced active pharmaceutical ingredients back to the United States (drug prices in the U.S. are higher than they are in other advanced economies).

Chip design houses no doubt play a similar game. By exporting IP rather than making their own chips in the United States, they can lower their U.S. tax rate. That’s part of the reason why the United States now imports far more chips (embedded in electronics) than it makes.*** The 45 percent market share of U.S. semiconductor firms is the share of U.S. owned designed firms in global chip sales, not the share of actual chip production in the United States. Many important firms are fabless, and rely on Taiwanese and Korean contract manufacturers (Intel is an honorable exception that has maintained cutting edge American manufacturing capacity). Here IP service exports result in fewer chip exports—and little embedded U.S. manufactured content in the world’s most advanced machines.

Why does this matter?

Well, the trade data here tells you something about how the world’s most profitable firms avoid paying the headline U.S. tax rate on much of their global profit. That’s a concern in a world where the public sector is often starved of the revenues needed to fund necessary public services.

And the structure of U.S. corporate tax also explains in part why the United States has run persistent deficits in manufacturing trade. The tax code pretty clearly incentivizes U.S. firms to export IP to low tax jurisdictions, and make IP heavy products for sale globally abroad rather than in the U.S.

Something to look at, perhaps, once the coronavirus is overcome.

* The Council is very generous here. I certainly used to do my part to help balance U.S. tourism trade.

** In 2015, Apple’s Irish subsidiary bought IP from Apple’s Jersey subsidiary for around $300 billion, and in the process generated an annual depreciation allowance and interest deductions of up to EUR 45 billion. As a result, Apple is a BEPS compliant tax resident of Ireland with a very low effective tax rate in Ireland (see the Wikipedia page on Ireland’s tax system, section 3.1.1).

*** This cannot be seen directly in the trade data, as the bulk of chips aren’t imported as chips but rather inside phones, tablets, computers, and telecommunication equipment. The U.S. share of global chip production is now around 10 percent.