Oil Production Has Moved North, and Auto Production South

Both Mexico and the U.S. are in a sense adjusting to (mild) oil shocks …

Mexico is producing and exporting a lot more autos. Texas is producing a lot more oil, and exporting a decent amount of refined product and gas too.

Any comment on swings in the pattern of trade these days tends to be viewed through a “Trumpian” lens.

But this one shouldn’t be.

At least not primarily.

Mexico, like the United States, in aggregate runs a trade deficit with the world. Mexico isn’t—despite Trump’s obsession with the bilateral deficit—a bad actor on trade. It helps the United States absorb the surpluses of East Asia and Europe.*

That though doesn’t mean there haven’t been big sectoral swings in the pattern of comparative advantage over the past ten years.

And one key change really has come more over the last ten years, long after NAFTA had been implemented. In the past few years, Mexico has largely stopped exporting oil and shifted to exporting cars. And the United States—thanks to the tight oil boom—has stopped being a big oil importer.

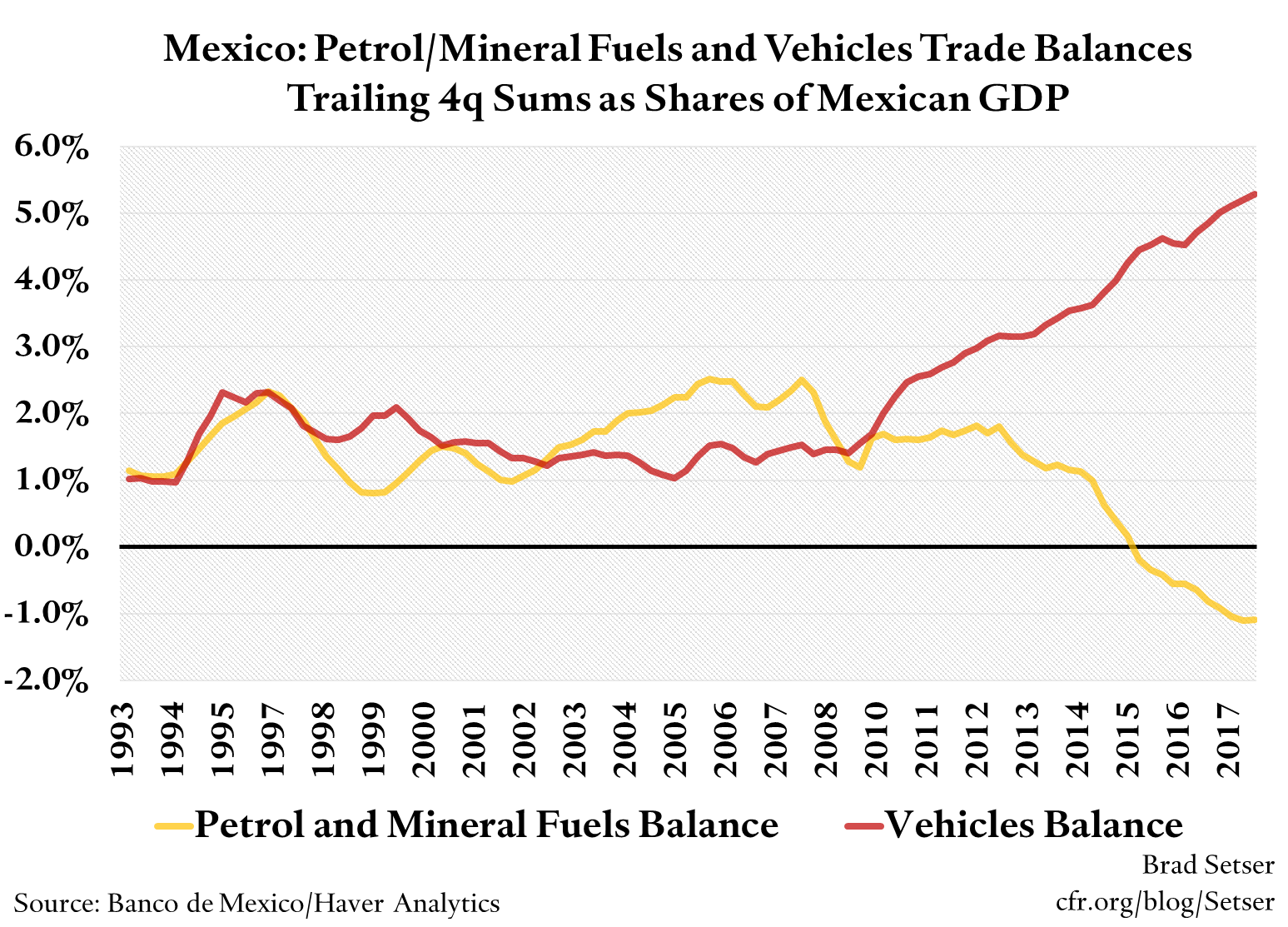

Look at Mexico’s overall trade. Auto exports (and the “surplus” in autos) is way up. And Mexico now runs a deficit in petrol and gas—it still exports some crude to U.S. refiners, but it imports more product (and gas) than it exports in crude.

Broadly speaking the jump in auto exports after the crisis has offset a structural deterioration in Mexico’s oil balance. And the adjustment came about the old fashioned way, through market signals.

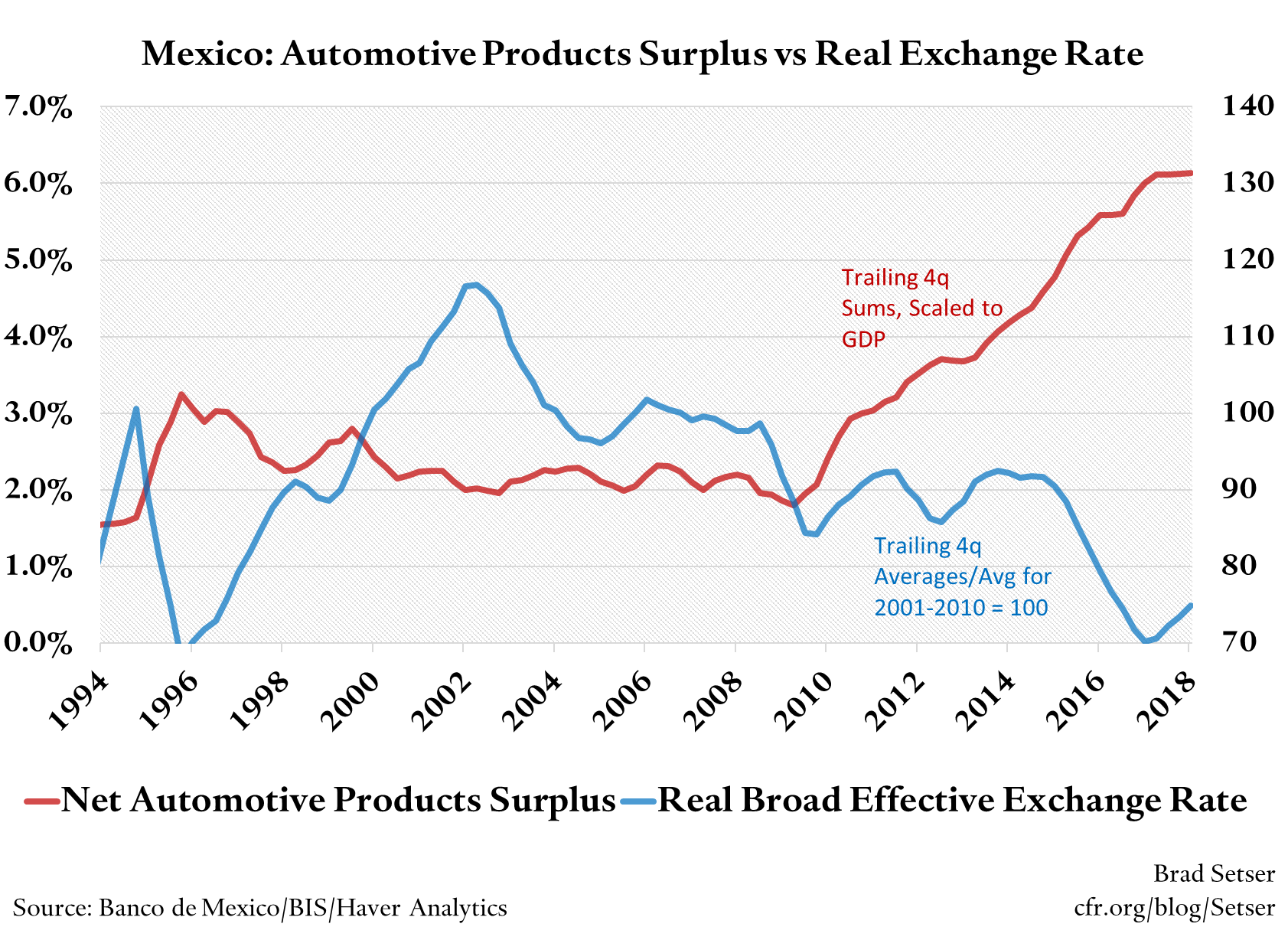

After the global crisis, the Mexican peso fell—and it has stayed well below its pre-crisis level since. In real effective terms the peso is about 25 percent below its pre-crisis level, and pretty close to its 1995 peso-crisis lows.

Mexican exports of autos more or less stalled from 2000 to 2008, even with the NAFTA preference. They only started to grow after the restructuring of the U.S. auto sector in the aftermath of the great North Atlantic financial crisis combined with the weakness of the Mexican peso to encourage production to shift south. No doubt the fact that Mexico’s auto industry has matured and obtained critical mass matters too (just as the U.S. tight oil revolution has matured and producers have learned how to exploit tight formations efficiently).

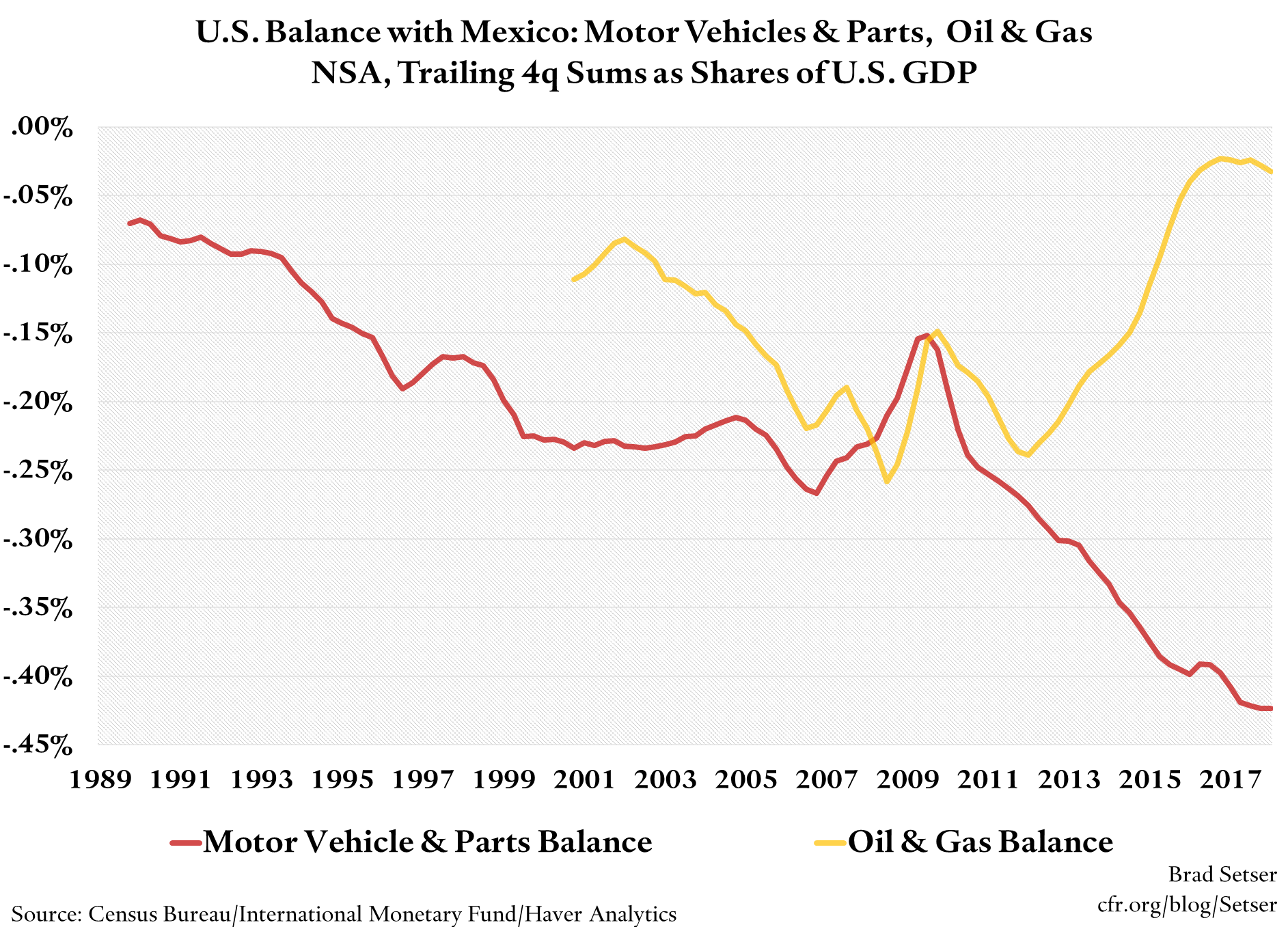

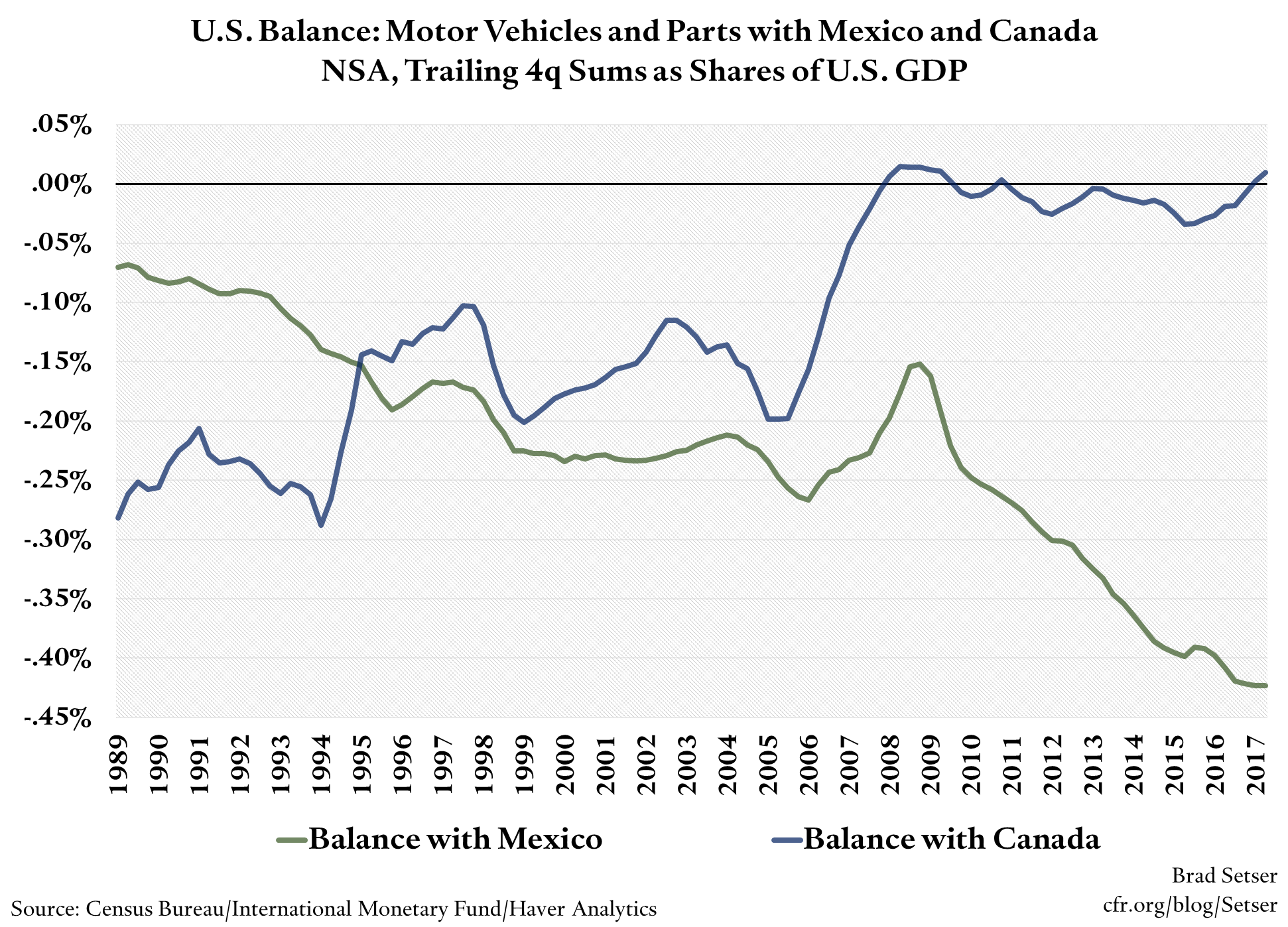

These trends of course show up in the U.S. data too. Net auto trade with Mexico has shifted into a substantial deficit while the deficit in petrol has almost disappeared.

This is sort of how trade is supposed to work—it should lead to shifts in jobs across sectors, but if it is fairly balanced, not a big shift out of tradables production.

By the way, the U.S. also gained automotive market share vis a vis Canada between 2003 and 2012, when the Canadian dollar was strong. The aggregate swing in the United States‘ NAFTA trade balance since say 2005 has been much smaller than the swing in the bilateral balance with Mexico.

Yet there clearly has been a swing in the balance with both North America and Mexico since say 2010 (the start of the tight oil revolution). In the United States’ case, there are now more jobs in the production of oil and gas than were the case in the past, but somewhat fewer jobs in auto manufacturing than would be the case had the shift in supply chains toward Mexico been less pronounced.

And those shifts in turn seem to have had an outsized political impact. Trump is threatening auto tariffs that would extend to the NAFTA countries absent a deal on a renegotiated NAFTA that has a “high wage” content requirement to discourage too rapid a shift in production toward Mexico. And AMLO wants Mexico to return to oil self-sufficiency, with more domestic production and more domestic refining capacity…

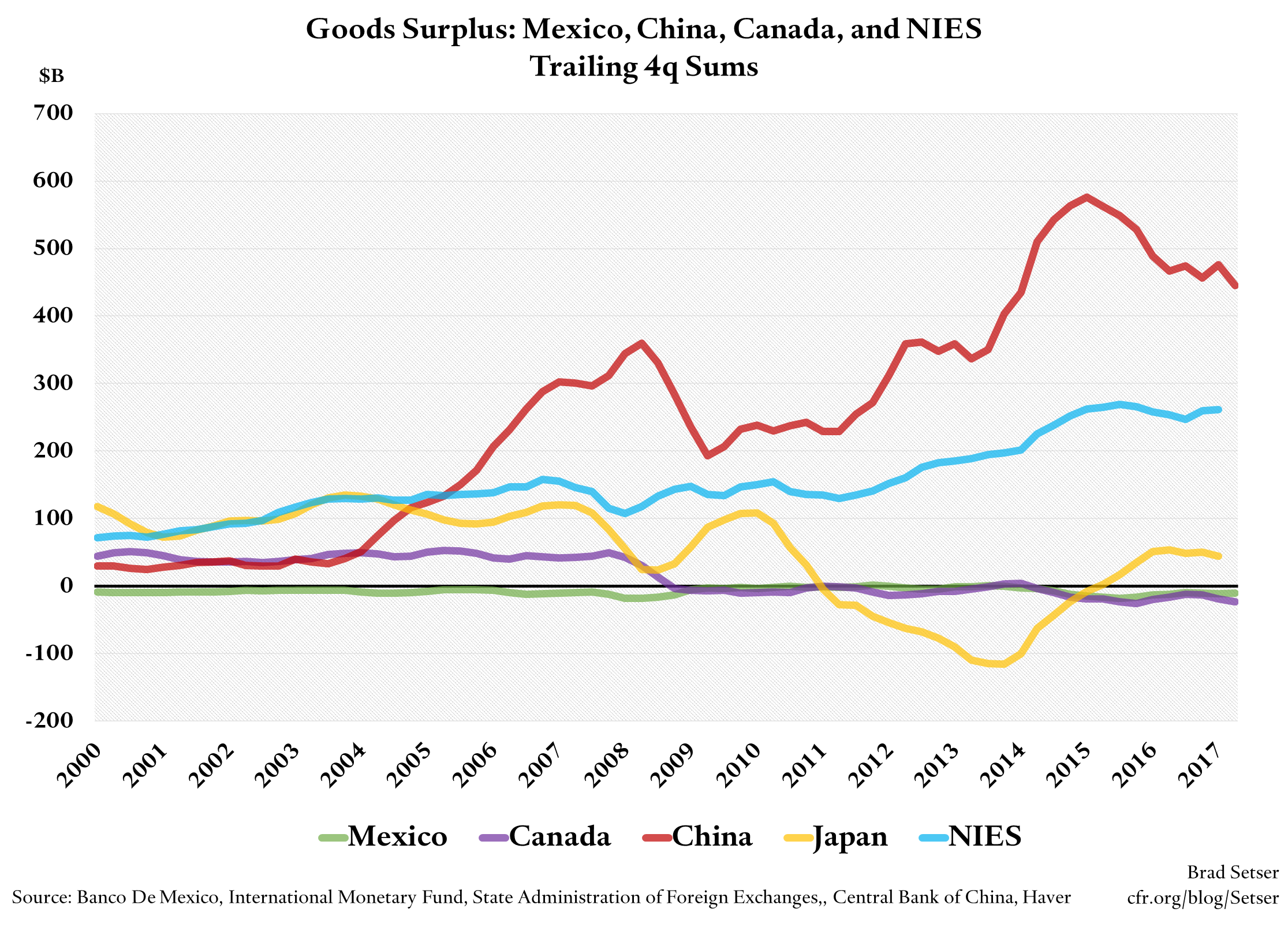

*/ A chart of the aggregate goods surplus of China, the Asian NIEs, Mexico and Canada is revealing. China’s goods surplus remains large, and it is much more precisely measured than the broader current account.