President Xi, Still the Deglobalizer in Chief…

Can China generate new friends by strategically opening its markets while…also importing less?

(Don’t judge China just by changes in its tariffs, the Chinese state has many other policy tools to limit imports)

Chad Bown of the Peterson Institute has argued that China is getting a leg up by, well, cutting tariffs for the world even as it raises tariffs on the United States.

That’s certainly true, even if the tariff cuts are modest relative to the increase in tariffs on the United States.

But, in my view, it is also only part of the story.

China naturally imports commodities, and it recently has tilted its commodity imports away from the United States (beans, oil, lobster, and so on). But diverting your commodity imports away from a commercial rival is pretty much standard trade strategy: to my personal chagrin the United States always retaliates against French wine and cheese in trade disputes with Europe.

The real issue, I think, is whether or not China is prepared to open up—for real—to non-American manufactured goods in order to squeeze the United States out of a big and growing potential market for U.S. made goods.

And there, I just don’t see the evidence.

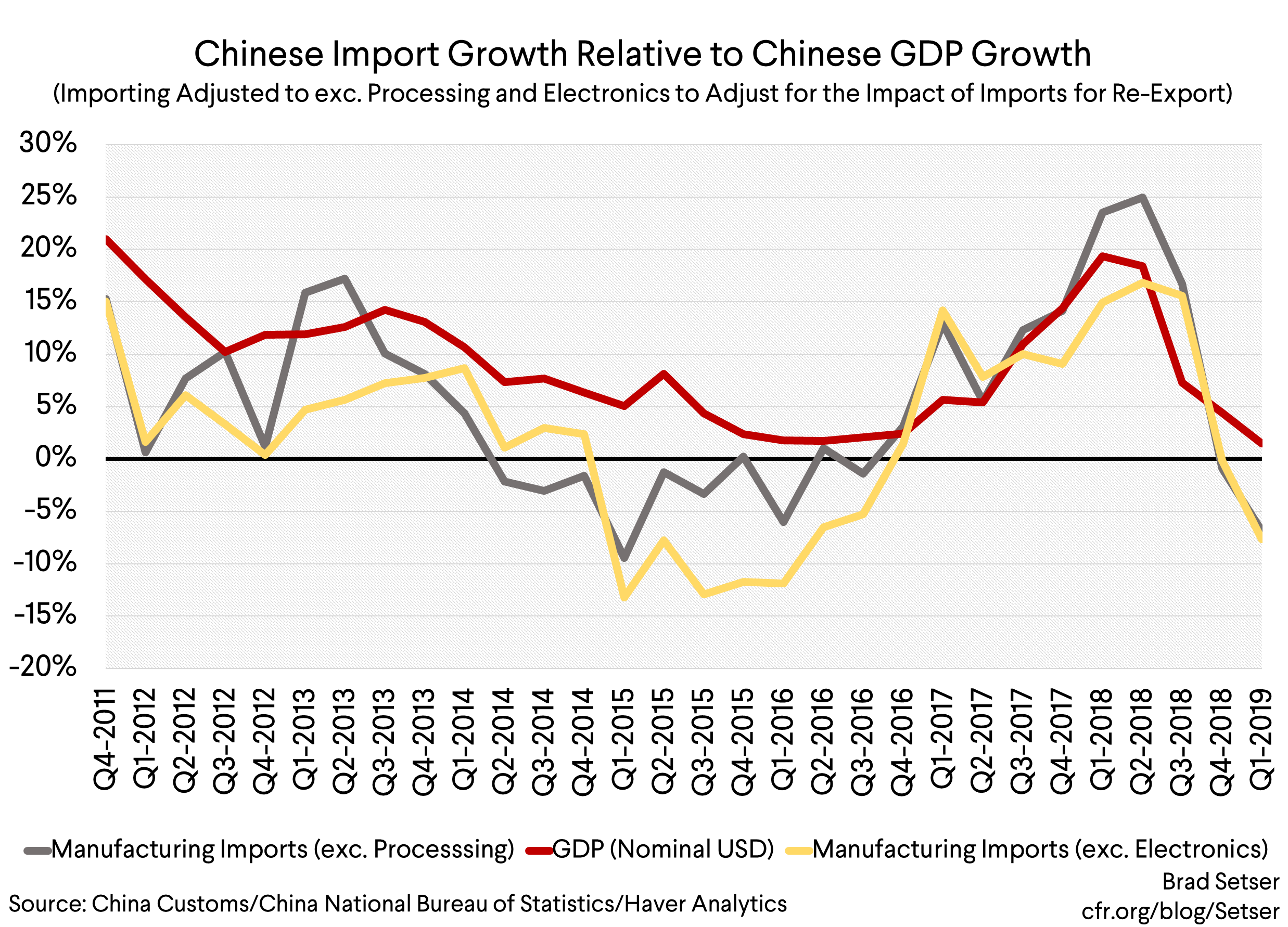

When it comes to manufactures, China is actually importing less from everyone right now—even with the (quite modest) tariff cuts.

Best I can tell that isn’t just a function of the fact that China is also exporting less, or a result of the global fall in semiconductor prices. As the chart above shows, it is true if you take out electronics imports, and it is true if you take out “processing” imports (imports for re-export).

And it isn’t a new story either.

I would argue that China under Xi has deglobalized more than the United States under Trump.

Imports, broadly speaking, should normally grow with a country’s GDP. During the globalization or hyper globalization era, they grew more rapidly than GDP. After the crisis, they have basically grown with GDP in most countries.

But import growth, in dollars, has lagged dollar GDP growth in China over the last eight years. Even when import growth was surprisingly strong in 2017 and 2018, it only matched dollar GDP growth.*

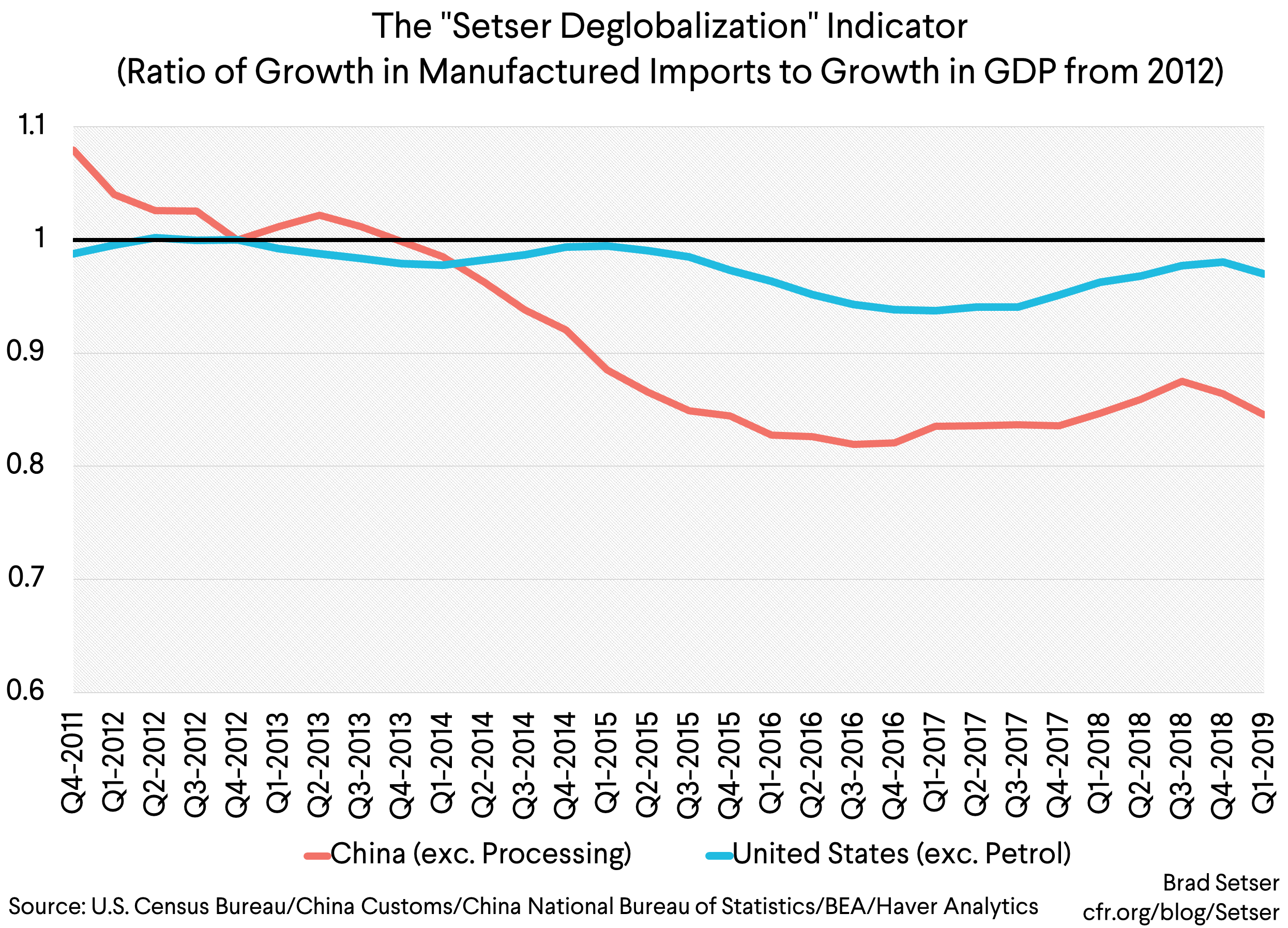

The fall in imports vs. GDP is deglobalization in my view. And with China you can adjust for imports that are (mostly) for re-export by netting out processing imports to try to get a measure of what’s happening to imports that are directed primarily at meeting China’s own demand.

To make a good-looking graph, I took the ratio of growth in (non-processing) manufacturing imports to the growth in China’s nominal GDP from the end of 2012. And for the United States, I looked at manufactured imports after taking out imports of refined petroleum (the U.S. is clearly “deglobalizing” when it comes to imports of petrol).

If imports are growing with GDP, then the ratio will be one. If they are growing faster than GDP, it will be over one. If they are growing by less than GDP, the ratio will be under one.

China’s ratio since 2012 is well under one, largely because import growth severely lagged GDP growth.

Trump’s ratio since 2016 is about one, even with the 2018 tariffs and the modest fall in imports (relative to GDP) in the first quarter of 2019.

So far, Trump’s “stimulus” has outweighed the impact of Trump’s “tariffs.” Of course that could change…there is a difference between putting tariffs on steel, aluminum, washing machines, and solar cells and putting tariffs on all trade with China, all trade with Mexico, and auto trade with Europe and Japan.

What of the fall in China’s imports (relative to the size of China’s economy)? That might just be the natural result of the evolution of the global economy. As China converges technologically, one possible result is a China that imports (and exports) less. In China’s case, however, the fall in imports seems linked to Chinese policy choices.

Until recently, China wasn’t shy about its import-substituting industrial policy goals.

In those sectors where it now imports a ton, it had a policy goal of wanting to import less (see this 2017 article from Jane Perlez, Paul Mozur, and Jonathan Ansfield) — and is throwing a lot of money at achieving its import-substituting goals.

And, generally speaking, China cannot achieve its industrial policy goals just by importing less from the United States. Take aircraft. China doesn’t simply want to replace U.S. made aircraft (Boeing) with European made aircraft (Airbus). At a minimum, it needs Airbus to move widebody production to China—and it isn’t clear that China would be satisfied just buying Chinese made Airbuses either. China clearly wants its own indigenous aircraft firm.

China already imports very few semiconductors directly from the United States. To achieve its goals, it needs to import less from Korea and Taiwan (of course, some of those chips are produced by contract manufactures using designs owned by U.S. firms, but they register in China’s data as imports from Korea and Taiwan).

I could go on. China isn’t terribly keen to continue to import medical equipment from anyone…and, well, China only lowered its auto tariffs after Chinese domestic auto production already far exceeded domestic Chinese demand.

I am not convinced that the tiger has changed its stripes in response to Trump’s tariffs, and that China is now making a bid to raise its global influence by expanding access to its market.

In a sense, though, there has been consistency in Chinese policy over time.

The break has come from the United States—Trump is the one threatening disruption of the existing set of rules in order to get a better deal for the United States.

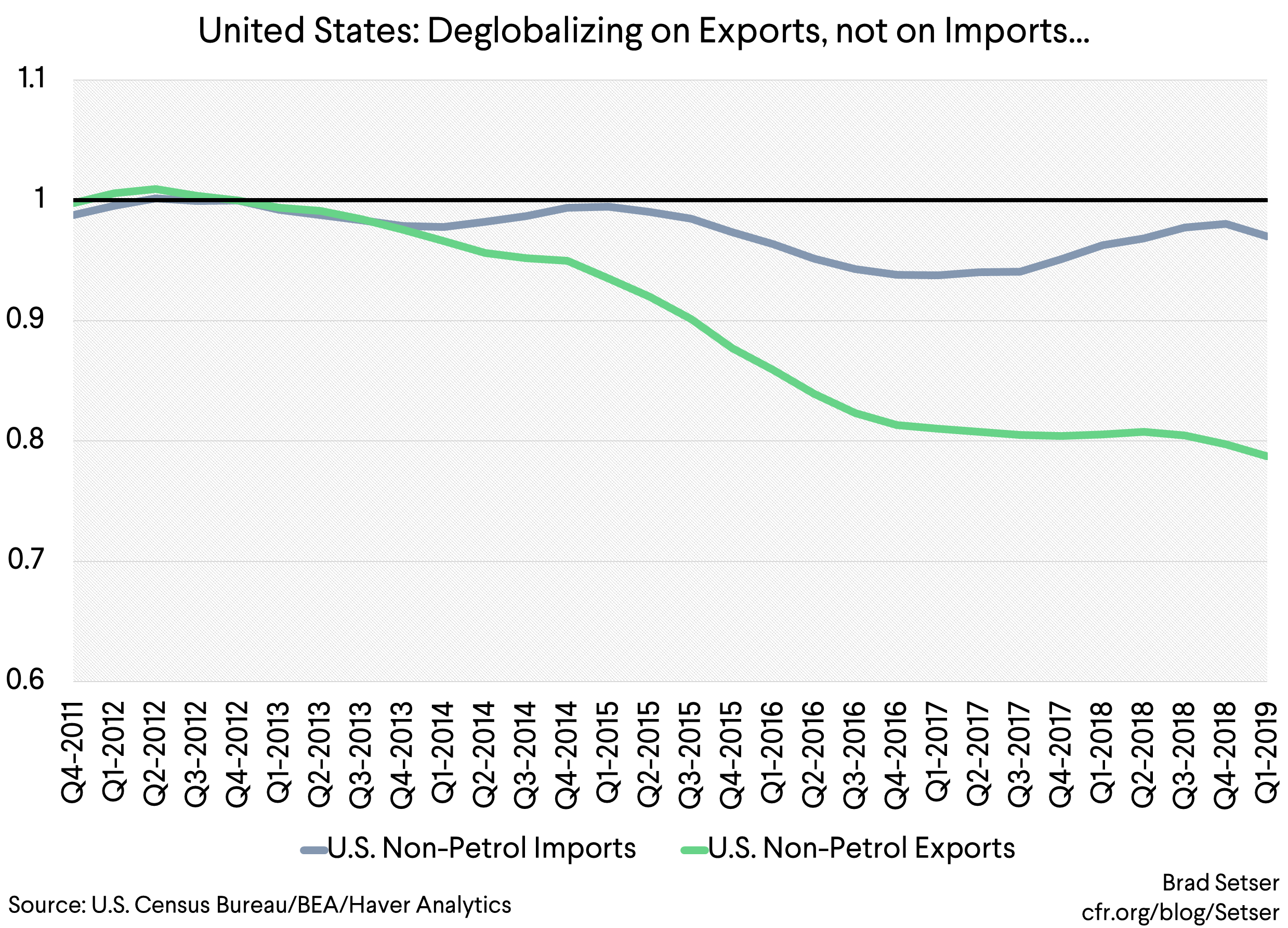

And Trump’s timing is interesting, as he isn’t directly responding to the shock and domestic disruption associated with a surge in imports. The pace of globalization, using my simple measure, had slowed after the crisis. U.S. imports were basically growing along with the U.S. economy, not faster.

The impact of the strong dollar has shown up much more on the export side—the growth in U.S. manufactured exports has seriously lagged the overall expansion of the U.S. economy since 2014—not on the import side.

Politics doesn’t move in a straight line…

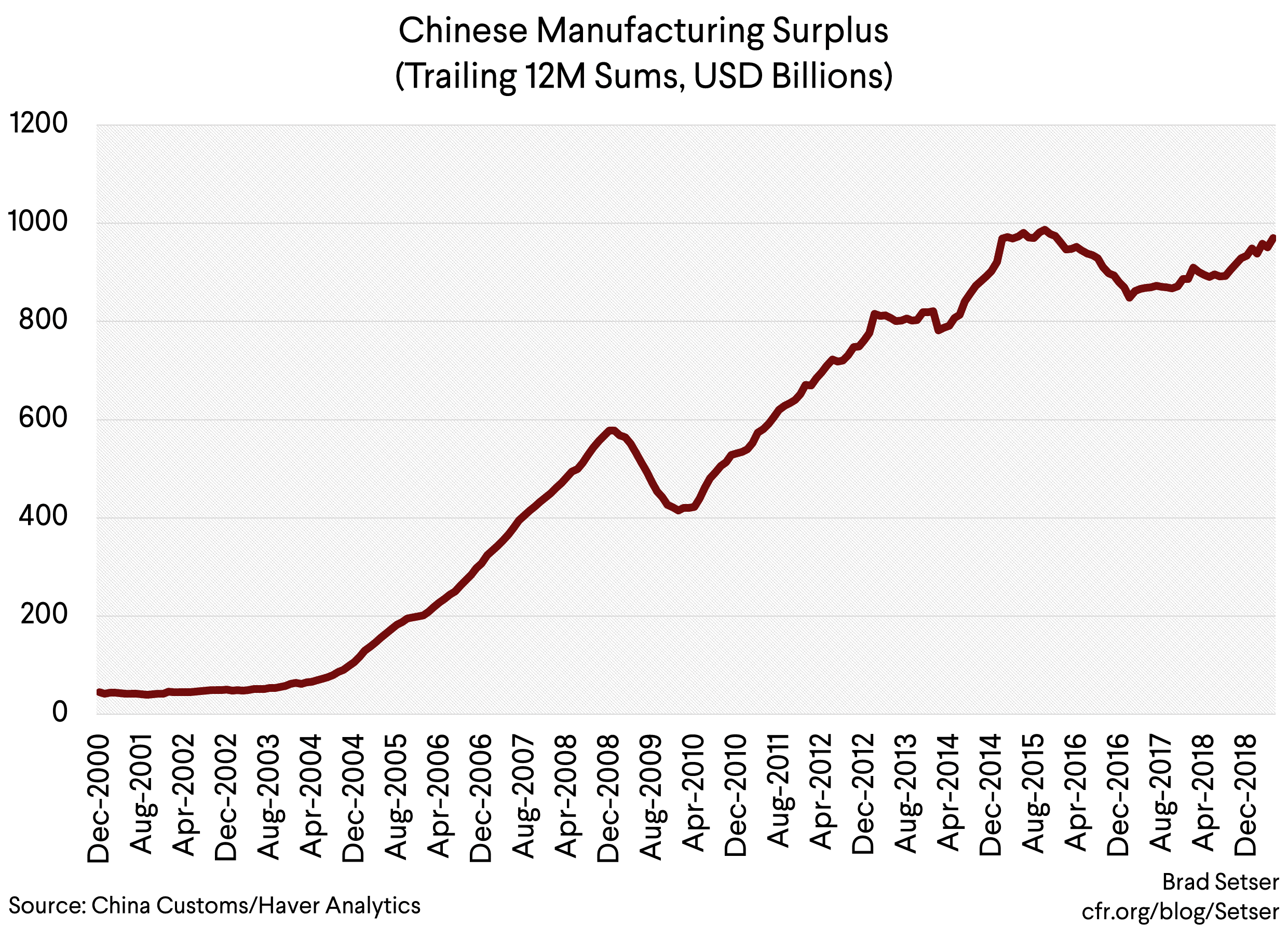

I am confident of one thing though. China’s cannot substitute for the U.S. as a source of demand for the world’s manufactures without a much bigger (and much more domestically disruptive) policy shift than has taken place to date.

Xi’s China, after all, still runs a trade surplus in manufactures every bit as big as the U.S. deficit in manufactures. And so far this year, that surplus has inched up, as imports have fallen by more than exports.

* Nominal import growth was inflated by higher semiconductor prices in 2017 and 2018, and it is now being held down by the fall in semiconductor prices (China at its peak imported close to $300 billion in integrated circuits, a sum comparable to its imports of oil and natural gas). In theory, it would be better to do all these calculations in real terms. But China doesn’t provide a real import series (as a level), and certainly doesn’t provide real import series that exclude commodities and processing imports. The IMF’s data on y/y real import growth (which includes commodities) shows that China’s imports significantly lagged its real growth rate in 2014 and 2015.