A Tale of Two Tariffs: China’s So Far Ineffective Tariffs on U.S. Manufacturing Exports

China’s tariffs on U.S. commodities? A huge impact. Especially on bilateral trade. But also on global U.S. exports of soybeans.

China’s tariffs on U.S. manufactures? By comparison, a relative modest impact.

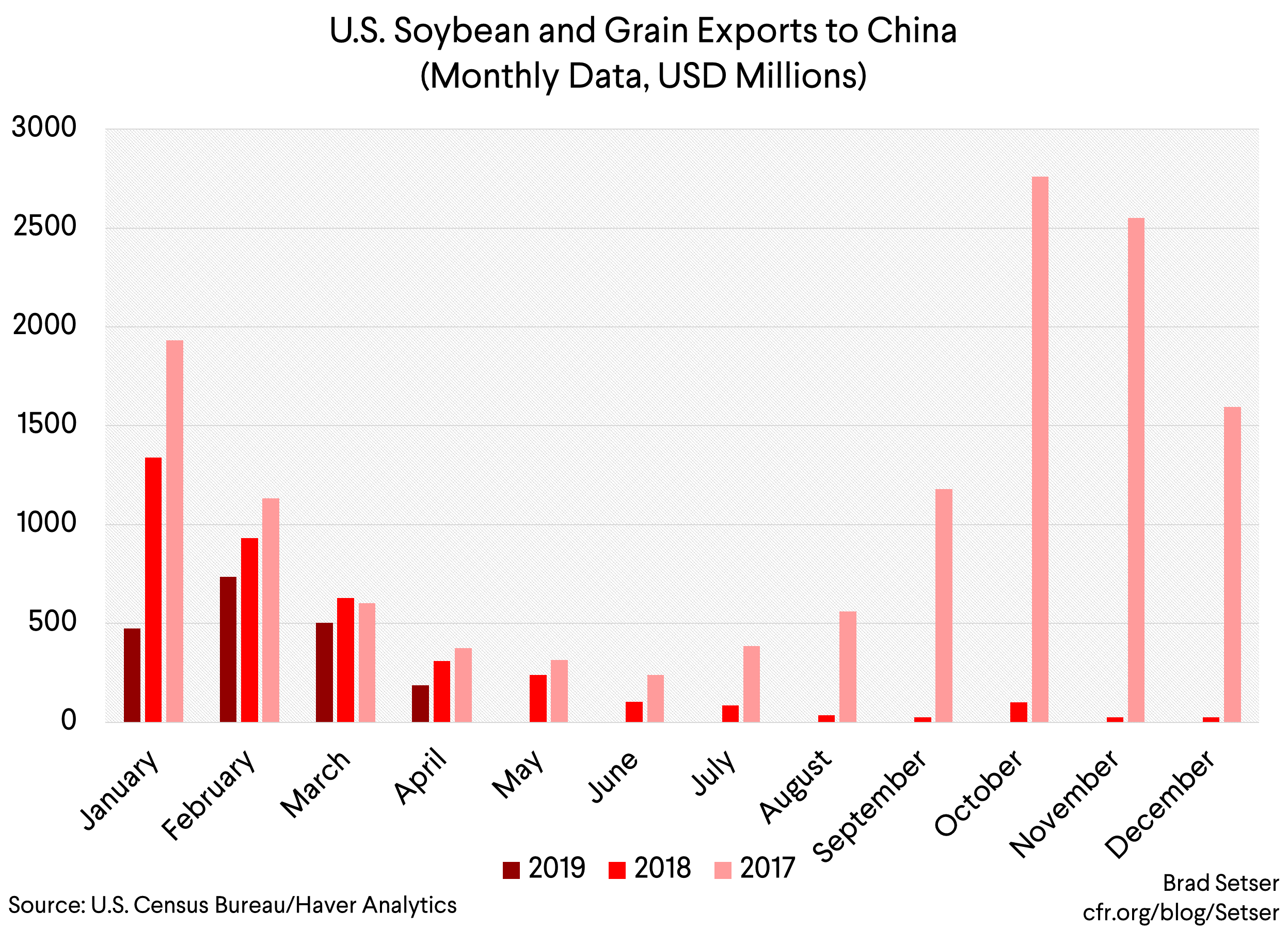

China’s soybean tariffs have—rightly—gotten a lot of attention. They have had a large impact not just on U.S. soybean exports to China, but on overall soybean exports. And, at least for a time, they pushed U.S. soybean prices below the global market price, as—without any purchases from China, Inc (and it really is China, Inc, think COFCO and Sinograin)—American beans had to sell at a discount to induce others to buy U.S. beans.

Soybeans traditionally have accounted for about 10 percent of total U.S. (goods) exports to China, so they alone have had a substantial impact on the overall trade numbers.

But, well, at least looking backwards, it seems that the success of China’s retaliation against U.S. soybeans isn’t actually all that typical.

In some other sectors, like oil, China’s tariffs reduced exports to China but not overall U.S. exports.

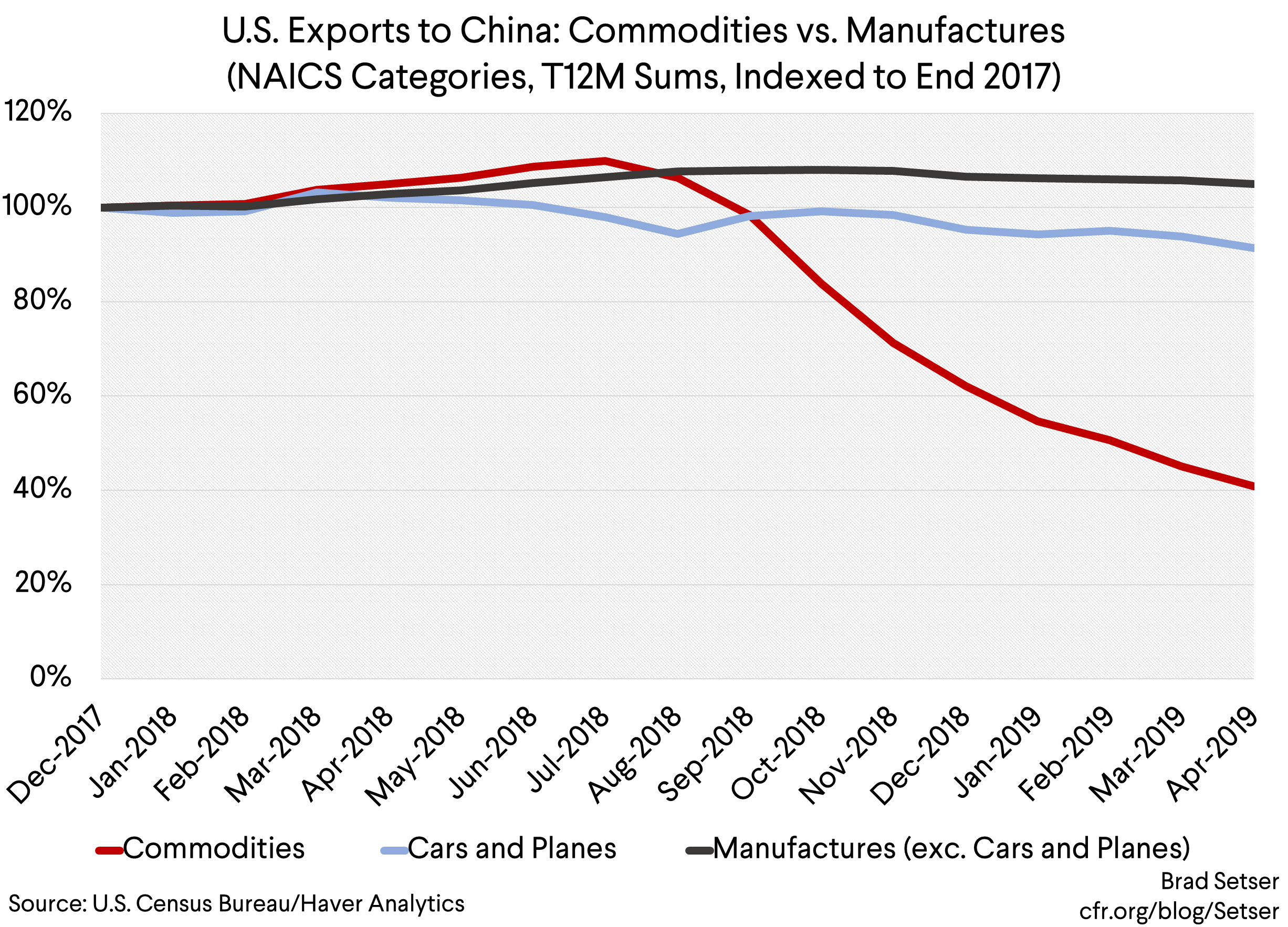

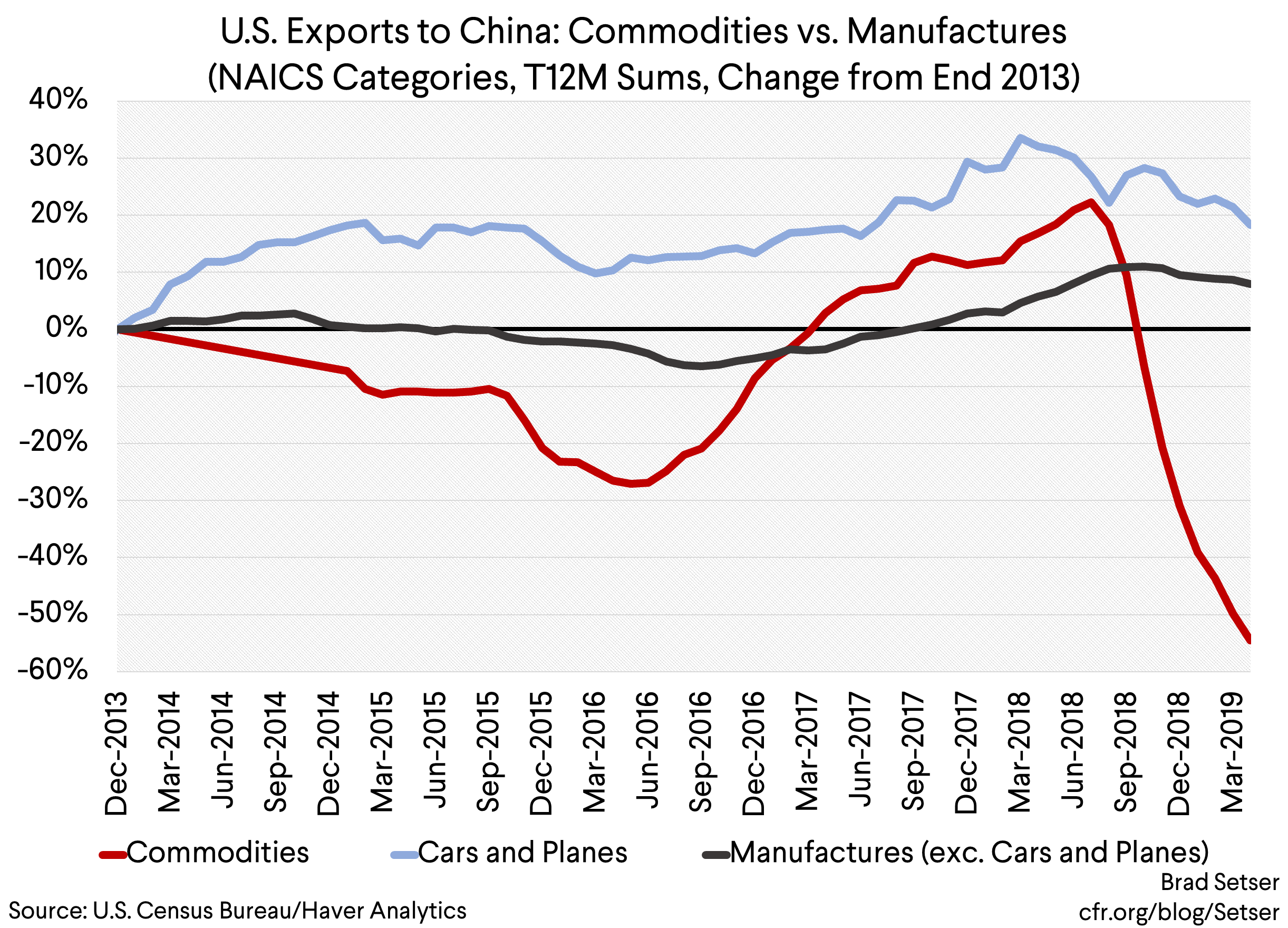

And China’s tariffs on U.S. exports for manufactures—together with a modest reduction in China’s tariffs on imports from others— haven’t had much of an apparent impact on total exports to China.* Somewhat to my surprise to be honest.

One set of tariffs (on commodities) has had a very large impact: exports are down over 60 percent, and the fall isn’t over (the trailing 12M sum is a slow moving indicator). And another (on manufactures) has had a more modest impact than expected.

Of course, China hasn’t put tariffs on all U.S. manufacturing exports: China, per Chad Bown of the Peterson Institute, has only put tariffs on 55 percent of U.S. goods exports and some major categories of U.S. manufactures (like aircraft) have been left out. But in the process of raising its overall effective tariff rate on U.S. exports from 8 percent to 18 percent last summer, it did put tariffs on a decent chunk of U.S. manufacturing exports (see Bown’s figure 3). So there should be some impact, and enough time has passed that there should be more of an impact in the numbers than is apparent at first glance. Or even at a second glance.

I challenge anyone to identify the date China’s raised tariffs on U.S. manufacturing exports just from the aggregate data on U.S. exports to China over the last 12 months (China’s 2015 slowdown actually jumps out more, for now)

To be sure, there has been some impact. That’s clear if you look at the changes in the trailing 3M sum of U.S. and European exports to China. There was a bigger drop off in American exports to China than in European exports to China last fall, though not one so big that it could not be, in part, a function of the dollar’s strength relative to the euro (the United States generally has under performed relative to Europe after the dollar’s 2014-15 appreciation).

And to be honest, the modest fall has been a bit of a surprise. I at least expected a bigger fall off in U.S. manufacturing exports to China.

Two potential reasons why.

One. China has exercised a bit of restraint, and held back on really restricting trade in some sectors to make sure it has targets to retaliate against should Trump broaden the tariffs further.

Two. China lacks good targets, as the bulk of its manufactured imports from the United States are in sectors where there isn’t (for now) a domestic Chinese alternative (widebody aircraft) and thus Chinese firms have to pay the tariff to get essential imports or in sectors where imports from the U.S. feed into China’s exports and thus Chinese tariffs would add to rather than reduce the shock to Chinese exports from the U.S. tariffs.

Of course, in reality, it can be a bit of both.

I don’t doubt for a second that China could bring U.S. auto exports (largely BMW and Mercedes SUVs) down to close to zero with a big enough tariff. And, as Chad Bown notes, China refrained from re-raising the tariff on U.S. auto exports when it responded to Trump’s move from 10 percent to 25 percent on the $200 billion tariff list earlier this month.

But, in other sectors where China might want to retaliate, it has already squeezed U.S. imports out of its market.

Suppose China wanted to retaliate against U.S. construction and mining equipment. After all, that’s a sector that produces a lot in electorally important parts of the United States. Even if Illinois itself isn’t a swing state, Caterpillar has a long supply chain—and Wisconsin produces a lot of mining equipment.

China though largely took away that target several years ago—U.S. exports of construction equipment to China are less than half their 2011-12 levels even before the trade war started.** China’s relatively high initial tariffs and its efforts to encourage “indigenous” production have already limited U.S. exports in some important sectors.

And well, it is also important to think a bit more about how different sectors in the U.S. economy responded to the fall in their exports to China.

Take three important sectors—soy, oil, and autos. In all three cases, China’s tariffs reduced bilateral trade. But so far, China’s retaliation only looks to have been far more effective—in an economic and political sense— in the soy market than in other markets.

The soy story is straightforward, and well known. Exports last fall more or less went to zero.

That’s consistent with many studies that find a high elasticity for tariffs. With an elasticity of 4, a 25 percent tariff would be expected to zero out trade.

But it is also consistent with a world where China’s state importing companies were told not to buy American. After all, with U.S. soy trading at a deep discount to Brazilian soy, buying American didn’t initially come as a financial penalty to Chinese importers (U.S. exporters, in this case, were arguably paying a large share of the tariff).

China then resumed (modest) purchases—with deliveries now expected for the next few months (unless China cancels the contracts).

But with a reduced Chinese pig herd, bad weather in parts of the Midwest, a shift by American farmers toward corn, and a decent harvest in the Southern Hemisphere, it seems likely that 2019 soy exports will be modest even if Trump strikes a new deal with Xi in Japan.

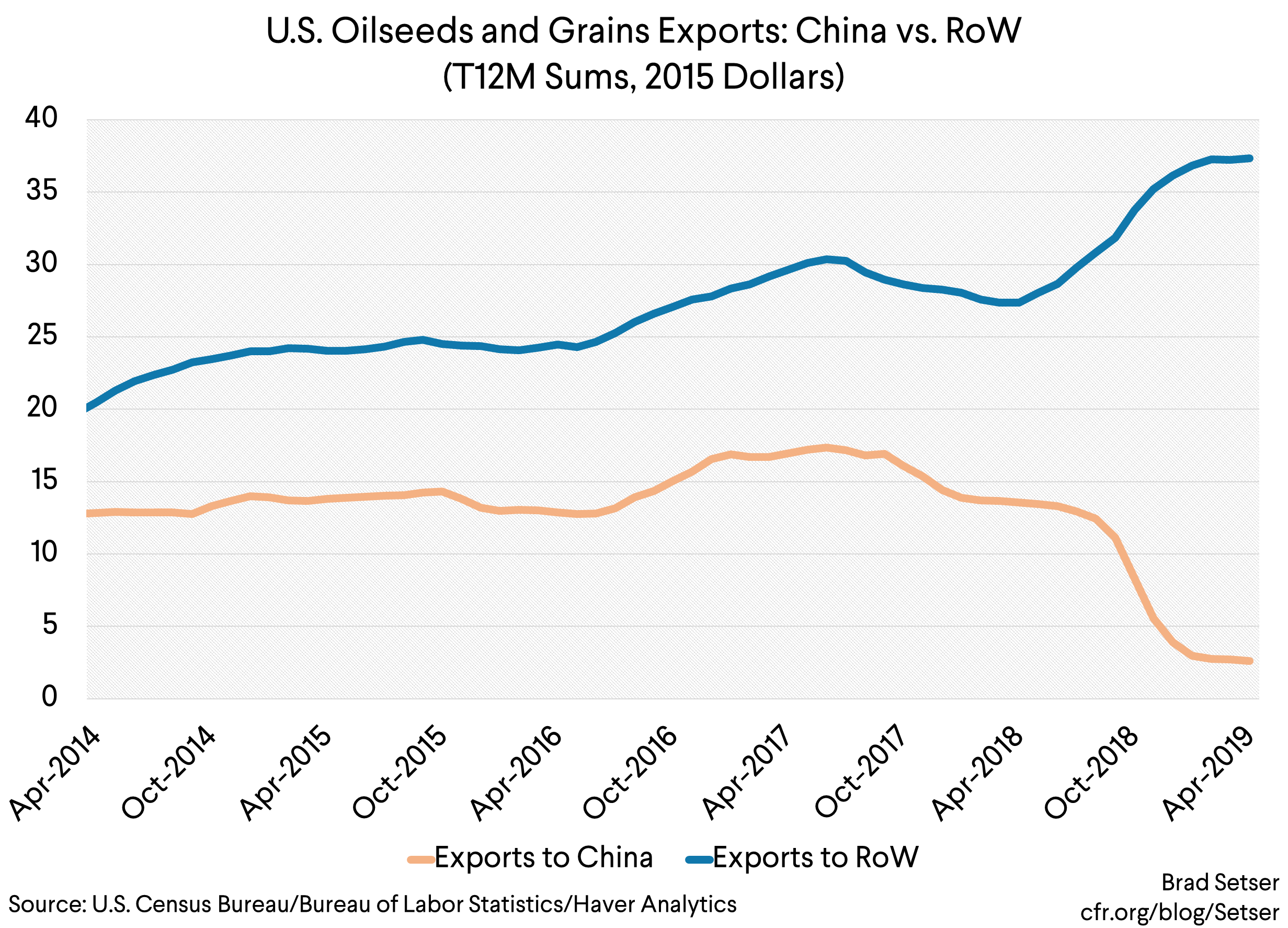

The reduction in China’s purchases of soybeans clearly hurt American farmers who weren’t able to make up for the fall in Chinese demand by exporting more to the rest of the world.

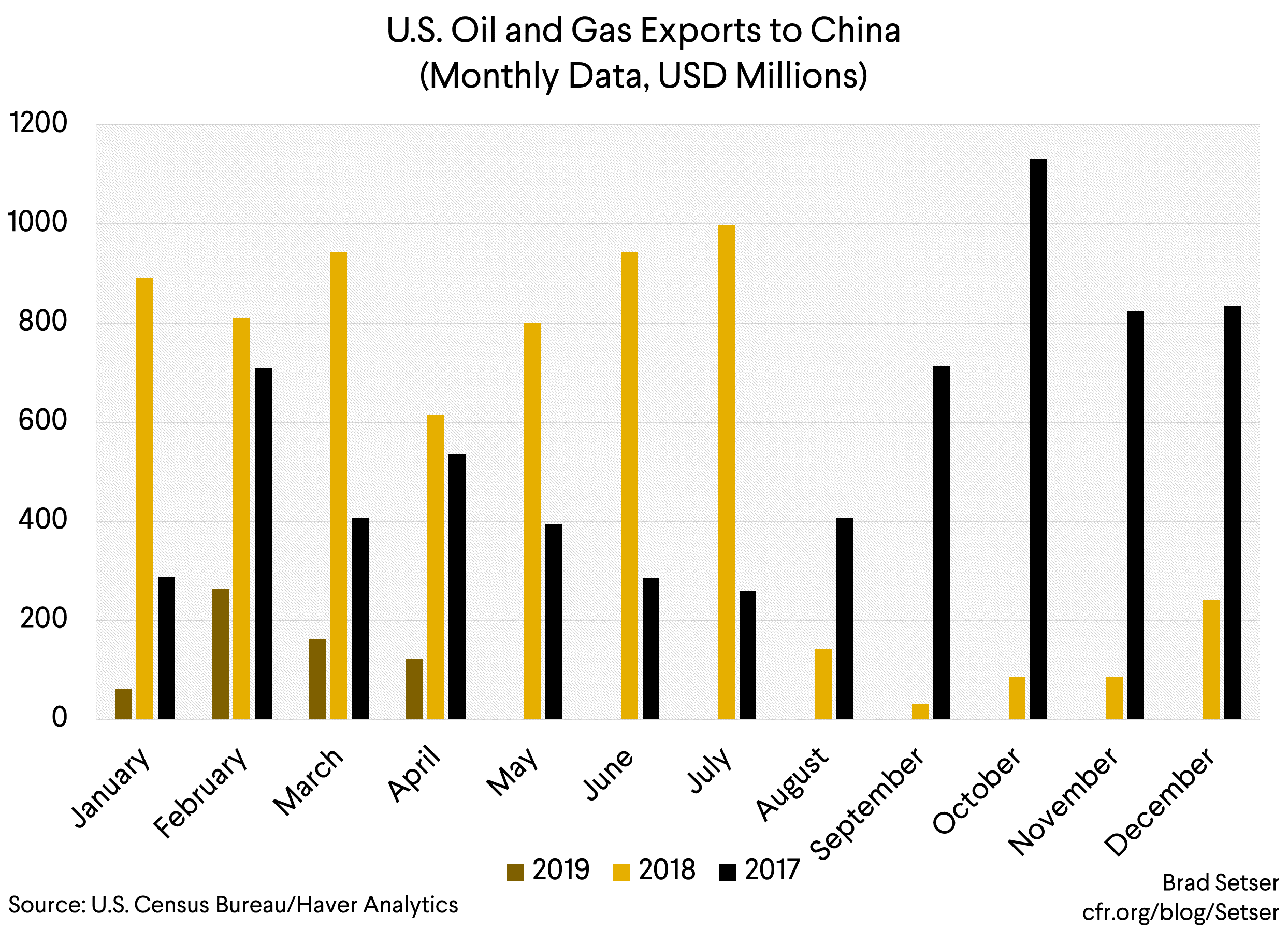

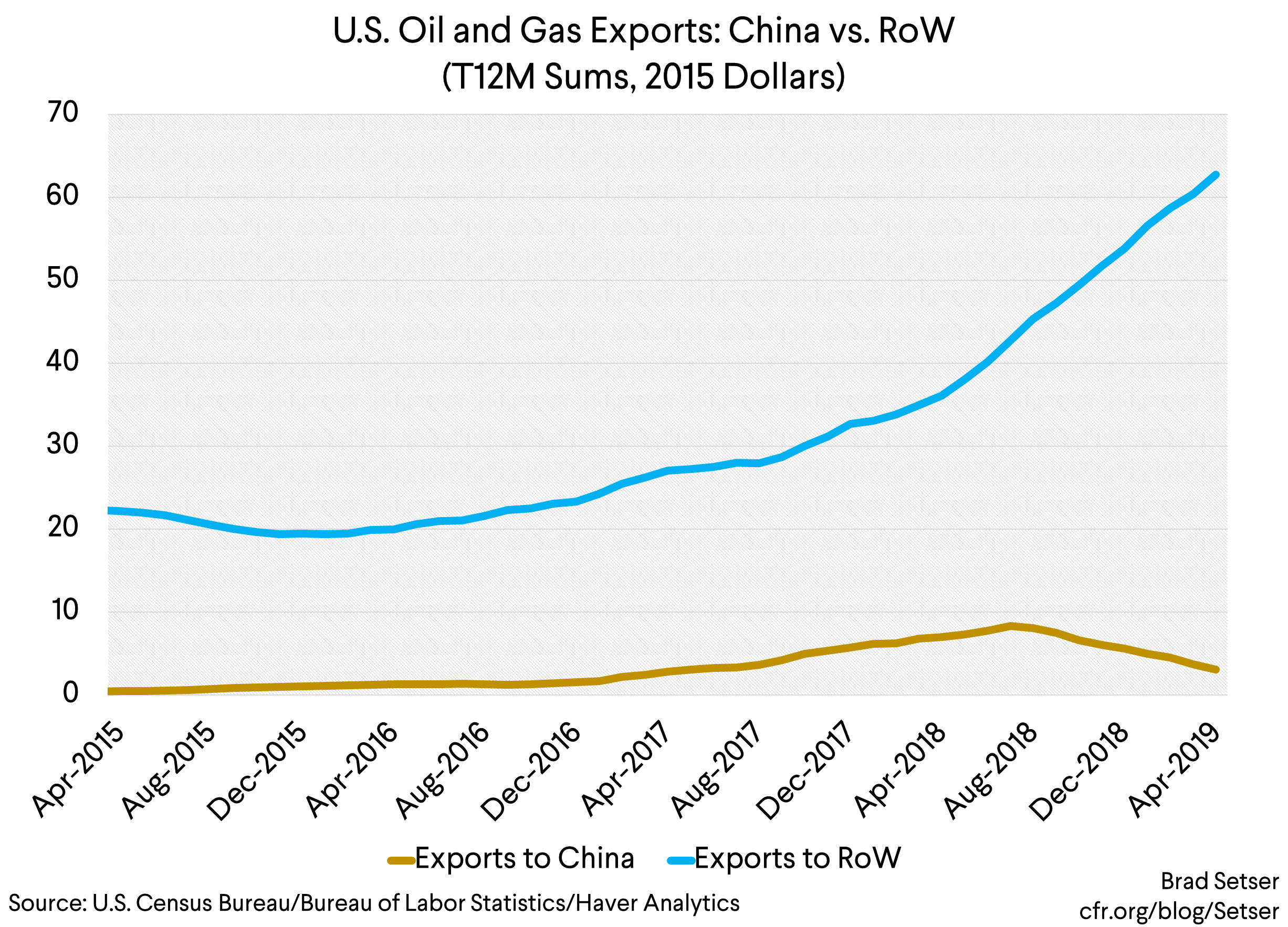

What about oil? Exports there also went to close to zero last fall, with only modest subsequent purchases.

But the fall in bilateral trade didn’t really have an impact on overall oil exports.

And the absence of exports to China’s market didn’t impede investments in the pipeline infrastructure needed to de-bottleneck the Permian. The tariffs diverted bilateral trade in oil away from China without impacting overall trade. That’s more or less what one would expect in a true commodity where it isn’t that hard to find alternatives to the Chinese market.

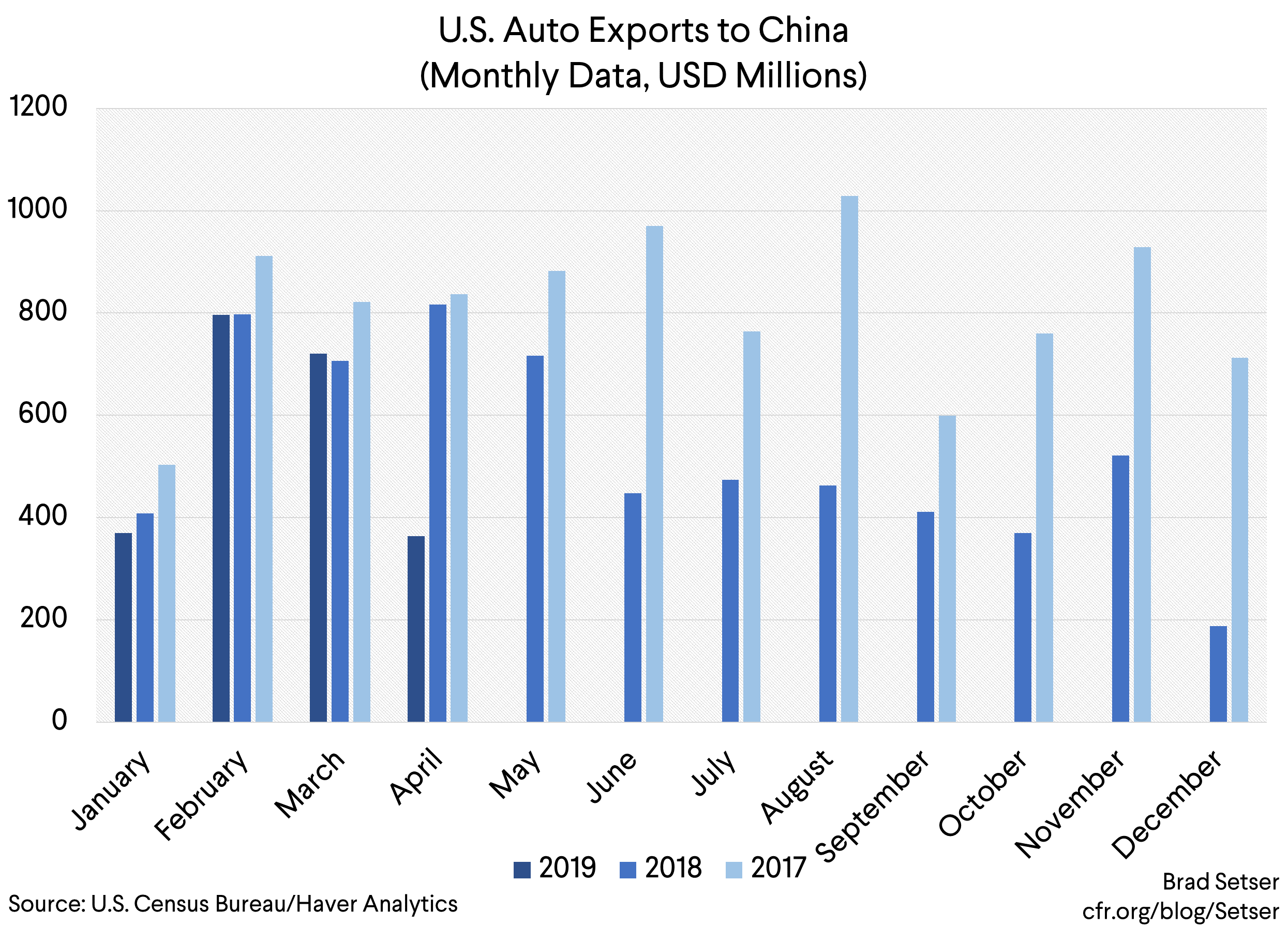

What about autos? In some ways, it is the most interesting case.

China’s tariff on autos did have an impact last summer and fall. U.S. exports to China fell significantly in the third and fourth quarter. They then rebounded in the first quarter, when China lifted the extra tariffs on U.S. autos as a goodwill gesture…

Exports here are largely Mercedes and BMW SUVs, so the data on trade by state provides an easy way to track this. Alabama and South Carolina both saw a fall in their exports to China in 2018. Alabama’s overall auto exports were down, while South Carolina’s overall exports look sort of flat.

But was there a broader impact on U.S. auto production? It isn’t clear.

Demand in the U.S. has been shifting toward SUVs, so it is possible that Mercedes and BMW were effectively able to offset their reduced exports to China by producing more for the U.S. market.

That indeed sort of seems to be what happened. BMW’s U.S. production was down a bit in 2018, in part because of a change over in a couple of key models last summer, though the fall in exports to China didn’t help.

But BMW says it is still planning to expand its output in South Carolina even as it plans to increasingly produce inside China for the Chinese market. And it doesn’t seem like the fall off in exports to China changed Mercedes‘ plan to shut down C series (sedan) production in Alabama in order to build more SUVs.

The counterfactual here is hard. As China’s SUV market grows and shifts towards electric vehicles—and as China liberalizes its JV requirement in autos to encourage BMW to produce more high value cars in China—I suspect that the United States‘ exports of autos (SUVs) to China will fall no matter what, as the German firms that now drive U.S. auto exports to China will increasingly “localize” their production for the Chinese market.

What’s the overall lesson?

Don’t equate changes in bilateral trade with changes in overall trade, or changes in total output. A lot depends on the sector.

There are occasionally surprises in the detailed data. To date, the overall fall in U.S. exports to China has largely been a function of the large fall in commodity exports. The implied elasticity on the manufacturing side so far looks modest (but I haven’t tried to disaggregate manufactures into those actually tariffed by China and those that have escaped so far).

And, well, the debate on the overall impact of China’s retaliation on the U.S. economy is sure to continue...

* Manufacturing exports come from the NAICs data, using all exports in the 300s. Commodities exports in the 100s (agricultural commodities) and in the 200s (oil and minerals).

** Exports of construction and agricultural equipment/ NAICS 3331 to China peaked at around $2 billion in 2012. They were running at between 0.6 and 0.8 billion a year before the trade war. Back in 2007, U.S. exports here were over $1 billion, so U.S. exports in this sector clearly haven’t grown with China’s economy. I am often a little frustrated by otherwise well informed commentators who have an out-of-date concept of what the U.S. exports to China. For example, it is common to argue that China might retaliate against U.S. construction equipment exports, and against U.S. switching equipment. But the U.S. has been running a substantial trade deficit with China in both construction equipment and telecommunications networking equipment for some time. In an exchange of tariffs in those sectors, China has more to lose (Do look at the end use data, which is easy to use).