The Return of Big Chinese Surpluses (And Large U.S. Deficits)

Global trade imbalances are, once again, largely the result of Chinese and American trade imbalances. China’s surplus has increased even as the pandemic has reduced global trade, as has the U.S. deficit.

For all the talk of Sino-American decoupling, the broad pattern of global trade—at least the unbalanced bit of global trade—is remarkably simple right now.

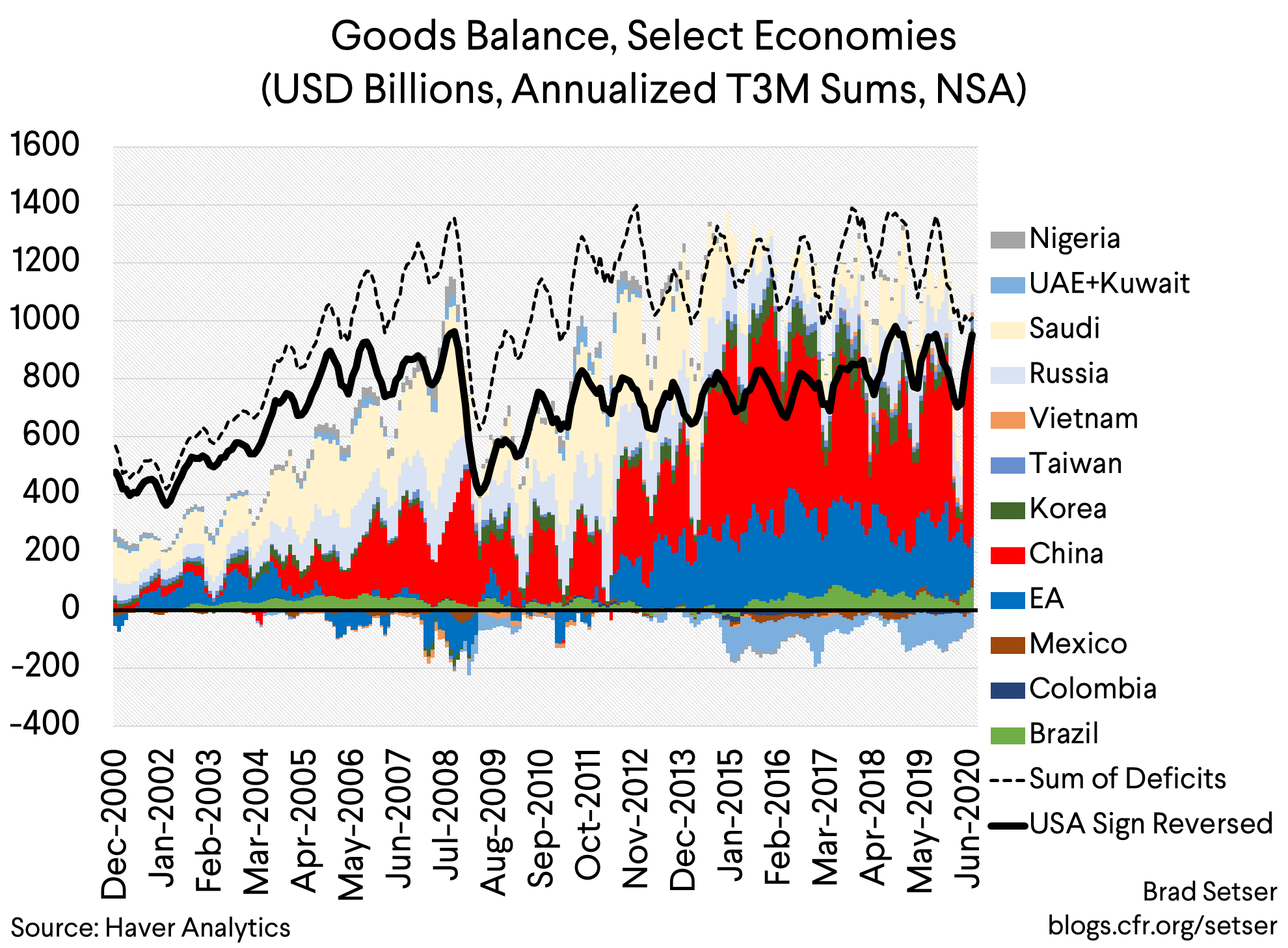

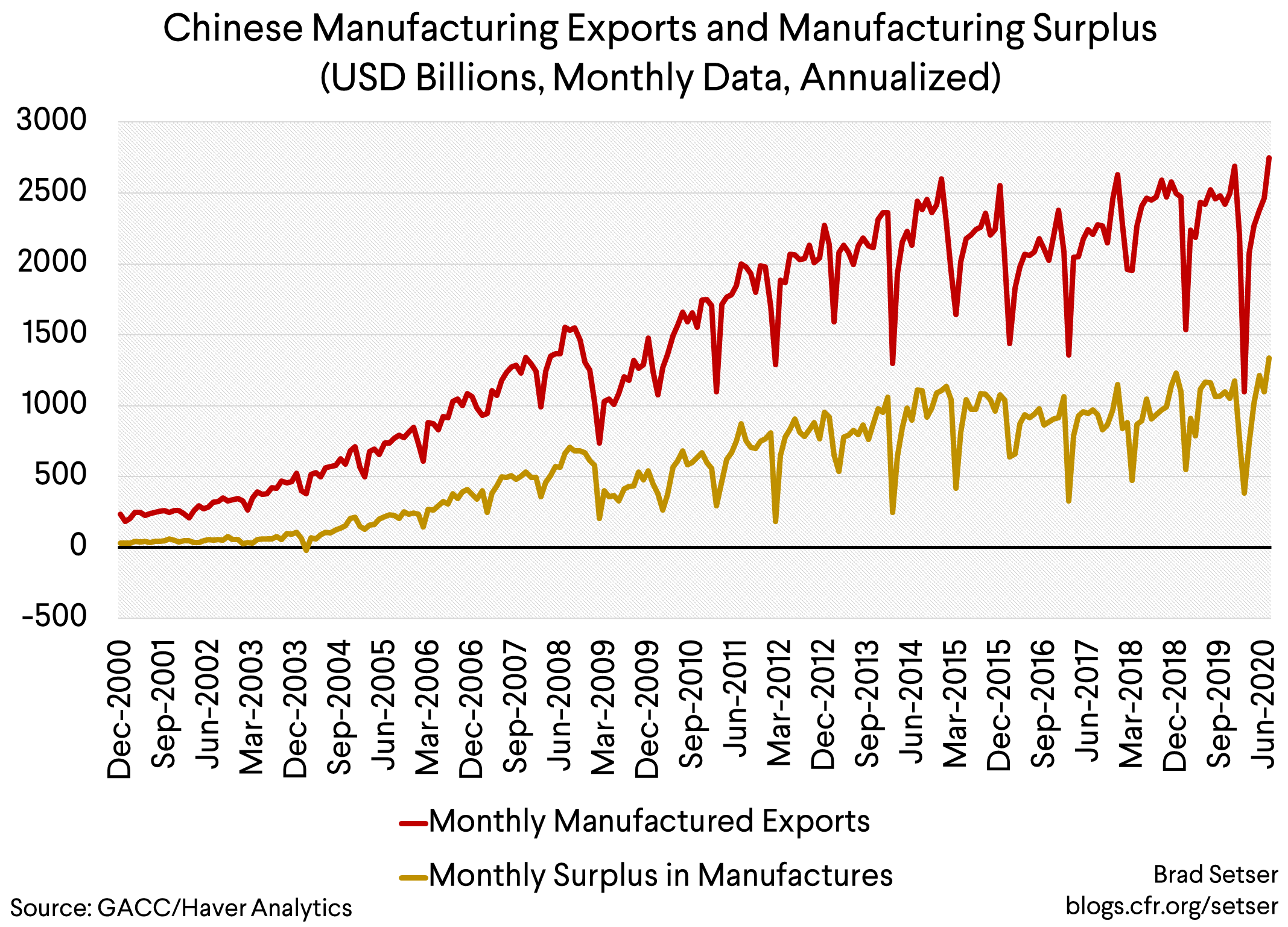

On the surplus side of the ledger there is China, along with a few other Asian producers of the manufactures. Keith Bradsher has reported that China’s share of global exports reached a record in the second quarter, at nearly 20 percent. Continued strength in exports has helped China post monthly (goods) surpluses of around $60 billion in July and August.

And on the deficit side of the ledger there is… the United States. The U.S. trade deficit (goods and services) topped $60 billion in July, its highest level in many years.

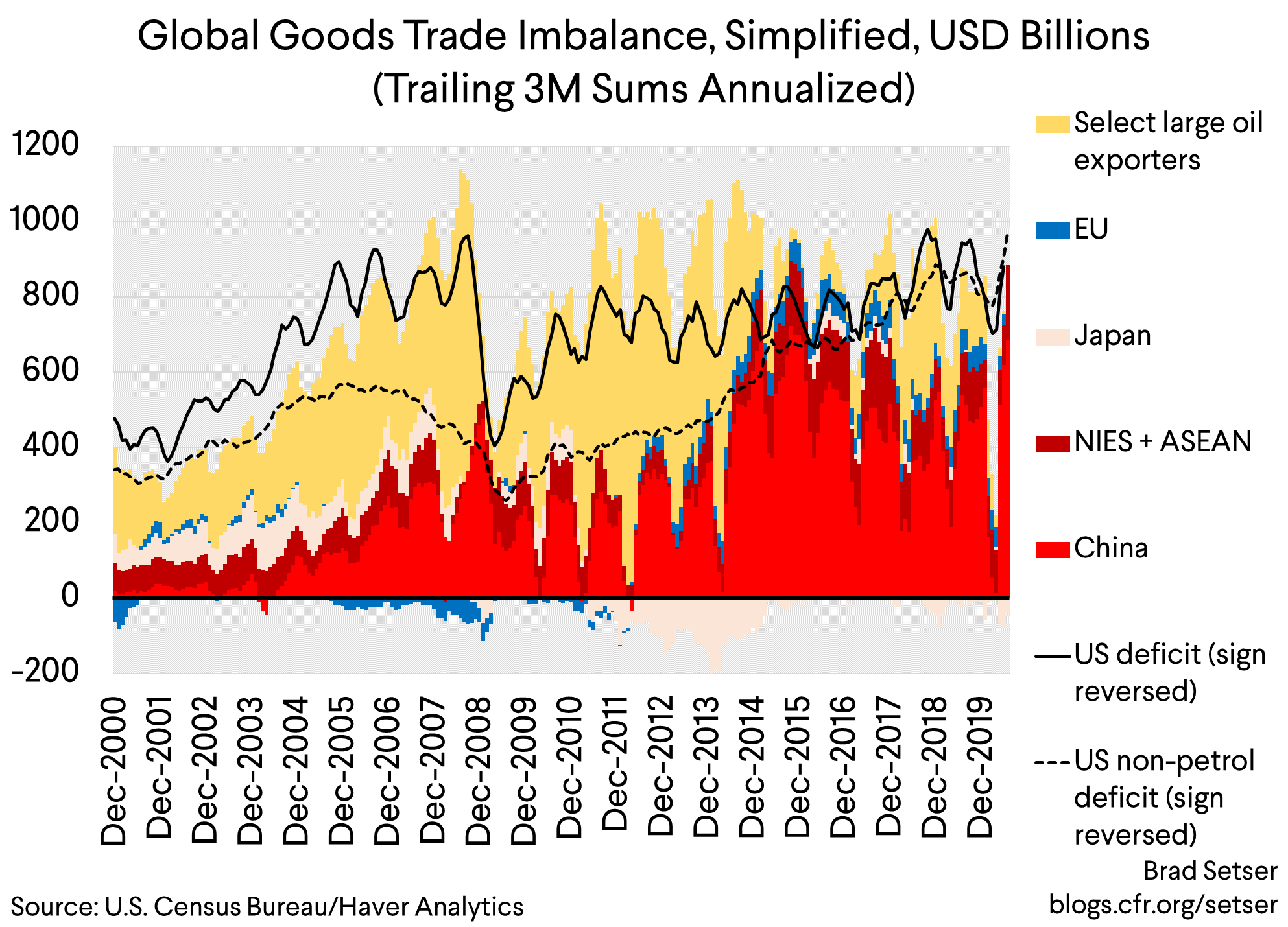

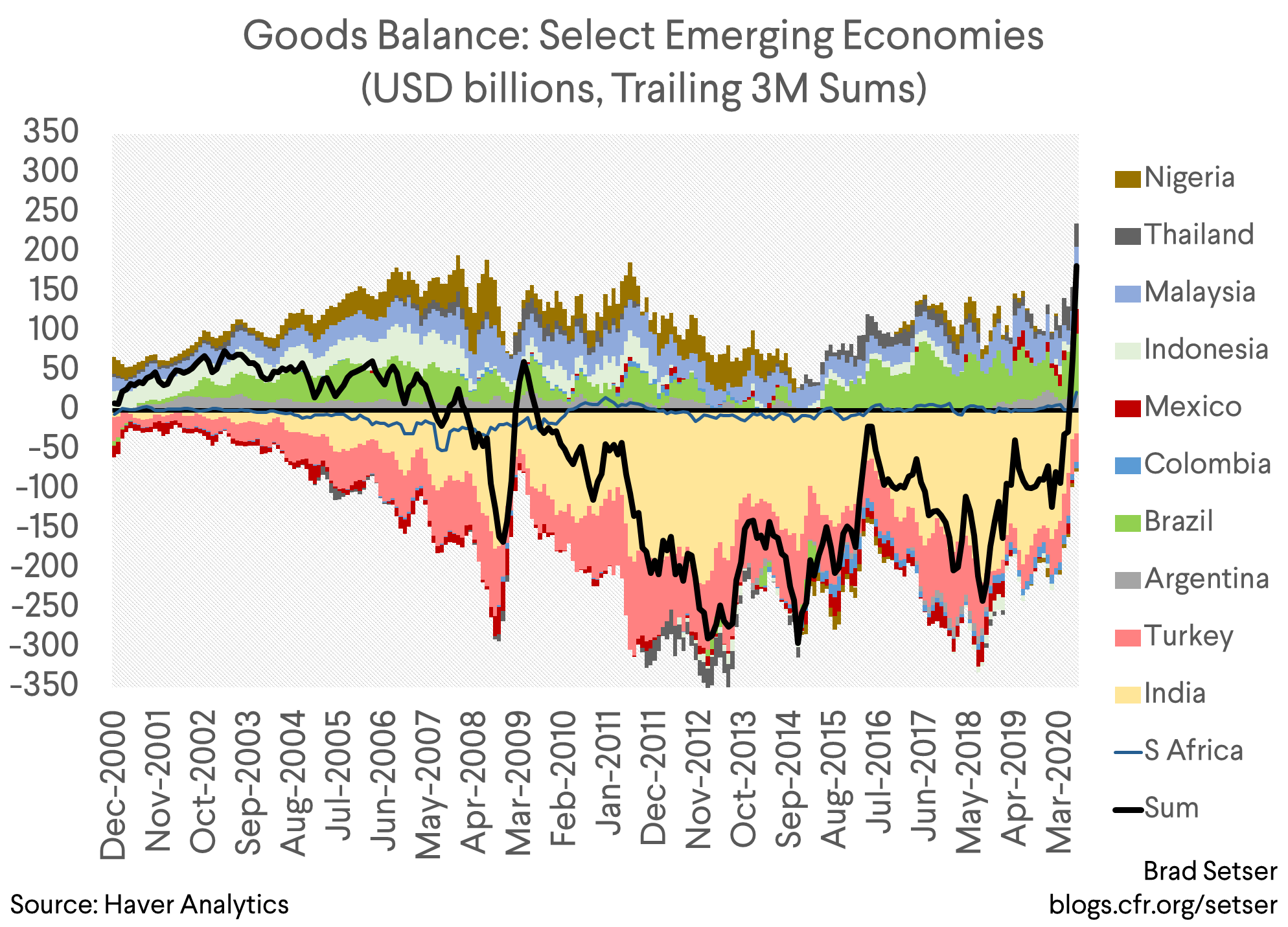

It is thus now more clear than ever that world trade in goods* doesn’t add up without China’s $1 trillion surplus in manufactures on one side, and the United States $1 trillion deficit in non-petrol trade on the other side.

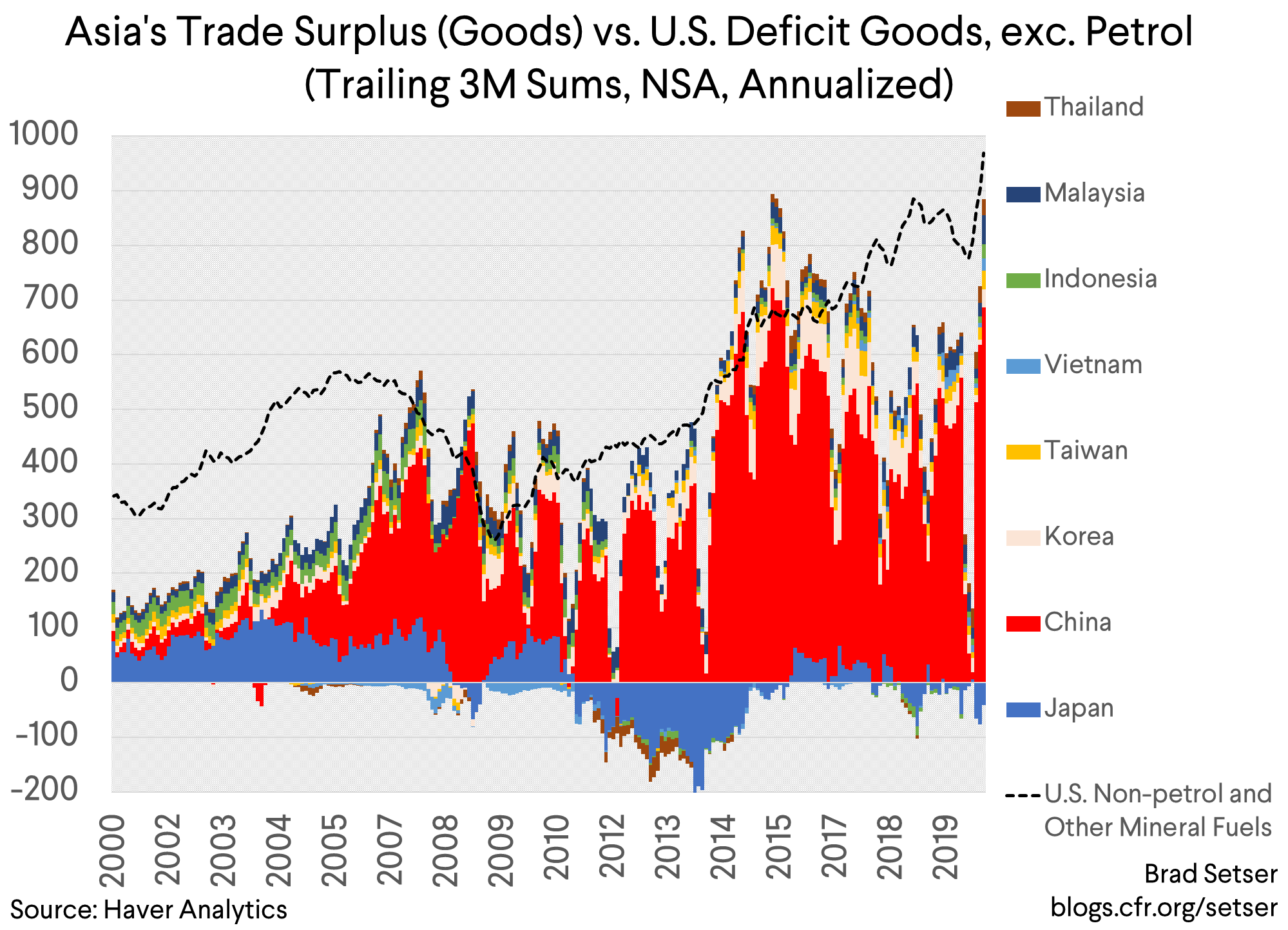

The need for a U.S. deficit to offset Asian surpluses (and Asian surpluses to fill the U.S. deficit) has to a degree long been true. What’s striking though is that the pandemic has led to a compression of most other trade imbalances, so almost all that is left now is the big Chinese surplus (from q2 on) and the equally big U.S. deficit (from q2 on).

There are of course other trade flows—Europe runs a surplus with the United States that is offset in part by its deficit with China, Australia runs a surplus with China that is offset by a deficit with the United States and so on. But the EU’s surplus has shrunk with reduced trade (the EU’s surplus is also much smaller than that of the euro area).

A set of emerging markets that used to run deficits when oil prices were higher now run surpluses.

And with oil in the 40s (or below), oil is close to the balance of payments breakeven of most oil exporters (many of whom have been forced to cut back)—though those oil exporters with lots of accumulated assets have higher break-evens and have been borrowing against those assets to fund ongoing deficits. The deficit in the Gulf Cooperation Council (GCC countries) now helps to offset surpluses in Europe and a lot of oil-importing emerging economies.**

But at the end of the day, a high frequency plot of global goods trade imbalances now is essentially dominated by China on one side, and the United States on the other. ***

Who would have predicted this a year ago?

These are “real” imbalances too—over the last 12 months, China generated a $1 trillion surplus in manufactures off around $2.3 trillion in exports. In July, China generated a $110 billion surplus in manufactures off $230 billion in exports—so even counting imported parts, China is getting close to exporting $2 worth of manufactures for every manufactured good it imports. And the United States roughly $1 trillion U.S. deficit in manufactures comes off around $2 trillion in manufactured imports, so the U.S. exports a dollar in manufactures for every two it imports.

There are of course reasons why the return of the Sino-American trade imbalance might be temporary.

China’s dominance of personal protective equipment manufacturing for example has helped push up its goods surplus. The pandemic created a temporary boom in electronics demand to facilitate remote work (and school) as U.S. consumption shifted away from domestic services toward imported hardware, playing into another Chinese strength.

And China’s overall current account surplus ($120 billion, or just over three percent of China’s GDP) has been increased by the fall in travel. That has cut into China’s reported services deficit.

But there is also a policy story that suggests the renewed Trans-pacific imbalance could be durable.

As Michael Pettis has noted, China has responded to the pandemic with policies that support firms and production—and been very restrained in its direct income support for consumers and households.

The United States, by contrast, provided a lot of support for households—at least initially.

China’s fiscal response is generally estimated to be far smaller than in 2009, while the United States’ response (to date) has been bolder. That policy differential—plus China’s ongoing exchange rate management which has kept the yuan relatively weak—could reinforce the return of pre-2008 style trade imbalances…

*Services trade is a different matter—the real bit is way down because of tourism and the “tax avoidance” bit is heavily distorted by the Irish-shoring of global IP and that data is in any case only available with long lags

** With more data from q2 the deficit in Saudi Arabia and the Gulf should become more pronounced—

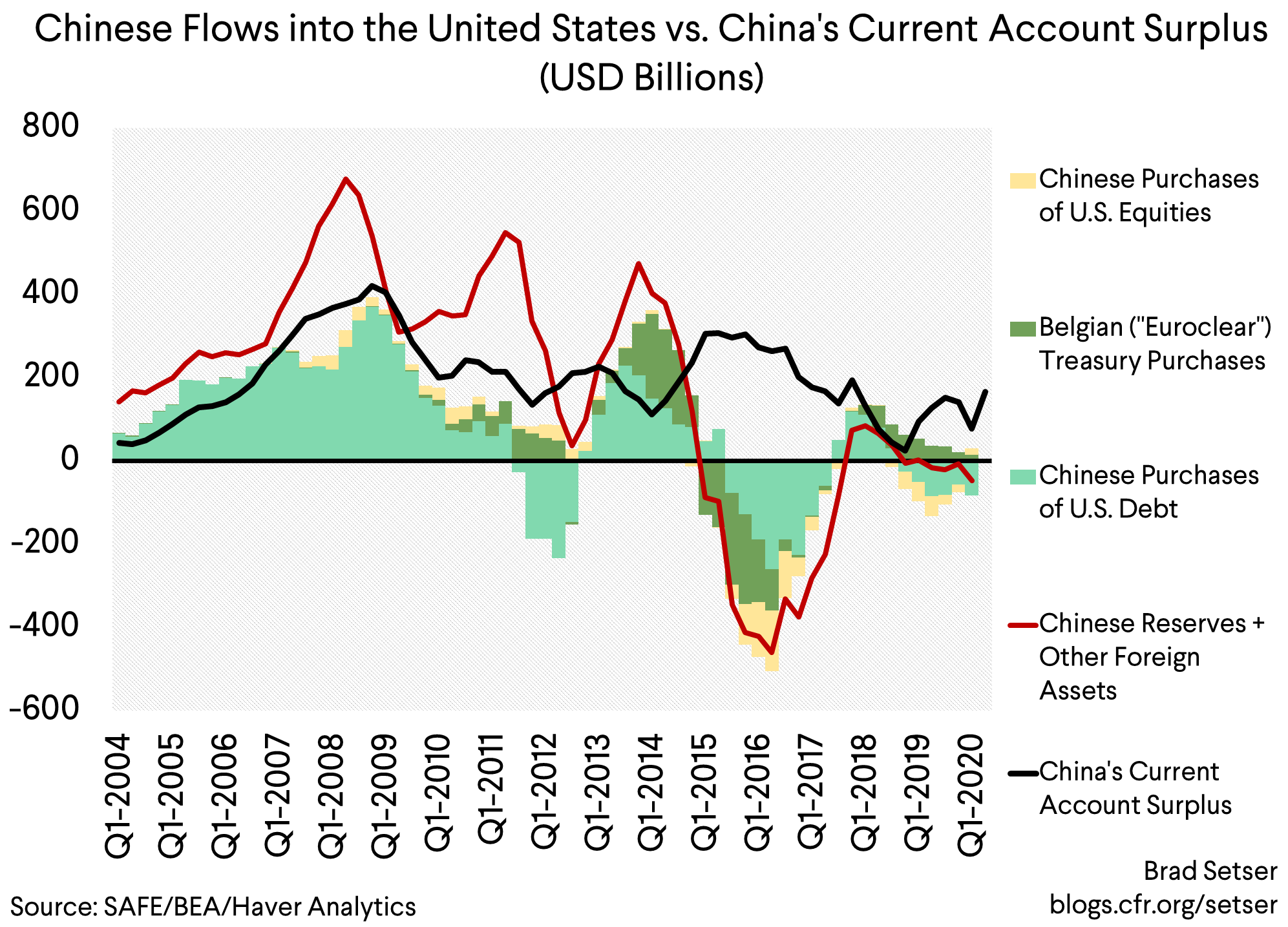

*** Of course these trade numbers raise another question, namely what is the financial flow story that goes together with these imbalances. In the past, China’s reserve growth and the resulting inflows into the U.S. fixed income market would have provided the answer. But with no apparent Chinese reserve growth, the trans-pacific flow of finance is harder to track than the trans-pacific flow of goods.