Did the Dollar’s Position as the Leading Reserve Currency Help Hold Treasury Yields Down This Spring?

Foreign Treasury sales, including large sales from reserve managers, made the Fed’s job harder, not easier, in March.

It is common to attribute the fall in U.S. interest rates over the course of the last few months to the fact that the dollar is the world’s leading reserve currency.

The dollar after all rallied during the course of the corona crisis even though the Trump Administration’s response to the virus didn’t avoid a major outbreak. And the dollar rallied back in late 2008, even as the United States emerged as the epicenter of the global financial crisis.

But it isn’t at all clear to me that low U.S. rates are a function of the dollar’s position in the international monetary system. All the advanced economies now have low rates—with many borrowing at rates well below that of the United States. Japan, Germany, France, Sweden, Great Britain, and Canada all pay less than the United States to borrow for ten years. Not all of these countries are home to a major reserve currency.

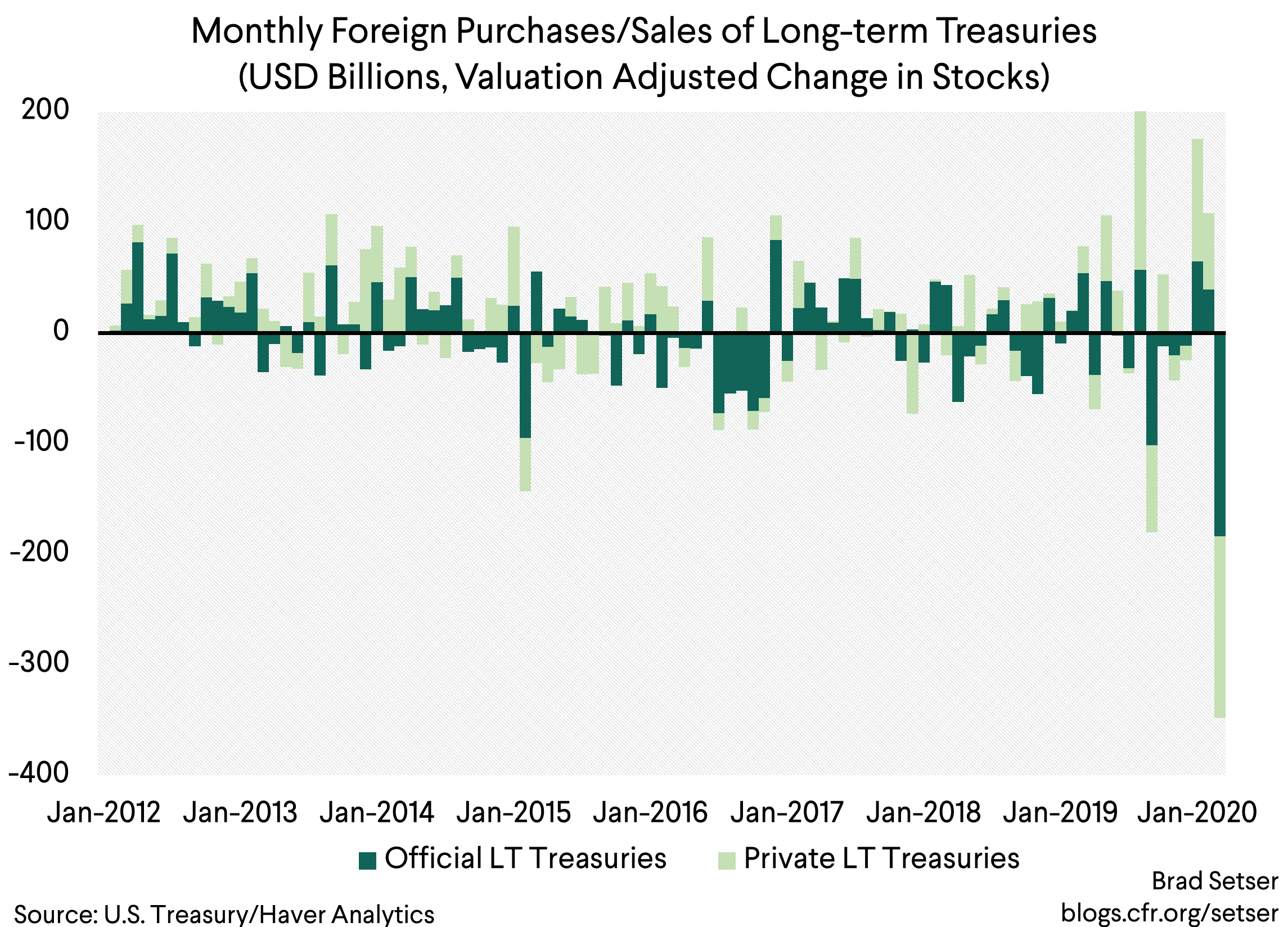

In some important ways the dollar’s global role actually has made it harder not easier for the Federal Reserve to bring down U.S. interest rates during the COVID-19 crisis. Foreign investors sold at least $300 billion of Treasuries in March—at a time when the Treasury market was otherwise in turmoil (Listen to the Odd Lots podcast with Josh Younger for the details). The extreme size of the Fed’s purchases was a function, at least in part, of the need to counteract foreign outflows, as the world’s reserve managers pulled funds out of the Treasury market.

The precise meaning of the phrase, “the dollar is the world’s leading reserve currency” isn’t actually all that clear.

Taken literally (and I am known to do this) it means that the dollar is the currency of denomination for the bulk of the world’s reserves.

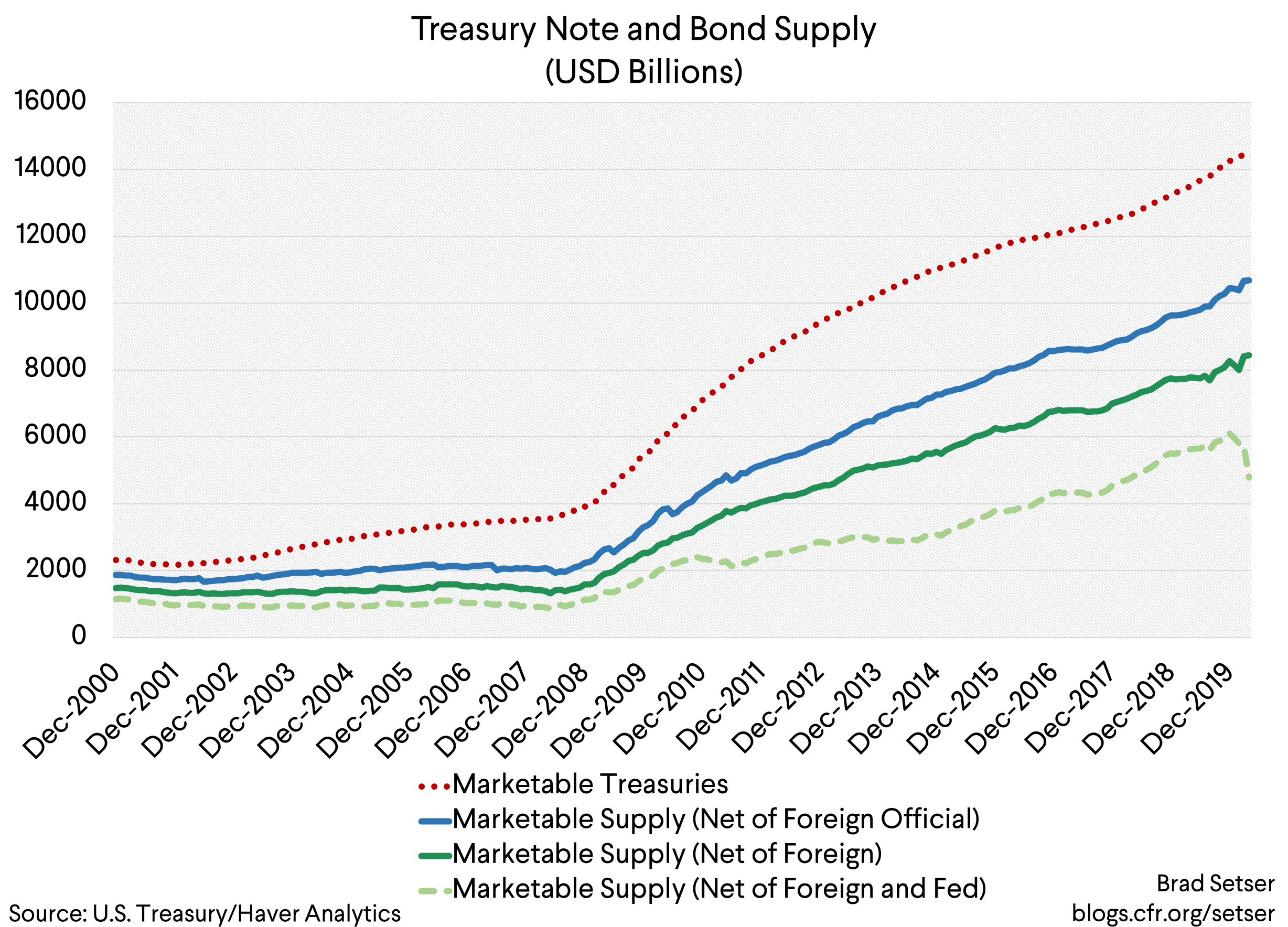

But just looking at the dollar’s share of global reserves can be misleading. It is one thing to be the currency of choice of the world’s reserve managers when reserves are static, and quite another to be the currency of choice when foreign exchange reserves are growing by a trillion or more a year (as they were back in 2007 and early 2008) and yet another when reserves are shrinking at a comparable pace. Reserve managers demand for Treasuries is a function of the pace of growth in their reserves just as much as the currency share. Demand for dollars—and Treasuries—from the world’s reserve managers shrank radically in March as the world’s emerging markets sold off record quantities of reserves to stabilize their own markets.

Those who argue that the dollar’s reserve currency role stabilizes the Treasury market often use the phrase “the dollar is the world’s leading reserve currency” to mean more than simply the dollar reserves held by central banks around the world. They also allude to the fact that the dollar is the currency of choice for a lot of transactions around the world that don’t involve the United States. The dollar in other words isn’t just the world’s leading reserve currency, it is also the leading global currency used in private transactions.

Fair enough. But the connection between the dollar’s private use around the world and large financial inflows into the United States isn’t always straightforward.

That should be obvious from the fact that the dollar is used heavily for private transactions in countries like Argentina, Turkey, and Lebanon yet none of these countries holds significant quantities of foreign exchange reserves (nor do they hold a significant number of Treasuries; see the major foreign holders table).

In fact, I am pretty sure there is a negative correlation between the countries that have the most dollar reserves and the countries that make the most use of the dollar for internal transactions. The big holders of dollars tend to hold dollars in their public reserves in part because their private actors are quite comfortable holding their own currency, and sustaining large trade surpluses thus tends to require the public sector accumulate dollars.*

This all matters because the U.S. data on international capital flows from March highlights a set of deep puzzles, puzzles that will keep academics busy for years.

The dollar rallied in March.

Yet the dollar’s rally came even as foreign investors sold massive quantities of Treasuries.

That strongly suggests the dollar’s rally wasn’t because of flows into the Treasury market.

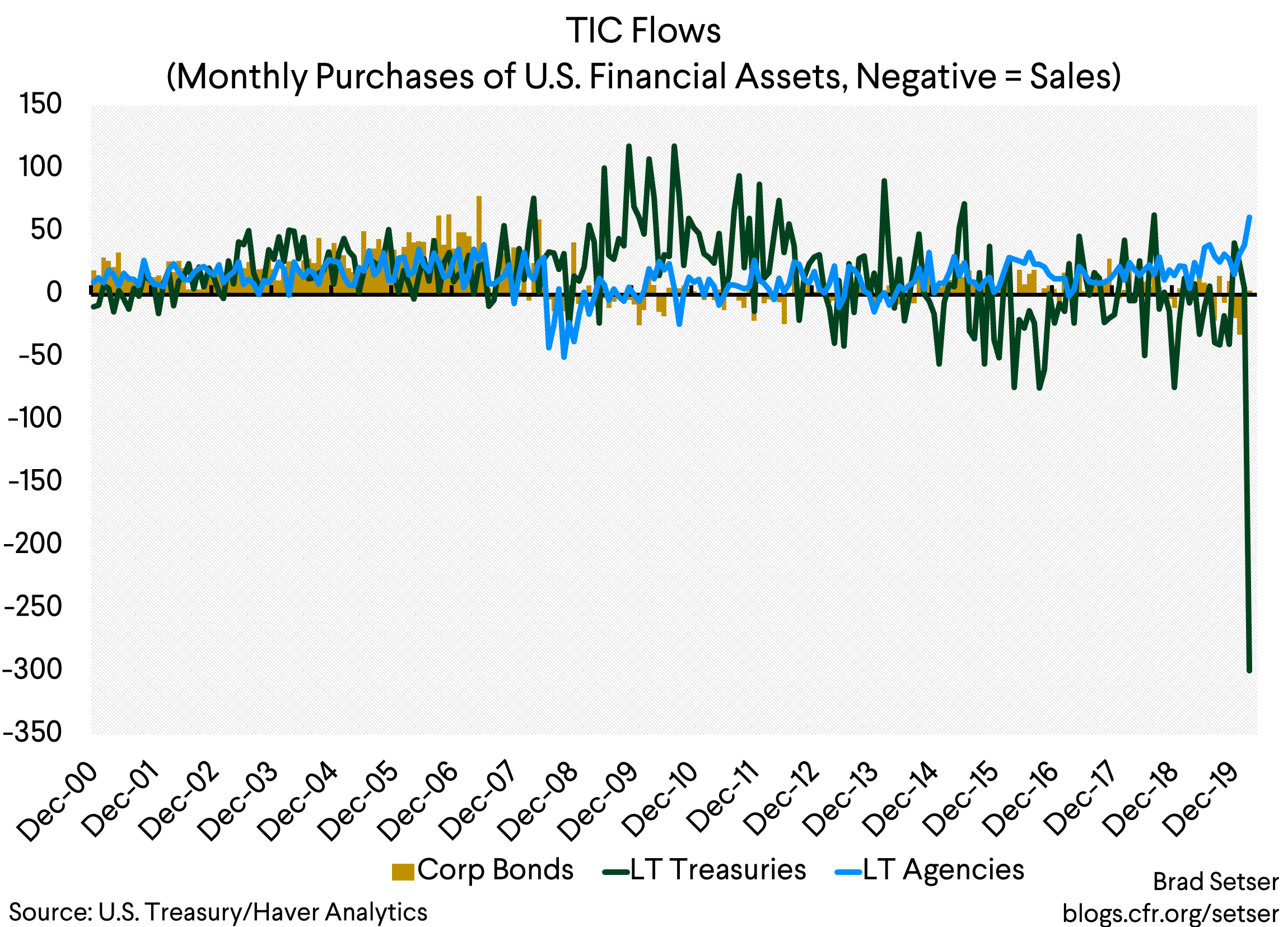

It is almost impossible to overstate the scale of foreign sales of Treasuries in March. The U.S. data on transactions with foreign residents—which isn’t perfectly accurate—shows over $300 billion in sales of long-term Treasuries. The “holdings” data shows $400 billion or so in sales after changes in reported holdings are adjusted for likely valuation changes (per Citi’s Daniel Sorid; Treasury yields fell in March because of the Fed, which pushes the market value of existing holdings up so the reported stock of Treasuries should have risen absent large sales). Those are huge sums.

Sales on that scale would normally be expected to push Treasury yields up, not down. As, I think, happened in early March.

March can be divided into three periods.

In the first period, the expectation of Fed rate cuts pulled long-term Treasury yields in the expected direction. Ten-year yields fell from 1.5 percent in mid-February to 55 basis points (0.55 percent) on March 9.

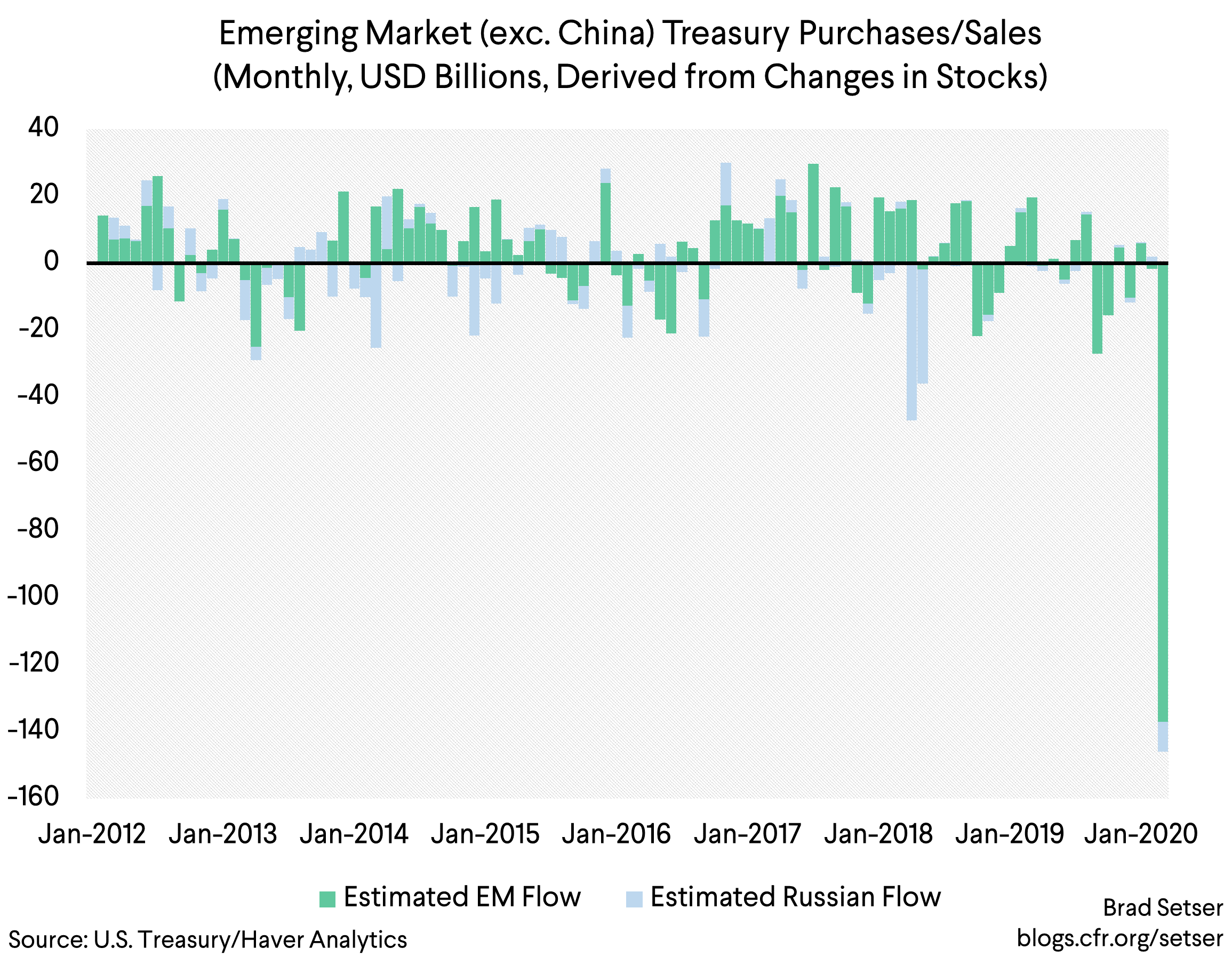

In the second period, the market panicked about the impact of COVID-19. American investors ran out of any kind of risk and ran into cash and short-term Treasury bills (through money market funds). Banks pulled back from market making in longer dated bonds (see Justin Baer of the Wall Street Journal for the gory details). And foreign investors pulled massive sums out of emerging economies, forcing emerging economy central banks to sell reserves and ultimately Treasuries to help limit the impact of these financial outflows. That is why the weekly data on custodial holdings at the New York Federal Reserve showed a rapid fall in central bank’s Treasury holdings.

So after initially falling, longer-term yields started to rise, moving from around 55 basis points on Monday March 9 to a high of 1.15 percent (115 basis points) on March 18.

There is an argument that the Treasury market is so deep and liquid that it can naturally absorb even large sales of Treasury from big reserve managers. But that wasn’t happening—the private market had seized up even as central banks were selling. See Josh Younger, Jeffrey Cheng and David Wessel:

“As one of the world’s most heavily traded assets, Treasuries should have been easy to sell. But a lot of other market participants were trying to sell amid the uncertainty about COVID-19: asset managers were seeking to raise cash to meet redemptions; foreign central banks were selling Treasuries to acquire dollars to manage capital outflows and exchange rates; banks needed to fund draws on their revolving corporate credit facilities; and investors were selling to rebalance their portfolios after the sharp fall in equity prices. Though there were clearly many buyers, there were not enough to meet this supply. Whereas in the past dealers would warehouse the excess until a match could be made, they ran up against a difficult combination of regulatory constraints on the size of their portfolios and extreme price fluctuations even over short time periods. This was worsened by the fact that the bonds being sold were predominantly off-the-run, another source of volatility that dealers struggled to manage. Extreme price fluctuations led to additional illiquidity.”

And then, of course, the “Desk” stepped in ** and bought far more in the last bit of March than the rest of the world sold over the full month. It started the week of March 16 by buying $40 billion a day, and then increased the pace of purchases to $70 billion a day on March 18. Total March purchases of notes and bonds topped $450 billion, and the Fed topped that with over $900 billion in additional purchases in April…

Yields on the ten-year note fell back to around 0.7 percent.

Now in principle the combination of large Fed purchases in the month of March and large foreign sales could mean one of two things.

The Fed could have, through its large purchases, pushed yields down and in effect induced foreigners to sell (and hold cash instead, or buy Agencies or some such). If the Fed is buying more than the Treasury is issuing, someone else by definition must be reducing their exposure. The ECB’s big purchases back in 2015 and 2016 for example induced foreign investors to sell some of their euro-denominated bond holdings (see Cœuré).

Or foreign selling could have pushed up yields, and in effect helped create the pressure that led the Federal Reserve to start buying to assure the smooth functioning of the Treasury market.

In this case, I don’t think there is any real doubt as to what happened—yields were rising through mid-March even as the weekly custodial data was moving down. The Fed was forced step in….

But there is enough technical complexity here that I have no doubt Ph.D. dissertations can (and hopefully will) be written on the topic.

No matter—

One thing should be clear. Distress in emerging markets led to a massive liquidation of reserves by emerging markets—and thus large Treasury sales. Setting China aside, I get around $150 billion in sales by the major emerging markets (this can be safely assumed to all come from their central banks).

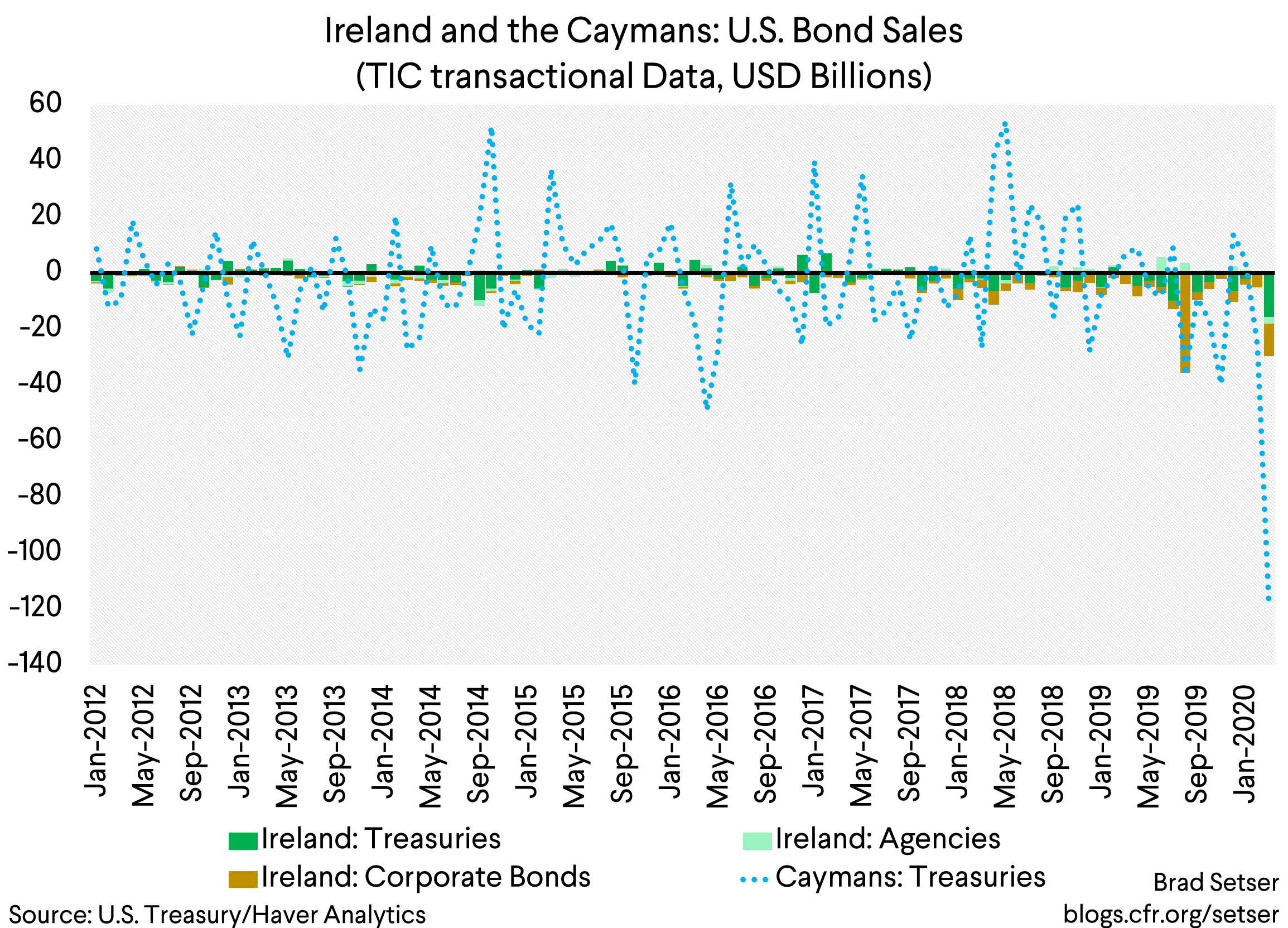

And some of the distress that Josh Younger described among private market participants (the cash futures basis trade done by some large hedge funds***) also likely impacted the Treasury International Capital data. I at least don’t have an alternative explanation for the large sales by entities in the Caymans.****

I have little doubt that reserve manager buying did hold down yields (by reducing the supply of Treasuries available for private buyers as reserve demand was so large) from 2002 to 2008 (see Warnock and Warnock). But the impact of reserve manager demand for dollar’s isn’t a constant (Ernie Tedeschi has a great visualization of this; I hope he updates it soon). When reserve managers sell, they put upward pressure on Treasury yields. And that made the Fed’s job harder not easier in March.

* Countries with a large M2 to GDP tend to have current account surpluses, likely because a large domestic deposit base is correlated with a savings glut. This is something the IMF didn’t put enough weight on in their (problematic) composite reserve metric. China and Turkey aren’t equally under-reserved even if that is what a blind application of the IMF’s metric implies.

** Jay Powell may go down in history as one of the Obama Administration’s most consequential legacies, as without his appointment to the Board of Governors by the Obama Administration (to clear a Republican Senate) he probably doesn’t get picked as Fed Chair by Mnuchin, and with a different Fed chair the financial history of the last few months may have played out very differently…

*** “The trade works like this: when Treasury futures are more expensive than the underlying cash security, traders buy the “cheap” security and short the “rich” futures to pocket the difference. A short is a bet that the price will fall. On its own, however, this is not very profitable because discrepancies tend to be very small—only a few cents per $100. So, to juice the returns on their investments, traders purchase the securities with mostly borrowed money. In a way, the cash-futures basis trade polices the relationship between the derivative and the underlying bond by keeping prices in line.” (Cheng, Wessel and Younger).

**** The actual size of Cayman sales/hedge fund deleveraging though isn’t clear. The transactional data shows over $100 billion in sales from the Caribbean (mostly the Caymans). The reduction in holdings by Cayman based entities in the typically more accurate holdings data is more modest—though still significant.