Shadow FX Intervention in Taiwan: Solving a 100+ Billion Dollar Enigma (Part 1)

Taiwan’s central bank, unlike most central banks, doesn’t disclose its position in FX derivatives. It really should. There is good reason to think its undisclosed exposure is quite substantial.

By experts and staff

- Published

Brad W. SetserCFR ExpertWhitney Shepardson Senior Fellow

Brad W. SetserCFR ExpertWhitney Shepardson Senior Fellow- Guest Blogger for Brad Setser

This is the first post in a series[1] on Taiwan’s life insurers and their private & sovereign FX hedging counterparties. It’s the product of a collaboration with S.T.W[2], a market participant and friend of the blog. Printable versions of entries in this series will be available in pdf format on his site (Concentrated Ambiguity).

Introduction

For the better part of the last 20 years, analyzing the ups and downs of FX interventions and the concomitant rise of global FX reserves has been an integral part of understanding FX and sovereign bond markets. Central banks from countries as diverse as Japan, China, Saudi Arabia, Russia, Switzerland, Hong Kong, India, and South Korea have each assumed FX exposures north of USD 400bn at the beginning of 2019.

What unites these, and practically every other here unmentioned country, is that the most comprehensive information about their activities in currency markets can be found in a standardized form created by the IMF, the ‘Data Template on International Reserves and Foreign Currency Liquidity’ (IRFCL). The template was initially developed in 1999 and is a key component of the Special Dissemination Standard (SDDS), to which IMF members subscribe in order to “provide[s] a standard for good practices in the dissemination of economic and financial data”.[3] As of today, 95% of all IMF member countries (including all G20 members), subscribe to the SDDS and accept the responsibility to produce an IRFCL.

The value of the reserve template lies in the provision of detailed ‘Foreign currency resources’ and ‘Foreign currency drains’, which includes positions in FX derivative markets, pledging or lending of FX reserves, as well as other contingent exposures—all factors which are not readily revealed by the headline FX reserve series alone. Because of the disclosure of these details, it is usually possible to understand even complicated FX maneuvers conducted by central banks.

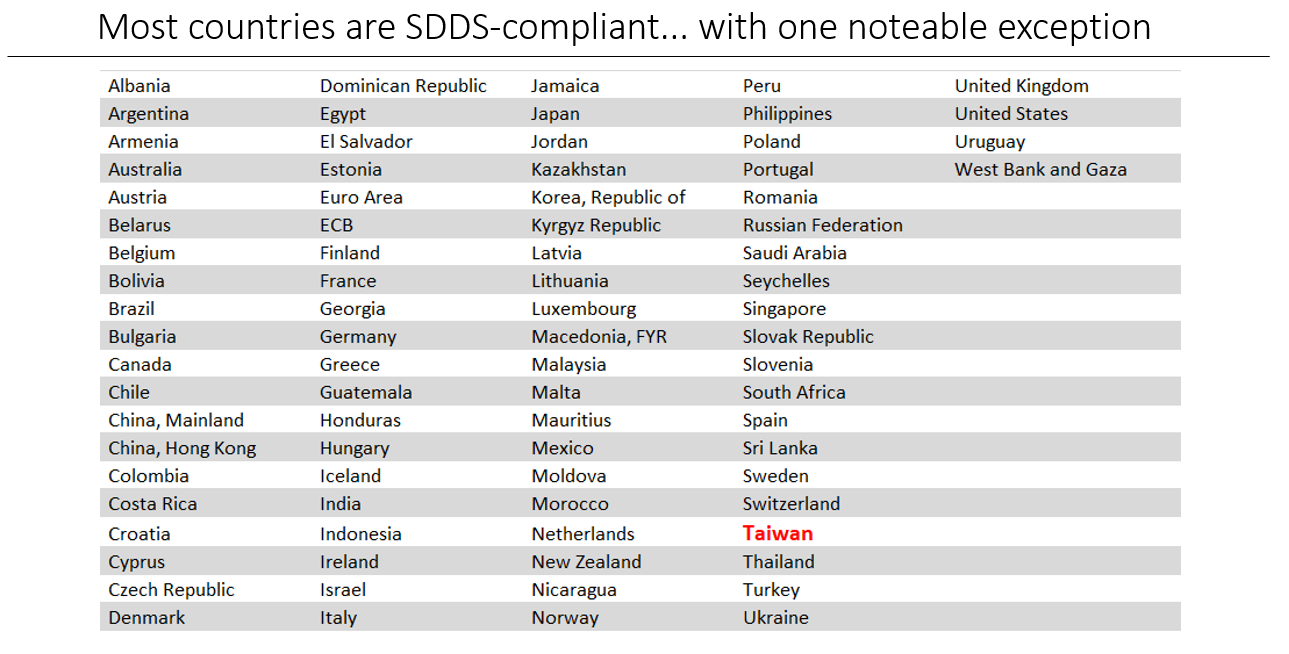

Over 70 of the world’s largest countries release an IRFCL, with one notable exception: Taiwan. As with any question, there exists an obvious, but ultimately dissatisfying answer: Taiwan is, for historical reasons, not an IMF member and as such has not officially adopted the Special Dissemination Standard.

The website of Taiwan’s central bank (the CBC) nevertheless prominently features an ’SDDS button’ on its main page[4], highlighting that Taiwan voluntarily ”provides most information on the financial and external sectors of the Republic of China” according to IMF established guidelines. Upon another click, it furthermore provides a ’Summary Page on Observance’ of the SDDS[5], and assigns itself full compliance in all tested dimensions (coverage, periodicity and timeliness) regarding the foreign sector, which includes the ’international reserves’ category.

Given these assurances, it is all the more striking that Taiwan does not follow IRFCL disclosure standards for its FX reserves. The CBC clearly has the technical capacity to compile the necessary information, as it is a straightforward process based on information covered by any central banks’ internal accounting systems.

Market participants are broadly aware of the absence of the data covered by the reserve template in Taiwan, as are foreign policy makers—including the U.S. Treasury Department which, in its biannual FX reports to Congress regularly bemoans the lack of insight Taiwan provides.[6]

This series of blogs will attempt to answer whether Taiwan simply does not consider the release of an IRFCL as particularly informative, or if there are deeper reasons why it has so far objected to releasing more detailed information about its reserves. The road to an answer will be bumpy and will require, among other things, a deep dive into Taiwan’s life insurance industry and its cross-border transactions, a detailed look at the demand and supply in TWD FX derivative markets as well as non-standard CBC FX operations. This resulting body of work will ultimately lay out evidence that suggests one of the largest FX derivative interventions any central bank globally has so far undertaken.

[1] The Council on Foreign Relations takes no institutional positions on policy issues and has no affiliation with the U.S. government. All views expressed on its website are the sole responsibility of the author or authors.

[2] Contact at [email protected]

[3] Quoted from the 2013 IRFCL manual, available from the IMF here.

[4] See its English website here.

[5] The English version is available here.

[6] Treasury’s latest FX report is available here. The request for Taiwan to release more granular FX intervention data is in footnote 20 on page 41. Earlier versions, for instance the Spring 2017 report, contain more explicit requests. Especially pertinent are the sections starting on page 19—in fact, this introduction is based on Treasury’s assessment set forth there.