Is Puerto Rico Back on a Path Toward Debt Sustainability?

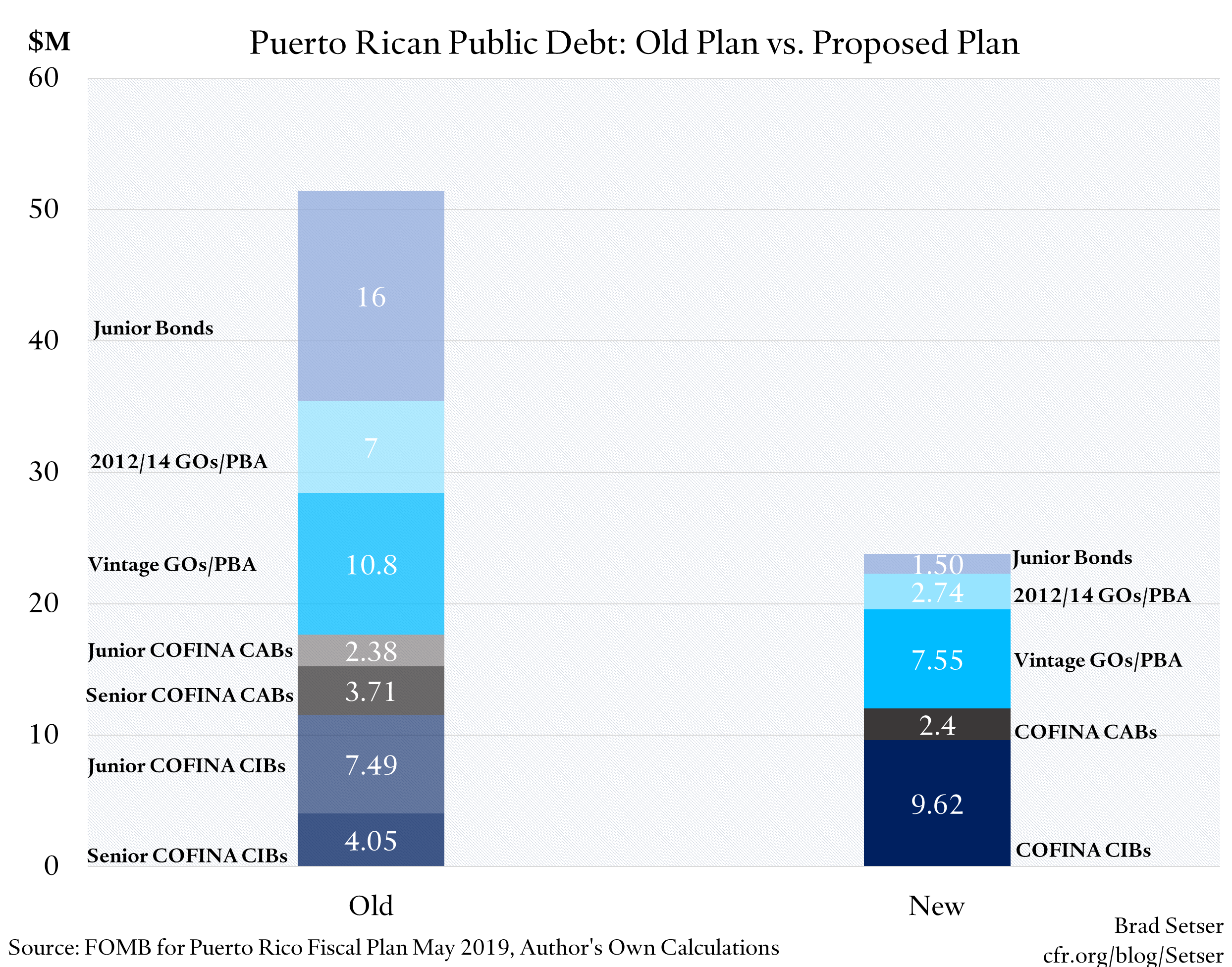

The plan of adjustment put forward by the oversight board, if approved by enough creditors and the courts, would cut Puerto Rico’s tax supported debt from $50 billion to $25 billion and smooth its repayment profile. Is that enough?

Puerto Rico’s oversight board has filed its plan to restructure the debts of the Commonwealth of Puerto Rico. If the plan is approved by at least one class of creditors and the court, it would more or less complete the restructuring of Puerto Rico’s tax supported debt.

A few years back, Puerto Rico had $50 billion or so in tax supported debt, a massive government pension system that had been used as a source of financing for the rest of the government and thus had no remaining financial assets, a declining economy and no guarantee of sustained Federal funding (the Affordable Care Act funds were set to run out).

If the restructuring of the commonwealth’s debt is completed on the terms the board proposed, Puerto Rico will emerge with around $25 billion in tax supported debt, somewhat smaller pension promises with the needed pay-as-you go funding built into the budget, and, to be honest, a still stalled economy.

When PROMESA—the special law modeled on chapter 9 that governs the restructuring of Puerto Rico’s debts—was passed by Congress back in 2016 it was expected that Puerto Rico would need to stand on its own, without any new federal support.

Hurricane Maria then radically changed a number of core fiscal assumptions: federal funding was needed to revive Puerto Rico’s economy in the short-run and the Congressional package included funds to help Puerto Rico rebuild—providing a jolt to Puerto Rico’s tax collections that has clearly helped to stabilize Puerto Rico’s budget (federal contractors are paying local corporate tax, see section 5.1.1 of the latest fiscal plan).

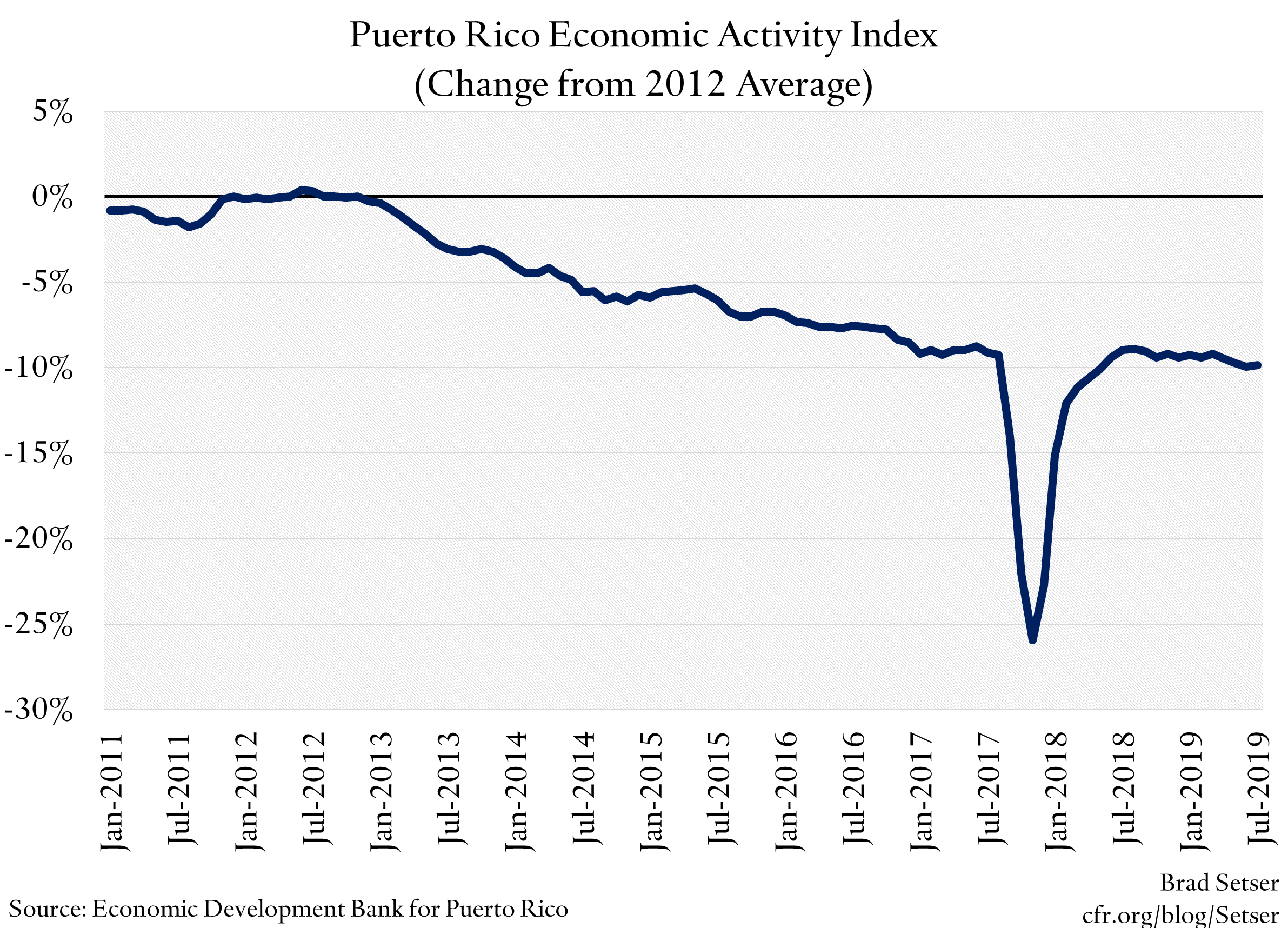

But disaster relief hasn’t changed everything—the relative buoyancy in tax revenues hasn’t been matched by broader strength in Puerto Rico’s economy, at least if Puerto Rico’s economic activity index is accurate.

More importantly, Puerto Rico’s future debt burden has to be scaled in a way that recognizes that federal disaster and recovery aid will eventually run out. The impulse from federal spending is now expected to fade after 2024, as the process of reconstruction has taken time to scale up (the previous governor didn’t help matters), creating a drag on Puerto Rico’s economy. And, well, given Puerto Rico’s demographics, Puerto Rico’s population is almost certain to shrink over time—with the fall in the working age population limiting the amount of debt Puerto Rico realistically can pay.

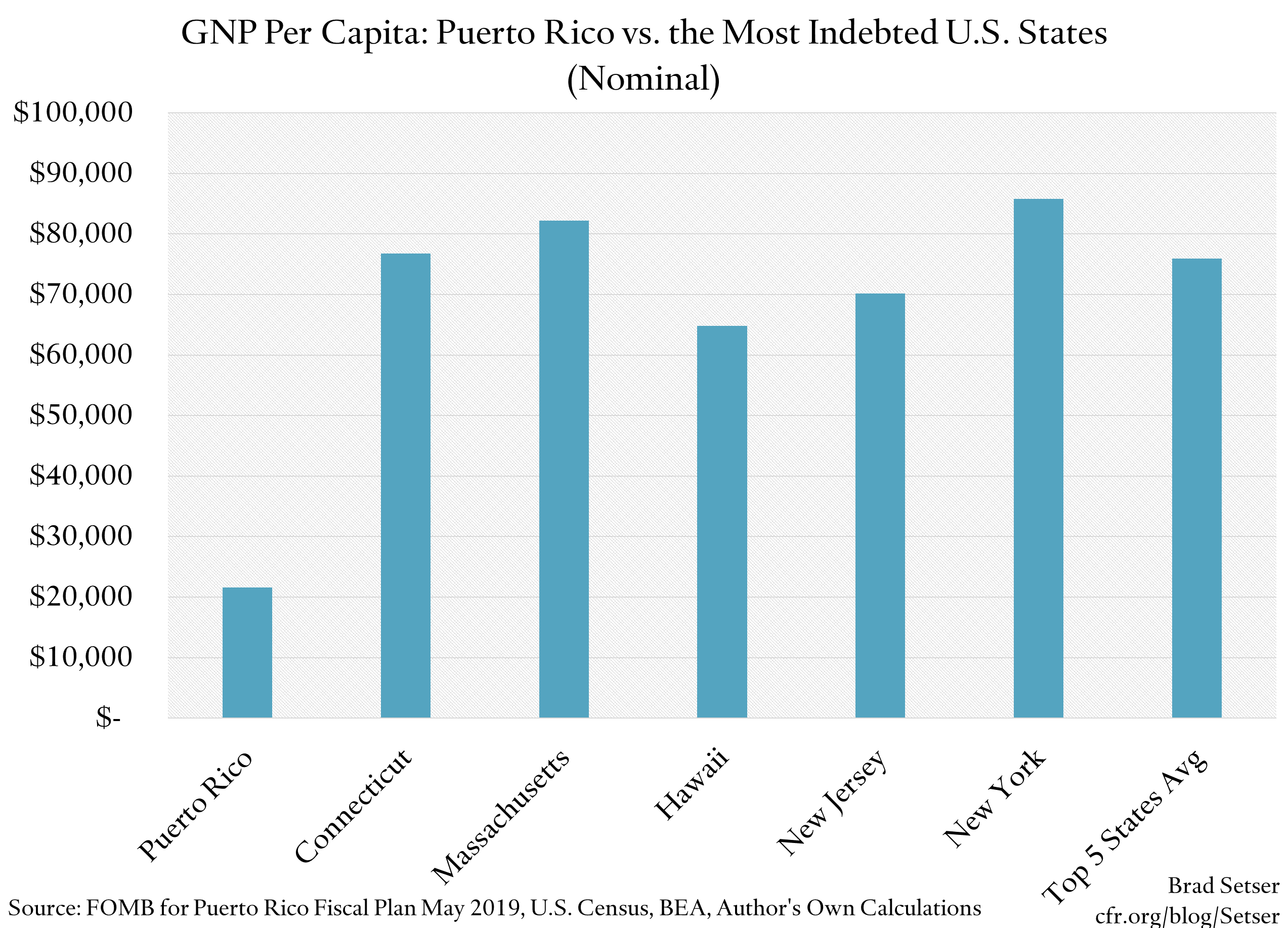

Cutting Puerto Rico’s tax supported debt in half certainly helps. But the return to sustainability isn’t completely clear cut. Even with the debt reduction, Puerto Rico will remain far more indebted than the average U.S. state (Puerto Rico obviously isn’t a state, but its debt sustainability is best assessed by comparison with the states).

What then is there to like about the proposed deal? And what concerns remain?

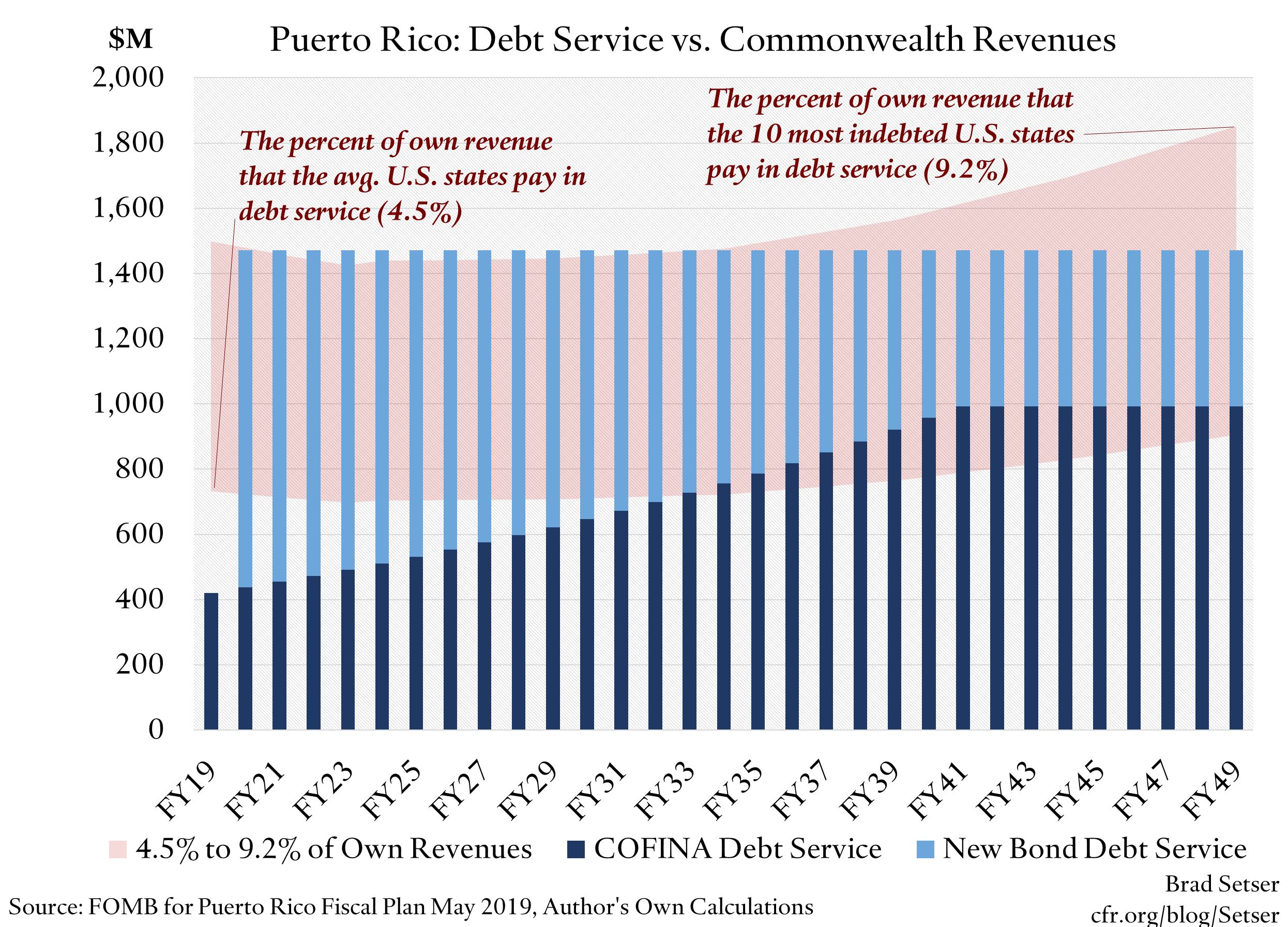

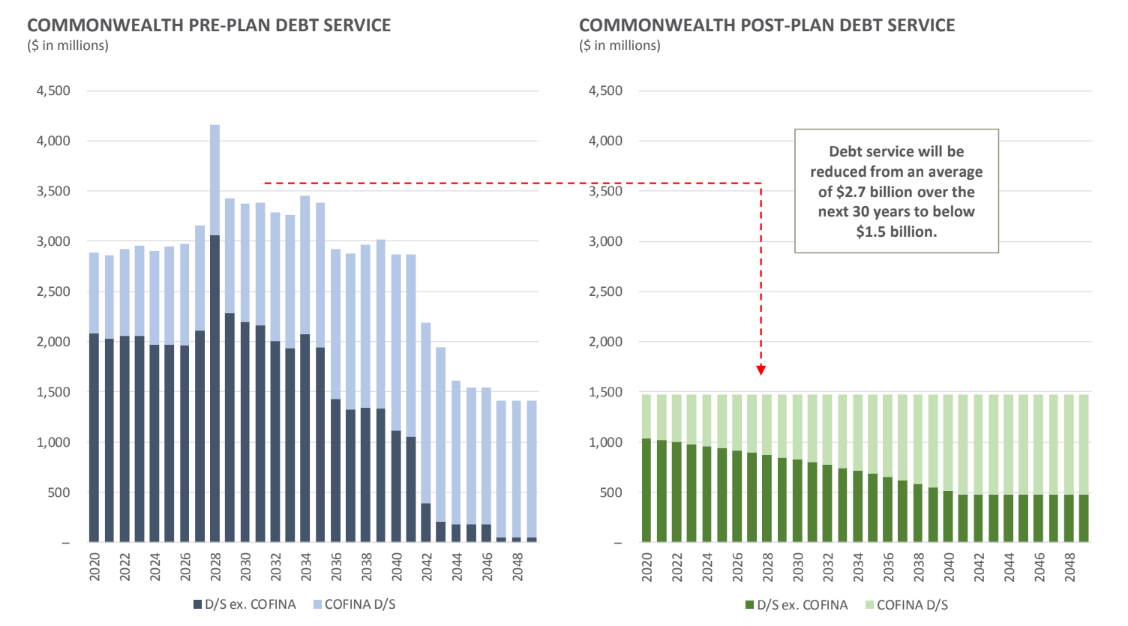

The best feature of Puerto Rico’s restructuring in my view isn’t the headline debt reduction. It is the flat debt service profile on the new debt.

In most restructurings, debt service is back-loaded—to give the country/state/municipality more time to grow out of its difficulties.

But one of the things that makes Puerto Rico unique is that its future is in many ways more uncertain than its present.

Most obviously, Puerto Rico’s economy is currently benefiting from the disaster and recovery spending approved after Maria. But that funding will run out—so we more or less know that Puerto Rico faces a significant negative economic shock over the next ten to fifteen years.

And, well, there is little basis to project future rapid growth. Before Maria, Puerto Rico’s economy was shrinking—see the Krueger report, among other documents. The trend wasn’t favorable. And Puerto Rico’s future demographics are likely to be much worse than they were during Puerto Rico’s 2005 to 2015 slump—without in migration, Puerto Rico’s population is expected to shrink by about a percentage point a year. Oh, and if you believe in the science of climate change, Puerto Rico will face increased risk of another catastrophic hurricane as the oceans around Puerto Rico rise in temperature.

Keeping debt service flat may seem extreme, but in my view it is actually a vital component of any restructuring that aims to provide a path to sustainability.

The stable debt service path was achieved by front-loading amortization on the new general obligation bonds, as the new sales tax backed bonds have a rising burden over time. I didn’t find a principal/coupon breakout in the material that the board has released, but my math suggests that the stock of outstanding new commonwealth bonds will fall from around $12 billion now to about $8 billion in 2030, and about $4 billion in 2040. That helps to offset the impact of the capital appreciation bond in the new COFINA (sales taxed backed bond) structure. I would much prefer a restructuring that completely eliminated the capital appreciation bond (now valued at around $2.5 billion, but it will generate around $14 billion in future debt service), but, well it is too late now.*

There is another thing to like about the proposed deal: the allocation of pain across different groups of creditors is reasonable, and broadly in line with the market’s expectations (with the exception of the proposed difference in treatment between the legacy general obligation bonds and the new general obligation bonds). More senior bonds got better terms, more junior bonds took a big haircut—that’s how bankruptcy is supposed to work.

A bit of background here: Puerto Rico’s pre-bankruptcy debt was notable not just for its size—$50 billion was a lot of tax supported debt relative to Puerto Rico’s tax revenues—but also for its complexity. There were broadly speaking two key sets of bonds that both thought they should be protected in any restructuring—the $17 billion (counting the capital appreciation bonds) in sales tax backed bonds and the $18 billion in “constitutional” general obligation bonds and constitutionally guaranteed Puerto Rico Building Authority (PBA) bonds. But there were a bunch of bonds issued by other parts of the government—the infrastructure authority, the highway authority, the retirement system, the university—that lacked constitutional protection (and were subordinate to the constitutional bonds because of the “clawback” feature). And the Government Development Bank had some unsecured claims on the government.

Putting Puerto Rico in a framework modeled on Chapter 9 was—as some investors recognized at the time—likely to be good for the senior sales tax backed bonds, as U.S. bankruptcy law protects secured claims.

The proposed deal, in aggregate, provides the highest recovery to the senior sales tax backed bonds, who get around 90 cents on the dollar. And the proposed deal would result in relatively similar terms for the junior sales tax backed bonds and the legacy “constitutional” general obligations bonds. Both get new bonds with a face value of over 50 cents on the dollar (the “unchallenged GO bonds” will get at least 64 cents on the dollar; COFINA junior bonds got 55 cents on the dollar and traded out of a junior claim). There will be one difference—the cash flow on the new general obligation bonds will be front-loaded while the cash flow on the new sales tax backed bonds is more back-loaded. However, it isn’t clear how that cash flow pattern cuts: in general, you want to be paid sooner not later, but in today’s low rate world, a 4-5 percent tax free coupon provides a lot more income than you can get elsewhere in the muni market.

The holders of the constitutional general obligation and PBA bonds also will be sharing close to $2 billion in cash (~ 10 percent of the bond’s face value), and the holders of the sales tax backed bonds got past due interest on their claims.

The biggest surprise relative at least to my expectations back in 2016 is the low potential recovery on the 2012 and 2014 general obligation bonds. The board challenged whether these bonds really should have constitutional status**—on the grounds that the bonds were issued in excess of the constitutional debt limit, and has offered these bonds (with a face value of around $7 billion) substantially less than it has offered holders of the roughly $11 billion in vintage general obligation and PBA bonds (see p. 6) . This is likely to be litigated further.

The recovery on the retirement bonds, if the deal is approved by the courts, will be 13 cents on the dollar. Other junior bonds will get even less. The overall recovery on the $15 billion in junior claims is estimated to be around 9 cents on the dollar.

Basically, the relative reduction in claims worked more or less as expected, apart from the differentiated treatment of the new and vintage general obligation bonds that followed from the Board’s forensic analysis.

So what’s not to like?

Well, Puerto Rico, the poorest part of the United States, will likely remain the most indebted part of the United States.

A key metric for assessing the sustainability of a state’s debt is its debt service relative to its own revenues—federal funds cannot generally be used to help cover a state’s debt, as they are allocated for specific purposes. Puerto Rico’s proposed restructuring will keep its debt payments about equal to the average debt payments of the most indebted states, and well above the payments of an average state.

There is reason to worry here, as debt service to “own” revenue is actually a pretty favorable metric for creditors, as Puerto Rico’s own revenues are above what would be expected given its income level.***

Many think that is because residents of Puerto Rico don’t pay federal income tax on income earned in Puerto Rico. But that’s not really the case—Puerto Rico collects about $2 billion a year in personal income tax, or 3 percent of its GNP. It could raise its tax on capital income and collect a bit more, but if it fully matched the federal income tax structure and replicated the earned income tax credit, it would actually collect substantially less than it now does. The federal income tax is relatively progressive, so replicating the federal income tax structure doesn’t yield that much revenue when Puerto Rico’s median family income is under $20,000.****

The actual reason for Puerto Rico’s relatively large tax base is the absence of federal corporate income tax on corporate income earned in Puerto Rico. Puerto Rico in turn has found various ways to extract a bit of revenue out of the firms that operate in Puerto Rico to avoid federal income tax—the corporate income tax, non-resident withholdings, and Act 154 all pull up Puerto Rico’s tax revenues relative to a typical state.

That’s one of the risks Puerto Rico faces going forward—it isn’t clear that Puerto Rico will be able to hold on to this tax base going forward. The Treasury, correctly, has concluded that Act 154 payments will no longer be creditable against federal corporate income tax (this was a backdoor transfer from the Treasury to Puerto Rico of around $2 billion a year). And, well, the current discussion about income inequality could well lead to broader changes in the corporate tax code that make it harder for firms to shift profit abroad, or Puerto Rico simply might well decide that it wants to become a state.

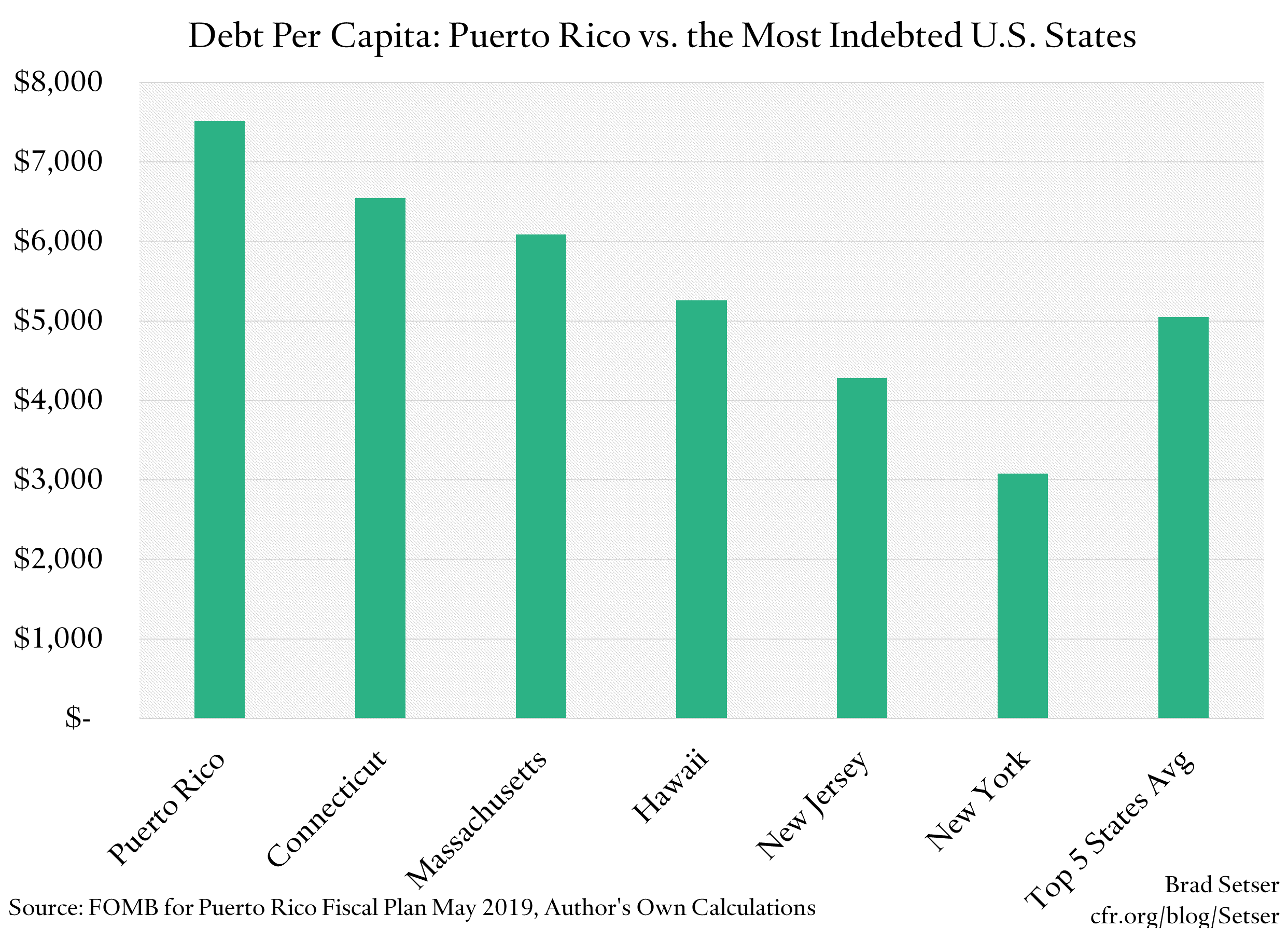

On other metrics, the proposed restructuring would leave Puerto Rico a bit more indebted than the most indebted U.S. states. Debt per capita for example would top the high state average.

Puerto Rico basically would have the per capita debt of a Connecticut or Massachusetts but not the per capita income of these states.

One easy way to see all this is to compare Puerto Rico’s post restructuring debts to those of Mississippi, the poorest U.S. state.

Mississippi has a similar population (3 million), and median household income of around $40,000 (twice that of Puerto Rico). It collects around $6 billion in its own revenue—and that supports around $5 billion in debt, and $400 to $500 million in annual debt service. Its state GDP is $115 billion, close to twice Puerto Rico’s state GNP.

Puerto Rico will be left with $25 billion in debt and just under $1.5 billion a year in debt service—which will be backed by $15 billion in own revenues and a $70 billion economy (Puerto Rico’s GDP, like Ireland’s GDP, is inflated by transfer pricing linked to its tax status—it isn’t reflective of the actual size of Puerto Rico’s economy).

You can see why I would have preferred a somewhat lower level of tax supported debt and a somewhat more modest debt service burden. I certainly don’t think Puerto Rico can afford more.

But the proposed restructuring is an enormous improvement—and the new debt profile at least provides Puerto Rico with a fighter’s chance to return to sustainability.

Full disclosure: I worked on Puerto Rico while at the Treasury in 2015, and helped craft some of the proposals that were ultimately passed by the Congress in 2016. I am not a completely neutral observer. But hope I am also a fairly informed observer.

* Capital appreciation bonds are municipal equivalent of zeros. They raise very little money, but create massive future payment promises. They are the reason why payments on the unrestructured COFINA sales-tax backed bonds were poised to go from around $650 million to close to $2 billion.

** Debt service on Puerto Rico’s constitutionally backed bonds was in principal limited to 15 percent of the revenues of the government’s General Fund—as defined by the government’s formal budget not the broader concept the Board uses—but Puerto Rico found various ways around this limitation. COFINA was moved off the budget for example, so it didn’t count toward the the debt limit. And payments on Puerto Rico Building Authority bonds entered the budget as “rent” payments not as debt service. There are other examples too.

*** The pre-restructuring debt service profile was an absolute mess. There was no way Puerto Rico could pay $3-4 billion a year in debt service on tax supported debt, at least not without a federal bailout.

**** The median family would get money back if Puerto Rico’s tax system fully mimicked the federal tax system, thanks to the Earned Income Tax Credit (EITC).