Argentina pushed back the deadline for its restructuring to the end of July, after failing to reach agreement with a majority of its creditors on terms for the restructuring of Argentina’s $65 billion in bonded debt.

Differences have narrowed to the point—a few cents on the dollar—that it isn’t that difficult to see how a deal could be struck in July. But the narrowing of differences with some creditors (Argentina’s most recent offer was worth around 50 cents on the dollar at a ten percent discount rate on the new cash flow, with the high coupon “discount” bonds offered about five cents more) has made the gap between Argentina and the subset of creditors who want a richer deal much clearer.

That in turn has drawn attention both to the tactics that Argentina may use to increase participation in its exchange, and the call by a subset of Argentina’s creditors to roll back recent reforms to sovereign debt documentation and return to (holdout friendly) bond-by-bond voting.

Ironically, Argentina is not actually using the most innovative feature of the new ICMA collective action clauses—so called single limb voting. Indeed, many of the difficulties Argentina now faces stem from the fact that around $25 billion of the $65 billion of bonds that Argentina is now seeking to restructure lack the new clauses. That reality, together with the absence of a formal bankruptcy process for sovereigns in distress, allows scope (even under the new(ish) ICMA clauses) for a deal that is crafted in a way that treats some bonds better than others.

To date, the dynamics among the different Argentina bond holders have gotten much less attention than the negotiation between Argentina and its bondholders. Yet as the end-game approaches, the different preferences and strategies of different groups of bond holders will start to loom larger. And the key divisions among creditors actually do not fall neatly along the distinction between Kirchner- and Macri-era bonds (the Kirchner bonds have the old collective action clauses, the Macri bonds use the new standard).*

------

Understanding the dynamics among creditors is hard without first understanding the underlying dynamic between the debtor and its creditors. At this stage, I think the key features of any restructuring (see Argentina’s latest offer) are pretty well defined:

1) The par value of the $65 billion in bonds that Argentina is seeking to restructure by and large will be maintained. Since these bonds now trade at around forty cents on the dollar, this means that the offer provides creditors with substantial upside should Argentina’s creditworthiness improve.

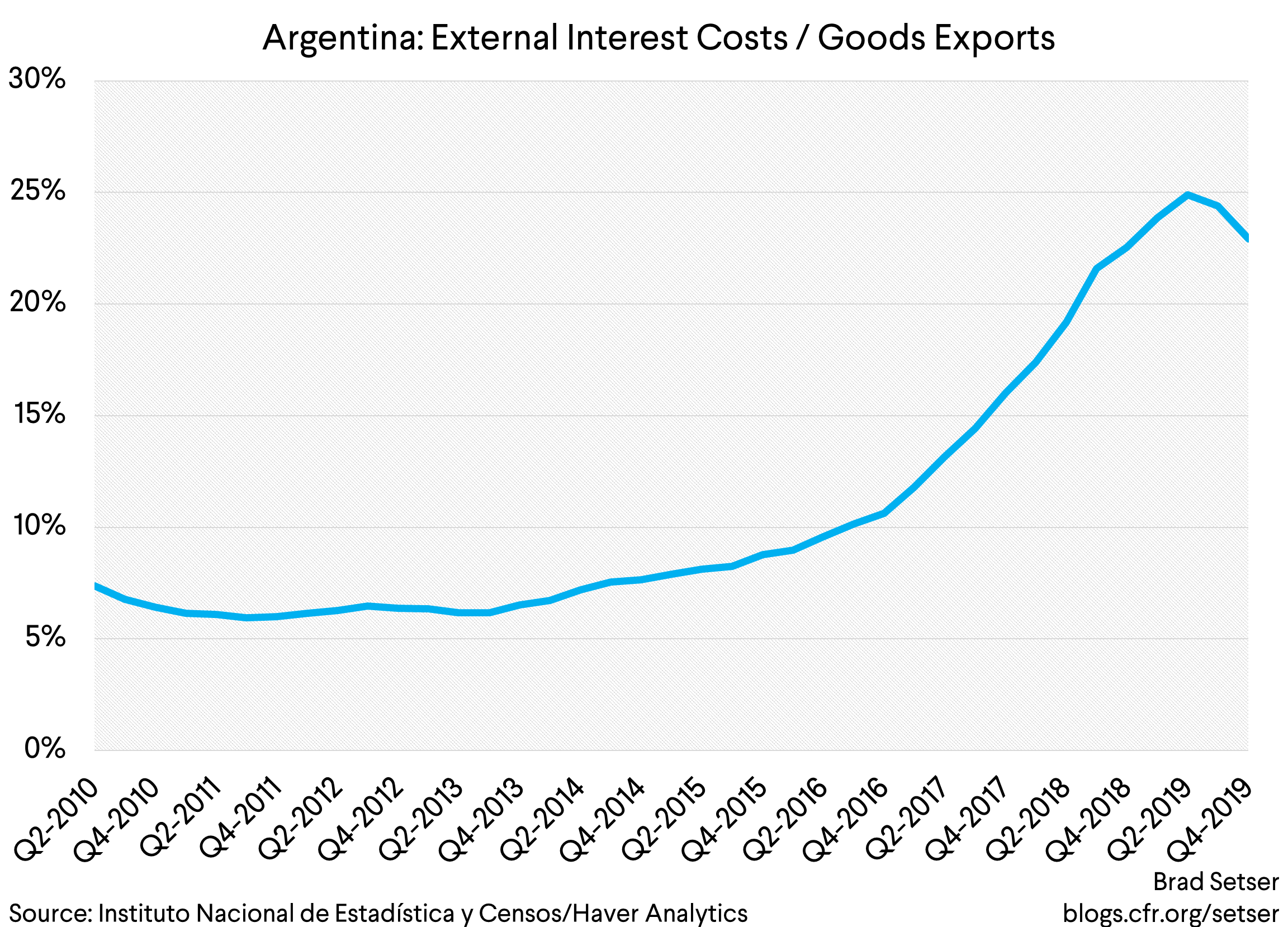

2) The coupon on the bonds will be cut to improve Argentina’s long-term solvency. The $45 billion in bonds that Argentina issued under President Macri have led to a rapid increase in Argentina’s external interest payments relative to its exports, as those bonds were issued at a relatively high (~7 percent) coupon. Argentina now needs a lower coupon to accommodate the increase in its debt stock and allow time for exports to catch up. Argentina’s latest offer proposes a terminal coupon of 5 percent, while the most aggressive subset of creditors is asking for 6 percent (the difference may not seem like much, but it represents a 20 percent increase in coupon payments that are fixed in some cases well into the 2030s).

3) And the restructuring will provide substantial upfront cash flow relief. Payments this year will be zero or close to it, and payments next year will be notional rather than real. Argentina is now running a substantial primary deficit, so any payments would have to come out of Argentina’s already depleted foreign exchange reserves.

But there are still a few variables in play. Argentina has now agreed to pay accrued interest on the existing bonds with a new bond, but the terms of that bond are still under negotiation. And the pace at which Argentina’s interest payments step up as well as the exact final rate are still a subject of negotiation. Finally, Argentina could give creditors a state-contingent instrument which pays out only in good states of the world—apparently, Argentina is considering a soy-linked bond, while some of its creditors still prefer a GDP linked bond.

Discounted at 10 percent, the current Argentine offer is worth around 50 cents, with the Kirchner-era discount bonds getting more like 55 cents on the dollar. But judging the debt relief provided by using the market discount overstates the amount of real relief. From the Argentine point of view, the relevant discount rate should be lower—at a discount rate of 4-5 percent (roughly long-term dollar GDP growth) the NPV is in the 70s or 80s. No doubt, Argentina is seeking real concessions from its creditors—but not a huge haircut.

------

Argentina though faces a second challenge: even if most of the creditors are willing to accept the basic contours of the proposed restructuring, it also has to get all of the individual bonds to vote in favor of the deal. And like all sovereigns, it is doing so without the backstop of a formal bankruptcy process.

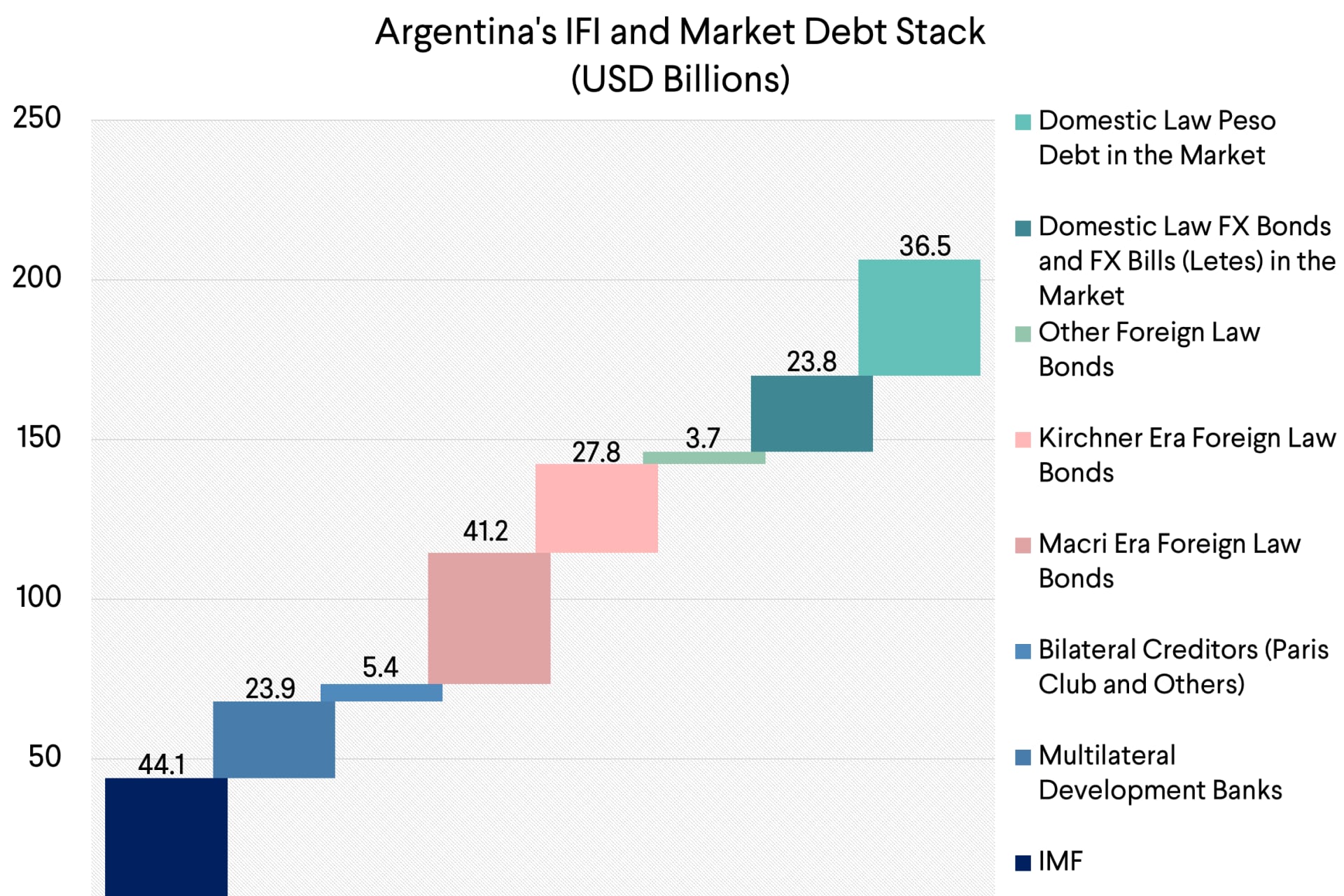

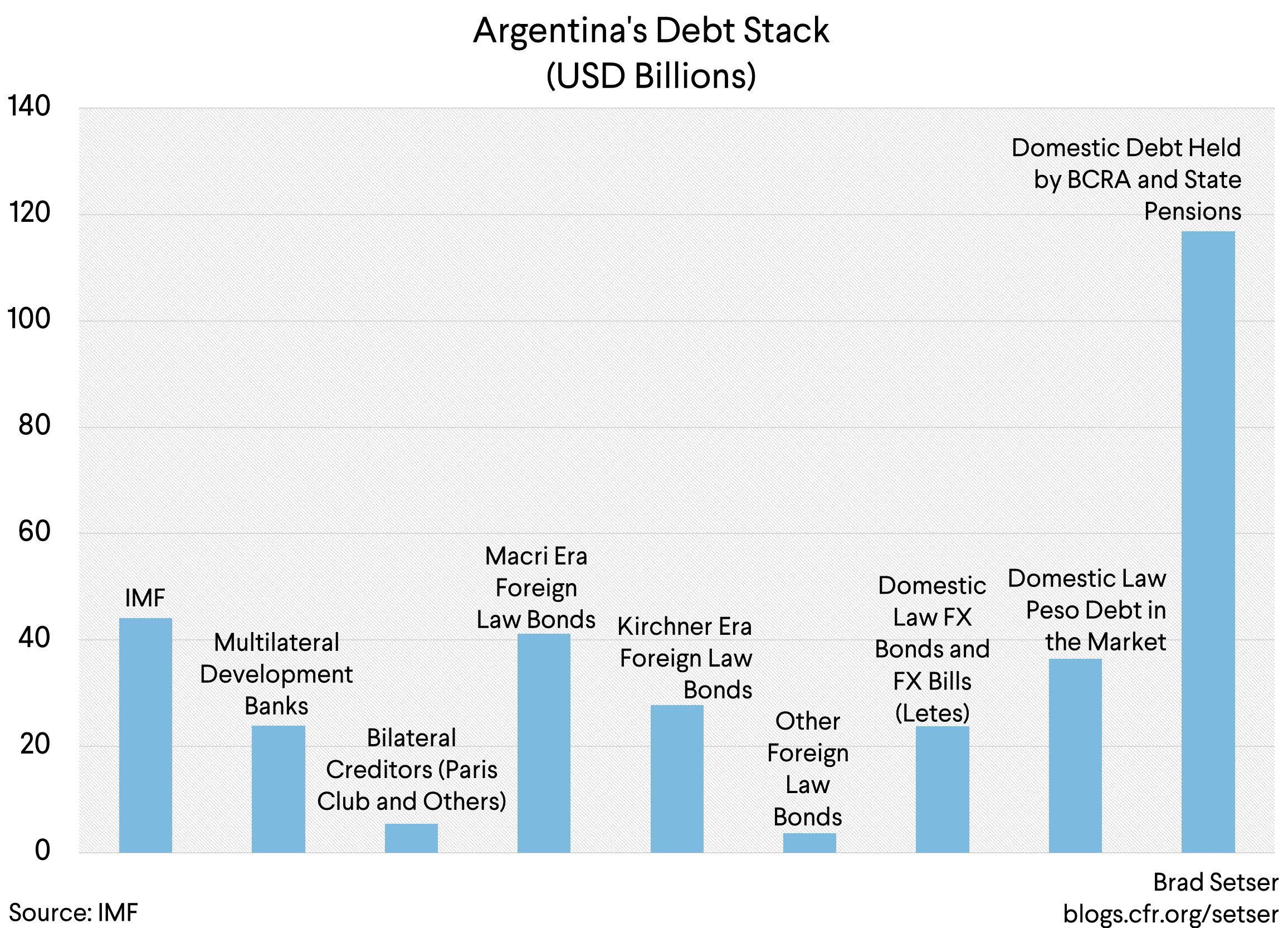

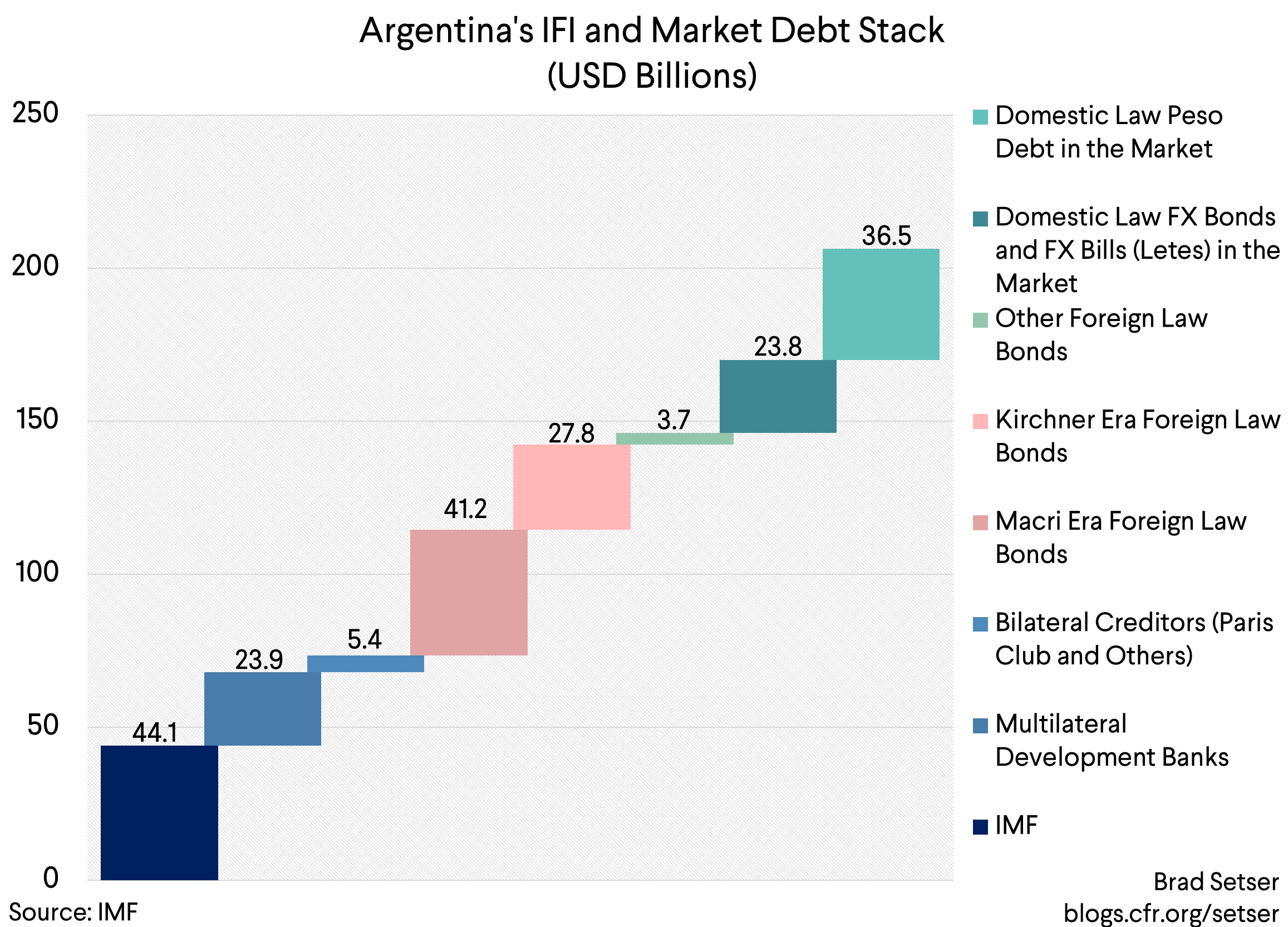

Technically, all of the international sovereign bonds are of equal legal rank. But that does not mean all the bond holders want the same deal. Some think their bonds have a claim to be treated better than other equally ranked bonds (and it is always worth remembering that the international bonds are only a portion of Argentina’s total debt).

There are two particular groups that want a sweeter deal than other bonds and think they have the leverage (and votes) to extract better treatment—the holders of the “discount” bonds issued under President Kirchner, and the holders of the bonds maturing in 2021 and 2022 that were issued under President Macri.

A bit of background is needed here.

Well, more than a bit of background, as the voting process for Argentina’s bonds is particularly complex.

In theory, the easiest way to restructure $65 billion in bonds is to offer all $65 billion in bonds the same package of new bonds—each dollar (or euro) of par gets the exact same thing, or the exact same set of choices. Every dollar of par (or face) goes, conceptually, into the same new bond with the same cash flow. That’s the idea behind the “uniform” offer provision of the new aggregating clauses.*

The reason why the offer is on the par value of the bonds is simple: after default on one bond, all bondholders have the right to accelerate so long-dated bonds become short-dated bonds. So legally, long-dated bonds have the right to collapse the curve and get the same deal as short-dated bonds.

But not all of Argentina’s $65 billion in bonds have the contractual provisions that allow voting on restructuring terms to be done through a single up or down 75 percent vote. Specifically, the $25 billion in Kircher-era bonds—split about evenly between the low-coupon pars and the high-coupon discount bonds—don’t have the new aggregation clauses. That means that even if Argentina used the uniform offer provision to restructure the Macri-era bonds, Argentina could only get full participation in its exchange if 75 percent of the holders of each of the Kirchner-era bond series (and there are two generations of Kirchner bonds, one from 2005 and one from 2010) vote for the deal.

And there is an added wrinkle: the Kirchner-era bonds have a dated form of aggregation in their legal documentation so if Argentina gets the votes of 85 percent of the Kirchner-era bonds, the threshold for restructuring each bond series falls to 67 percent of the holders of that bond series.

A complete restructuring of Argentina’s international bonds thus would require at a minimum winning the votes of:

- 75 percent of all $40 billion and change of the Macri-era bonds…so an affirmative vote of around $30 billion in par value

- And at least 6 percent of the holders of each of the pars and discounts if 85 percent of the Kirchner-era bonds collectively vote for the deal, or (more likely) 75 percent of the vote of each series.** (In practice, the 85 percent to drop the threshold to 67 percent aggregation clause doesn’t give you that much)

The Kirchner-era par bonds aren’t likely to be much of a problem. The par bonds aren’t due for a while anyway, and they already have relatively low coupons. The Kirchner-era discount bonds are by contrast a bit of problem. They have a relatively high coupon (that’s what they got in return for giving up par back in 2005)*** and don’t like the coupon reduction in this deal. And the holders of the discount bond think they have a better than average legal claim should they holdout, as their bonds have the old flavor of pari passu clauses and thus in theory have an easier path to litigate for full payment. This replicability of the NML legal strategy is debatable****, but there is little doubt that the discount bond with its high coupon offers the best vehicle for a holdout and litigate strategy.

The emphasis on the old legal language in the Kirchner-era bonds though masks another difficulty with the restructuring: the holders of the Macri-era bonds coming due in 2021 don’t want the same deal as holders of other Macri-era bonds, including the famous century bond. That in turn has made it hard to restructure the Macri-era bonds through a single uniform offer.

In fact, Argentina is currently seeking to use the provisions in the ICMA clauses that allow the bonds to be restructured through a more tailored offer rather than restructuring the Macri-era bonds through a straight up and down vote. The two limb aggregation provisions allow Argentina to provide better terms to the near dated bonds—the offer doesn’t have to be uniform on par value. But in order to do a deal, Argentina needs the votes of half of the holders of each bond series so long as it gets two-thirds of all Macri-era bonds (and just to make things more complicated in some circumstances the votes of the Kirchner-era bonds can be added in here, but set that aside).

Why would Argentina want to use this more complicated voting process when it unquestionably could restructure the Macri-era bonds through a single 75 percent vote?

Well, because there are a lot of holders of the near-dated bonds (there are nearly $8 billion in 21s and 22s outstanding) and if those bonds vote in a block against the deal, Argentina needs to get almost all the votes of the longer-dated Macri-era bonds to get 75 percent.

And why would the holders of the near-dated bonds reject an equal offer on par?

Some apparently think Argentina doesn’t want a hard payments default and thus they have leverage.

But some of the holders of the 2021 bond in particular are themselves in a bit of a pickle, and want Argentina to help them out—funds that had a strategy of buying the cheapest near dated bond ended up with portfolios concentrated in Argentina and Lebanon and a few other countries that are in difficulty, and thus they have a particular incentive to play hardball (the Ad Hoc committee has proposed giving the near dated bonds new bonds worth about 65 cents on the dollar—so substantially more than other bonds would get).

So Argentina and its advisors—for now—seem to have concluded that it is easier to get the votes of 51 percent of the 2021 and 2022 bonds by giving them a slightly better offer than it is to get all the votes of the long-dated bonds with an equal offer.

That is what financial advisors are paid to figure out. And Economy Minister Guzman actually knows a fair amount of bond math while still having full command of the legal intricacies of a restructuring.

These dynamics among Argentina’s various creditors aren’t exactly a secret—but they also aren’t exactly obvious. The divisions within different groups of creditors are masked so long as the holders of the pars and discounts have united under the “exchange bonds” rubric, and so long as the mainly institutional investors in the Blackrock group that primarily hold the Macri-era bonds stick together. In practice, the holders of the pars and discounts have slightly different interests, as do the holders of the near and long-dated Macri bonds. And of course there are other groups of creditors as well: the bonds collectively are only about a fifth of total public debt.*****

------

That is the background to the current debate over legal tactics.

Faced with aggressive demands from a subset of its creditors—including demands to roll back the ICMA clauses and use holdout friendly documentation on its new bonds, Argentina has responded by proposing some aggressive legal tactics of its own.

For what it is worth, I personally don’t think amending the bonds to change the voting rules (re-designation) should be possible—that is something that the ICMA could consider adjusting in its model clauses, if in fact it is allowed now. The intent of the ICMA clauses was clearly to force the issuer to set out the voting rules it was using before it started counting the votes (and thus to run the risk of a failed exchange). But if there is a Macri-era bond that votes against the proposed deal, carrying out a second vote where the holdouts are aggregated with participating creditors and get an equal offer in the second exchange (Pacman) strikes me as consistent with both the letter and spirit of ICMA clauses. The new offer would have to treat all par claims equally; no one would get less than the majority of participating creditors—plus, well, if a majority of the (big) 2021 bond turn down the deal they could only be brought into the restructuring through a second vote that commands a super-majority of a big new bond, so carrying out this strategy would not be easy or cheap.

To me the broader lesson here isn’t to abandon one limb voting (the new ICMA voting process) but rather to double down on it—some of the complex dynamics in this negotiations would go away if all the bonds were governed by the same documentation and it was clear that if any complicated offer that appealed to different funds failed Argentina would just do a straight 75 percent vote that treated all par claims the same.

In fact, I think the best way forward now may be a one limb vote of the Macri-era bonds that binds in the short-end with a bit of help from the pars (with the voting rules spelled out in advance). That at least becomes a plausible tactic if the front-end of the Macri-bond curve starts asking for too much.

But the bigger issue here is that Argentina’s restructuring matters both for Argentina and for the sovereign debt architecture. Argentina’s example matters much more so than any talk of a generalized standstill on emerging market debt, which always was a bit hypothetical and didn’t reflect the reality that only a subset of countries currently lack reserves and really need to restructure their hard currency debt. Argentina is by far the biggest such country. Yet it would equally be a mistake not to recognize the specific financial considerations that are driving certain creditors complaints—the discussion over architecture isn’t coming from neutral parties operating behind a veil of ignorance.

* Full disclosure: I have spoken to a number of creditors over the last year both privately and over Twitter and I also know Argentina’s advisors—the set of people who have a deep interest in sovereign debt restructuring is growing, but it remains a specialized world. I have no financial position in any bond. I joined a number of others in signing a letter supporting the basic structure of Argentina’s offer.

** The details of what constitutes a uniform offer were hammered out in consultation with a number of large bond holders. More disclosure—I also was involved in the process that helped develop the ICMA model clauses and I am among those who believe the new clauses are a substantial improvement to the sovereign debt architecture (see Count the Limbs).

*** Over the last 15 years, the discounts have gotten 4 percentage points more than the pars in coupon, which has basically made up for the discount to face in the exchange—so the discount bond holders actually do not have much of a claim for better treatment than the pars based on abstract notions of financial equity. Their calls for getting compensation now for concessions made by another set of bondholders back in 2005 strike me as rather, umm, bold.

**** Key issues include how the courts interpret the “course of conduct” test for determining what constitutes subordination and thus a violation of the Kirchner-era pari passu (equal rank) contractual language in the Kirchner bonds—and whether or not the courts will award the “nuclear” remedy (blocking payments on all the bonds that emerge out of a consensual restructuring) for a violation of pari passu in today’s context. I personally would like to see the Greisa rulings narrowed, as I am among those who think that they risk changing the balance of power in a sovereign debt renegotiation in a way that could make out-of-court settlement difficult. Indeed, if creditors push for the removal of single limb aggregation clauses in future bond issuance and in effect try to walk back the reforms introduced (in full consultation with creditors; ICMA isn’t exactly a debtor led organization) to limit holdout risks there is a possibility, noted by Anna Gelpern, that one consequence could be a new push toward sovereign bankruptcy. The 1990s argument that holdouts were more of a theoretical than a real problem in bond restructuring is no longer credible as more and more creditors have adopted litigation based strategies—no doubt influenced by the large financial return NML secured after winning a legal lottery ticket.

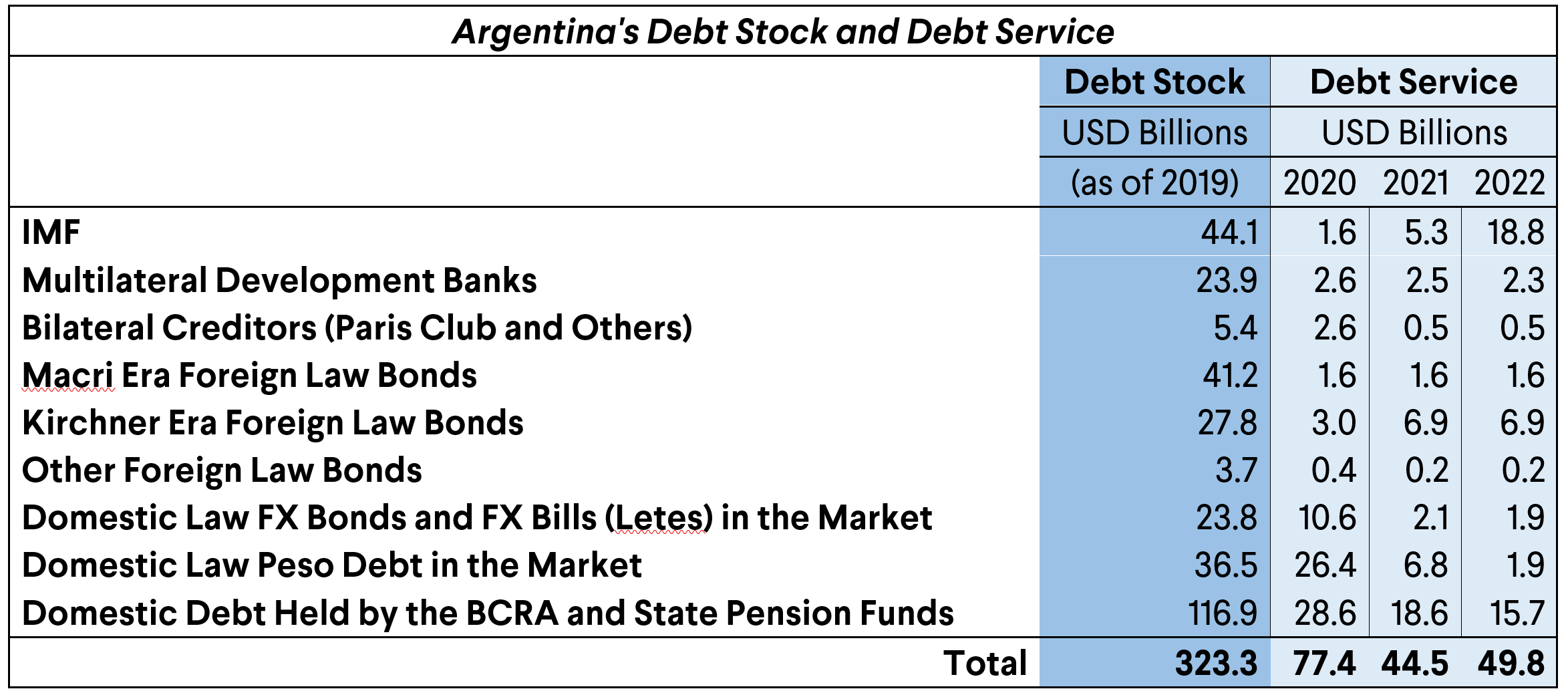

***** The IMF’s split between debt service on the Macri and Kirchner era bonds looks off. The April 2021 and the January 2022 Macri bonds should push up the Macri era totals in these years.