What Role Should the IMF Play in Responding to COVID-19?

Right now the bulk of the IMF’s lending capacity likely won’t be used in the face of the economic, financial, and public health shock from COVID-19. Mobilizing the IMF’s lending capacity likely will require a new facility. The Short-term Liquidity Line created this spring isn’t actually well suited for the moment.

The coronavirus shock was, for many emerging economies, a financial shock—not just a shock to the economy and public health. Advanced economies can borrow to help tide their economies (and societies) through a difficult period of social distancing. The same cannot be said for many emerging economies—and certainly not for the world’s poorest economies.

A couple of weeks ago former Treasury Secretary Larry Summers suggested that discrepancies in countries ability to borrow amid a pandemic constituted a global problem, as they would inhibit an effective recovery in global public health:

“What are some of the elements of that global response? Assuring an adequate flow of credit so that people can—countries can borrow to get themselves through the extraordinary expenses and extraordinary deficits that are going to take place right now. Why should the richest be able to borrow, as the United States is, on an inordinate scale, and those who are even more in need, those with even less reserves, be unable to borrow.”

In the advanced economies, powerful central banks have been able to keep markets stable and allow all the G-10 countries—reserve currency issuers or not—to borrow the funds needed to keep their economies afloat at very low interest rates.

But for emerging economies it has been more of a struggle.

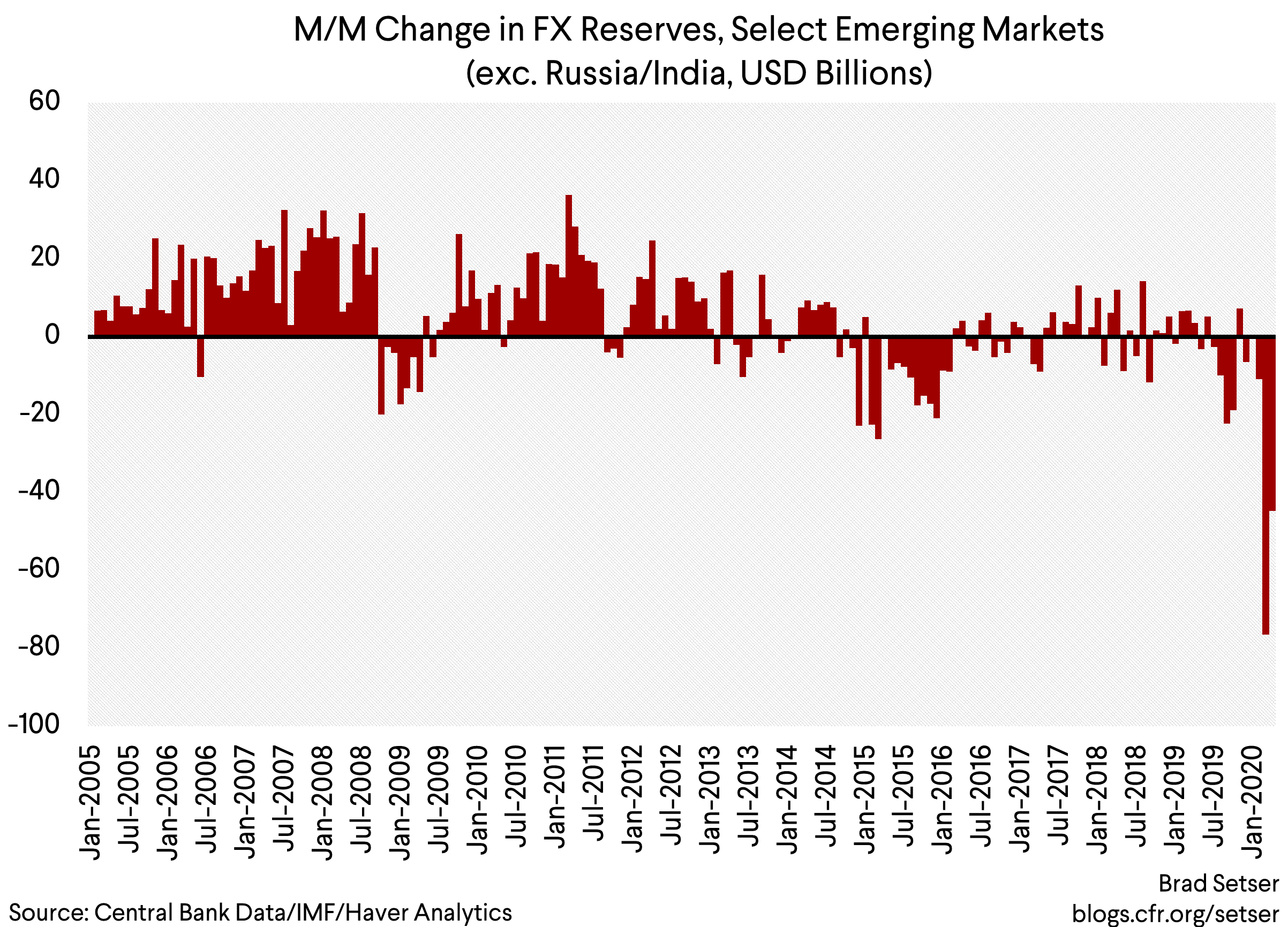

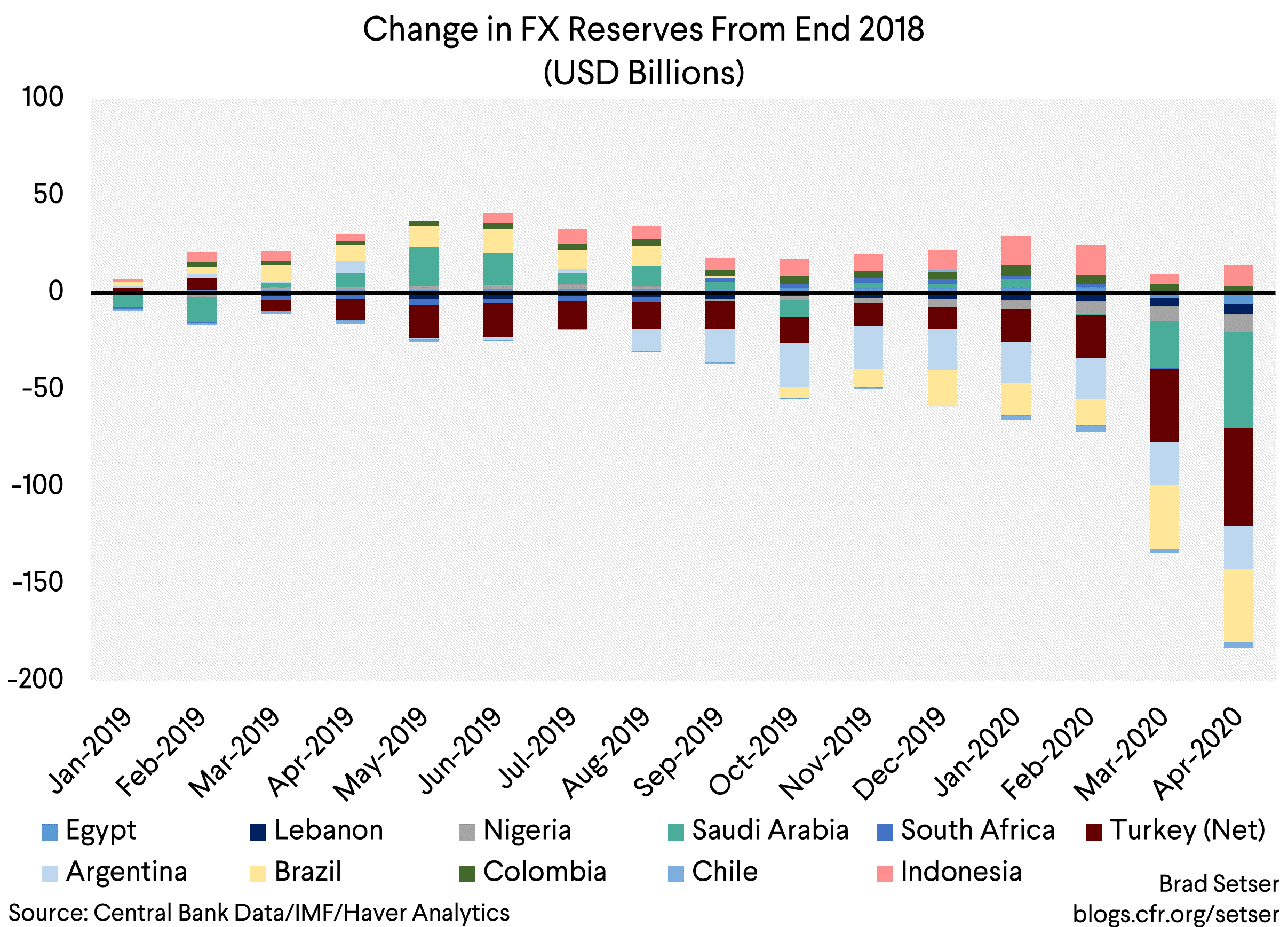

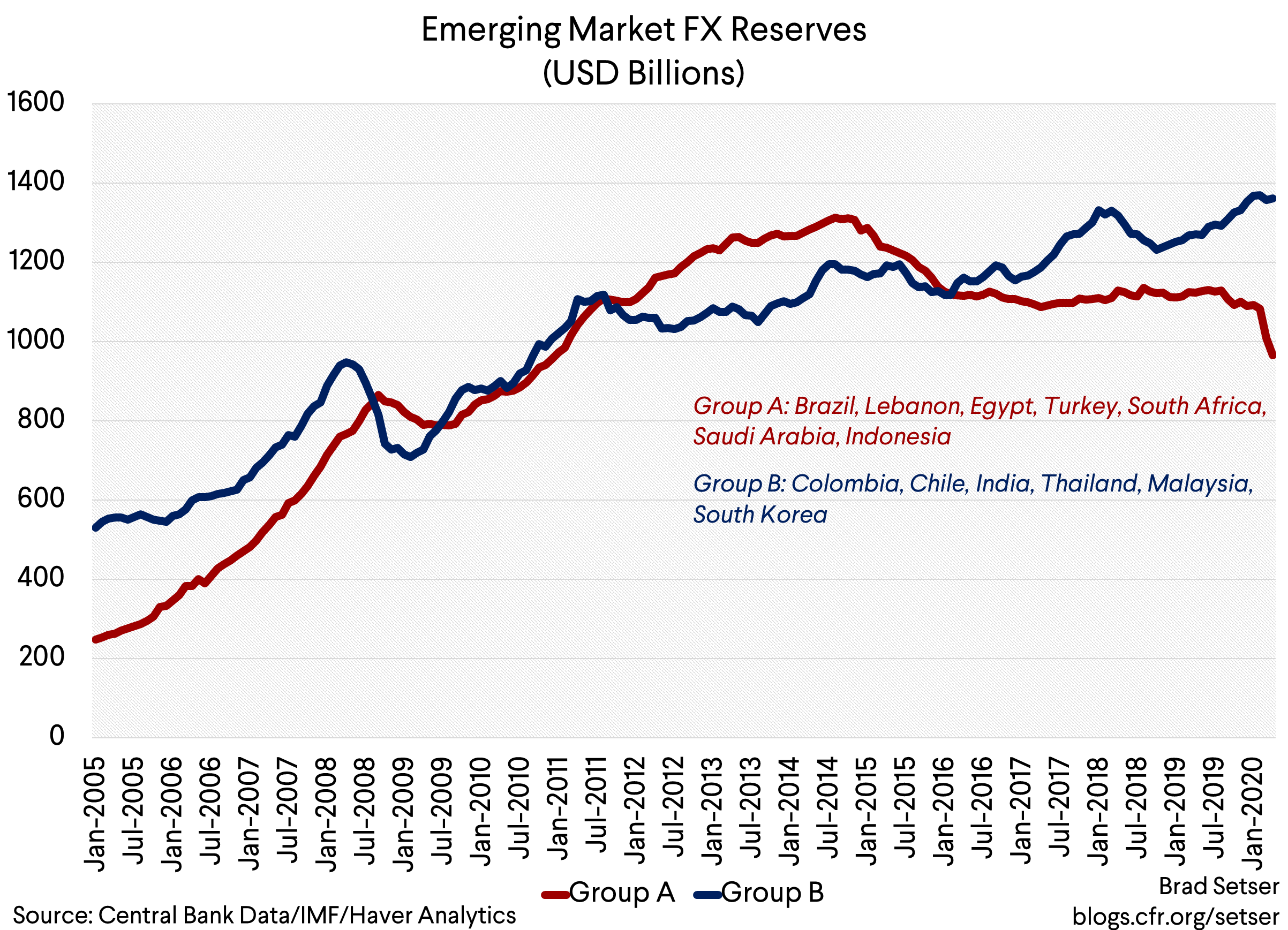

The withdrawal of foreign financing from emerging economies in March was by some measures sharper than the withdrawal during the global financial crisis. The swing in portfolio flows (investment in local bonds and equities) was certainly bigger. The swing in bank flows looks to be smaller. But there is no question that there has been an enormous withdrawal of foreign private financing from emerging markets just as borrowing needs have shot up. That shows up cleanly in the fall in the reserves of many emerging markets in March and April.*

April was better than March and May and June likely will be better than April—but even the stronger countries that can still borrow internationally are generally doing so in dollars or another international currency, and at a decent premium.

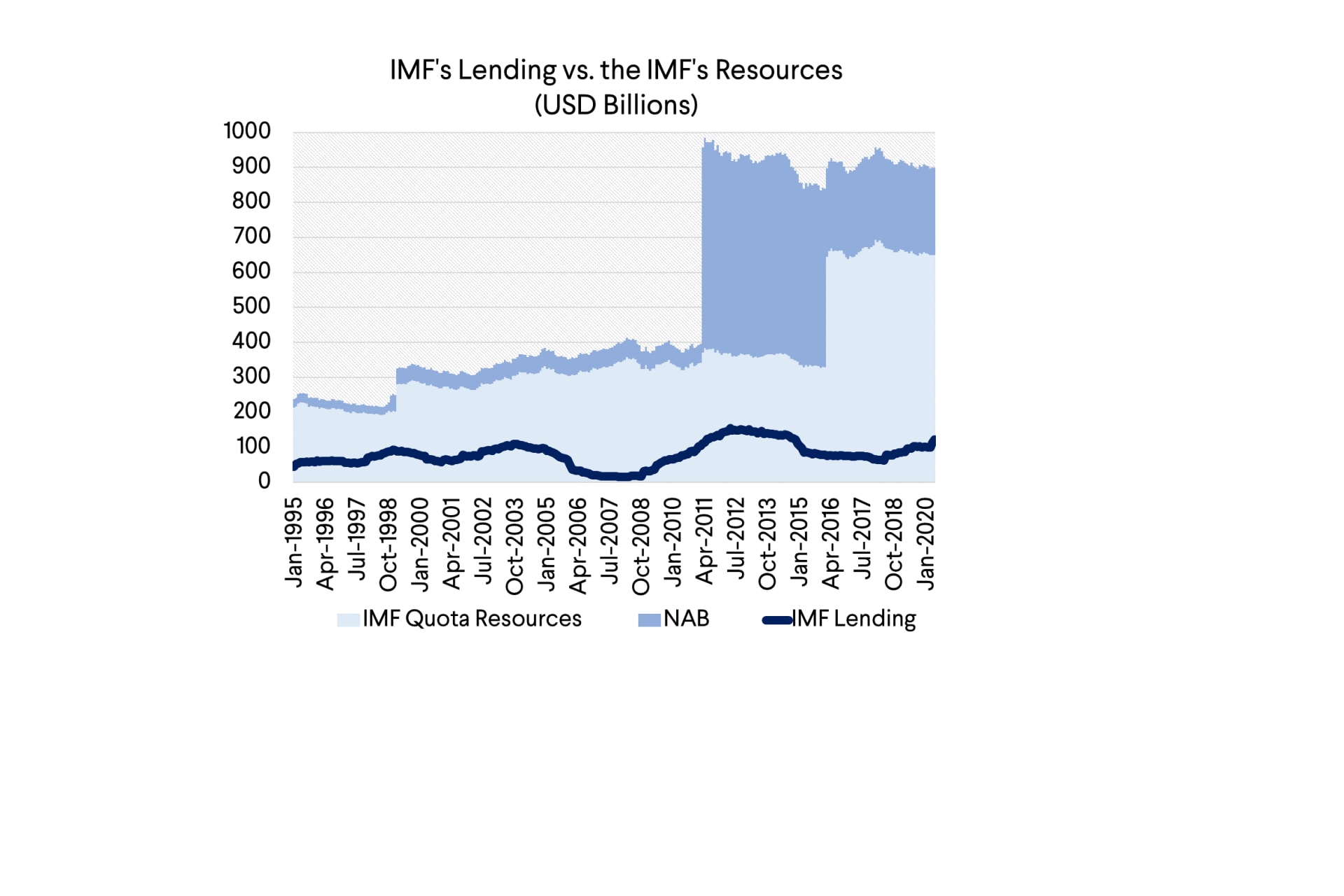

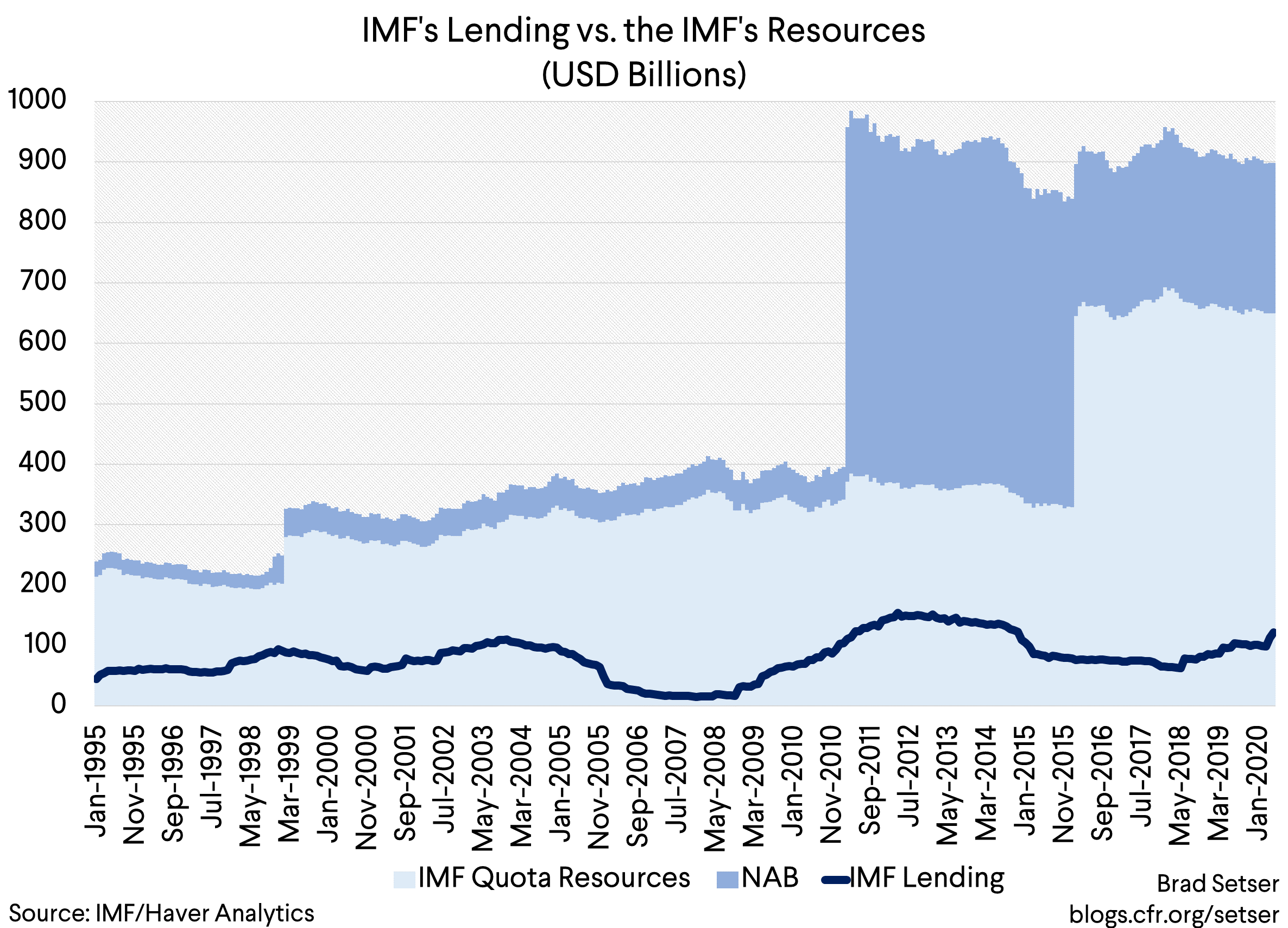

And so far at least, emerging economies haven’t gotten much direct financial help from the IMF. The IMF has $600 billion in quota resources, and another $600 billion in supplementary credit lines (the New Arrangement to Borrow (NAB), and the backup bilateral credit lines). That should be enough to support close to a trillion dollars in IMF lending, especially as the New Arrangement to Borrow is slated to double in size at the end of the year.

The IMF went into the shock with about $100 billion outstanding—and another $100 billion in standing commitments (backstop credit lines, including a large one with Mexico). So it had substantial financial capacity if it wanted to use it.

Right now, the IMF is set to disburse another $100 billion or so through its rapid financing instrument—including a Rapid Financing Instrument for South Africa, add maybe $50 billion in additional flexible credit line commitments (Chile and Peru have joined Mexico and Colombia) and do conventional programs for Egypt of a modest size. Lending has increased by about $20 billion to $120 billion since March, and credit commitments are now $130 billion (see the IMF’s weekly report). About $250 billion of its balance sheet has been formally tied up, and there is a bit more than another $50 billion in the pipeline.

But so far, that’s it.

Amid the biggest shock in at least a decade—and amid a shock that isn’t the responsibility of bad economic or financial decisions—the bulk of the IMF’s lending capacity is still sitting idle.

Now some of that balance sheet will eventually need to be deployed to support the weakest emerging economies—countries that have will have no option but to seek traditional and highly conditional IMF lending programs. Lebanon is in discussions with the Fund (see Bisat, Cassard, and Diwan). Argentina really needs to start talking to the Fund so it doesn’t have to rely on the BCRA to finance its response to the coronavirus. Turkey may need to turn to the IMF to make sure its central bank has the resources needed to pay back the foreign currency the Central Bank of the Republic of Turkey is now borrowing from Turkey’s domestic banks (net reserves, after adjusting for swaps, are now negative).

The Fund already has backstop facilities for countries with sterling policy reputations—the flexible credit line in particular (the short-term liquidity line provides less access than a flexible credit line with the same access criteria, so it isn’t obviously a good deal). But the criteria for accessing the flexible credit line are demanding (A sustainable external position, a track record of steady sovereign access to international capital markets at favorable terms, a relatively comfortable reserve position, sound public finances, including a sustainable public debt position, low and stable inflation, a sound financial system and the absence of solvency problems that may threaten systemic stability). it isn’t obvious that all the advanced economies would meet all of the criteria…

What is missing, to me at least, is a facility to help flawed but solvent countries manage the financial costs associated with a pandemic with significant amounts of financing (up to 300 percent of quota). Right now, the only option for funding beyond the 100 percent of quota provided by the rapid financing instrument is a traditional fund program with the standard conditionality.

Most countries don’t find that to be an attractive option.

Yet there are a number of flawed yet still solvent countries that could use a helping hand right now.

Maybe India ran too high a budget deficit in good times and hasn’t done enough to clean up its state banks. But its external balance sheet is clean—over $400 billion in reserves, and very little external public sector debt.

Maybe Indonesia should have held a few more reserves and done a bit more to reign its state banks. But with public debt of 30 percent of GDP, its public balance sheet isn’t overly extended.

Maybe Brazil should have moved toward primary fiscal balance much earlier (though it has been locked in a long-term recession since commodity prices slumped back in 2014). Its domestic fiscal balance sheet is clearly stretched. But thanks to the foreign exchange reserves built up by President Lula back in the early day of the commodity boom, Brazil’s government has more foreign currency assets (reserves) than foreign currency debts (even counting the foreign currency debt of Petrobras and BNDES) and thus its public sector solvency improves as the real weakens—helping to provide a bit of ballast to what otherwise would be a very unstable financial structure.

South Africa has a host of problems—not the least of which is the big state energy company that needs a deep restructuring (Eskom) and a stagnant economy. The increase in the primary fiscal deficit in 2019 was perhaps not wise. But with public debt to GDP of 60 percent and with $60 billion in reserves, it also isn’t heading toward default (foreign investors hold a lot of rand denominated bonds, which helps protect solvency).

Right now, all these countries have been more or less left on their own—without any substantial help from the IMF or a large increase in World Bank lending for budget support.

There is a fair debate if all should get help, or some should be forced into conditional fund programs. Lines are always hard to draw. But at a moment like now, I personally would err on the side of being slightly generous. Especially as the IMF is sitting on a large and currently largely unused balance sheet.

Ramin Toloui has suggested reworking the short-term liquidity line to make it more useful. Right now, it provides too little money (145 percent of quota) for too little time (a year) to too few countries (no one has applied). Ramin would raise the limit to 250 percent of quota, with access on a sliding scale—i.e., access would phase out, rather than there being a “bright line” for eligible versus non-eligible. Countries with prior average spreads of less than 100 basis points would be eligible to draw 250 percent of quota, with accessing phasing out so that countries with average credit spreads of 250 basis points would lose eligibility (details) . The lending terms of the “Systemic liquidity facility” would be available for a year at a fairly high rate though—with the expectation that countries would generally be able to re-access the markets before the line comes due.

I suggested going a bit further and creating what in effect would be Pandemic Support Fund for flawed but still solvent countries that won’t qualify for the kind of large-scale access possible with a flexible credit line (see my Foreign Affairs article).

Rather than providing short-term financing, I suggested providing cheap longer-term financing to help cover the financing needs associated with the pandemic this year—with the low cost meant to help assure long-term-term solvency, or at least not put it excessively at risk. The idea, basically, would be to give a broad set of emerging economies access to 300 percent or so of quota in cheap long-term funding—and put $250 billion or so of the IMF’s balance sheet to work to help exogenous shock. Yes, lending standards would drop a bit—but not permanently. This would take some of the strain off the balance sheet of the major emerging market central banks.**

Countries would lose eligibility if they already have sufficient resources of their own—say reserves over a third of GDP. The intent is not to allow countries like Saudi Arabia to borrow foreign exchange to buy global equity and add to their sovereign wealth funds but rather to help those countries that have no choice but to borrow to address the economic and budget shock from the pandemic.

A $500b SDR allocation would also help, as it would raise emerging economies’ reserves by $200 billion. Focusing on the limited resources that go to the very poorest misses the point in my view. There are a number of countries that could use larger reserves right now.

But some fraction of that would go to those emerging economies that already have substantial reserves so it isn’t enough on its own—hence the notion of a lending program designed around the specific fiscal and financial shock from the pandemic.

Debt relief can be the answer or at least a part of the answer for the poorest countries who don’t generally rely on market financing. But it cannot be the answer for the broader set of emerging economies that do participate in global capital markets and don’t want to jeopardize their access unless absolutely necessary.

But the broader point is simple: there needs to be a debate now about how the IMF could do more to help emerging economies cope with the financial costs of the pandemic. The Fund has $500 billion in spare balance sheet capacity, capacity that is likely never to be used absent some tinkering with the Fund’s programs and conditions.

If this isn’t the time to find creative ways to use it, then when is?

The United States should lead here—finding smart ways to use the existing multilateral institutions is a relatively low cost way for the United States to show it remains a leading player in the world, and to demonstrate that it still has the strength needed to offer others a helping hand and the vision to know when to extend one.

As I said at the end of my piece in Foreign Affairs: “This is a once-in-a-century pandemic that calls for a once-in-a-century response. The IMF has yet to deliver.”

----

* Emerging markets faced pressure from different sources in March. Some countries, like Korea, used their reserves to provide dollar funding to their own financial institutions. Once Korea had access to the Federal Reserve’s swap lines, it no longer needed to use its own reserves for this purpose and its reserves subsequently recovered. Others—notably Brazil and Indonesia—sold reserves to limit the pressure on their currency as foreign residents fled their local debt market. Others are drawing on their reserves to cover the impact of reduced oil export proceeds and the fall in tourism revenue.

** The fund can directly provide budget support—and it can support a central bank’s reserves while the central bank provides the financing. Say you don’t want to lend directly to the fiscal authorities. Have the central bank buy a ten-year local currency bond, and then offset the direct monetary expansion by selling some of its foreign exchange reserves. That transactions leaves the central bank’s balance sheet unchanged, but obviously reduces reserves. The fund then can backfill reserve levels with its lending (and the country would get the additional reserves far more cheaply than through market borrowing in foreign currency).

*** The Fed’s swap lines are often suggested as a solution but 90 day swaps aren’t really the way to provide budget support. The Fed’s swap lines aren’t also intended to fund currency intervention. They have been designed to allow counterparty central banks to provide dollar funding to their “home” financial institutions who are holding good dollar collateral (typically U.S. bonds). That is an important role—but it is also a narrow role. There are many other needs for dollar financing in the global economy that cannot really be met with 90 day money.