What Does Taiwan’s Hidden Forward Book Mean for Taiwan’s Financial Stability and U.S. Currency Policy?

Taiwan’s central bank—and Taiwanese households—have taken on an awful lot of foreign currency risk over the years …

By experts and staff

- Published

Brad W. SetserCFR ExpertWhitney Shepardson Senior Fellow

Brad W. SetserCFR ExpertWhitney Shepardson Senior Fellow- Guest Blogger for Brad Setser

This is the sixth post in a series* on Taiwan’s life insurers and their private & sovereign FX hedging counterparties. It’s the product of a collaboration with S.T.W**, a market participant and friend of the blog. Printable versions of entries in this series are available in pdf format on his site (Concentrated Ambiguity).

Part Six: Mercantilism, Excessive Private FX Risk-taking, & the Hedging Backstop

A. Putting the Pieces Together—The Case So Far

Taiwan is the only major economy which does not comply with the IMF’s standard for reserve disclosure, and thus effectively hides its FX derivatives book. Immediately after the global crisis, its central bank’s visible intervention accounted for the bulk of Taiwan’s current account surplus. But over the past years, visible intervention has been relatively small, as private financial institutions—notably Taiwan’s life insurers—have built up their foreign asset position.

Life insurers do not hedge all of the resulting foreign exchange exposure. But they do hedge about USD 250bn of their USD 465bn in foreign assets. The banking system appears to provide ~USD 60bn of the needed USD 250bn in hedges. Non-financial firms and global investors are a bit harder to track, but all evidence suggests each of these have provided less than USD 20bn of hedges. That leaves about USD 150bn of the life insurance sector’s hedging need unexplained.

The CBC has indicated in its annual reports that it is a regular participant in the FX swap market, and—like other central banks—it has sterilized FX interventions via the banking system. It has also reported that the root cause of the banks’ need for foreign exchange is often FX hedging demand by Taiwan’s large life insurance companies. The use of FX swaps would lower the CBC’s level of reported reserves (as the CBC provides foreign exchange to the financial system, while contractually committing to buy the foreign exchange back at a pre-determined price). That is why the disclosure of the forward leg of the swap in the IMF’s standard template for reserve disclosure is critical—it helps provide a guide to the central bank’s true foreign exchange position.

The CBC does not make it easy, but it does seem to report moves to estimate its true foreign exchange exposure. A well- grounded mid-point estimate suggests that the CBC’s undisclosed FX exposure—and thus undisclosed FX intervention—is USD 130bn, with a 90% confidence interval between USD 60bn and USD 200bn.

B. Effects on U.S. treasury’s Currency Policy

The CBC, like many other central banks, claims its interactions with FX markets are ’smoothing’ in nature “when seasonal or irregular factors disrupt the market, the CBC will step in to maintain an orderly foreign exchange market”[1]. Alas it is difficult to square the CBC’s actual actions in the FX markets with this description. The CBC’s intervention is one-sided and large both absolutely and relative to the size of Taiwan’s economy and persistent.

The CBC has added USD 118bn to its reported FX reserves since 2009. This reported number is deceptive however as it leaves out the central bank’s derivative exposures. That has been estimated to have increased by USD 130bn since 2009, or 20% of Taiwan’s GDP.

The higher level—and different trajectory—of Taiwan’s foreign exchange interventions of course has important implications for the U.S. Treasury Department’s biannual report to Congress[2]. In its current format, the FX report requires all larger U.S. trading partners’ trade and FX activities to be reviewed against three specific criteria.

- A material overall Current Account surplus, with two percent of GDP set as threshold.

- A significant bilateral trade surplus vis-a`-vis the U.S., with an annual threshold set at USD 20bn.

- Persistent, one-sided purchases of foreign currencies in FX markets, defined as net FX intervention purchases of at a minimum two percent of GDP per annum and in at least 6 of the 12 preceding months.

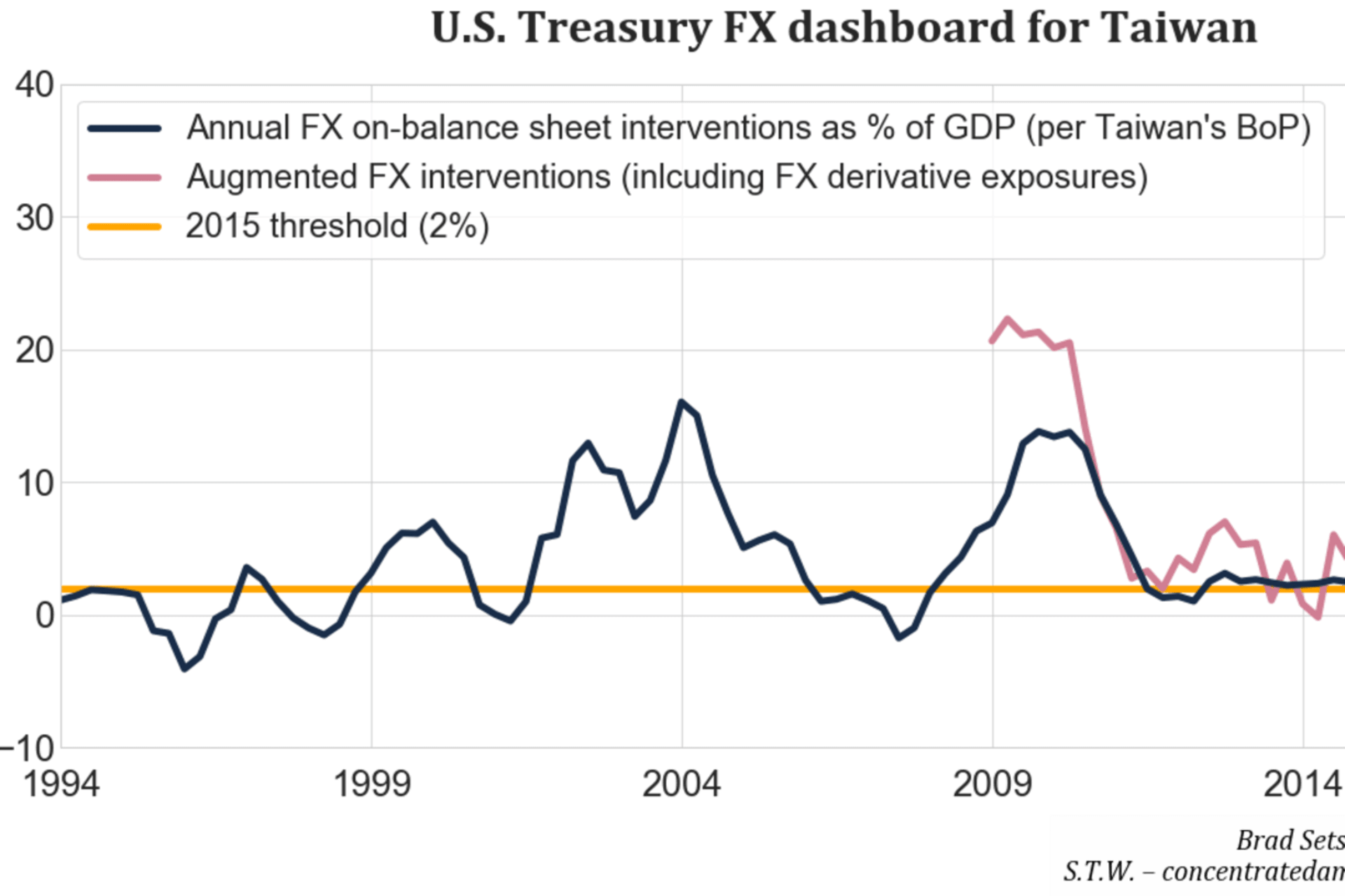

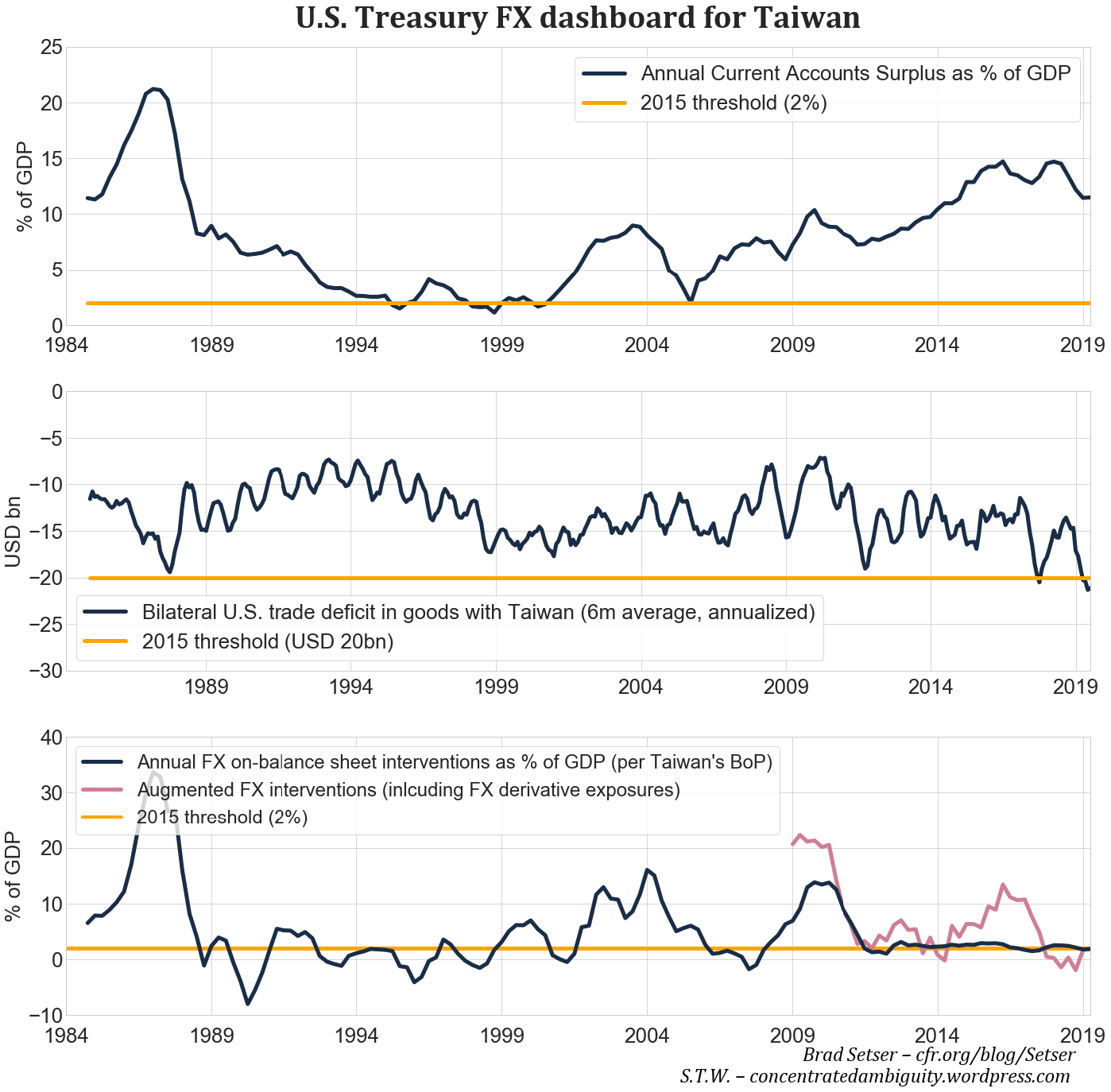

Fig. 1 shows the Treasury’s FX evaluation dash board for Taiwan.

Taiwan’s Current Account surplus has exceeded the two percent threshold in all but a few months since 1984. In the last six years it has been north of 10% of GDP.

The bilateral balance is not the most intellectually well grounded criteria—some, including one of the authors, have suggested that it should be deemphasized by the U.S. Treasury[3]. Taiwan has recently avoided scrutiny in the Treasury’s FX report in part because the U.S. bilateral deficit with Taiwan has not been close to the USD 20bn threshold (even if it likely would on alternative measures[4]). But Taiwan is in a bit of a bind, as trade diversions away from China subsequent to the imposition of tariffs could easily push the bilateral deficit above the USD 20bn threshold.

The third criterion is FX interventions by a country’s central bank. Treasury nets out interest income from reserve growth to estimate currency interventions, but it also includes interventions via FX derivative markets. In the absence of any disclosure by Taiwan of its derivative position, Treasury has so far measured Taiwan’s FX intervention by looking at the growth of reported foreign assets on the CBC’s balance sheet.

The blue line in the third panel shows Taiwan’s rolling annual reserve growth as reported in Taiwan’s Balance of Payments statistics. Three major intervention periods stand out, in the mid-1980s, early 2000s and after the financial crisis in 2009/10. Since late, the growth of Taiwan’s reserves has hovered around the threshold of two percent of GDP, with a suspicious lack of volatility.

Utilizing the insights gained around the CBC’s FX derivative interventions in prior parts of this series, it is possible to provide a more accurate picture of the CBC’s total FX interventions. Starting in 2009, the time when lifers accelerated their overseas bond purchases, the pink line adds an estimate[5] of the CBC’s derivative intervention to the blue regular FX reserve acquisitions. On this enhanced measure, Taiwan’s FX intervention clearly exceeded the two percent threshold between 2014-2018. In addition, its interventions in the immediate post-crisis period in 2009 seem to have been even larger than commonly assumed.

During 2018, the enhanced measure came in below the official FX reserve figure as lifers, policy holders and depositors each assumed more FX risk themselves—though the latest available data again suggests that intervention has exceeded reported FX reserve growth.

Taiwan’s central bank is likely to challenge this analysis. But it could settle the matter through complete disclosure of its historical derivatives position using the IMF’s IRFCL standard—something the U.S. Treasury has long called for. Absent such disclosure, the Treasury should develop the analytical capabilities needed to independently estimate Taiwan’s actual action in the market.

C. Financial Stability Risks from Excessive Private Sector FX Exposures

Traditionally, households and financial institutions that provide vehicles to safely invest for retirement are cautious about assuming meaningful amounts of FX risk. FX risk is, after all, much harder to control than regular fixed income exposures. Yet if risks associated with outright currency exposures never materialize to any larger degree, even cautious actors may start to take large FX risks.

Intentionally or unintentionally, the CBC’s actions have inspired outright private sector FX risk taking and the partial dollarization of such institutions’ balance sheets, especially in recent years. With U.S. interest rates above Taiwanese interest rates, in the absence of currency volatility, or more precisely the risk of TWD appreciation against USD, Taiwanese actors should logically increase their allocations to USD-denominated assets.

This is exactly what appears to have happened through at least three channels:

- Taiwanese corporations and households shifted their cash holdings into (mostly domestically-held) USD deposits.

- Taiwanese households acquired USD-denominated poli- cies, directly taking currency risk.

- Taiwan’s lifers themselves assuming larger open net FX positions.

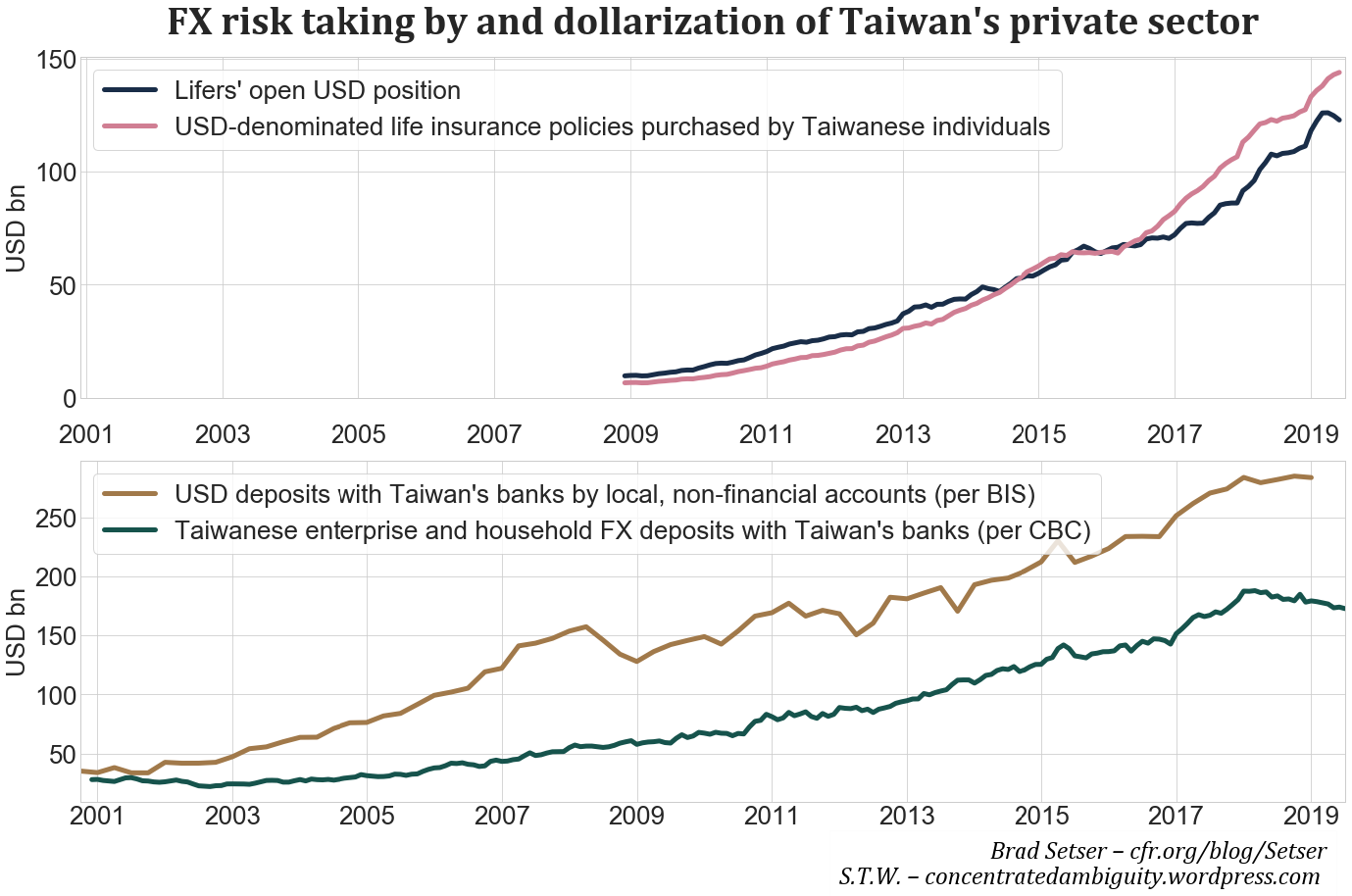

Fig. 2 quantifies the degree of FX risk taking by each of these.

USD deposits held with Taiwan’s banking system grew, depending on the source, by USD 150bn or USD 106bn. FX risks taken by households via FX denominated life insurance policies grew from practically zero in 2008 to USD 140bn. The life insurers’ own open FX position increased to USD 120bn as of mid-2019. Altogether, these actors currently house FX risk of almost USD 500bn, 80% of which was accumulated this cycle. These actors, even more than the CBC directly, kept TWD from appreciating against USD.

How such large FX risk taking by typically conservative institutions in a clearly undervalued currency will evolve going forward is obviously of great interest from a financial stability perspective.

The macro implications seem twofold:

- Had the CBC not intervened by at least USD 130bn[6] in FX markets via its swap book, TWD would likely have appreciated and safety-oriented private sector actors in Taiwan would have been much less likely to assume long USD positions. Pondering counterfactuals might not always be helpful, yet in a world in which the CBC had not intervened sizeably, a USD/TWD exchange rate in the mid 20s would not surprise.

- In the event of meaningful FX losses, cutting USD positions by purchasing TWD is probable[7]. Then, the one-way street into USD would reverse and push TWD upwards, reflexively inflicting further losses on others while seriously hampering the ability of banks to provide the current quantity of hedges to life insurance companies[8]. Unless the CBC steps in meaningfully at such a point, a swift revaluation of TWD would be likely.

Given that Taiwan still maintains a large trade surplus[9], the CBC appears to have itself boxed in and has, at least implicitly, written a put on USD/TWD, keeping TWD weak to shield its private sector from FX losses. For most actors, this put is merely implicit: “TWD has not appreciated in the past so why should it in the future; let’s buy USD”.

For life insurance companies themselves, this put might actually be rather explicit. In a relatively closed system as Taiwan, the major actors on the demand and supply side typically know each other fairly well. This is especially the case for lifers owned by a financial holding company also operating a banking subsidiary. This would apply to three of Taiwan’s four largest insurers: Cathay, Fubon and Shin Kong. While conjecture for now, this is exactly the framework the Bank of Korea[10] used to provide FX hedges under in a similar situation.

If lifers know the CBC is the ultimate counterparty to the majority of their current FX hedges and know that it will likely continue to be so in the future, it is much easier to run larger open FX positions. In case of difficulties, the CBC would, after all, be ready and provide additional FX hedges at reasonable rates. Switching perspectives, if the CBC knows lifers are unlikely to unwind open FX positions at the first sign of trouble, Taiwan’s authorities can be much more lenient in their regulation of FX exposures. Currently, this is most relevant for the regulation of FX exposures lifers acquire via domestically-listed bond ETFs acquiring foreign bonds FX-unhedged.

Any attempt to scale these risks suggests they are big: Lifers in aggregate currently hold ~65% of assets in foreign bonds, of which 22% is FX unhedged. This implies long USD exposures worth USD 123bn, or 14.3% of assets. Against that, lifers hold capital of USD 50bn, or 5.5% of assets. In a static environment without hedge adjustments, a 10% increase in TWD/USD thus inflicts losses of USD 12.3bn, or 22% of stated capital, on lifers. Larger moves are of course possible.

D. Effects of Providing FX Hedging Services to Life Insurers

A final effect of the CBC’s FX interventions via FX swaps concerns the pricing of TWD cross-currency basis markets. In a textbook setting, forward FX markets[11] would be only set by USD-TWD interest rate differentials, giving rise to the academically revered no-arbitrage condition. In such a state, the excess return a Taiwanese insurer would earn over TWD risk-free rates by investments abroad would only be affected by its return on duration and credit risk taken in USD markets.

In the post-crisis environment, however, deviations of the cross-currency basis from zero are not uncommon, even in developed markets. For countries with large historical cumulative Current Account surpluses and subsequent large positive Net International Investment positions, the X-CCY basis is usually negative, increasing the cost for locals acquiring foreign assets in an FX-hedged manner. In Taiwan, both the onshore and offshore X-CCY basis were deeply below zero – persistently for the former and on average even more so for the latter, but also more volatile[12]—for virtually their entire history.

As it looks likely that the CBC is the prime supplier of FX hedges to domestic life insurers, the CBC is effectively the lead price setter of TWD X-CCY basis markets, thus indirectly affecting the economics Taiwan’s life insurers face when considering whether to acquire FX-hedged USD- denominated debt.

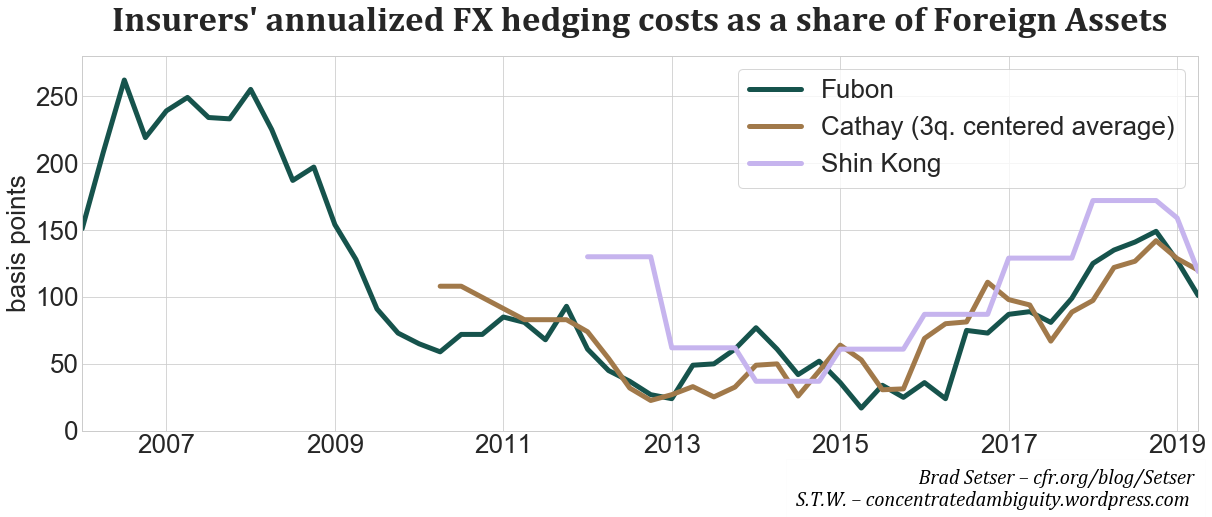

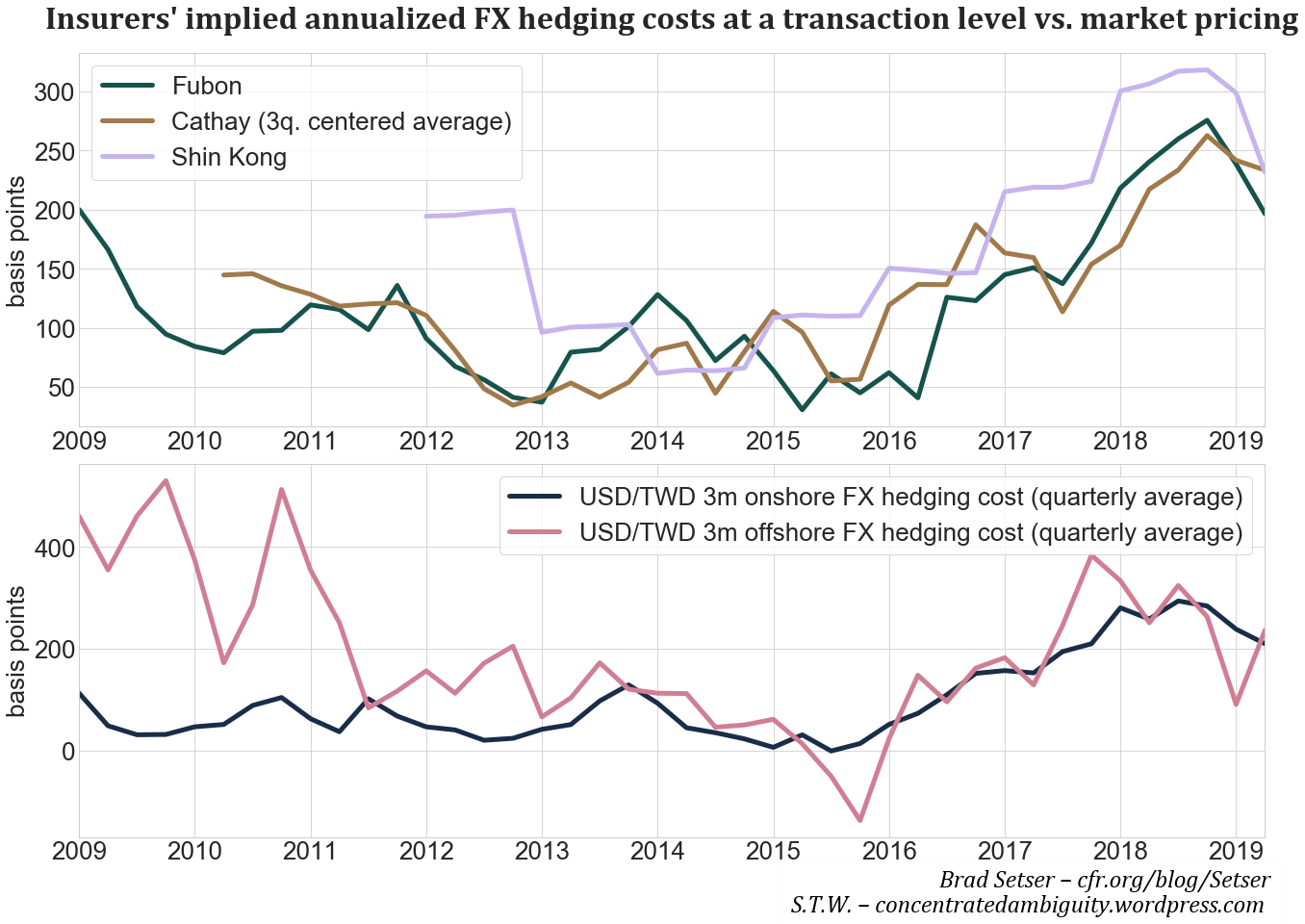

One way to understand how the CBC is shaping the pricing in FX hedging markets is to closely look at insurers’ disclosed hedging costs. Cathay, Fubon and Shin Kong, all of which disclose their annualized FX hedging costs as a share of total foreign assets, are shown in Fig. 3.

In order to infer the actual pricing of the hedges, these values have to be adjusted for foreign assets not hedged in derivative markets by insurers, i.e. their open USD position and FX policies sold[13]. Results are shown in the upper panel of Fig. 4, with average quarterly FX hedging costs at the 3m tenor for USD/TWD as quoted in markets shown in the bottom panel.

The lifers’ hedging costs are fairly obviously[14] in line with quotes from markets. The Federal Reserve’s interest rate increases since 2015 are clearly visible as they changed the interest rate differentials and thus increased FX hedging costs. Some insurers, in this sample Shin Kong most notably, rely more on the offshore market and thus their hedging costs are linked to the more volatile offshore X-CCY basis.

A hasty look might suggest not much can be learned from the developments shown in Fig. 4 Insurers simply pay market rates on their hedges. But the definition of a market price in this context is not as straight-forward as it may appear. If the CBC always provides lifers FX hedges at market rates and such transactions constitute the dominant trade in a market, the market price is not created by the intersection of the entire demand and supply curves, but just the portion which does not have any CBC involvement.

Hypothetically, assume a case in which current demand for FX hedges is USD 100bn (of which lifers represent USD 80bn), while the supply side is also USD 100bn, of which the CBC provides USD 80bn. If the CBC-lifer transaction (intermediated by banks) is done at, say, yesterday’s market price, today’s price is the clearing price of the USD 20bn transactions done without central bank involvement. In this setting, the pricing pressure exerted by the net USD 80bn private sector imbalance towards acquiring FX hedges is entirely neutralized by the central bank offering trades at ’market rates’. If the USD 80bn provided by the central bank were removed, the market would still clear—but at a different price, and likely at a different volume level.

TWD X-CCY basis markets have traded deeply in negative territory almost the entire time since the early 2000s, imposing on average an extra cost of 100 and 200bps on insures hedging FX risk at the 3m tenor in onshore and offshore markets respectively. This has been among the reasons why insurers seek to either sell more USD-denominated policies or assume FX risk themselves. If the CBC did not backstop the TWD- XCCY basis markets by providing FX hedges at ’market rates’, the cost of hedges for lifers would likely be much higher. In such a world, it is likely that lifers’ business model of channeling domestic savings into overseas fixed income markets, a large portion on an FX-hedged basis, would be untenable.

Just as there are cases where it can make sense for a central bank to intervene, at times, in the spot market, it can also make sense for a central bank to provide cheap FX hedging services to domestic institutions, especially in cases where the central bank has large FX reserves and can do so easily. What seems special in this case is the CBC’s lack of transparency.

A final hypothetical consideration is at what levels X-CCY basis markets would clear if the CBC retreated from its FX swap provision to lifers. Following the thinking in chapter IV., the foreign sector and domestic financial institutions would be expected to step up their provisions of FX hedges. The latter would likely require much deeper basis values to substantially step up arbitrage activities, simply because pure arbitrage is inefficient from a balance sheet perspective. So, as in other markets, foreigners would have to fill the gap. But Taiwan’s current regulations on foreigners’ activity in Taiwanese fixed income and money markets makes this virtually impossible today.

Per FSC regulations, “The total amount invested by an offshore overseas Chinese or foreign national in government bonds, corporate bonds, financial bonds, money market instruments, and money market funds [...] must not exceed 30 percent of the net inward remittance”[15]. Since foreign arbitrageurs necessarily need to secure safe TWD collateral to carry as an offset to the long USD position in the forward FX market, such regulation effectively makes arbitrage activities, as done in Europe or Japan, impossible. Given Taiwan institutions’ large requirements for FX hedges, relaxing regulations on foreigners in this area might be worth considering.

E. Conclusion

Taiwan’s central bank has been a much larger player in the foreign exchange market—and in the domestic market for providing foreign exchange swaps to Taiwan’s lifers—than is apparent from looking at the modest growth in Taiwan’s headline reserves. Its actions have likely been a key reason why Taiwan’s dollar has remained so weak, and why Taiwan’s household and financial sector have taken on so much currency risk. Taiwan, rather uniquely, has dug itself into a financial hole not by borrowing too much in foreign currency, but by investing too much of its national savings abroad – and thus leaving its population exposed to financial losses when its currency inevitably appreciates. Taiwan needs to address these financial vulnerabilities before they become even bigger, and take the needed steps to develop a new economic and financial model, one that does not balance through the accumulation of ever larger foreign exchange positions among Taiwan’s households and at its central bank. Meeting international disclosure standards for its reserves is a first step in this necessary, though difficult, transformation.

* The Council on Foreign Relations takes no institutional positions on policy issues and has no affiliation with the U.S. government. All views expressed on its website are the sole responsibility of the author or authors. The Council on Foreign Relations takes no institutional positions on policy issues and has no affiliation with the U.S. government. All views expressed on its website are the sole responsibility of the author or authors.

** Contact at [email protected]

[1] Quoted from the CBC’s explanation of its Foreign Exchange regime here.

[2] Established by the Omnibus Trade and Competitiveness Act of 1988, 22 U.S.C. § 5305, and Section 701 of the Trade Facilitation and Trade Enforcement Act of 2015, 19 U.S.C. § 4421.

[3] Setser, B, 2019, ’Make the Foreign Exchange Report Great Again’, Council on Foreign Relations

[4] An important ongoing economic discussion is how accurately bilateral tradestatistics reflect two countries’ trade links. For instance, Taiwan’s direct exports to the U.S. are quite small, but it delivers significant amounts of intermediate stage products to China, where final assembly frequently occurs. If China then exports the finished products to the U.S., it records the entire export as its own, even though meaningful amounts of the value added in its export content is attributable to Taiwan. Global input-output tables, while available less frequently, could help in determining the actual value added bilateral position of two economies. In such a valued added based framework, Taiwan’s surplus with the U.S. is likely to exceed the directly measured values currently relied upon.

[5] This estimate combines the direct and indirect approach to figuring out the CBC’s FX derivative exposures. The detailed examination in blog 5 of this series is the best evidence that the CBC is intervening and its size, as well as the uncertainty in that estimate. Since it is however also known that the CBC acts as counterparty to lifers, the specific time-wise allocation of CBC interventions is better approached indirectly, taking lifers overall FX hedges and subtracting known (or estimated) exposures by the institutions discussed in part 4. The estimate depicted takes its ultimate size in mid-2019 from chapter V., while the allocation per quarter follows the indirect method.

[6] USD 130bn is the mid-point of the modeling efforts in the prior chapter and the confidence intervals around it were discussed as well. One simple, indirect way to further evaluate where the actual exposures likely lie within the confidence band is to subtract all known FX derivative exposures established in part four from lifers USD 250bn FX hedging demands calculated in chapter II. In mid-2018, Taiwanese banks provided USD 65bn of hedges, while the foreign sector and non-financial Taiwanese firms provided (in a very generous reading of the data) ~USD 15bn each. This leaves USD 145bn to be allocated to remaining counterparties (i.e. the CBC) and is USD 20bn higher than the mid-point estimate.

[7] For lifers’ open FX position and USD deposit holders, such a shift in FX exposures is straightforward. In contrast, ’redenomination’ of USD- denominated policies into local currency would typically be expected to be more cumbersome. In Taiwan, where insurance policies are frequently marketed as shorter-term wealth management products (anecdotally, only ~50% of policy purchases are affected due to the provided safety features), minimum surrender periods and surrender charges are however insignificant, enabling policy holders to quickly alter FX exposures should they wish.

[8] Taiwanese banks used most of the increase in domestic USD deposits from 2016-2018 (see Fig. 47) to provide FX hedges to lifers. This is visible on the asset side of their balance sheet, where USD assets did not see a commensurate rise. Instead, TWD assets increased, while their net FX position, per CBC data, remained unchained. As shown in Fig. 8 (part 4), this implies an increasing long USD position via derivatives, i.e. the counterposition to lifers’ FX hedges. Should households and corporates pull USD deposits and convert into TWD, banks would have to close FX hedges written to lifers to stay FX neutral, unless they can source USD funds elsewhere. Given the sizes involved, this appears unlikely and, if done in wholesale markets or via USD bonds issuance, unprofitable.

[9] Even despite unfavorable pricing trends in semiconductor industries in 2018 and 2019.

[10] See Sangdai Ryoo & Taeyong Kwon & Hyejin Lee, 2013 ’Foreign exchange market developments and intervention in Korea’, Bank for International Settlements. From page six: “As to the intervention tools used, direct interventions in both the spot and swap markets have been employed. Which instrument the authorities choose depends upon the objective of the intervention. [...] The Korean FX authorities do not publicly disclose any information related to intervention, because we believe that such information could stimulate speculative trading in the FX market. We thus intervene in the market through agents selected from among major banks. The Bank of Korea imposes a confidentiality requirement on these agent banks to maintain secrecy concerning intervention. As for the criteria used to select the agent banks, priority is given to institutions with the following characteristics: no danger of default risk, ability to provide the Bank of Korea with instant market information, and active role in the market.”

[11] A broad definition of the ’forward market’ is assumed here, i.e. including FX swaps and CCS. These are, as outlined in part three just regular FX forwards paired with spot transactions and entered with a common counterparty.

[12] The higher volatility of the offshore basis is mostly attributable to the lower liquidity of NDF markets and the higher share of speculative foreign actors present than in onshore FX markets, which require prior confirmation by Taiwan’s authorities.

[13] In practice, this means dividing the stated annualized FX hedging costs for foreign assets by the ’share of foreign assets hedged via FX derivatives’. Information on the latter will be taken from Fig. 12 in part two of this series, which will be uniformly applied to all three insurers.

[14] They are lagging the actual quotes slightly since the market prices are for future instead of past hedges, as well as occasional use of longer tenors by insurers.

[15] From the FSC’s ’A Brief History of Liberalization on Foreign Portfolio Investment’.