What Exactly is in the New Agreement Between Puerto Rico’s Board and its Creditors?

How much tax supported debt will Puerto Rico be left with if the Board’s most recent proposal is accepted by the courts?

Puerto Rico has reached agreement with a large portion of its general obligation bond holders—and the holders of the constitutionally protected “Puerto Rico Building Authority bonds.”

But the announcement of the agreement was confusing—the Oversight Board prioritized salesmanship over clarity.

There are two key things to realize about this deal:

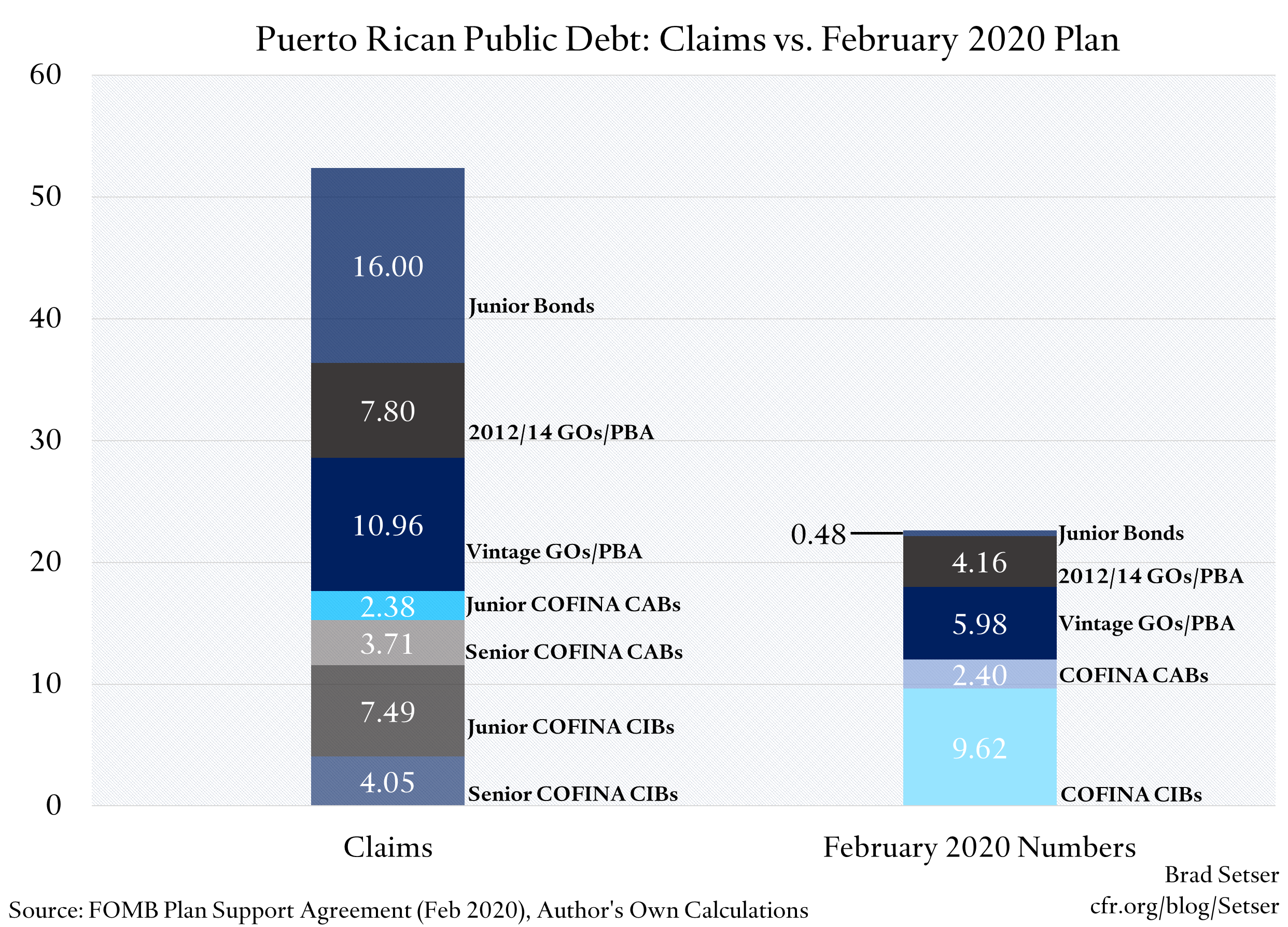

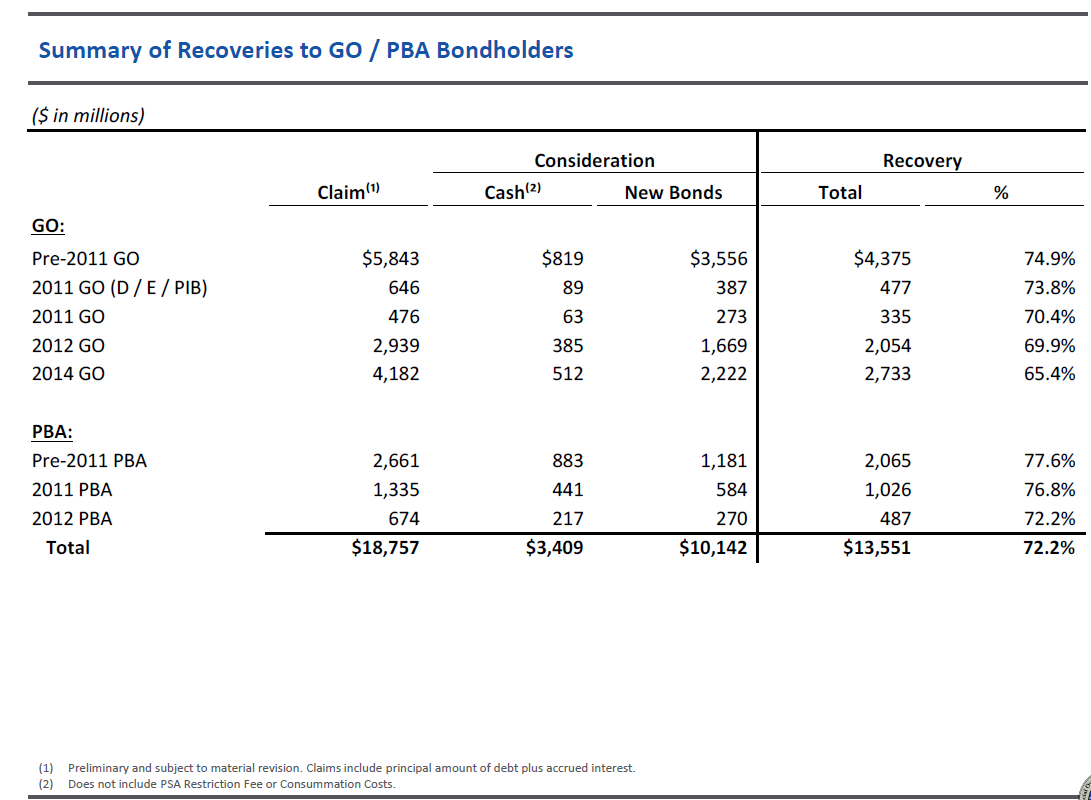

First, the General Obligation (GO) bonds (which have priority under Puerto Rico’s Constitution, and special status under PROMESA) are only a portion of the $35 billion in debt covered by the commonwealth plan of adjustment. The GO and PBA bond holders have $18.6 bn in claims (the total is higher than the old bonds‘ face value thanks to accrued interest), and those creditors that are party to the agreement have accepted haircuts of around 27 cents on the dollar on average relative to their claim. The GO and PBA bond holders did agree to accept $10 billion or so in new bonds for $18 billion in claims—but only because they are also getting $3.4 billion in cash. The bulk of the $24 billion in debt reduction that the board highlighted is thus coming from the proposed 97 cent haircut on the $16 bn in junior claims of the commonwealth, and those creditors clearly haven’t agreed to these terms. Basically, the announced deal slightly sweetened the terms for the GO bonds, at the expense of the more junior claims.

Second, the GOs and the more junior claims on the commonwealth (the pension bonds, the clawed back bonds including the clawed back Highway bonds, the PFC bonds, and the GDB’s legacy loans to the commonwealth) only constitute a portion of the Commonwealth’s tax supported debt. When assessing overall debt sustainability, the sales tax backed bonds (COFINA)—which have already been restructured—need to be added to the total. That changes the overall picture a bit—total claims on the commonwealth’s taxes pre-restructuring totaled a bit over $50 billion. If the proposed terms are accepted without further modification, they will be settled for around $23 billion in new bonds and something like $5 bn in cash (including the cash paid on the COFINA bonds as part of that settlement, see schedule 2 here).

Puerto Rico’s public sector debt is confusing. Which in turn makes the proposed restructuring confusing.

But the public sector debt can broadly be divided into four buckets:

- The sales tax backed bonds (COFINA). These are claims on Puerto Rico’s tax revenue, but were kept (intentionally) off budget and were restructured separately from the other tax supported debts.

- The General Obligation debt together with the Puerto Rico Building Authority (PBA) debt, which have “constitutional” guarantees. These claims ($18.4 billion now) had special status under Puerto Rico’s law, and the PROMESA required that the Federal courts “respect” this status. The board originally proposed splitting the constitutional debt into two buckets—legacy bonds whose constitutional status was unchallenged, and post 2012 bonds who arguably were issued when Puerto Rico already had more debt than allowed and thus shouldn’t have been accorded constitutional status, but as part of the latest deal the board dropped this challenge. These bonds are also obviously supported out of Puerto Rico’s tax revenues.

- The other claims on the commonwealth—which generally are legally junior to the constitutional debt and lack any revenue pledge (unlike COFINA). The junior unsecured claims ($16b) would essentially be zeroed out (the board reserved a bit under $500 million in new bonds to settle these claims) if the court approves the Plan of Adjustment.

- The debt of the public utilities. The debt of the Water authority (PRASA) is essentially being paid. The debt of the hugely troubled electrical authority is still subject to debate—the board has approved a restructuring plan, but Puerto Rico hasn’t agreed to the pricing structure required for the bond restructuring. This debt isn’t tax supported debt.

The board’s announcement covered the middle two groups of claims—but the emphasis was (for fairly obvious reasons) on the deal with the GOs/PBA bonds, not on the reduced offer for the more junior debts.

In order to secure the agreement of a broad set of holders of the GO bonds, the Board made a set of modest concessions:

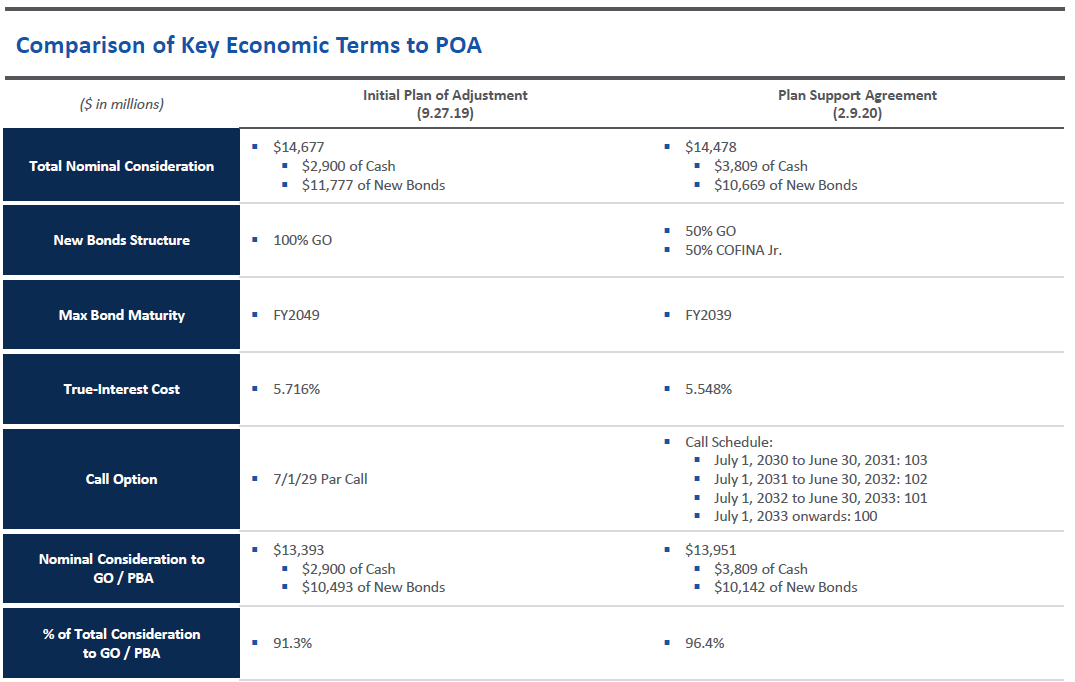

- The board increased the total “consideration” (cash and new bonds) going to this set of creditors from $13.4 billion to $13.95 billion.

- The board raised the cash component of the deal (which is valuable if the new bonds are expected to trade below par)

- The board allowed the general obligation bonds to trade “up” into bonds backed by a security interest, at least in part. 50 percent of the new bonds will be backed by a sales tax pledge (they will be junior to the “New” COFINA bonds)

- The maturity structure of the new bonds was shortened—they will be paid ahead of some of the “New” COFINA bonds. The new GOs have a coupon of around 6 percent (seems high to me given where highly rated municipal bonds are trading, but that’s the deal) and the new COFINA bonds a coupon of around 5 percent (see p. 112 of the agreement for payment terms)

And to keep the sweetened offer to the general obligation bonds from raising new questions about overall debt sustainability, the board reduced the proposed offer on the more junior commonwealth claims. The “consideration” left for other claims fell to 3.6 percent of the overall offer.

This raises two questions:

Can the board succeed at cramming down these terms on the junior creditors of the commonwealth? The Pension (ERS) bonds and the holders of the clawed back Highway bonds (the clawback makes the bonds largely unsecured) are unlikely to vote to accept these terms, so final approval of the overall deal will require that the courts impose the terms on the more junior bonds (using the “cramdown” features in Title III that were imported from Chapter 9). To be sure, the recovery on these bonds was always going to be low. But now it is really low—so there is a risk that the court could demand that the Board improve its offer.

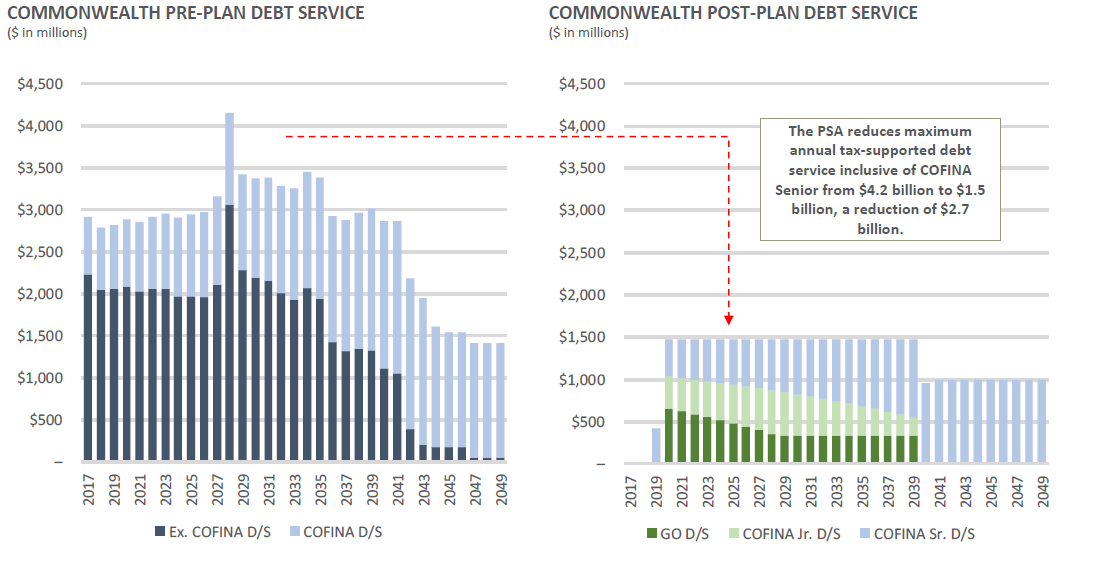

And does the deal leave Puerto Rico with a sustainable level of debt? The board has noted that raising the cash component of the deal means that fewer new bonds will be issued. That’s true, but the amount that Puerto Rico will be paying over the next twenty years won’t change (it is still a relatively high $1.5 billion a year) and since more of the new bonds will be secured (by the broader sales tax pledge), the new debt structure will be harder to restructure again.

The big picture though remains broadly unchanged—

Even with the debt reduction that has been proposed, Puerto Rico will be left with a relatively high level of debt.

Mississippi, which has a similar population to Puerto Rico and a somewhat larger economy, has between $4-5 billion in tax supported debt, around $500 million in annual debt service and around $6 billion in revenue. Puerto Rico thus will be left with roughly five times the debt of Mississippi, and three times more annual debt service.

After the proposed restructuring, debt per capita (over $7000) will still be far higher than any other state. Debt service to own revenue will be under the most indebted states. But that’s largely because Puerto Rico’s revenues are unusually high not because the debt service that emerged from the restructuring is particularly low.*

Yet the old debt stock was unambiguously unsustainable—relative to what was there before, this is an improvement.

And clarity on the debt service path would allow the board to focus on using the revenue windfall from federal spending to raise public investment—and making sure that already authorized federal aid actually flows to Puerto Rico.

* Puerto Rico’s revenues are above what would be expected for a low-income state thanks largely to the roughly $3 billion in tax revenue collected from multinationals operating in Puerto Rico because Puerto Rico falls outside the scope of U.S. corporate income tax. The Board has also adopted a broad measure of “own” revenue. The coupon on Puerto Rico’s new debt equally will be relatively high, so the new bonds are designed to trade above par if Puerto Rico’s economy normalizes.